S&P 500 eases slightly from fresh record high after stronger economic growth

Introduction & Market Context

RPM International Inc. (NYSE:RPM) reported record fourth-quarter and full-year 2025 results on July 24, 2025, showing a strong recovery from its disappointing third-quarter performance. The specialty chemicals company’s shares jumped 6.5% in premarket trading to $120.29, reflecting investor enthusiasm for the better-than-expected results.

The fourth-quarter performance marks a significant turnaround from the company’s third-quarter results, which had missed both earnings and revenue forecasts, sending the stock near its 52-week low. RPM’s recovery demonstrates the effectiveness of its operational efficiency initiatives and strategic positioning in key markets.

Quarterly Performance Highlights

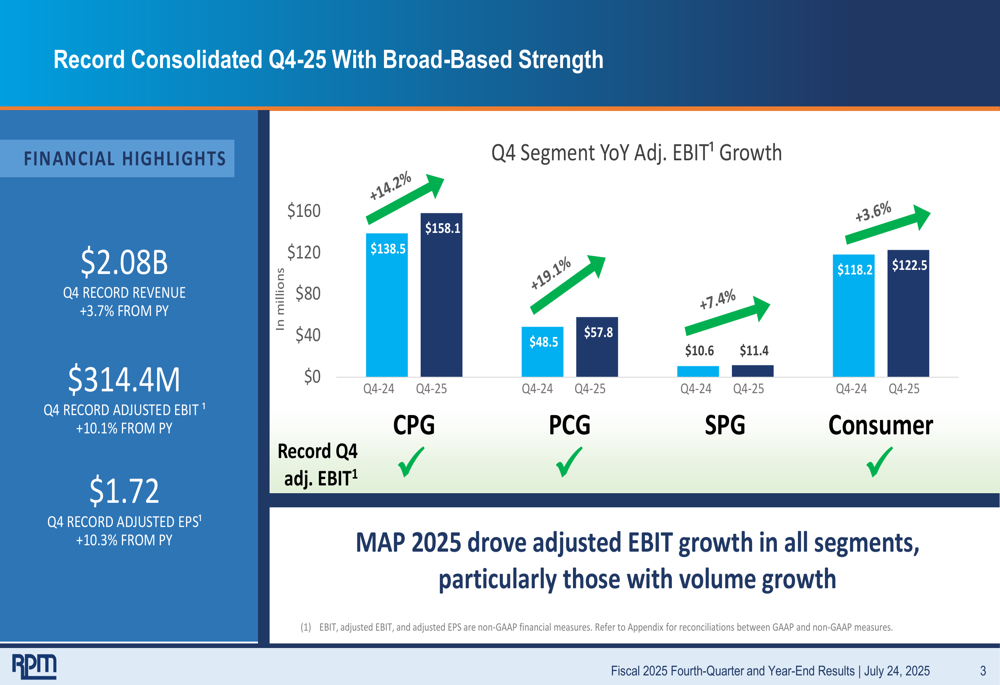

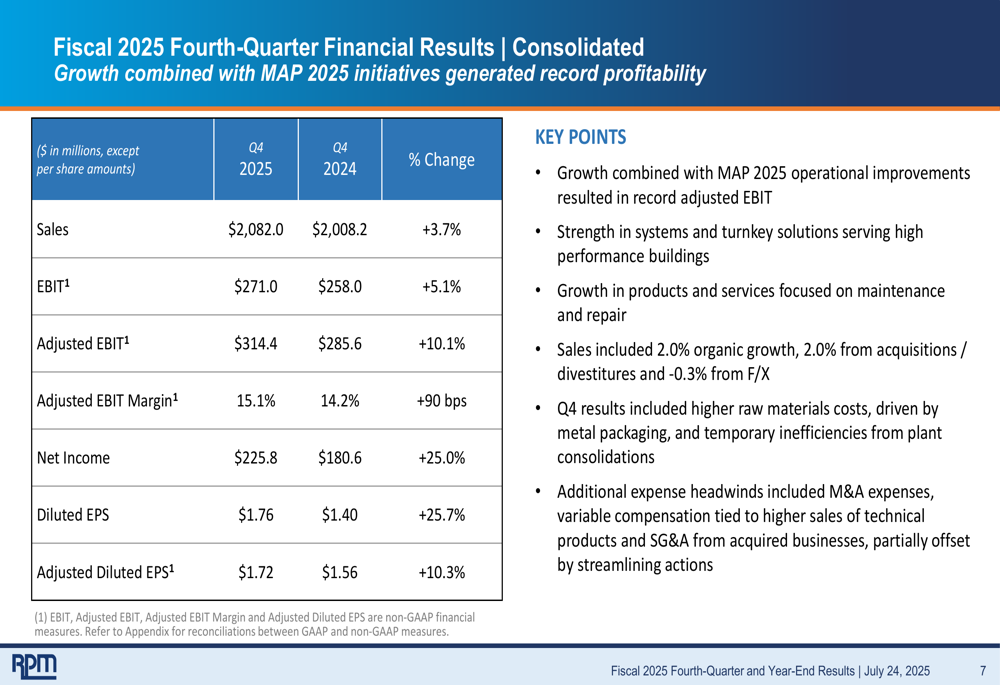

RPM achieved record fourth-quarter results with revenue of $2.08 billion, up 3.7% year-over-year, adjusted EBIT of $314.4 million, increasing 10.1%, and adjusted EPS of $1.72, rising 10.3% compared to the same period last year.

As shown in the following consolidated results chart:

All four segments delivered adjusted EBIT growth, with the Construction Products Group (CPG) and Performance Coatings Group (PCG) leading the way with increases of 14.2% and 19.1%, respectively. The Specialty Products Group (SPG) and Consumer Group also contributed with growth of 7.4% and 3.6%.

The company’s consolidated financial results show impressive margin expansion, with adjusted EBIT margin reaching 15.1% in Q4 2025, up 90 basis points from 14.2% in Q4 2024:

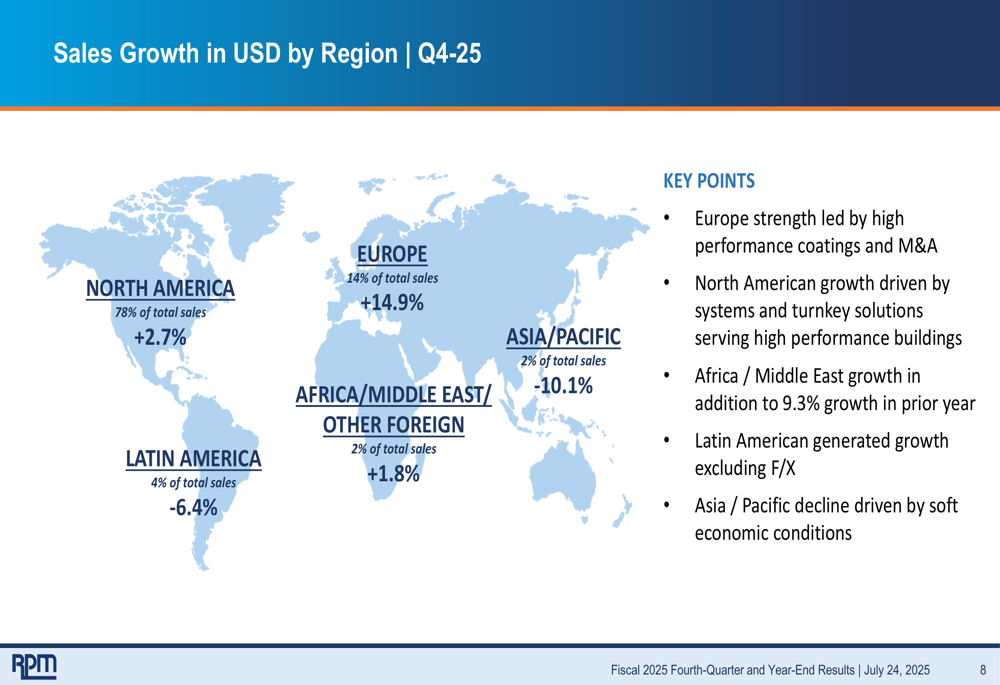

Regional performance varied significantly, with Europe showing the strongest growth at 14.9%, driven by high-performance coatings and acquisitions. North America, which accounts for 78% of total sales, grew by 2.7%, while Asia/Pacific and Latin America experienced declines of 10.1% and 6.4%, respectively:

Segment Performance

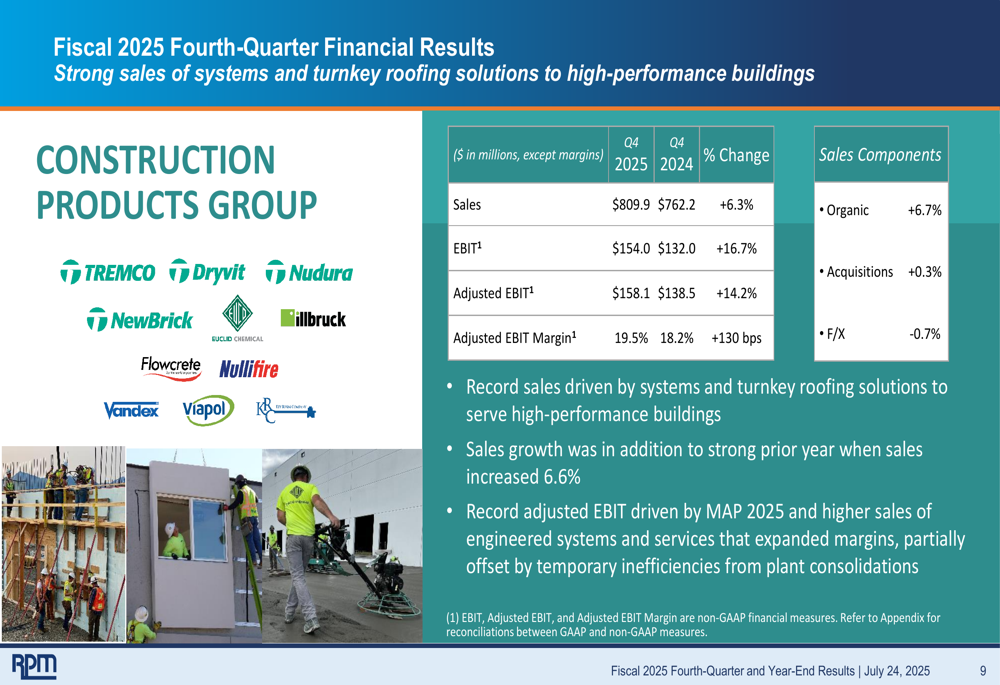

The Construction Products Group delivered the strongest performance among RPM’s segments, with sales increasing 6.3% to $809.9 million and adjusted EBIT rising 14.2% to $158.1 million. Organic growth of 6.7% was the primary driver, with record sales attributed to systems solutions:

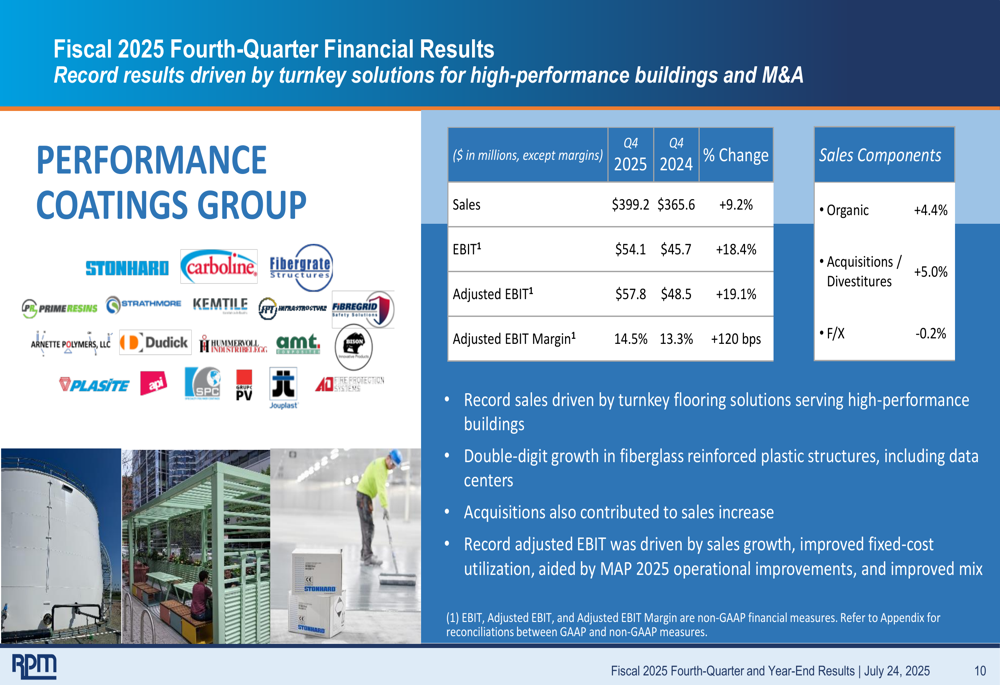

The Performance Coatings Group also showed robust growth, with sales up 9.2% to $399.2 million and adjusted EBIT increasing 19.1% to $57.8 million. This growth was driven by a combination of organic growth (4.4%) and acquisitions (5.0%):

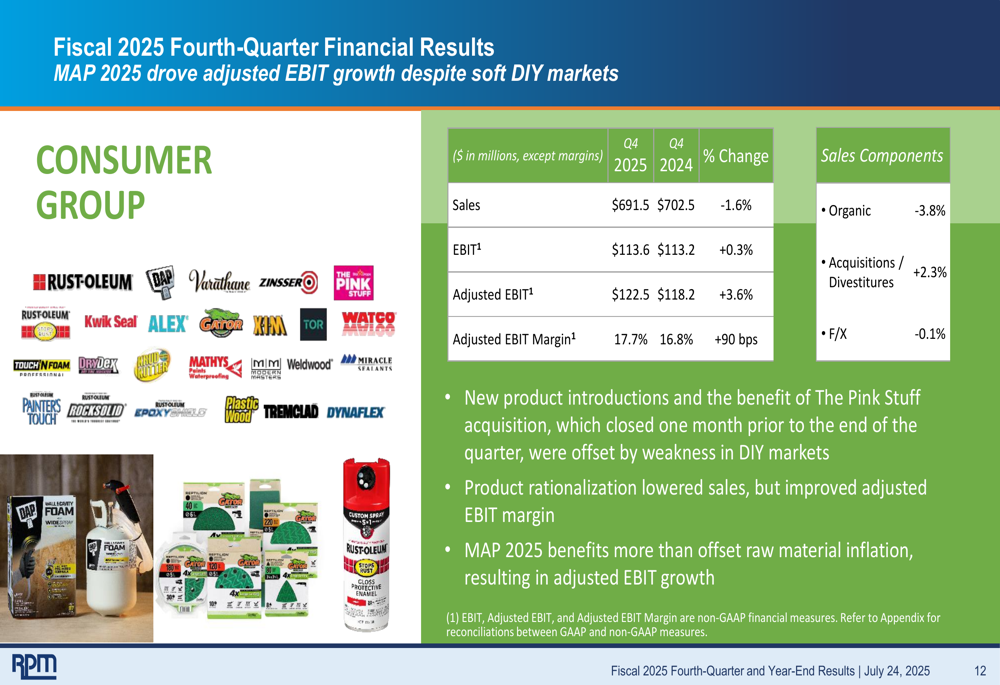

The Consumer Group, despite a 1.6% decline in sales to $691.5 million, managed to increase adjusted EBIT by 3.6% to $122.5 million, demonstrating effective margin management. The sales decline was attributed to a 3.8% decrease in organic growth, partially offset by 2.3% growth from acquisitions:

Strategic Initiatives

RPM’s MAP 2025 operational efficiency program has been a key driver of the company’s improved performance. The initiative has delivered significant improvements across multiple metrics, including a 510 basis point increase in gross margins, a 260 basis point increase in adjusted EBIT margins, and a 320 basis point improvement in working capital as a percentage of sales:

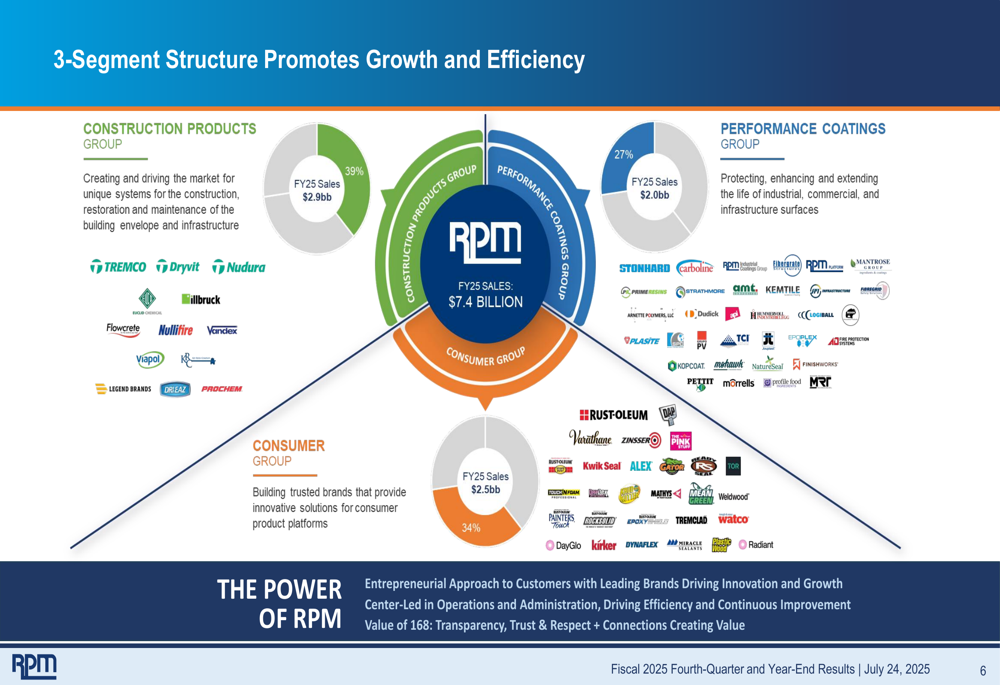

The company has restructured into three main segments – Construction Products Group (39% of FY25 sales), Performance Coatings Group (27%), and Consumer Group (34%) – to promote growth and operational efficiency:

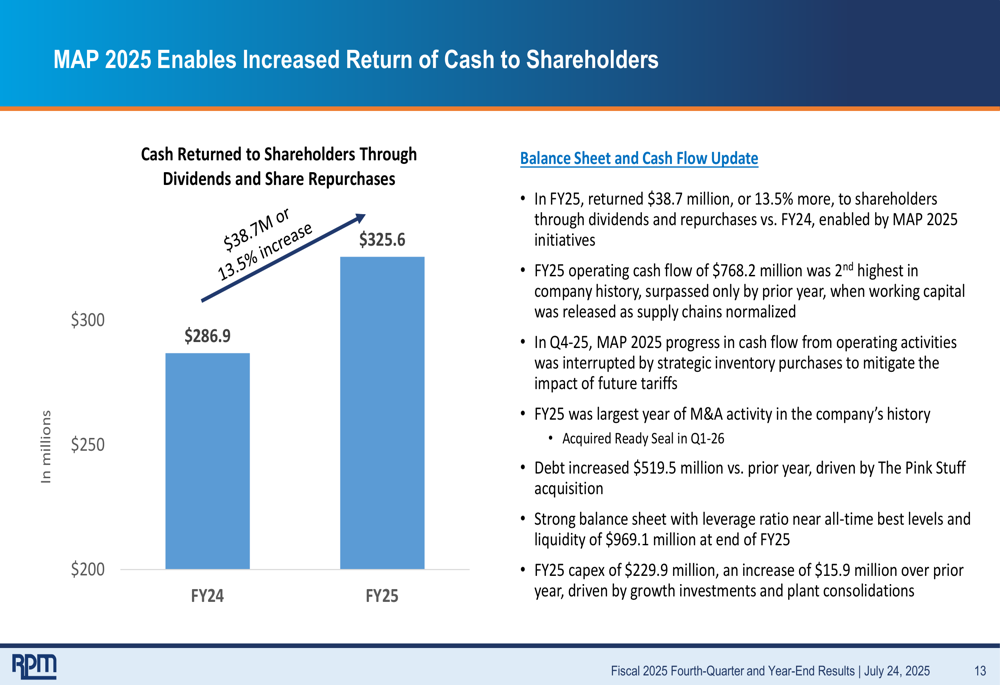

This reorganization has helped RPM increase cash returned to shareholders through dividends and share repurchases by 13.5% to $325.6 million in FY25, compared to $286.9 million in FY24:

Forward-Looking Statements

Looking ahead to fiscal year 2026, RPM expects consolidated sales to increase in the low-to-mid single digits, with adjusted EBIT projected to grow in the high single digits to low double digits. This outlook is supported by ongoing operating efficiency initiatives and pricing strategies, though tempered by economic uncertainty.

For the first quarter of fiscal 2026, the company anticipates similar growth rates, with sales expected to increase in the low-to-mid single digits and adjusted EBIT projected to grow at a similar pace. The Consumer segment is expected to show slightly higher sales growth due to merger and acquisition activity.

Conclusion

RPM’s fourth-quarter and full-year 2025 results demonstrate a strong recovery from its third-quarter challenges, with record performance across all segments. The company’s MAP 2025 initiatives have successfully driven margin expansion and operational efficiencies, positioning RPM well for continued growth in fiscal 2026 despite economic uncertainties.

The consistent improvement in adjusted EBIT margins, which reached an all-time record of 13.2% for the full fiscal year 2025, highlights the effectiveness of the company’s strategic focus on efficiency and high-potential opportunities. With a strong balance sheet and positive outlook, RPM appears well-positioned to continue delivering value to shareholders in the coming fiscal year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.