Raymond James raises Fulgent Genetics stock price target to $36 on strong performance

Introduction & Market Context

The RMR Group Inc. (NASDAQ:RMR) released its fiscal fourth quarter 2025 results on November 13, 2025, revealing significant misses on both earnings per share and revenue expectations. The company’s stock closed at $15.60, up 0.83% on the day despite the earnings disappointment, though it showed weakness in premarket trading with a 0.32% decline.

The real estate asset management company reported adjusted earnings per share of $0.22, well below analyst expectations of $0.41, representing a 46.34% miss. Revenue came in at $159.41 million, significantly below the forecasted $210.1 million.

Quarterly Performance Highlights

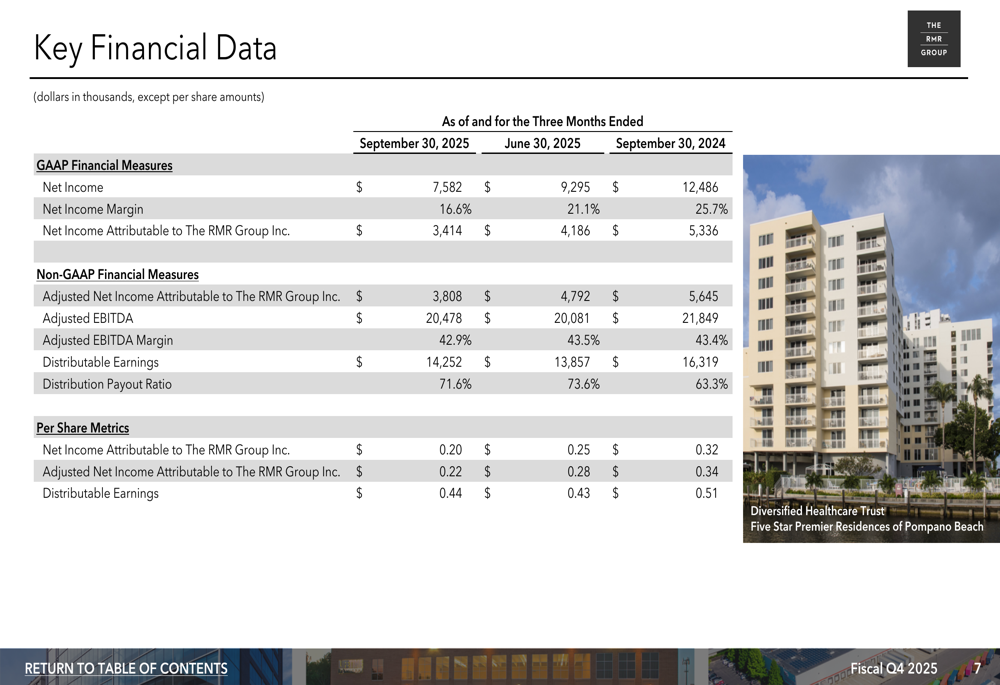

RMR Group reported net income of $7.6 million for Q4 2025, with a net income margin of 16.6%. Net income attributable to The RMR Group Inc. was $3.4 million, or $0.20 per diluted share. Adjusted Net Income, which excludes certain items, was $3.8 million or $0.22 per diluted share.

As shown in the following comprehensive financial data table, the company’s performance declined both sequentially and year-over-year:

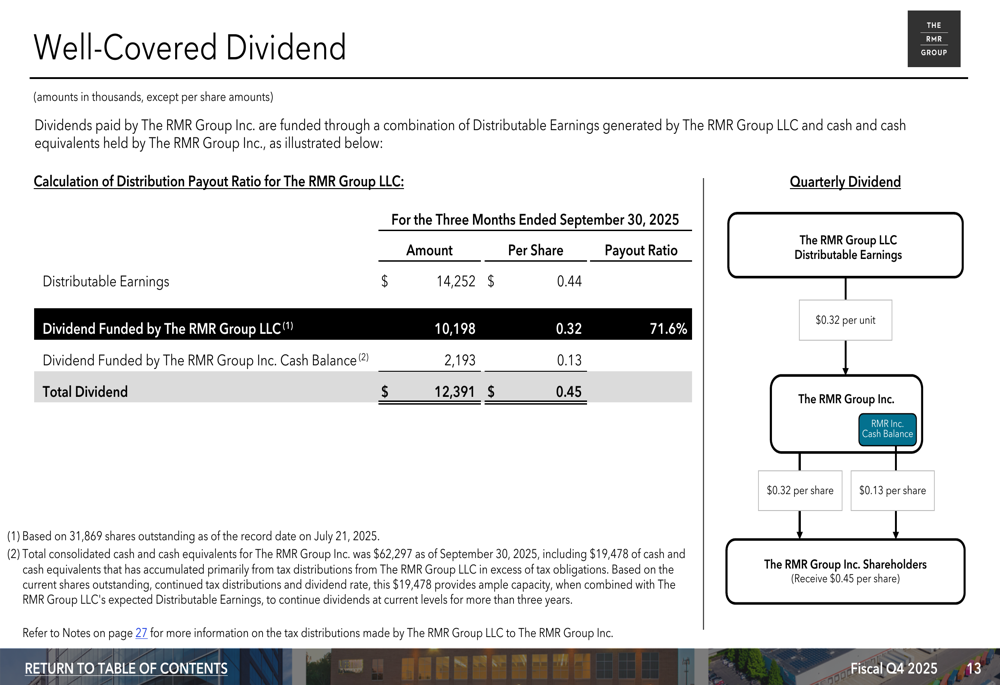

The company maintained its dividend at $0.45 per share, representing a distribution payout ratio of 71.6%. RMR’s dividend remains well-covered by its distributable earnings of $0.44 per share, as illustrated in the following flowchart:

Detailed Financial Analysis

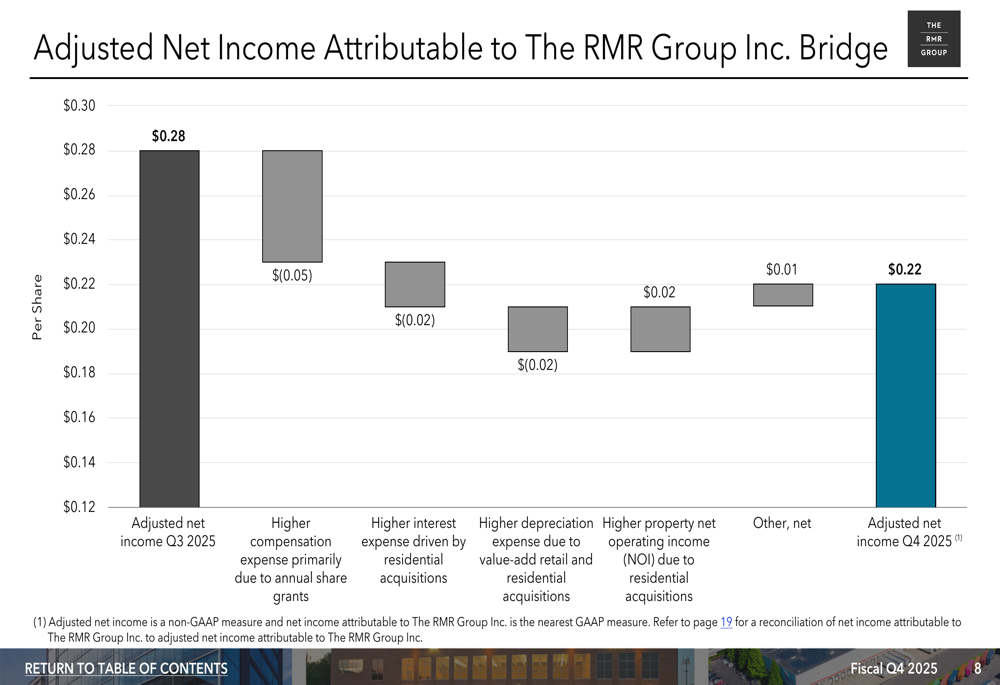

RMR’s financial performance showed notable declines across several key metrics. The adjusted net income per share decreased from $0.28 in Q3 2025 and $0.34 in Q4 2024 to $0.22 in the current quarter. The following bridge chart illustrates the factors contributing to this decline:

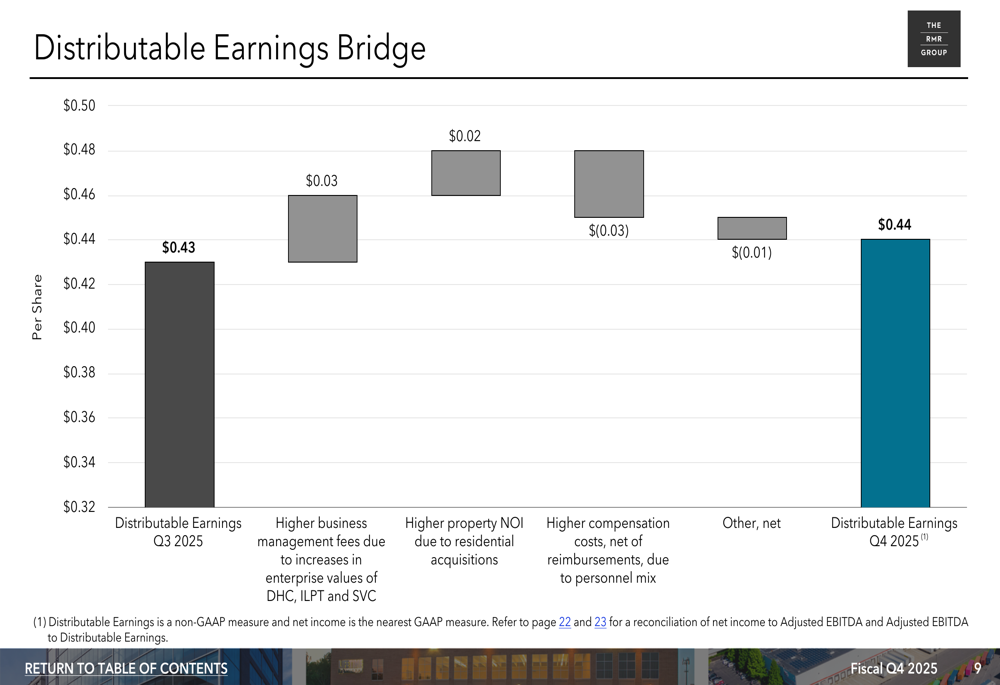

Despite the overall earnings decline, distributable earnings per share showed a slight improvement from $0.43 in Q3 2025 to $0.44 in Q4 2025, though still down from $0.51 in the same quarter last year. The following chart breaks down the components affecting distributable earnings:

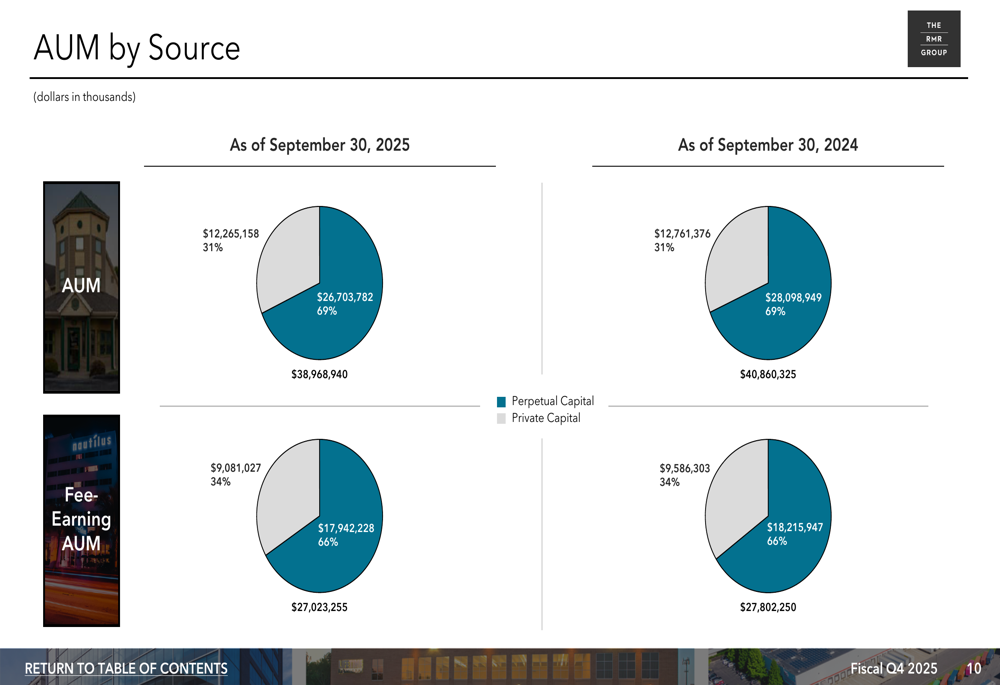

The company’s total Assets Under Management (AUM) stood at $39.0 billion as of September 30, 2025, down from $40.9 billion a year earlier. The AUM remains balanced between perpetual capital (69%) and private capital (31%), as shown in the following breakdown:

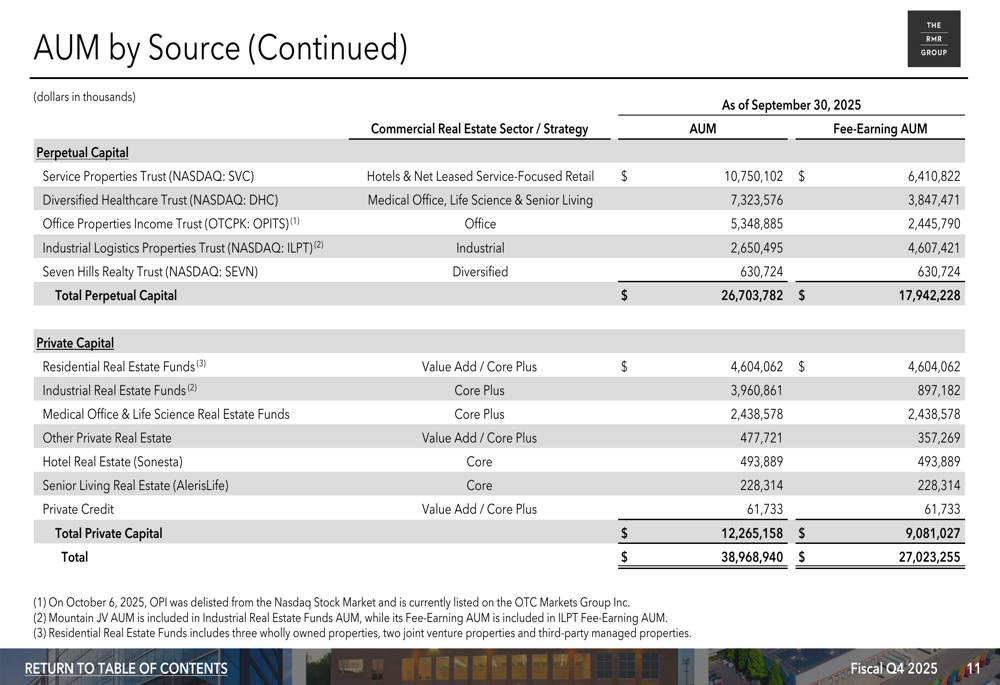

A more detailed analysis of AUM by source reveals the company’s diversified portfolio across various commercial real estate sectors:

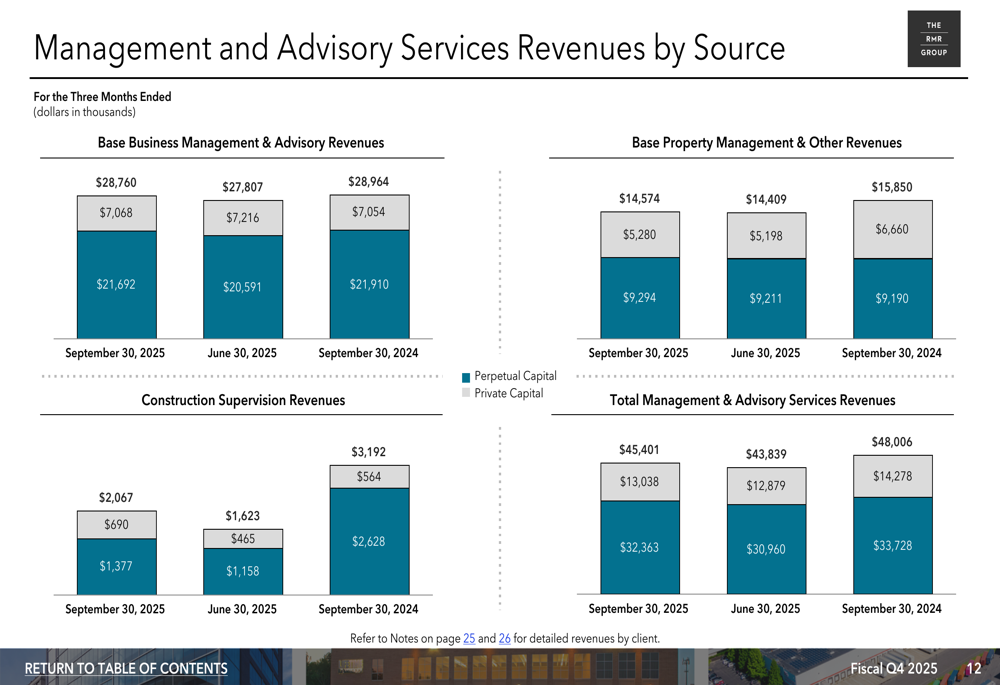

Management and advisory services revenues, a key income source for RMR, totaled $45.4 million for the quarter, down from $48.0 million in Q4 2024. The following chart illustrates the revenue composition:

Strategic Initiatives

Despite the earnings challenges, RMR highlighted several strategic initiatives during the quarter. The company acquired two garden-style apartment communities in Raleigh, NC and Orlando, FL for a combined $143.4 million, using cash on hand and $93.2 million in mortgage financing. This expansion into residential real estate aligns with the company’s strategy to diversify its portfolio.

CEO Adam Portnoy stated in the earnings release: "RMR’s fourth quarter results were consistent with our expectations, supported by continued improvements in the enterprise values of certain of our Managed REITs and incremental operating income contributed by recent residential acquisitions."

The company also announced plans to sell its loan portfolio to Seven Hills Realty Trust (NASDAQ:SEVN), which is expected to generate net proceeds of approximately $16.7 million, excluding closing costs.

Forward-Looking Statements

Looking ahead, RMR Group expects adjusted EBITDA for Q1 Fiscal 2026 to range between $18 million and $20 million, with distributable earnings projected at $0.42 to $0.44 per share. The company maintains a strong liquidity position with $162.3 million in total liquidity, including $62.3 million in cash and $100 million available on its revolving credit facility.

During the earnings call, COO Matt Jordan expressed optimism about the coming year, stating, "We believe 2026 will be a better year for institutional investments in real estate." CEO Adam Portnoy also highlighted the company’s interest in retail properties, noting that "Retail has really gone through transformation over the last 10 to 15 years."

However, the significant earnings miss raises questions about the company’s near-term performance and ability to meet future expectations. Investors will likely watch closely for signs of improvement in the coming quarters, particularly regarding the integration of recent acquisitions and the impact of strategic portfolio adjustments on the company’s bottom line.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.