Veeco launches Lumina+ MOCVD system, receives Rocket Lab order

Introduction & Market Context

Rizal Commercial Banking Corporation (RCBC) presented its first half 2025 financial results during an analyst briefing on August 7, 2025, highlighting a 20.2% year-over-year increase in net income to P5.3 billion. The bank’s performance comes amid a moderating Philippine economic growth forecast of 5.5%-6.0% for 2025 and expectations of monetary policy easing from both the Bangko Sentral ng Pilipinas (BSP) and the U.S. Federal Reserve.

The bank’s presentation highlighted how consumer lending has become a key growth driver, with the segment expanding 38% compared to the industry average of 18%. This growth occurred as the Philippine Stock Exchange Index (PSEi) traded around 6,321, with market sentiment improving following a U.S.-Philippines trade deal signed in July 2025.

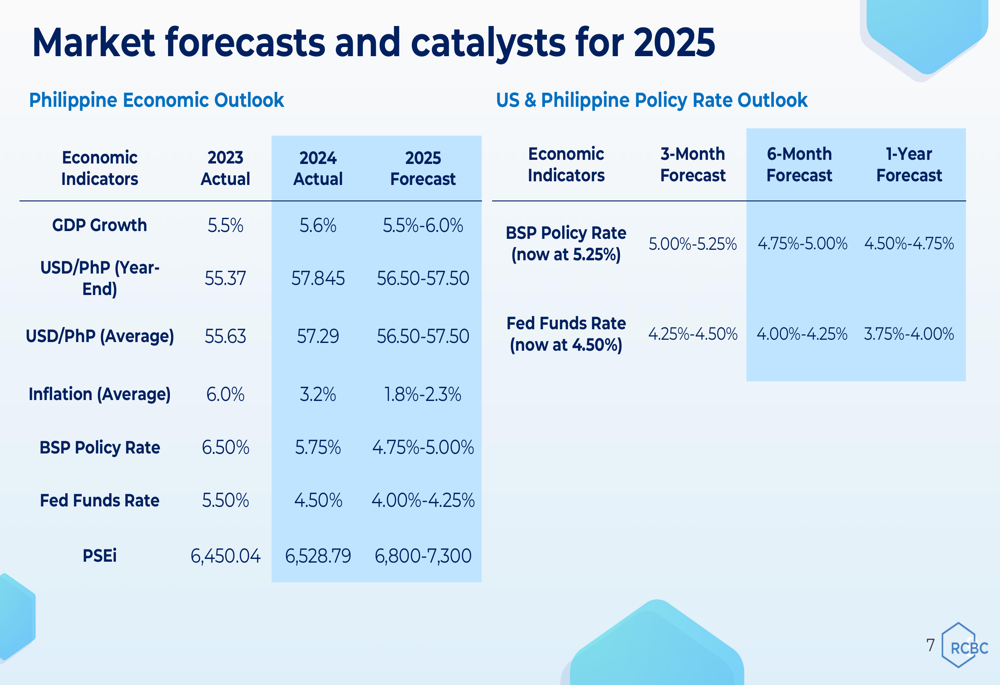

As shown in the following economic outlook chart, RCBC expects the BSP policy rate to decrease from its current 5.25% to between 4.75%-5.00% within six months, while the Fed Funds Rate is projected to drop from 4.50% to 4.00%-4.25% in the same period:

Executive Summary

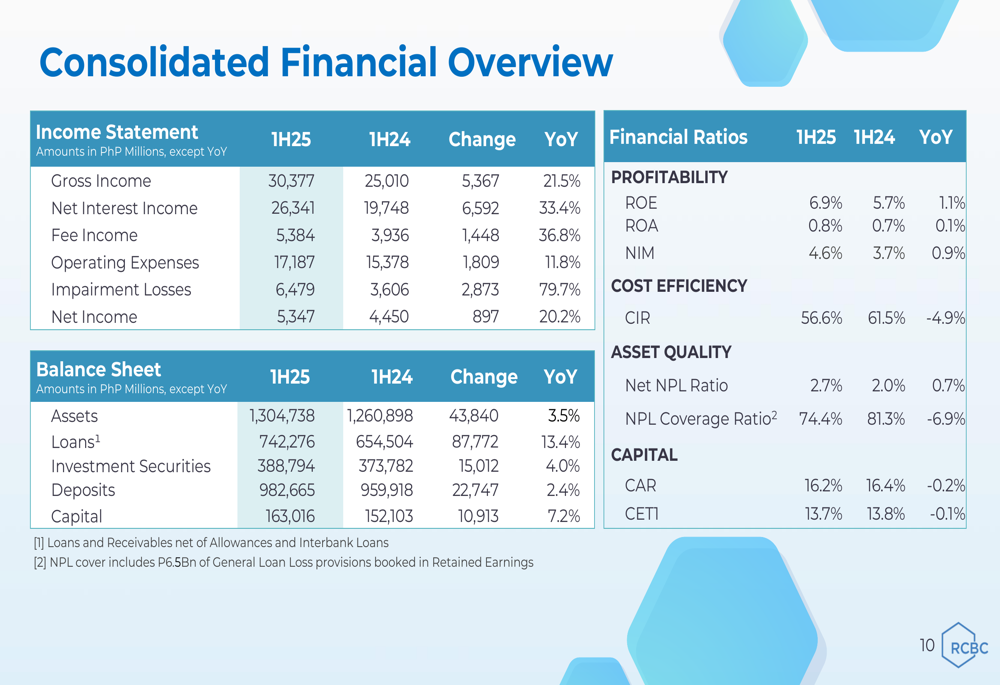

RCBC’s first half performance was characterized by robust growth across key metrics, with gross income surging 21.5% year-over-year to P30.4 billion. The bank maintained a strong capital position with a Common Equity Tier 1 (CET1) ratio of 13.7% and Capital Adequacy Ratio (CAR) of 16.2%, while total assets reached P1.3 trillion.

The following highlights chart summarizes RCBC’s key achievements for the first half of 2025:

The bank’s consolidated financial overview reveals significant improvements in profitability metrics, with Return on Equity (ROE) increasing to 6.9% from 5.7% a year earlier. Net Interest Margin (NIM) showed substantial improvement, reaching 4.6% compared to 3.7% in the same period last year. However, the presentation also acknowledged challenges in the SME portfolio, which contributed to an increase in the bank’s overall non-performing loan (NPL) ratio.

The detailed financial performance is illustrated in the following consolidated overview:

Detailed Financial Analysis

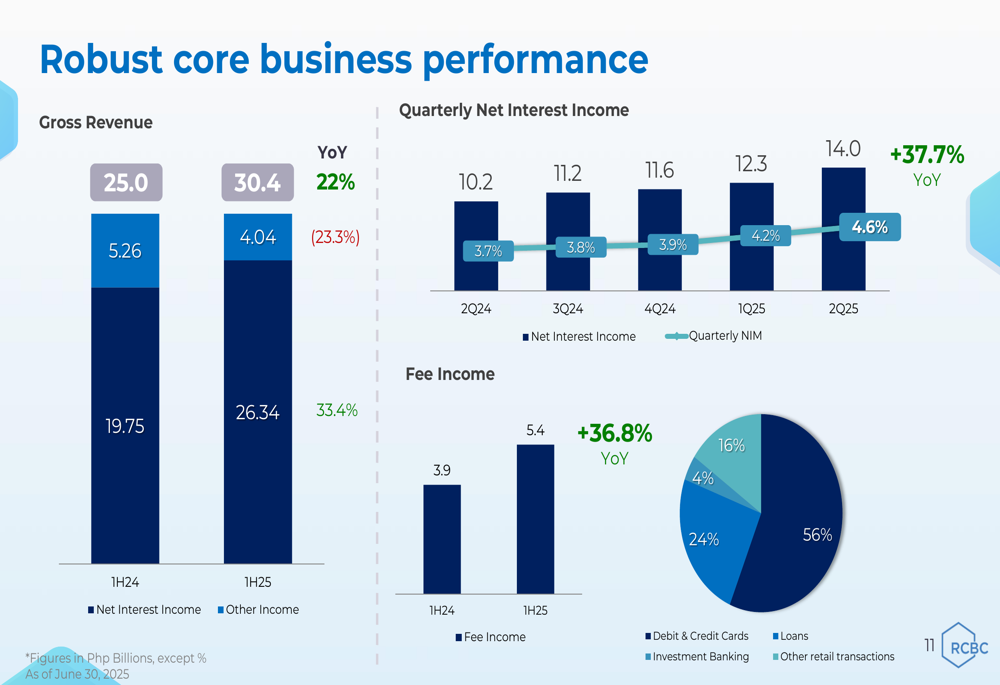

RCBC’s core business showed robust performance in the first half of 2025, with gross revenue increasing 22% year-over-year to P30.4 billion. This growth was primarily driven by a 33.4% increase in net interest income, which reached P26.3 billion. The bank’s fee income also showed strong growth, rising 36.8% to P5.4 billion, with credit and debit cards accounting for 56% of fee income.

The following chart illustrates the bank’s revenue growth and the significant improvement in quarterly net interest income:

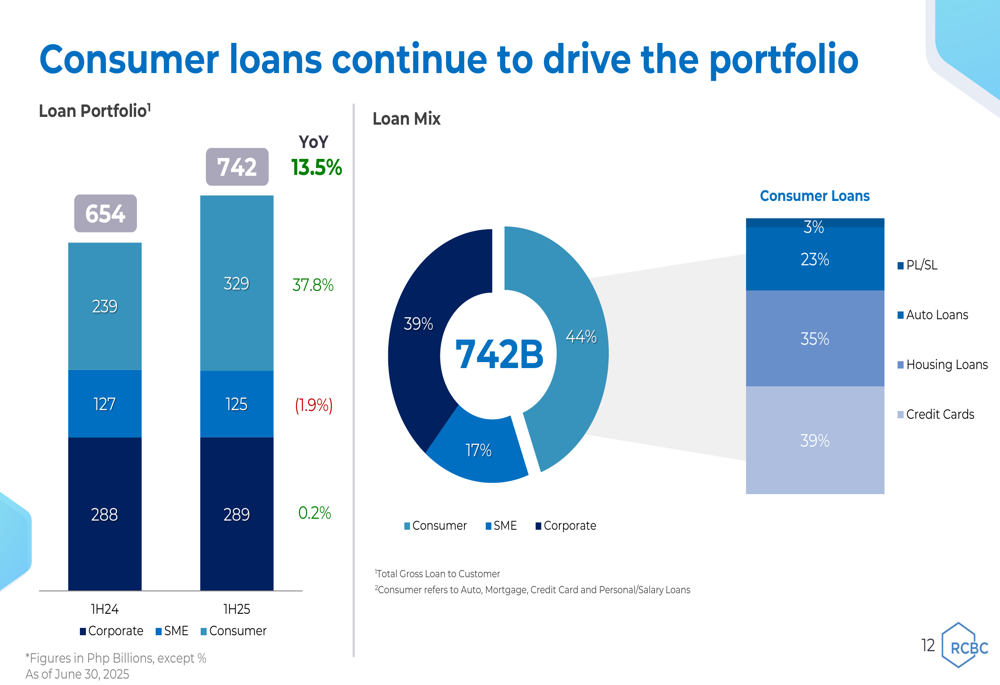

RCBC’s loan portfolio expanded by 13.5% year-over-year to P742 billion, with consumer loans now comprising 44% of the total portfolio, followed by corporate loans at 39% and SME loans at 17%. Within the consumer segment, credit cards represented the largest portion at 39%, followed by auto loans at 35%, personal loans at 23%, and housing loans at 3%.

The loan portfolio composition is detailed in the following chart:

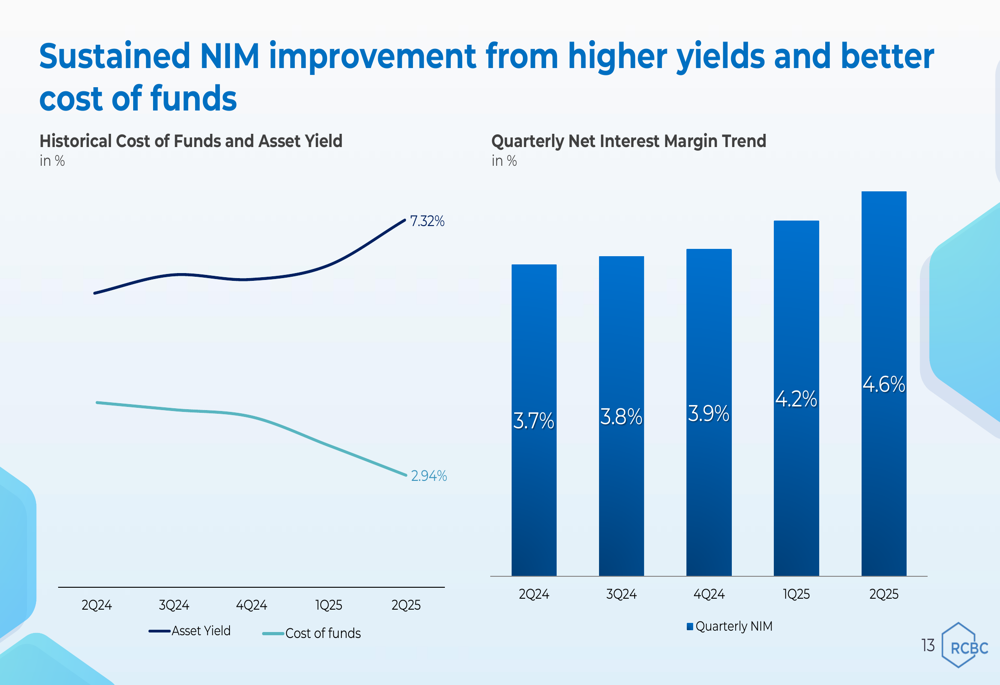

A key driver of RCBC’s improved profitability has been the sustained enhancement of its net interest margin, which reached 4.6% in the second quarter of 2025, up from 3.7% in the same period last year. This improvement was driven by higher asset yields and better management of funding costs.

The NIM improvement trend is illustrated in the following chart:

Strategic Initiatives

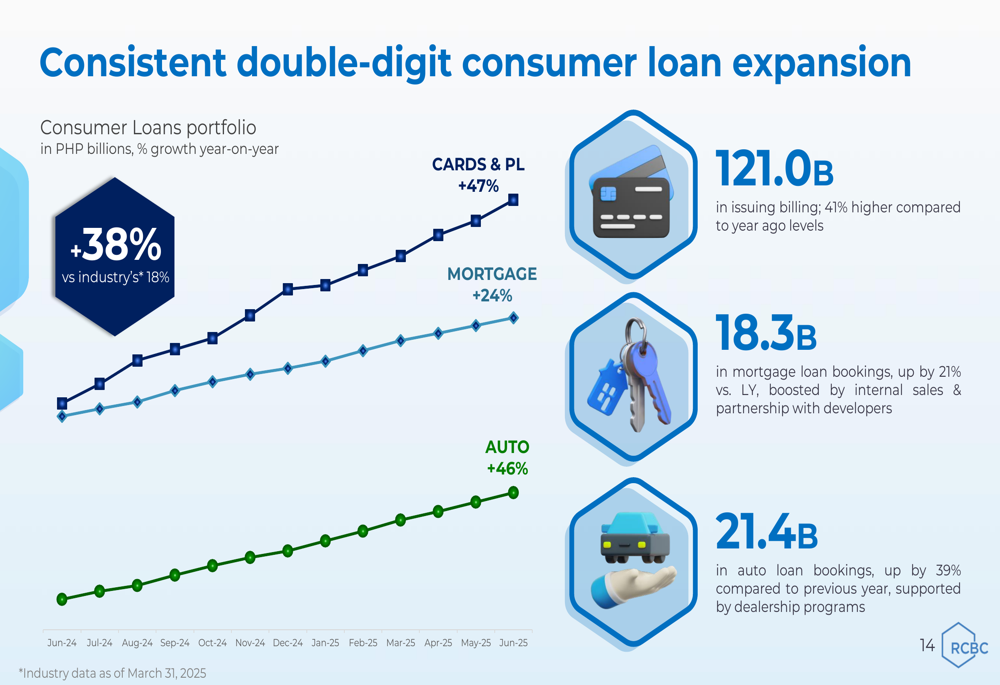

RCBC’s strategic focus on consumer lending has yielded significant results, with the segment growing at more than double the industry rate. Credit cards and personal loans led this expansion with 47% growth, while auto loans and mortgages grew by 46% and 24% respectively.

The consumer loan expansion is detailed in the following chart:

The bank’s credit card business has been particularly strong, with P128 billion in balances representing a 44% increase from last year. RCBC reported P92,000 in receivables per card, exceeding the industry average of P64,000. The bank’s personal loan portfolio also showed impressive growth, increasing 85% year-over-year to P11.1 billion, with digital channels accounting for 64% of total disbursements.

As shown in the following chart, credit card issuing billings have shown consistent growth, reaching P21.5 billion in June 2025:

Digital transformation remains a key strategic priority for RCBC. The bank’s digital platform, RCBC Pulz, facilitated P4.5 billion in digital loan bookings and P220.1 billion in transaction value. Meanwhile, the bank’s ATM Go service expanded to 6,549 terminals, generating 31% year-over-year growth in fee income.

The bank has also maintained its commitment to sustainability, with a P138 billion eligible sustainable portfolio, including P65 billion allocated for renewable energy projects. In 2025, RCBC raised P32 billion from sustainability bonds, supporting projects with a total renewable energy capacity of 2,037 MW.

Forward-Looking Statements

Looking ahead, RCBC expects to maintain its growth momentum while addressing challenges in its SME portfolio. The bank noted that while its overall NPL ratio increased to 4.82%, the SME segment, which accounts for only 17% of the total loan portfolio, experienced higher stress with an NPL ratio of 8.19%. The bank indicated that many of these accounts are pending restructuring.

RCBC’s management expressed confidence in the bank’s ability to sustain its growth trajectory, supported by continued expansion in consumer lending and digital channels. The bank expects to benefit from anticipated policy rate cuts by both the BSP and the Federal Reserve, which should further enhance its net interest margin.

The bank also highlighted its strong capital position, which provides a solid foundation for future growth. With a CET1 ratio of 13.7% and CAR of 16.2%, RCBC remains well-capitalized to pursue its strategic initiatives while navigating potential economic challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.