German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

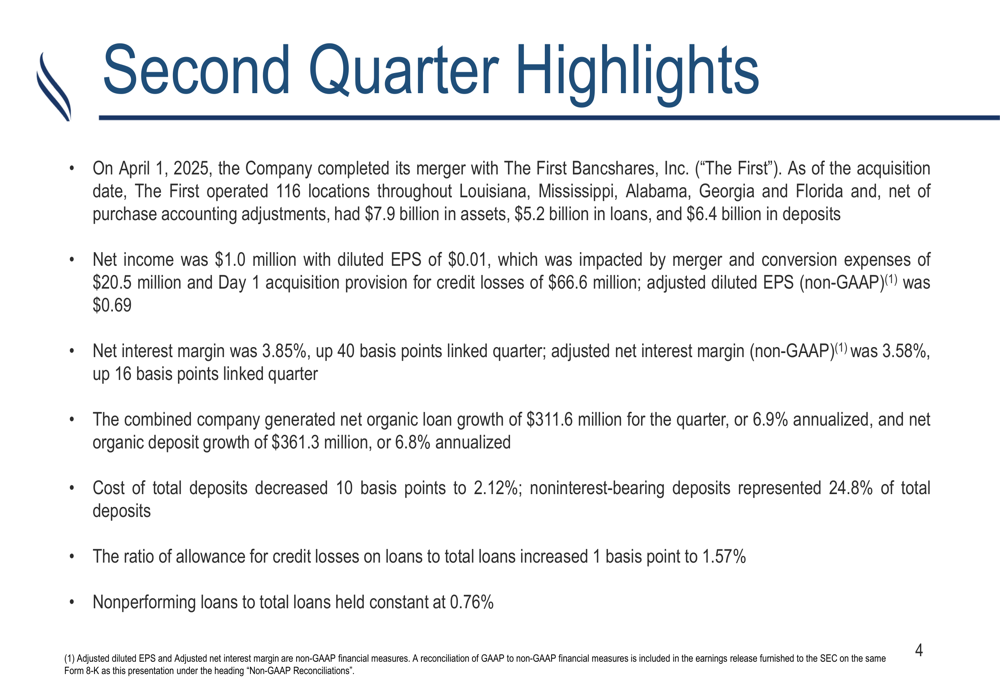

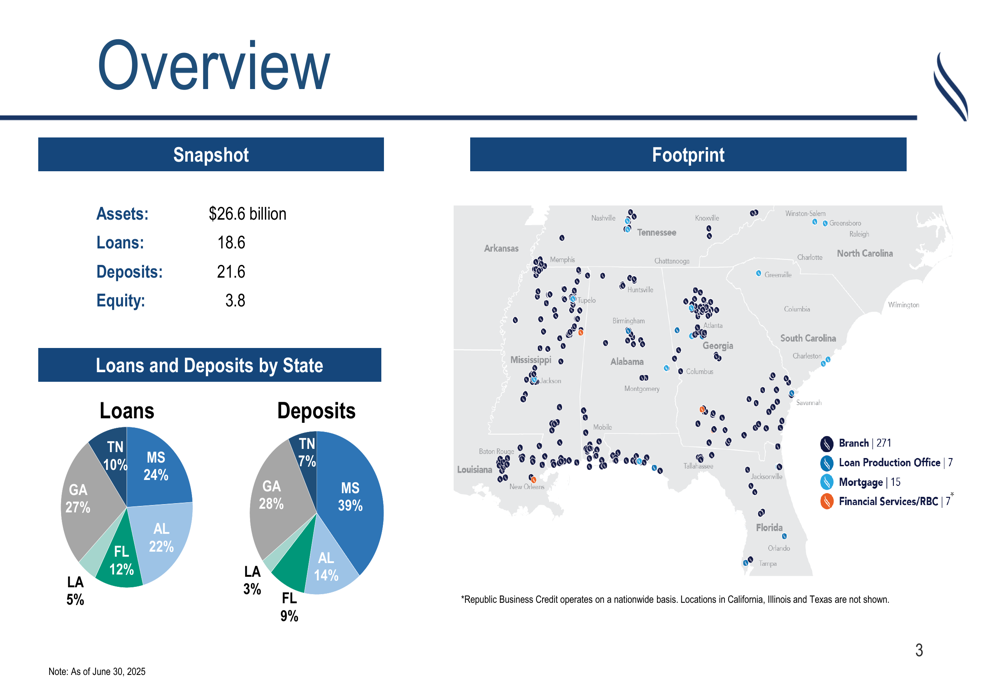

Renasant (NYSE:RNST) Corporation (NASDAQ:RNST) presented its second quarter 2025 earnings results, highlighting the completion of its merger with The First Bancshares (NYSE:FBMS) while demonstrating strong organic growth despite merger-related expenses. The acquisition has significantly expanded Renasant’s presence across the Southeastern United States, increasing its total assets to $26.6 billion.

The bank reported net income of $1.0 million, or $0.01 diluted EPS for Q2 2025, heavily impacted by merger and conversion expenses and Day 1 acquisition provisions. However, adjusted diluted EPS reached $0.69, matching the year-ago quarter despite the integration challenges.

Renasant’s stock closed at $38.46 on July 22, 2025, down 1.12% from the previous session, but remains near its 52-week high of $39.63, suggesting investor confidence in the company’s expansion strategy and underlying performance.

Quarterly Performance Highlights

The second quarter of 2025 showed significant improvement in key banking metrics despite merger-related disruptions. Net interest margin expanded to 3.85%, up 40 basis points from the linked quarter, while the adjusted net interest margin increased 16 basis points to 3.58%.

As shown in the following quarterly highlights:

Organic growth remained robust with net organic loan growth of $311.6 million (6.9% annualized) and net organic deposit growth of $361.3 million (6.8% annualized). This performance exceeded the "low single-digit loan growth" guidance provided during the Q1 2025 earnings call, demonstrating stronger-than-expected business momentum.

The cost of total deposits decreased 10 basis points to 2.12%, reflecting the company’s effective deposit management strategies in a competitive environment. Noninterest-bearing deposits represented 24.8% of total deposits, providing a stable, low-cost funding base.

Merger Integration and Financial Impact

The merger with The First Bancshares has transformed Renasant’s scale and geographic footprint, as illustrated in this overview:

The acquisition expanded Renasant’s presence across six southeastern states with 271 branches, 7 loan production offices, 15 mortgage locations, and 7 financial services offices. Georgia now represents the largest portion of the loan portfolio at 27%, followed by Mississippi at 24% and Alabama at 22%.

While the merger significantly enhanced Renasant’s scale, it also resulted in substantial one-time expenses. Merger and conversion costs totaled $20.5 million in Q2 2025, increasing $19.7 million from the previous quarter. Additionally, the company recorded Day 1 acquisition provisions, including $23.5 million for purchased credit deteriorated (PCD) loans and $62.2 million for non-PCD loans.

Management expects cost savings to materialize more fully in Q4 2025, with complete integration targeted for Q1 2026, consistent with guidance provided during the previous quarter’s earnings call.

Balance Sheet and Asset Quality

Renasant’s balance sheet expanded significantly year-over-year due to the merger, with total assets increasing from $17.51 billion in Q2 2024 to $26.63 billion in Q2 2025. Loans grew from $12.61 billion to $18.56 billion, while deposits increased from $14.26 billion to $21.58 billion during the same period.

The company maintained stable asset quality metrics despite the substantial growth, with nonperforming loans to total loans holding steady at 0.76%. The allowance for credit losses on loans to total loans increased slightly by 1 basis point to 1.57%, reflecting prudent risk management amid economic uncertainties.

Renasant’s deposit base demonstrates strong granularity, with an average deposit account balance of $35,000. The top 20 depositors (excluding public funds) comprise only 4.1% of total deposits, reducing concentration risk. The customer mix is well-balanced with consumers representing 50% of deposits, commercial clients 31%, and public funds 19%.

Profitability and Efficiency

Despite merger-related expenses, Renasant’s underlying profitability metrics showed improvement. Adjusted return on average assets (ROAA) increased to 1.01% in Q2 2025 from 0.90% in Q2 2024, while adjusted return on tangible common equity (ROTCE) jumped significantly to 11.56% from 6.68% a year ago.

The efficiency ratio improved slightly, with the adjusted efficiency ratio decreasing to 66% from 67% in the prior-year quarter, indicating enhanced operational effectiveness despite integration challenges. Pre-provision net revenue (PPNR) increased substantially, with adjusted PPNR rising to $84 million in Q2 2025 compared to $51.8 million in Q2 2024.

Net interest income (FTE) grew significantly to $207.6 million on an adjusted basis, up from $127.6 million in Q2 2024, primarily due to the expanded balance sheet following the merger and improved margins.

Liquidity and Capital Position

Renasant maintains a strong liquidity position with cash and securities representing 16.9% of total assets, down slightly from 18.5% in Q1 2025 but up from 15.9% in Q2 2024. The loans-to-deposits ratio stands at 86%, indicating ample funding capacity for future loan growth.

Available liquidity sources total $13.6 billion, well exceeding uninsured and uncollateralized deposits of $6.3 billion, providing a substantial buffer against potential funding pressures. The company’s securities portfolio, with an amortized cost of $3.7 billion, is diversified across agency mortgage-backed securities (28%), agency CMOs (30%), municipals (15%), and other securities.

The bank announced a $100 million stock repurchase program, though no buyback activity occurred during Q2 2025. This authorization provides flexibility for capital management as integration proceeds and synergies materialize.

Strategic Initiatives and Outlook

With the merger now complete, Renasant is focused on integration and realizing cost synergies. The company’s expanded footprint provides opportunities for growth across diverse markets in the Southeast, particularly in high-growth states like Georgia and Florida.

The mortgage banking segment showed resilience with income of $11.3 million in Q2 2025. Purchase mortgages represented 84% of originations, down from 91% a year ago but still indicating limited dependence on refinancing activity. The gain-on-sale margin improved to 1.87% from 1.69% in Q2 2024.

While the presentation did not provide specific forward guidance, the strong organic growth rates in loans and deposits, combined with expanding margins and stable asset quality, position Renasant well for continued performance improvement as merger-related expenses subside and operational synergies are realized.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.