SoFi stock falls after announcing $1.5B public offering of common stock

Introduction & Market Context

Real Matters Inc. (TSX:REAL) released its third quarter 2025 financial results on July 31, 2025, revealing a mixed performance characterized by sequential growth across all segments despite missing overall earnings expectations. The company’s stock closed at $5.15, down 0.97% following the announcement, reflecting investor caution about the company’s financial trajectory in a challenging mortgage market environment.

The quarter unfolded against the backdrop of what the company described as a "soft spring market," with Real Matters working to position itself strategically for an anticipated market transition. The company highlighted the growing potential for refinance activity, noting approximately 12 million mortgages with rates at or above 6% and 8 million mortgages above 6.5%.

Quarterly Performance Highlights

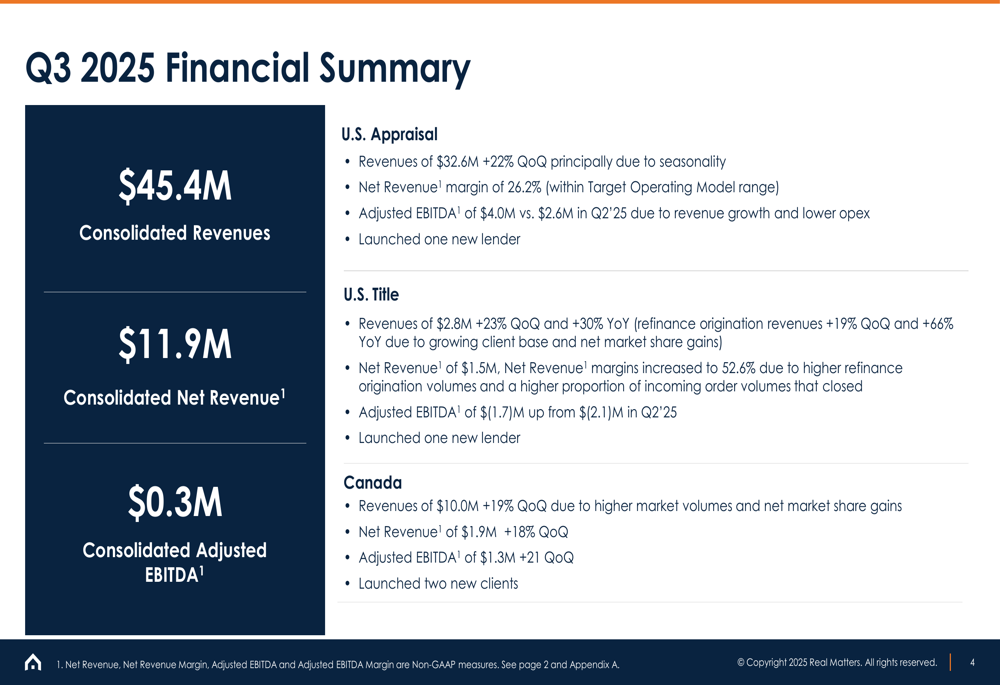

Real Matters reported consolidated revenues of $45.4 million for Q3 2025, representing a sequential increase but an 8% year-over-year decline compared to Q3 2024. The company achieved consolidated net revenue of $11.9 million, falling short of analyst expectations of $13.23 million. Despite this revenue miss, Real Matters returned to positive adjusted EBITDA territory at $0.3 million, a significant improvement from the $1.9 million loss reported in the previous quarter.

As shown in the company’s financial summary slide, all three business segments delivered double-digit sequential growth:

The U.S. Appraisal segment, which remains the company’s largest revenue generator, posted revenues of $32.6 million, representing a 22% increase quarter-over-quarter. This segment maintained healthy profitability with adjusted EBITDA of $4.0 million and a net revenue margin of 26.2%.

U.S. Title continued its growth trajectory with revenues of $2.8 million, up 23% sequentially and 30% year-over-year. While this segment still operates at a loss with adjusted EBITDA of $(1.7) million, its net revenue margins improved to 52.6%, indicating progress toward the company’s profitability goals.

The Canadian operations delivered revenues of $10.0 million, a 19% increase from the previous quarter, with adjusted EBITDA of $1.3 million, up 21% quarter-over-quarter.

Detailed Financial Analysis

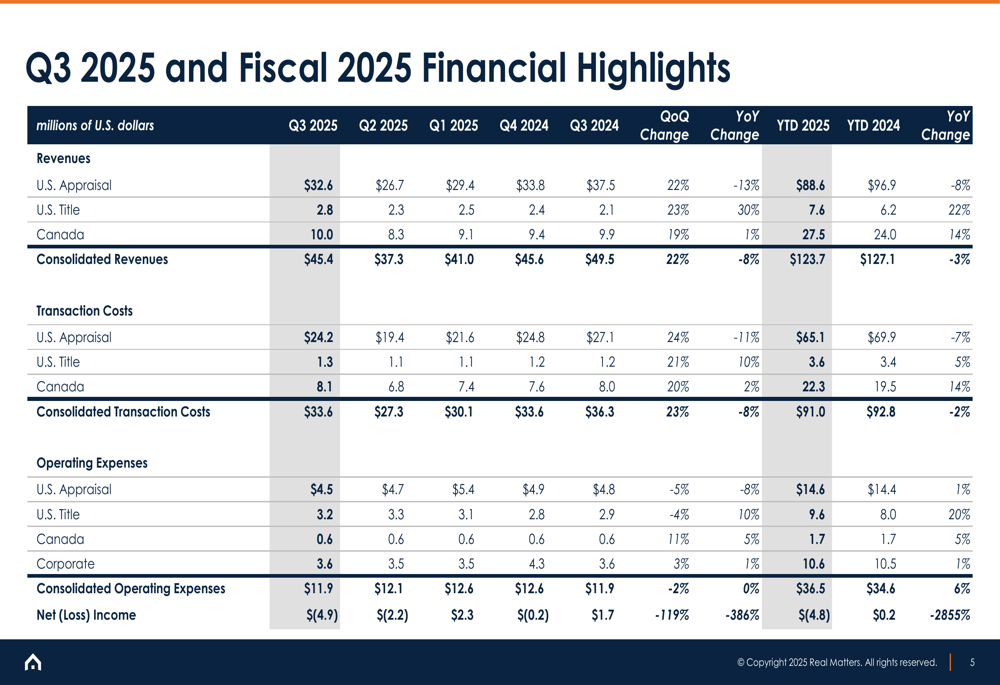

A closer examination of Real Matters’ financial performance reveals both strengths and challenges. The company reported a consolidated net loss of $(4.9) million for Q3 2025, a significant deterioration from the $1.7 million net income reported in the same quarter last year. This resulted in earnings per share of -$0.01, missing analyst expectations of $0.0033 by a substantial margin.

The following table provides a comprehensive view of the company’s financial performance across multiple quarters:

Despite the year-over-year revenue decline, the sequential improvement across all segments suggests the company may be stabilizing its operations. The return to positive consolidated adjusted EBITDA ($0.3 million) in Q3 2025 from negative territory in Q2 2025 ($1.9 million loss) represents a meaningful improvement in operational efficiency.

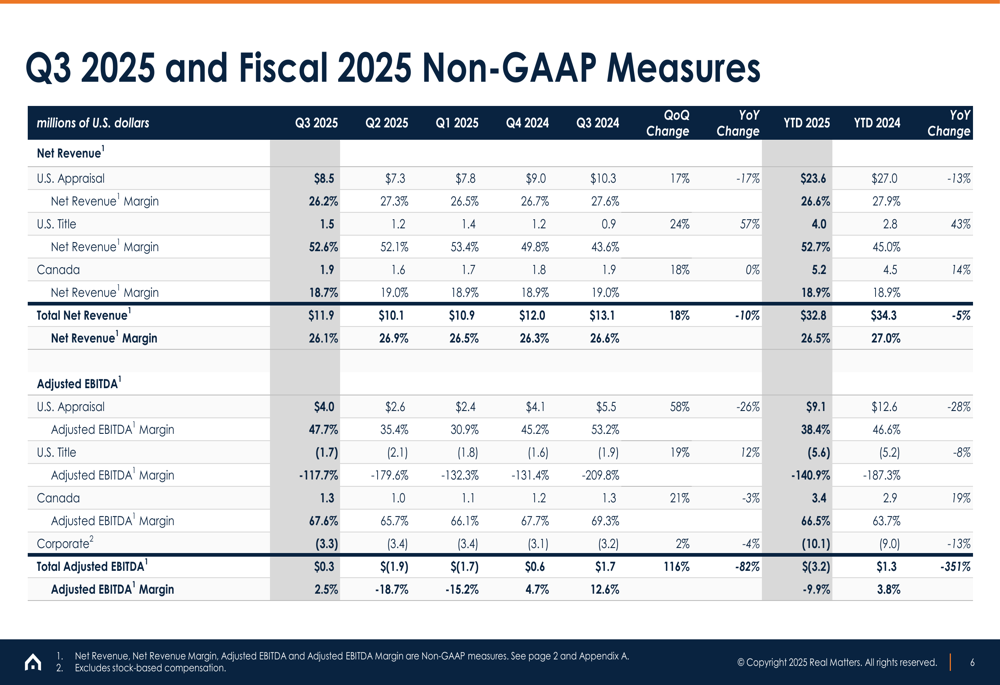

The non-GAAP measures table further illustrates the company’s performance trends:

Real Matters maintained a strong balance sheet with $44 million in cash and no debt as of the quarter end. This financial flexibility provides the company with resources to pursue its growth initiatives while navigating market uncertainties.

Strategic Initiatives

Real Matters emphasized several strategic achievements during the quarter, focusing on client acquisition and market share expansion. The company launched four new clients, including the largest credit union in U.S. Title, and doubled its market share quarter-over-quarter with the largest reverse mortgage lender in the U.S. Title segment.

The company’s key strategic highlights for the quarter included:

Post-quarter developments included the launch of a second Tier 1 lender in U.S. Title and the onboarding of a top-15 lender in U.S. Appraisal. These client wins align with Real Matters’ strategy of expanding its market presence and diversifying its revenue streams across different segments of the mortgage industry.

CEO Brian Lang emphasized the company’s strategic positioning, stating, "We believe there is substantial pent-up demand in the U.S. mortgage market." Lang highlighted the differentiation provided by their network management model and their readiness to drive growth as the market transitions.

Forward-Looking Statements

Looking ahead, Real Matters anticipates potential market improvements driven by refinancing opportunities. The company’s presentation emphasized the significant number of mortgages with rates at or above 6%, representing a substantial pool of potential refinancing activity when market conditions become more favorable.

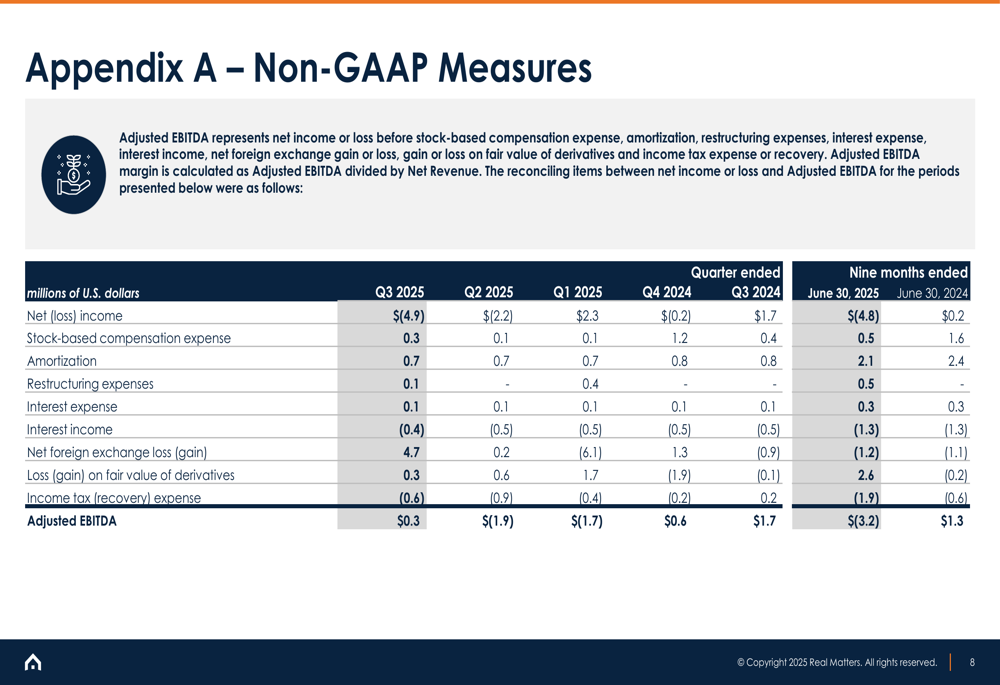

The reconciliation of non-GAAP measures provides additional context for understanding the company’s financial trajectory:

While Real Matters faces ongoing challenges in achieving consistent profitability, particularly in its U.S. Title segment, the company’s focus on client acquisition and market share expansion appears designed to position it advantageously for an eventual market rebound. The company aims to scale its business and grow market share, focusing on its target operating model EBITDA potential for U.S. Appraisal and Title segments.

Investors should note that with a beta of 2.46, Real Matters stock exhibits higher volatility compared to the broader market, which may present both risks and opportunities as the company works to execute its strategic initiatives in a challenging mortgage environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.