Datavault AI completes second tranche with Scilex for 1,237.6 Bitcoin

Regional Management Corp. (NYSE:RM) delivered impressive third-quarter results according to its earnings presentation released on November 5, 2025, with record revenue and substantial earnings growth driving a positive market reaction.

The company's stock rose 3.63% in aftermarket trading following the announcement, reflecting investor confidence in its strong performance and growth trajectory.

Quarterly Performance Highlights

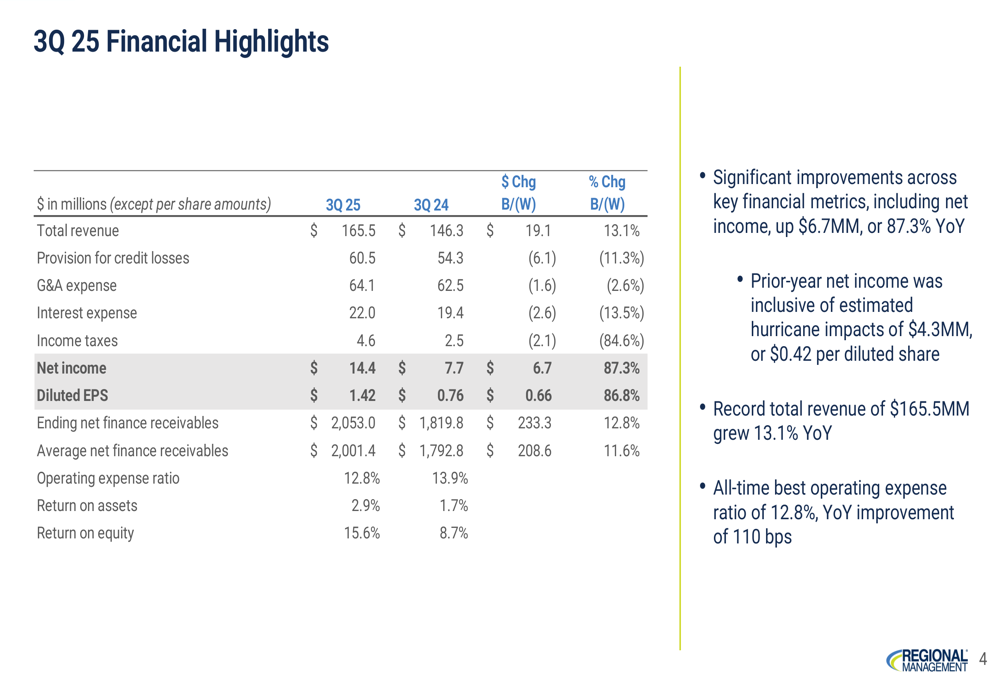

Regional Management achieved record total revenue of $165.5 million in Q3 2025, representing a 13.1% increase year-over-year. This revenue growth, coupled with improved operating efficiency, led to net income of $14.4 million and diluted earnings per share of $1.42 – an 87.3% and 86.8% increase year-over-year, respectively.

The company's performance was particularly impressive given that Q3 2024 results were negatively impacted by hurricane activity, which reduced prior-year net income by an estimated $4.3 million or $0.42 per diluted share.

As shown in the following financial highlights table, the company demonstrated significant improvements across key metrics:

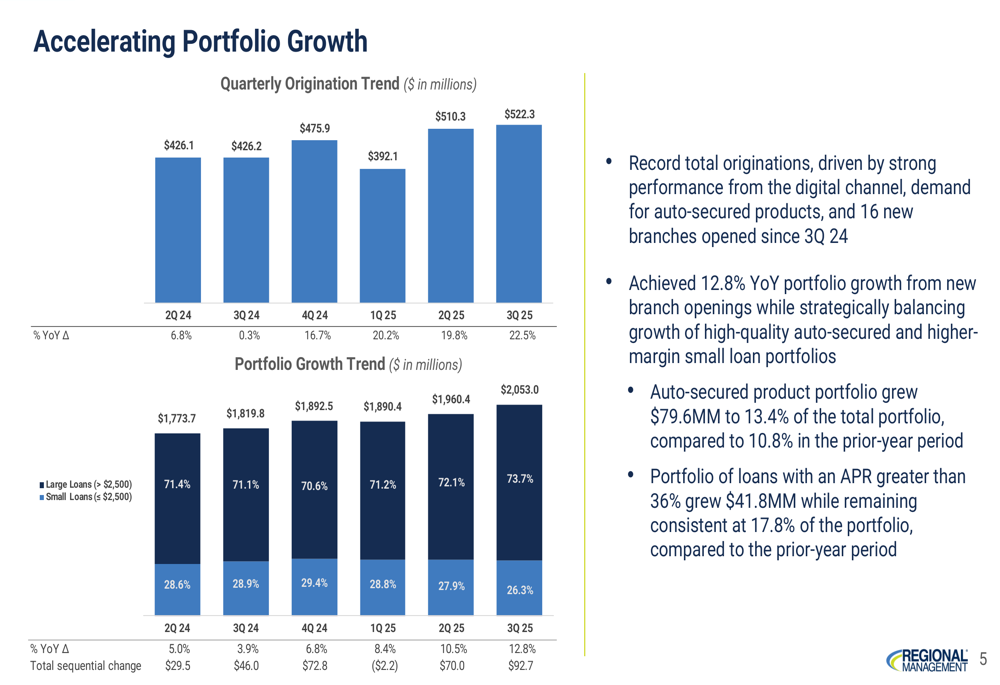

Regional Management achieved a major milestone by surpassing $2.1 billion in ending net receivables (ENR), representing $93 million in sequential growth and $233 million in year-over-year growth. This portfolio expansion was driven by strong origination volume of $522 million, up 22.5% from the prior year.

The company's key performance metrics showed substantial improvements, with return on equity reaching 15.6% (up 690 basis points year-over-year) and return on assets hitting 2.9% (up 120 basis points year-over-year).

Strategic Growth Initiatives

Regional Management's growth strategy centers around branch expansion, digital origination growth, and portfolio diversification. The company opened 16 new branches since Q3 2024, which generated $52.4 million or 22.4% of the total year-over-year portfolio growth.

The following chart illustrates the company's accelerating portfolio growth trends:

A key efficiency metric for the company is ENR per branch, which increased 9.9% year-over-year to $5.9 million. New branches are showing particularly strong growth trajectories, with branches less than one year old more than doubling their ENR from $1.5 million in Q3 2024 to $3.3 million in Q3 2025.

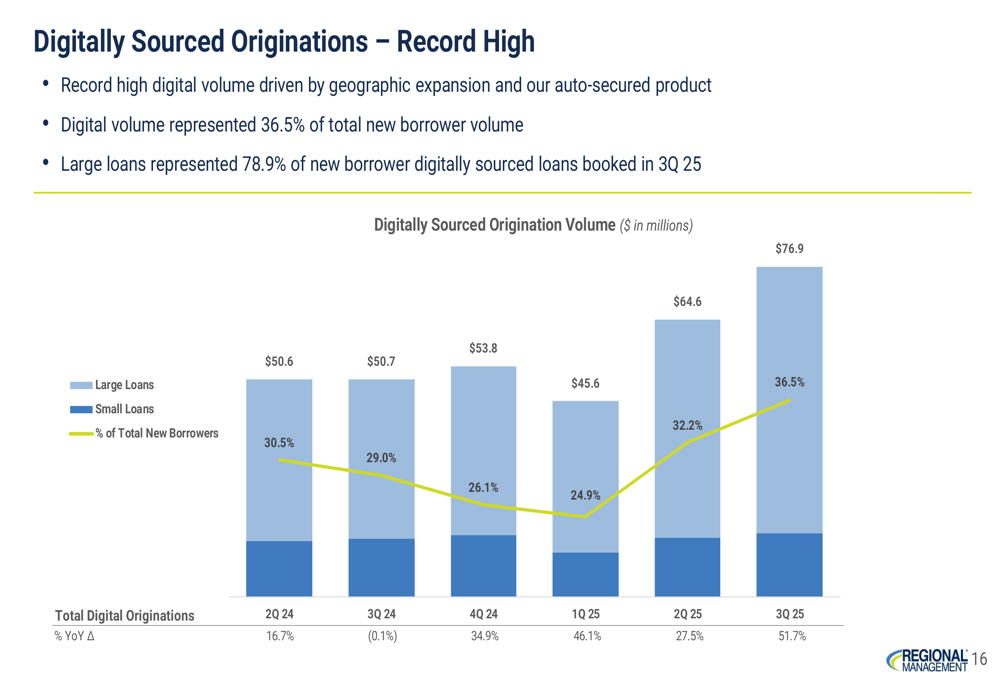

Digital originations reached a record high in Q3 2025, representing 36.5% of total new borrower volume. The company's focus on digital channels is paying dividends as shown in the following chart:

Regional Management has also strategically expanded its auto-secured portfolio, which grew to $275 million, representing a 40.6% increase year-over-year. This diversification helps balance risk while capturing growth opportunities in the secured lending market.

Detailed Financial Analysis

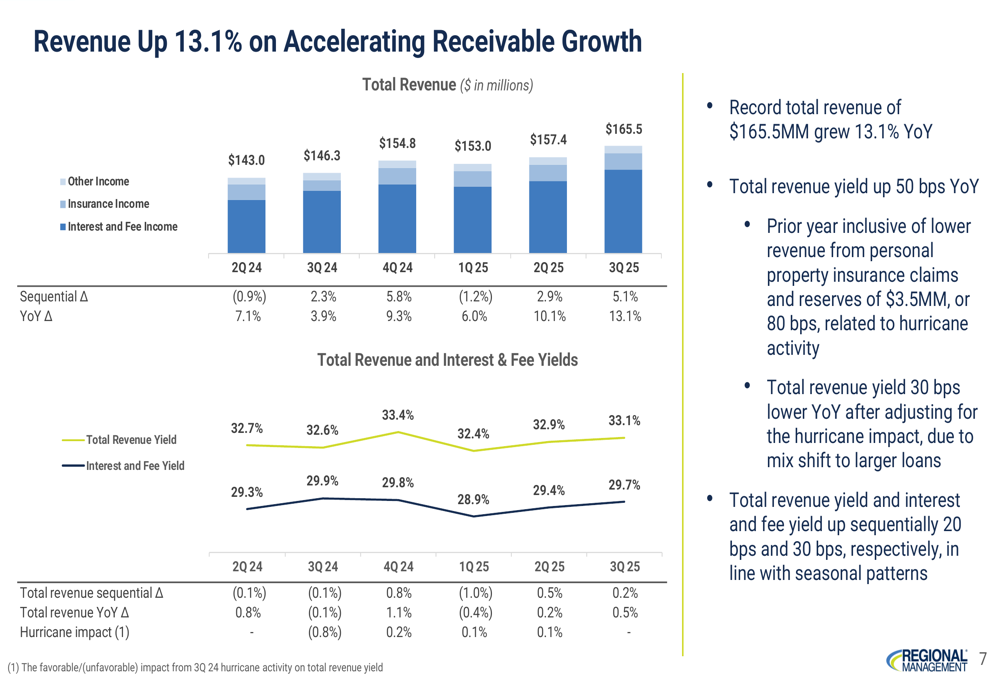

Revenue growth has accelerated in recent quarters, reaching 13.1% year-over-year in Q3 2025, while maintaining stable yields. The following chart illustrates this trend:

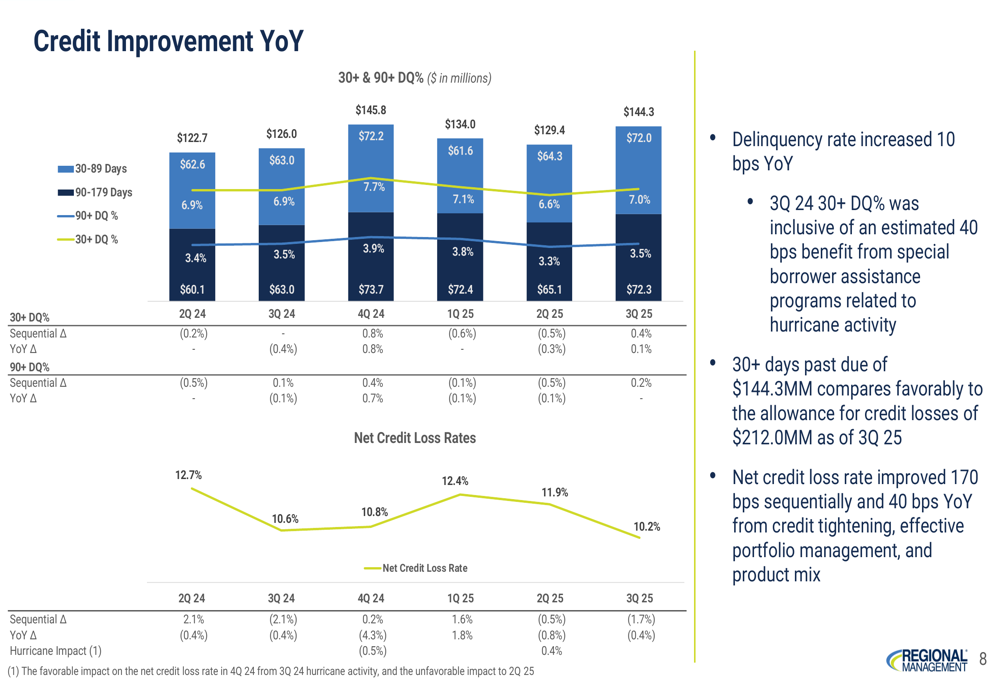

Credit performance showed improvement year-over-year, with the net credit loss rate decreasing to 10.2%, a 40 basis point improvement from Q3 2024. The 30+ day delinquency rate stood at 7.0%, representing a 30 basis point improvement year-over-year after adjusting for the prior-year hurricane impact.

The following chart shows the trend in delinquency rates and net credit losses:

Operating efficiency continued to improve, with the company achieving an all-time best operating expense ratio of 12.8%, representing a 110 basis point improvement year-over-year. This improvement reflects the company's ability to grow revenue faster than expenses while continuing to invest in the business.

Regional Management maintained a strong funding profile with $400 million in unused capacity as of September 30, 2025. The company has strategically positioned its debt portfolio with 76% fixed-rate debt at a weighted average cost of 4.6%, providing stability in the current interest rate environment.

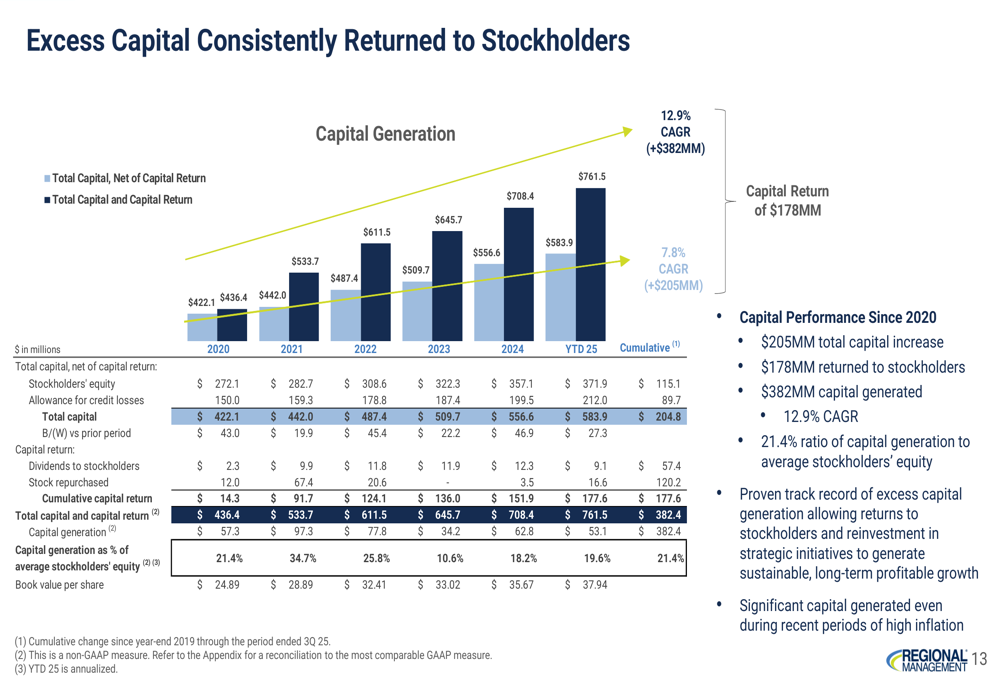

The company has consistently returned excess capital to shareholders while maintaining strong growth, as illustrated in the following chart:

Forward-Looking Statements

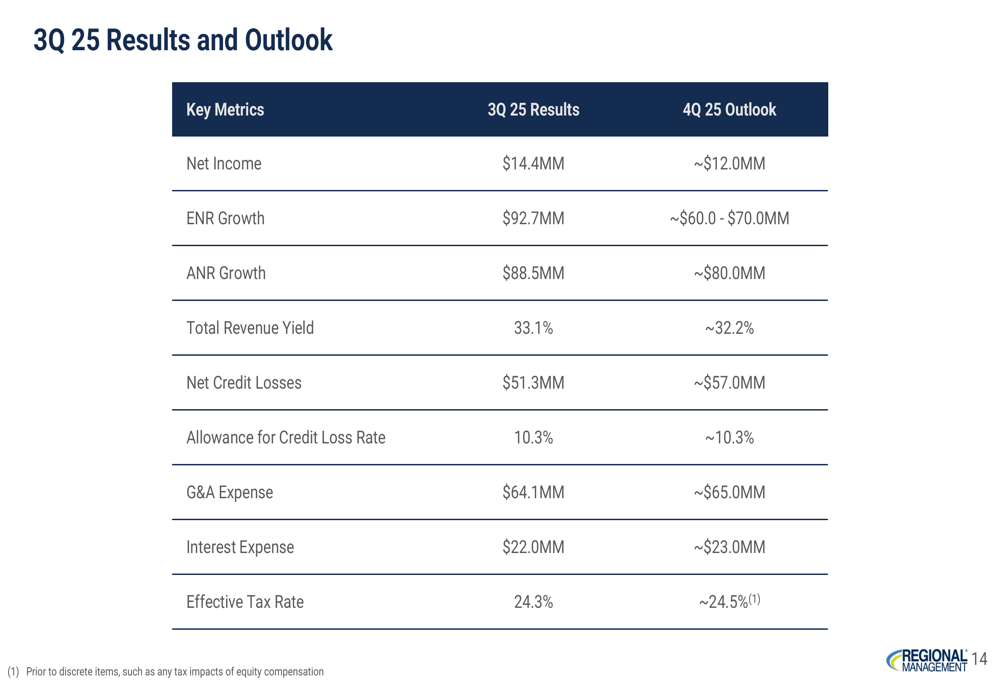

For Q4 2025, Regional Management provided the following outlook:

The company expects net income of approximately $12 million in Q4 2025, with ending net receivables growth of $60-70 million. Total revenue yield is projected to decrease slightly to 32.2%, while the allowance for credit loss rate is expected to remain stable at 10.3%.

According to the earnings call, Regional Management plans to open 5 new branches by the end of 2025 and an additional 5-10 branches in the first half of 2026, continuing its geographic expansion strategy.

Executive Changes

While not mentioned in the presentation slides, the earnings call revealed that CEO Rob Beck announced his retirement, with Lockbier Lomba set to succeed him. During the call, Beck emphasized the company's commitment to "grow the company responsibly while increasing shareholder value."

CFO Harp Rana highlighted the efficiency of the company's new analytical models during the earnings call, noting that "Our new models are very efficient, and we're able to make use of them."

Despite the strong quarterly performance, investors should be mindful of potential risks including macroeconomic factors such as inflation and interest rates, execution risks associated with geographic expansion, competitive pressures in the consumer lending market, and regulatory changes affecting lending practices.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.