German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

Ready Capital Corporation (NYSE:RC) released its second quarter 2025 financial results presentation, revealing widening losses as the company continues to navigate challenges in its commercial real estate portfolio while actively repositioning its assets. The stock closed at $4.23 on August 7, 2025, near its 52-week low of $3.93, reflecting ongoing investor concerns about the company’s performance trajectory.

The Q2 results follow a disappointing first quarter when the company missed earnings expectations with a $0.09 per share loss. The latest presentation shows further deterioration, with losses more than tripling sequentially despite management’s previous guidance suggesting a similar earnings profile for Q2.

Quarterly Performance Highlights

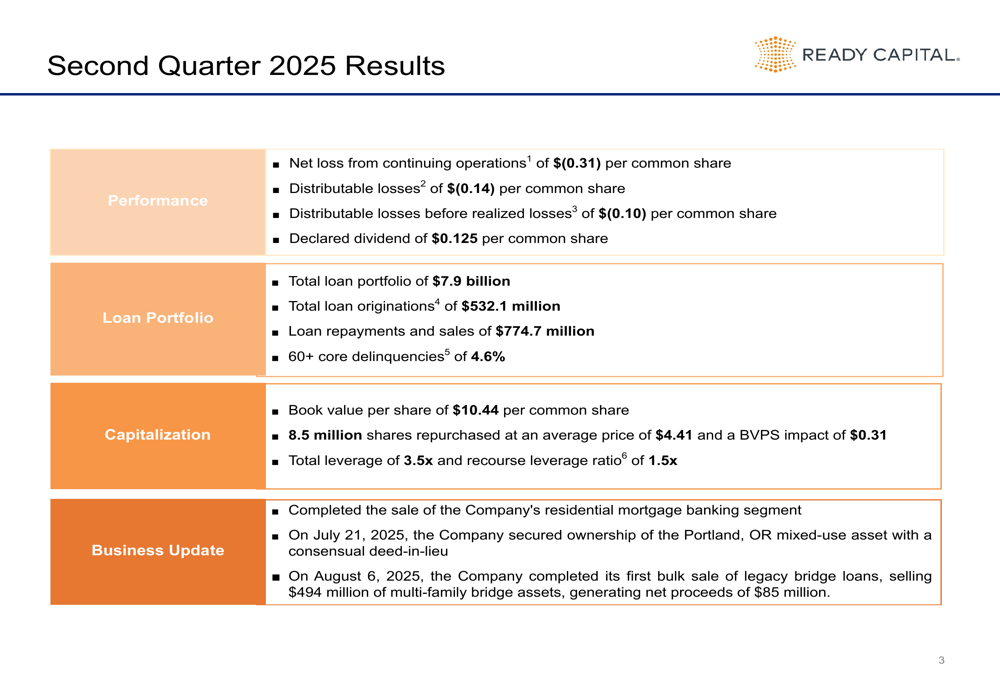

Ready Capital reported a net loss from continuing operations of $0.31 per common share for Q2 2025, significantly worse than the $0.09 loss reported in the previous quarter. Distributable losses were $0.14 per common share, while distributable losses before realized losses were $0.10 per share. Despite these challenges, the company maintained its quarterly dividend at $0.125 per share.

As shown in the following comprehensive summary of Q2 results:

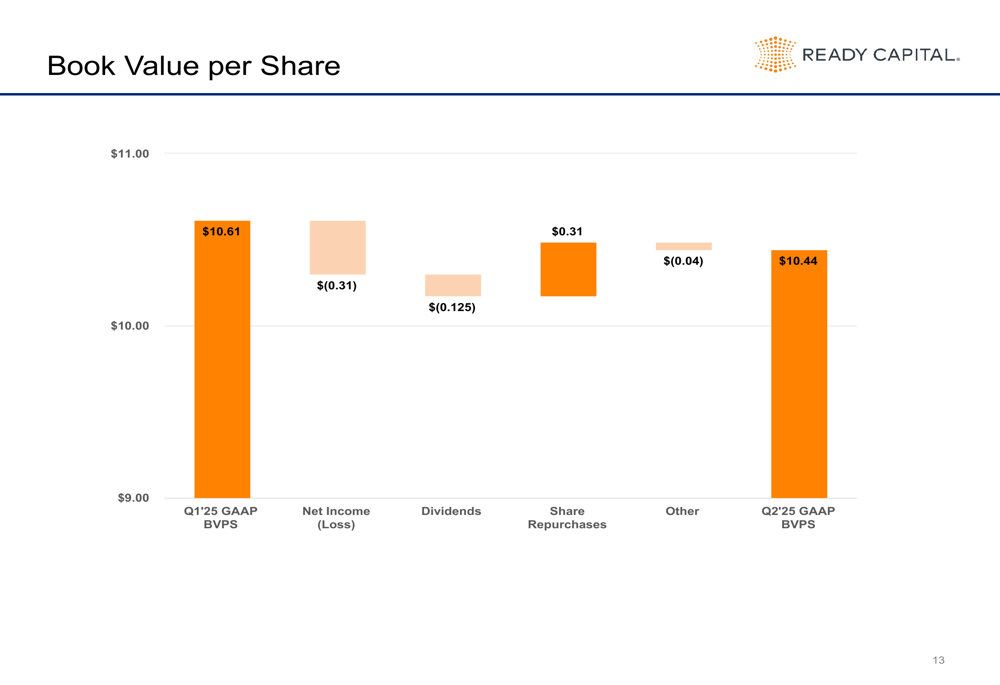

The company’s total loan portfolio stood at $7.9 billion, with new loan originations of $532.1 million offset by loan repayments and sales of $774.7 million during the quarter. Core delinquencies (60+ days) increased to 4.6%, continuing the negative trend from previous quarters. Book value per share declined slightly to $10.44 from $10.61 in Q1 2025.

Portfolio Repositioning Strategy

A key focus of Ready Capital’s strategy is the repositioning of its portfolio, particularly the divestiture of non-performing and non-core assets. The company completed its first bulk sale of legacy bridge loans after the quarter end, selling $494 million of multi-family bridge assets and generating net proceeds of $85 million on August 6, 2025.

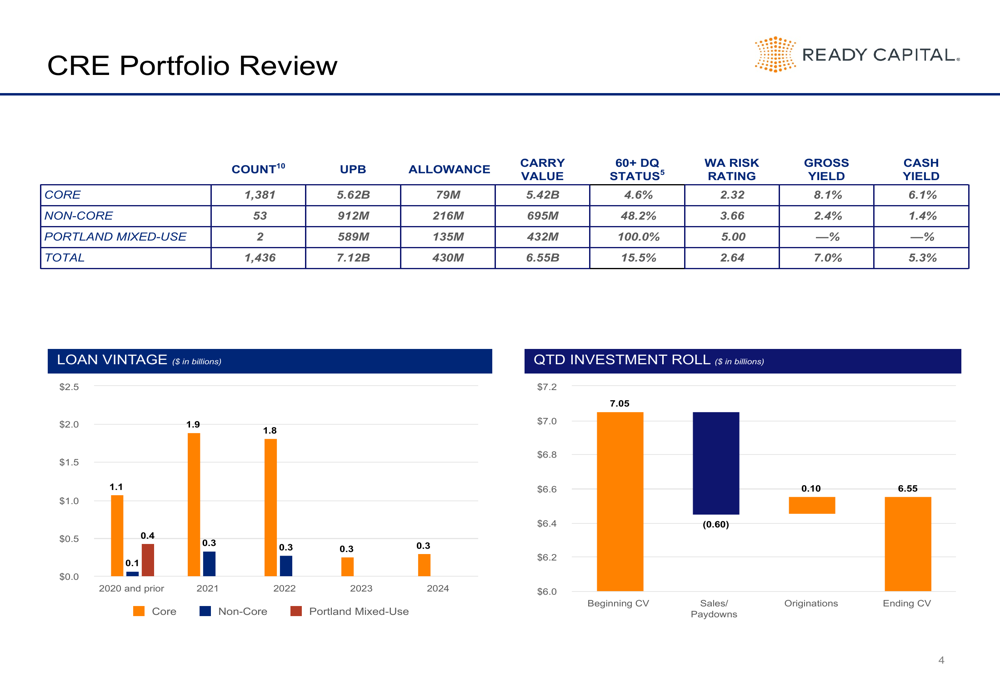

The company’s CRE portfolio review reveals the stark contrast between core and non-core assets:

The data shows that while the core portfolio maintains a relatively healthy 4.6% delinquency rate, the non-core portfolio is experiencing severe stress with a 48.2% delinquency rate. The Portland mixed-use asset, which Ready Capital acquired through a consensual deed-in-lieu arrangement in July 2025, shows 100% delinquency.

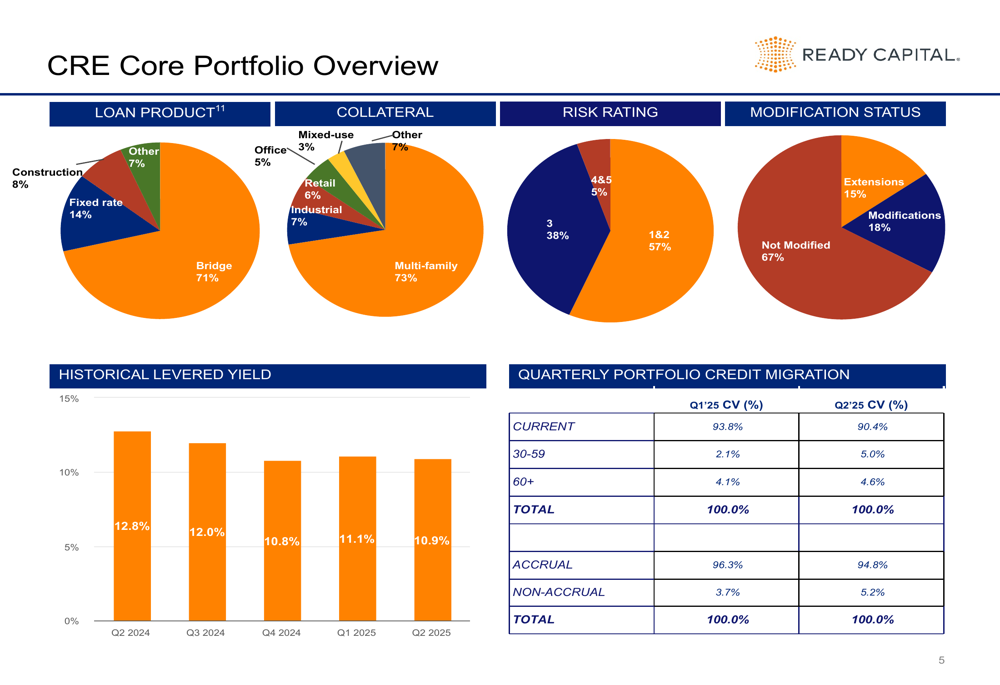

The core CRE portfolio, representing the majority of the company’s assets, shows the following characteristics:

Bridge loans constitute 71% of the core portfolio, with multi-family properties representing 73% of the collateral. Risk ratings show 57% of loans in the 1&2 category (lowest risk), though this has declined from previous quarters. The quarterly credit migration table reveals a concerning trend, with current loans decreasing from 93.8% to 90.4% quarter-over-quarter, while non-accrual loans increased from 3.7% to 5.2%.

Segment Performance Analysis

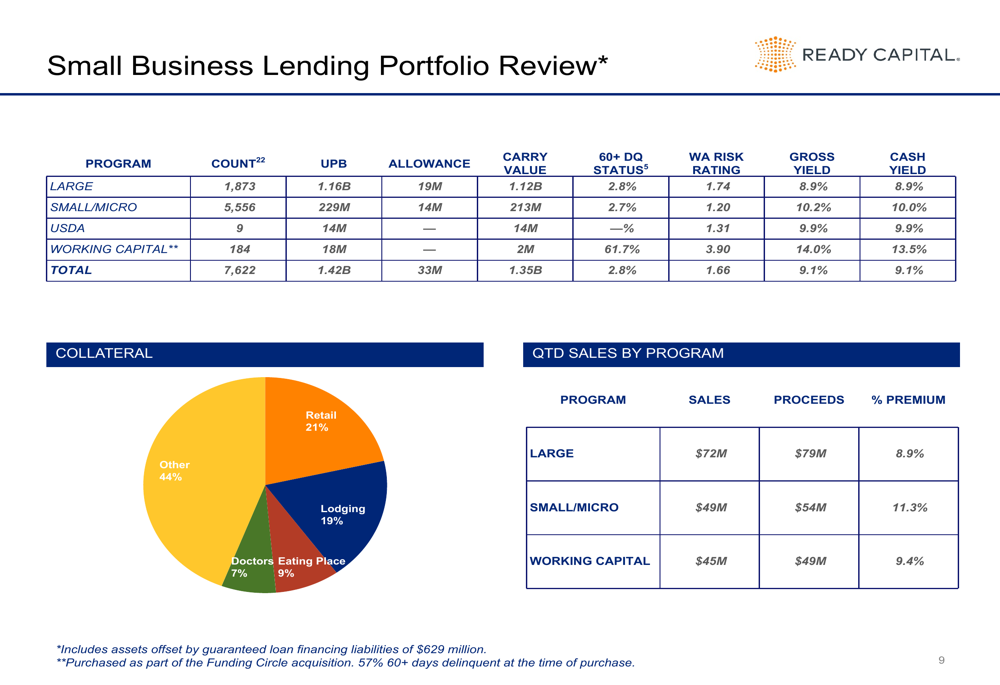

Ready Capital’s operating segments show dramatically different performance profiles. The Small Business Lending portfolio demonstrates significantly better credit metrics compared to the CRE portfolio:

With a delinquency rate of just 2.8% and strong yields of 9.1%, the Small Business Lending segment represents a bright spot in Ready Capital’s portfolio. The segment generated sales premiums ranging from 8.9% to 11.3% across different programs, indicating strong market demand for these assets.

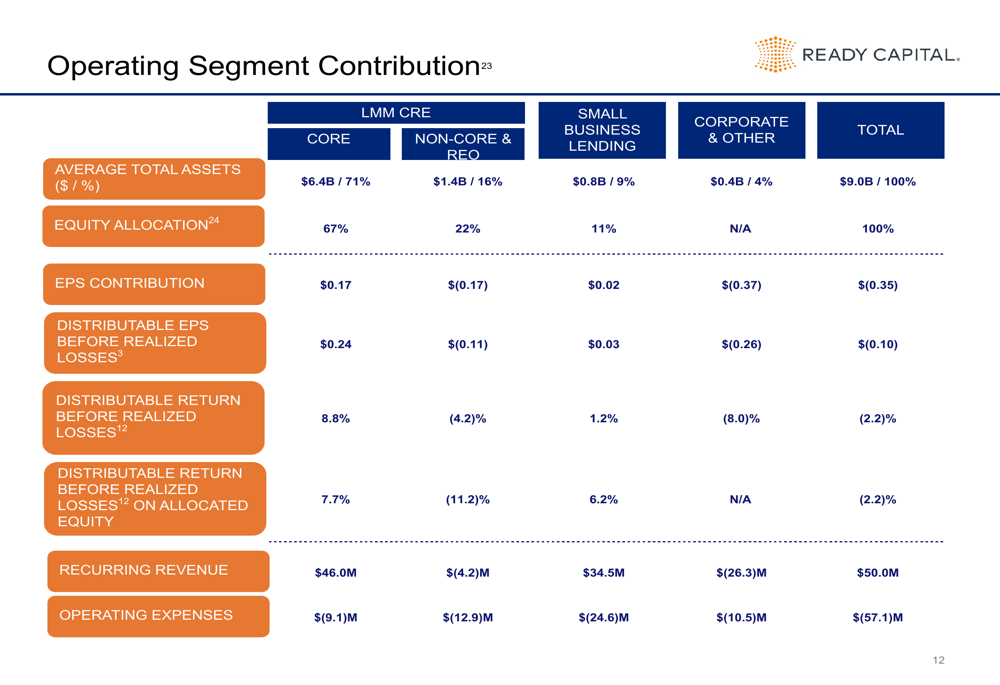

The company’s operating segment contribution analysis further highlights these disparities:

While the Core segment contributed $0.17 to EPS, the Non-Core & REO segment detracted $0.17, effectively canceling out the positive contribution. The Corporate & Other segment was the largest drag on performance at $(0.37) per share. The distributable return before realized losses on allocated equity shows Core at 7.7%, Small Business Lending at 6.2%, and Non-Core & REO at a troubling (11.2)%.

Capital Management & Outlook

Despite the challenging performance, Ready Capital has been actively managing its capital structure. The company repurchased 8.5 million shares at an average price of $4.41 during the quarter, which had a positive impact of $0.31 on book value per share. This partially offset the negative impacts from operating losses and dividends.

The progression of book value per share illustrates these dynamics:

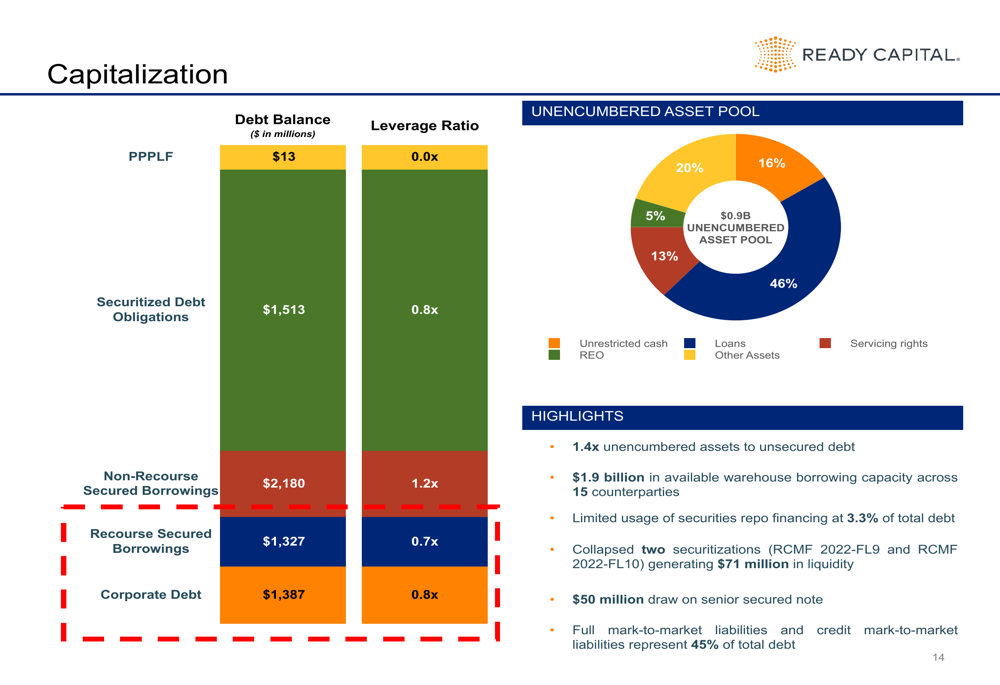

Ready Capital’s capitalization structure shows a total leverage ratio of 3.5x and a recourse leverage ratio of 1.5x. The company maintains $1.9 billion in available warehouse borrowing capacity across 15 counterparties, providing liquidity for operations.

The company’s debt structure and unencumbered asset pool are detailed in the following slide:

Looking ahead, Ready Capital faces significant challenges in resolving its non-performing assets, particularly in the CRE portfolio. The company’s strategy of divesting non-core assets and focusing on better-performing segments like Small Business Lending will be crucial for returning to profitability.

The Portland mixed-use property, which includes a Ritz-Carlton hotel, residences, and commercial space, represents both a significant challenge and opportunity. Management indicated they will manage this project in partnership with Lincoln Property Company and plan to sequentially exit the three components after stabilization.

While Ready Capital continues to face headwinds in its CRE portfolio, the active management of non-core assets and the relatively stable performance of its Small Business Lending segment provide potential paths to recovery. However, investors should note that the company’s financial performance has deteriorated beyond what management had previously indicated, suggesting ongoing challenges in the near term.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.