US LNG exports surge but will buyers in China turn up?

Introduction & Market Context

Regal Rexnord (NYSE:ZWS) Corporation (NYSE:RRX) released its second quarter 2025 earnings results on August 6, showing resilience with earnings per share growth despite a slight sales decline. The company’s stock was down 2.97% in premarket trading, suggesting investors may have concerns about certain aspects of the results or guidance.

The industrial manufacturer reported mixed segment performance, with its Power Efficiency Solutions business showing strong growth while its other segments faced headwinds. The company also made significant progress in debt reduction through a new receivables securitization facility.

Quarterly Performance Highlights

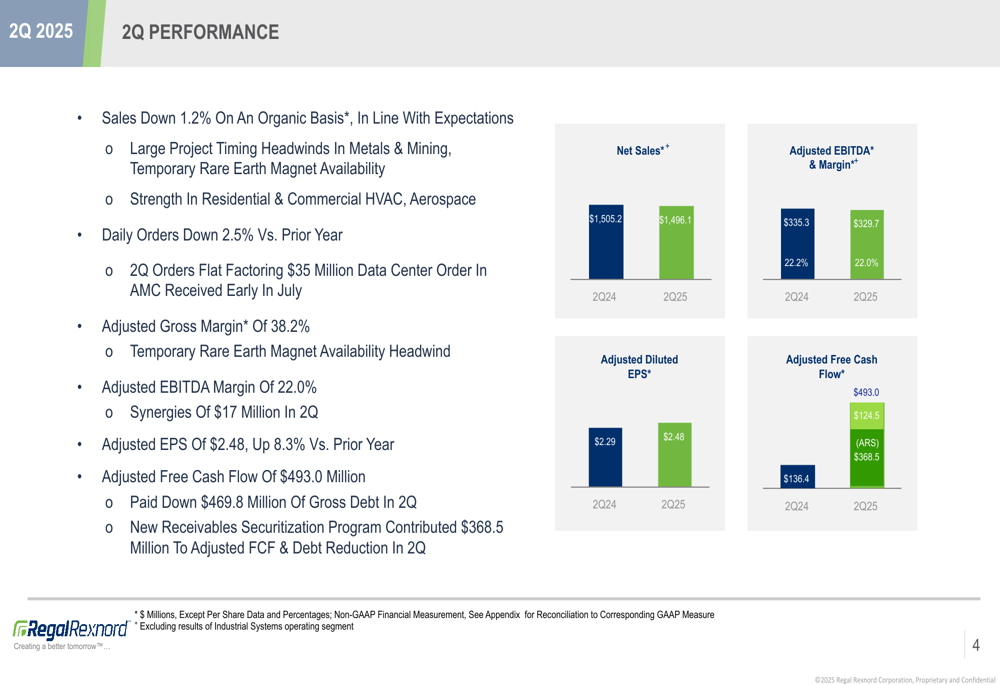

Regal Rexnord reported Q2 2025 sales of $1.496 billion, down 1.2% on an organic basis compared to the prior year, which the company noted was in line with expectations. Daily orders were down 2.5% versus the prior year, though the company indicated Q2 orders would have been flat when factoring in a $35 million data center order received in early July.

As shown in the following comprehensive performance summary:

Despite the sales decline, adjusted earnings per share reached $2.48, up 8.3% compared to $2.29 in Q2 2024. This continues the positive earnings momentum from Q1 2025, when the company reported EPS of $2.15. Adjusted gross margin improved to 38.2% from 37.8% in the prior year period, while adjusted EBITDA margin was 22.0%, slightly down from 22.2% a year ago.

The most dramatic improvement came in adjusted free cash flow, which surged to $493.0 million from $136.4 million in Q2 2024, allowing the company to pay down $469.8 million of gross debt during the quarter.

Segment Performance Analysis

Performance varied significantly across Regal Rexnord’s three business segments, with only one showing positive growth.

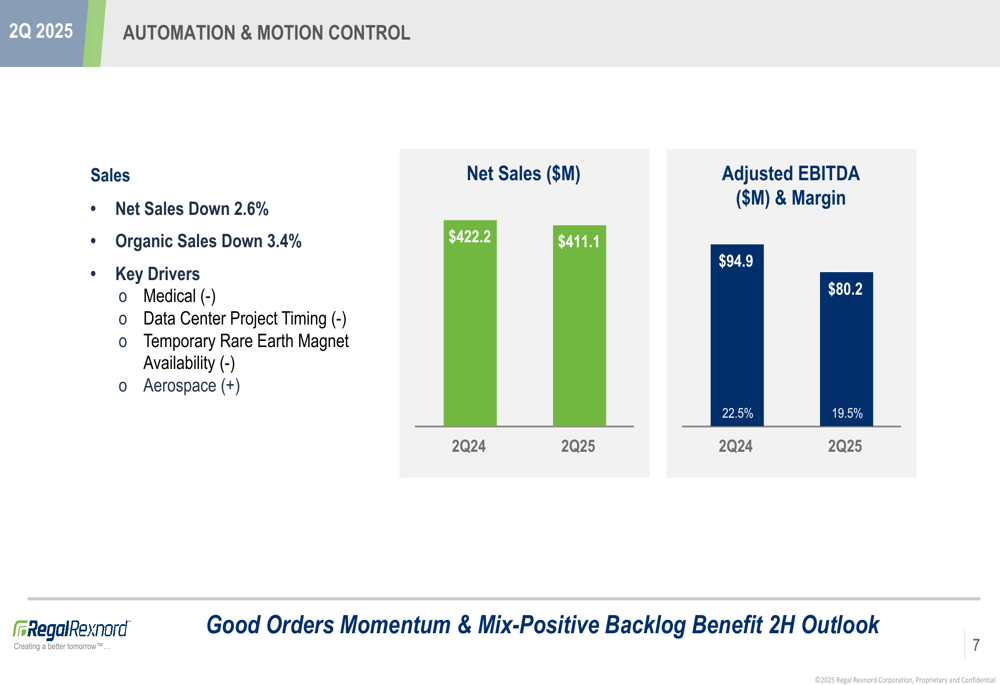

The Automation & Motion Control segment faced the most significant challenges, as illustrated in this segment breakdown:

This segment reported net sales down 2.6% and organic sales down 3.4%, with adjusted EBITDA margin declining to 19.5% from 22.5% in the prior year. Key headwinds included weakness in medical markets, data center project timing, and temporary rare earth magnet availability issues, partially offset by strength in aerospace.

The Industrial Powertrain Solutions segment also experienced sales declines but improved profitability:

While net sales fell 3.8% and organic sales declined 4.4%, primarily due to weakness in metals and mining, the segment’s adjusted EBITDA margin improved to 26.9% from 25.8% in Q2 2024. Management highlighted that backlog was up 15% year-to-date, reinforcing a positive outlook.

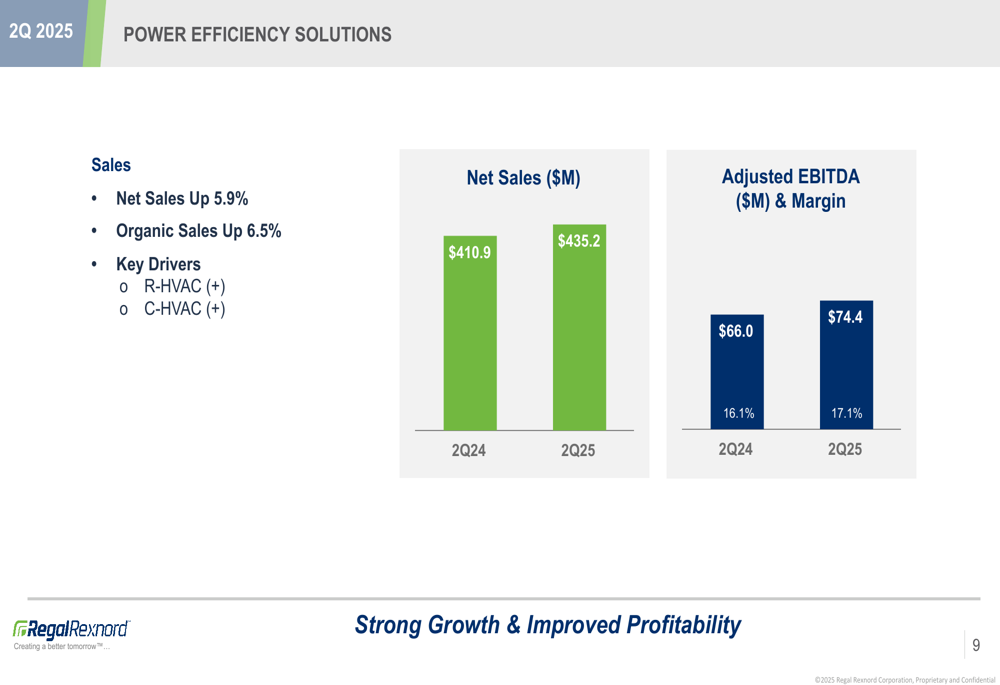

The Power Efficiency Solutions segment was the standout performer:

This segment delivered 5.9% net sales growth and 6.5% organic sales growth, driven by strength in both residential and commercial HVAC markets. Adjusted EBITDA margin improved to 17.1% from 16.1% in the prior year period.

Strategic Initiatives

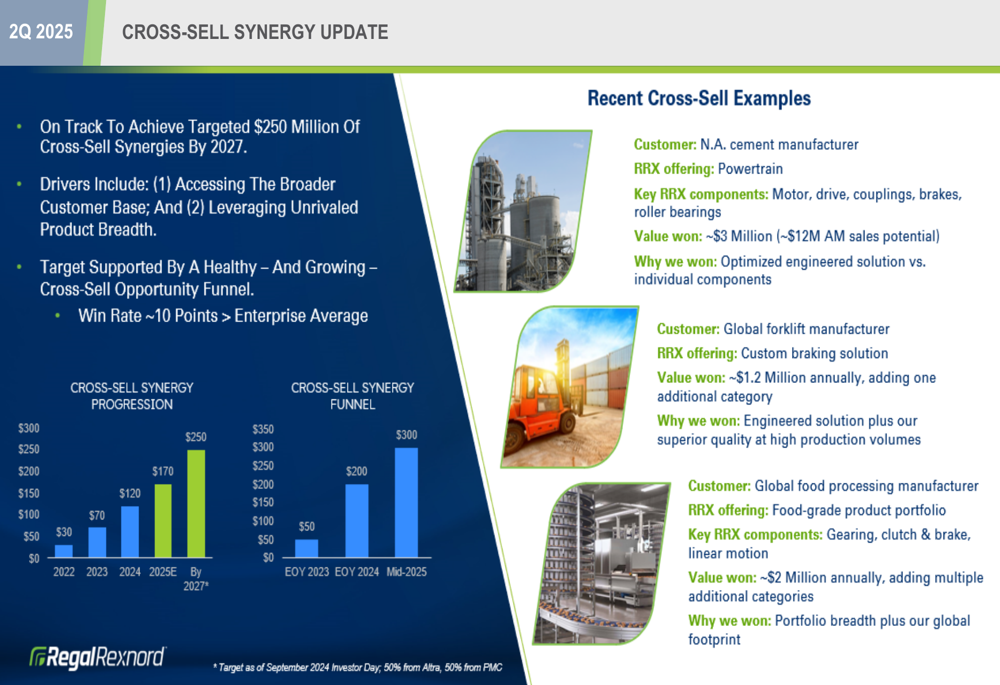

A key strategic focus for Regal Rexnord remains its cross-sell synergy program, which the company reports is on track:

The company is progressing toward its target of $250 million in cross-sell synergies by 2027, leveraging its broad customer base and extensive product portfolio. Management noted that the win rate for cross-sell opportunities is approximately 10 percentage points higher than the enterprise average.

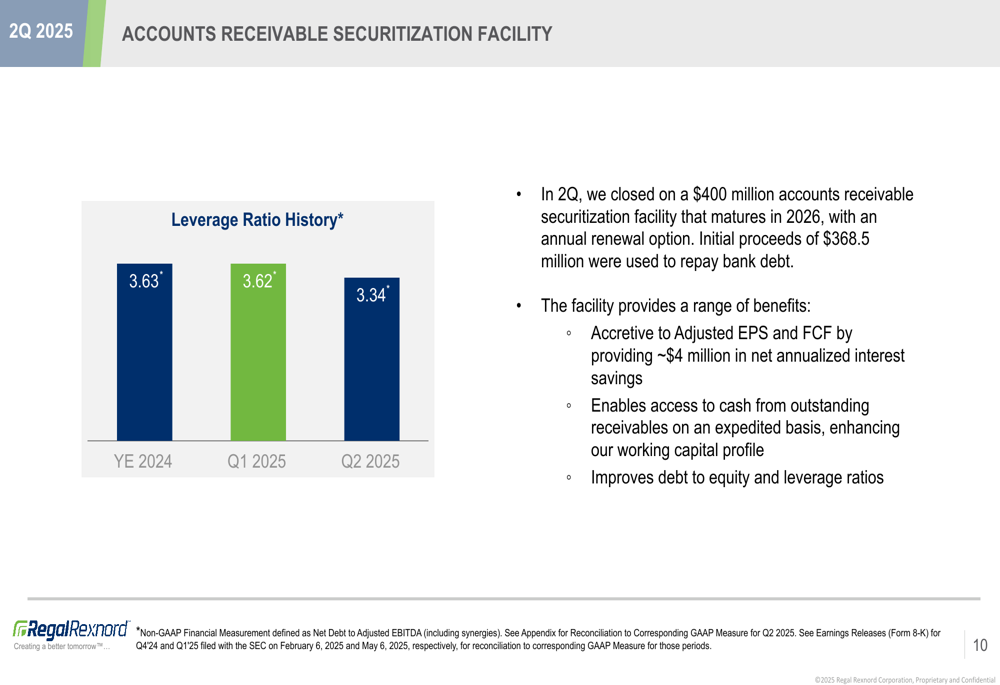

Another significant strategic move was the implementation of a new accounts receivable securitization facility:

In Q2, the company closed on a $400 million accounts receivable securitization facility that matures in 2026, with an annual renewal option. Initial proceeds of $368.5 million were used to repay bank debt, providing approximately $4 million in net annualized interest savings. This contributed to improving the company’s leverage ratio from 3.63 at year-end 2024 to 3.34 in Q2 2025.

Forward-Looking Statements

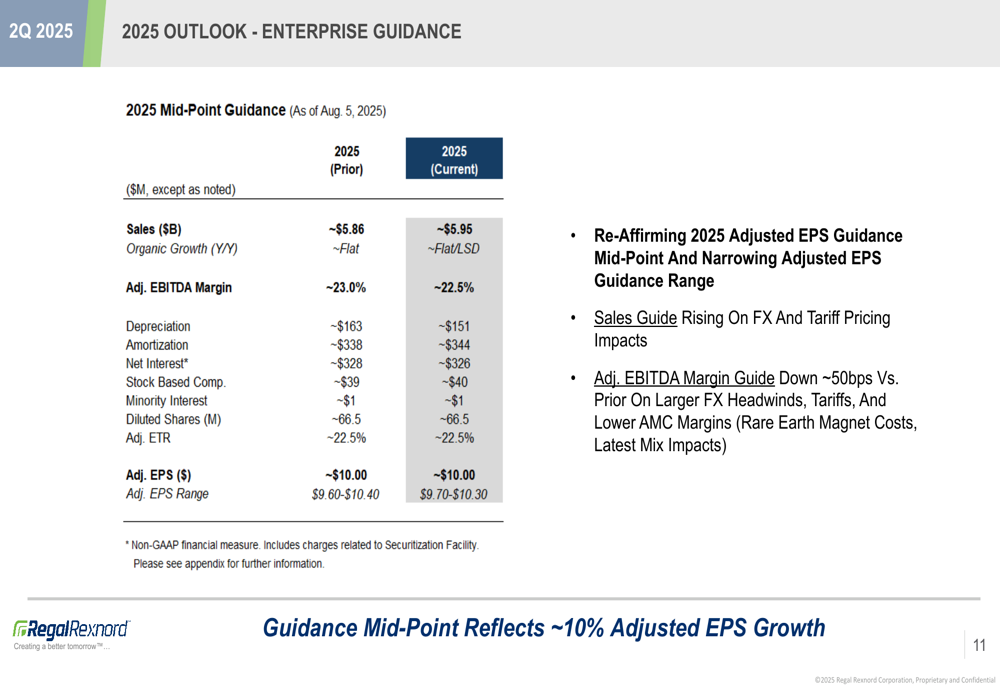

Regal Rexnord reaffirmed its 2025 adjusted EPS guidance midpoint of approximately $10.00, while narrowing the range:

The company raised its sales guidance to approximately $5.95 billion, primarily due to foreign exchange and tariff pricing impacts. However, it lowered its adjusted EBITDA margin guidance by about 50 basis points to approximately 22.5%, citing larger foreign exchange headwinds, tariffs, and lower margins in the Automation & Motion Control segment.

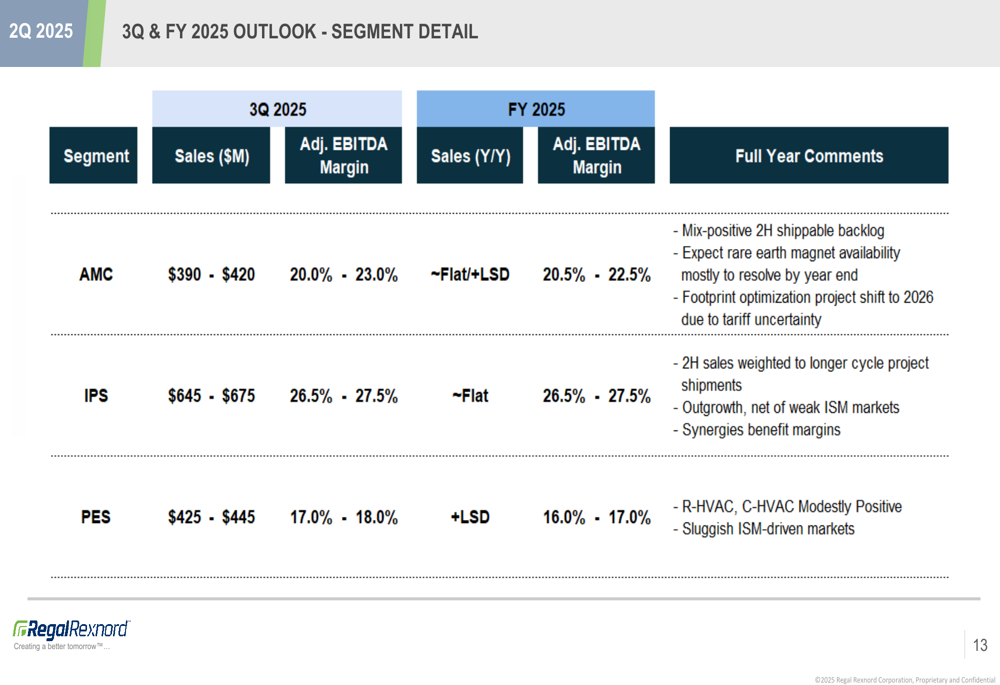

The company also provided detailed segment-level guidance for both Q3 and the full year 2025:

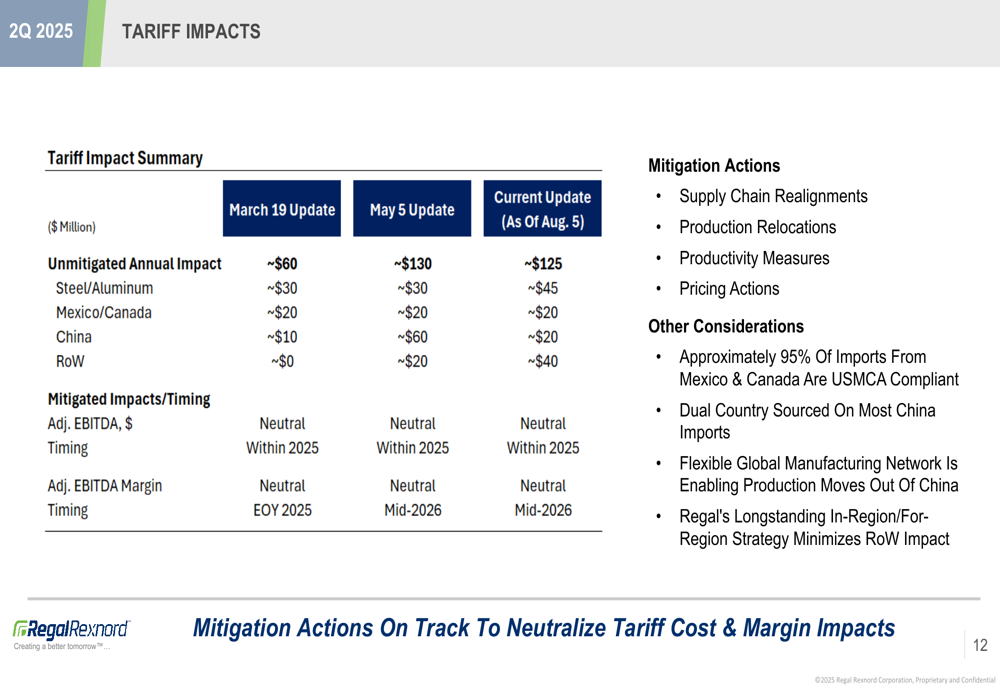

Tariffs remain a significant concern, but the company is implementing various mitigation strategies:

Management detailed several approaches to address tariff impacts, including supply chain realignments, production relocations, productivity measures, and pricing actions. The company’s longstanding in-region/for-region strategy and flexible global manufacturing network are helping to minimize these impacts.

Debt Management

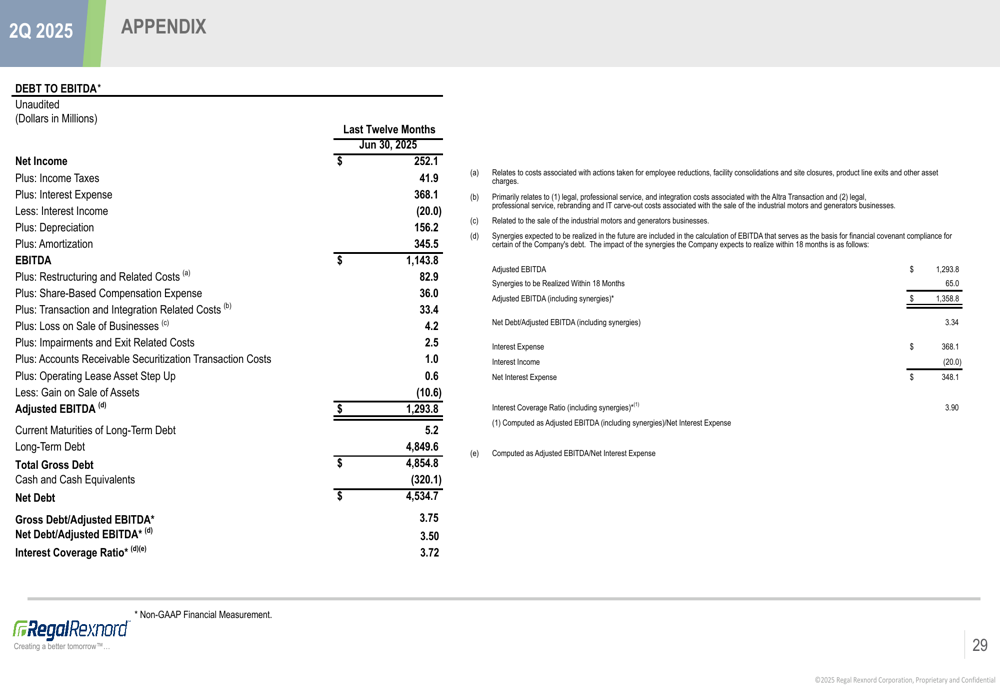

Regal Rexnord’s debt position has improved significantly, as shown in the following debt metrics:

The company reported net debt of $4.53 billion, resulting in a net debt to adjusted EBITDA ratio of 3.50, down from previous quarters. The interest coverage ratio stands at 3.72, indicating the company’s ability to service its debt obligations.

Conclusion

Regal Rexnord’s Q2 2025 results demonstrate the company’s ability to grow earnings and generate strong cash flow despite sales challenges in some segments. The significant debt reduction achieved through the new securitization facility represents a positive step toward strengthening the balance sheet.

While the company faces headwinds from tariffs and segment-specific challenges, the reaffirmation of full-year EPS guidance suggests management confidence in its ability to navigate these issues. The strong performance in the Power Efficiency Solutions segment, driven by HVAC market strength, partially offsets weakness in other areas.

Investors will likely focus on the company’s ability to execute its tariff mitigation strategies and capitalize on the growing backlog in the Industrial Powertrain Solutions segment as they evaluate the stock’s prospects for the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.