German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

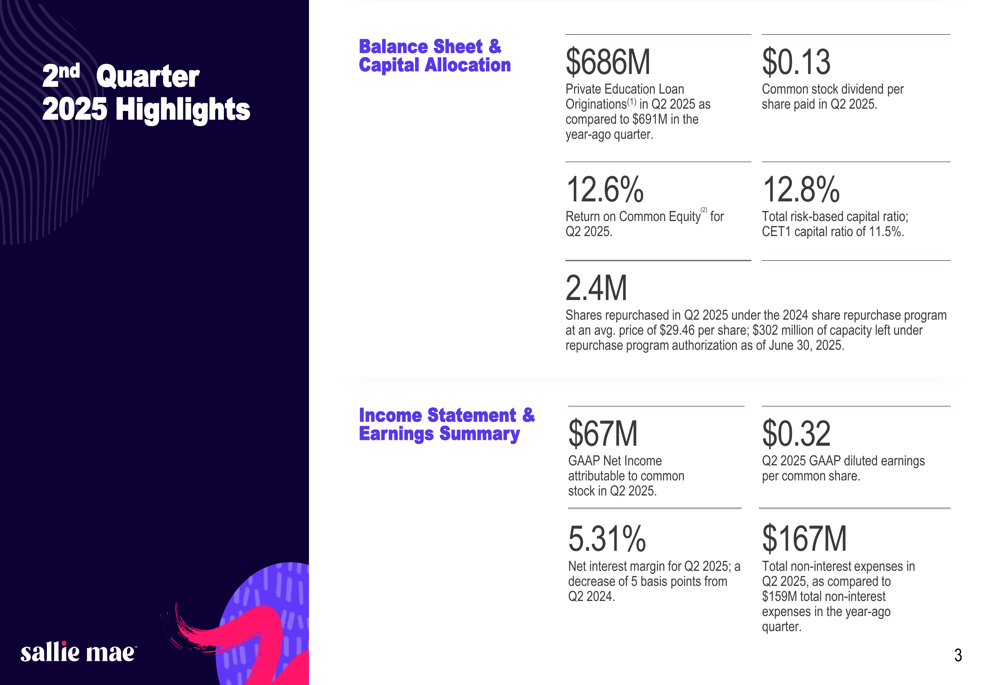

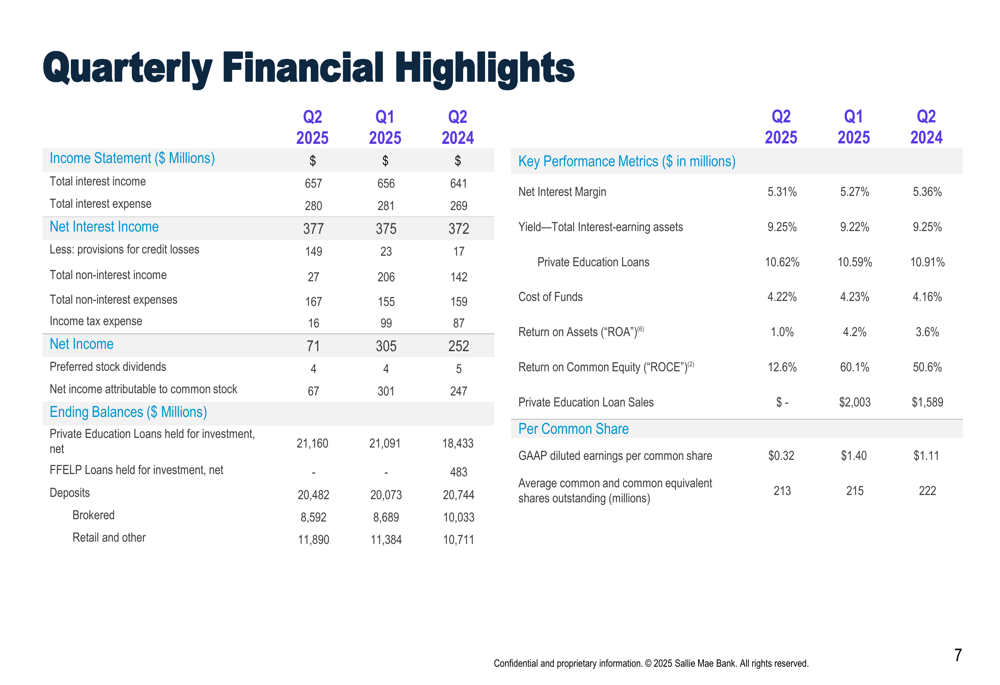

Sallie Mae (NASDAQ:SLM) released its second quarter 2025 earnings presentation on July 24, showing a significant decline in quarterly net income despite maintaining stable loan originations. The student loan provider reported GAAP net income of $67 million, substantially lower than the $305 million reported in the first quarter of 2025.

The company’s stock reflected investor concerns, with premarket trading showing a decline of 3.19% to $30.99 following the release. This reaction comes after SLM had demonstrated strong momentum earlier in the year, with its stock trading between a 52-week range of $19.39 and $34.97.

Quarterly Performance Highlights

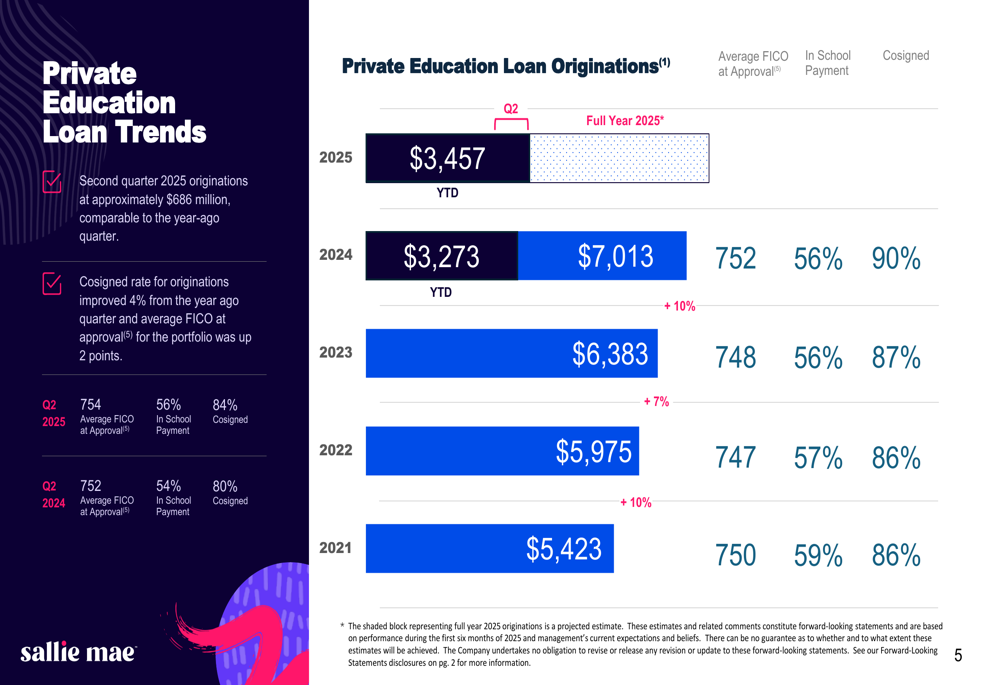

Sallie Mae reported private education loan originations of $686 million for Q2 2025, continuing its growth trajectory from previous years. The company maintained a return on common equity of 12.6% and declared a common stock dividend of $0.13 per share.

As shown in the following key financial metrics summary:

The company’s capital position remained solid with a total risk-based capital ratio of 12.8% and CET1 capital ratio of 11.5%. During the quarter, SLM repurchased 2.4 million shares, demonstrating its commitment to returning capital to shareholders.

However, the net interest margin decreased slightly to 5.31% in Q2 2025 from 5.36% in the same quarter last year, while total non-interest expenses reached $167 million.

Credit Performance and Loan Originations

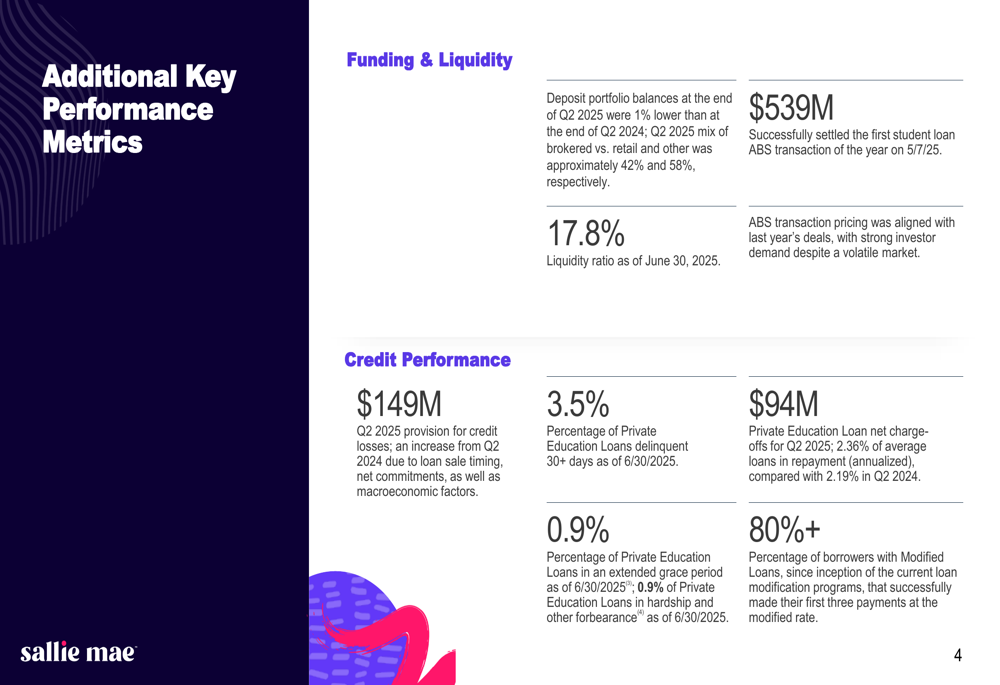

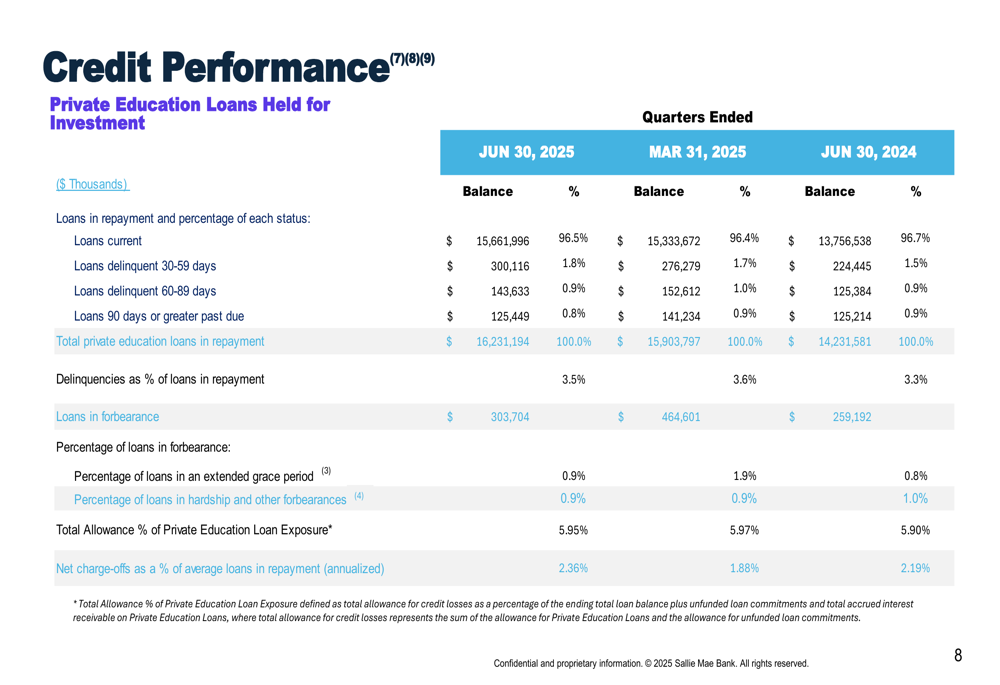

Sallie Mae’s credit metrics showed some pressure in the second quarter, with a provision for credit losses of $149 million. Private education loans delinquent 30+ days stood at 3.5% as of June 30, 2025, slightly lower than the 3.6% reported in Q1 2025. Net charge-offs for private education loans reached $94 million during the quarter.

The following slide illustrates the company’s private education loan origination trends:

The data shows consistent growth in loan originations from 2021 through projected 2025 figures. Notably, the cosigned rate for originations improved by 4% from the year-ago quarter, and the average FICO score at approval improved by 2 points, indicating enhanced credit quality of new borrowers.

Additional performance metrics reveal that deposit portfolio balances at the end of Q2 2025 were 1% lower than at the end of Q2 2024, while the liquidity ratio as of June 30, 2025, stood at 17.8%.

Federal Student Loan Reform Impact

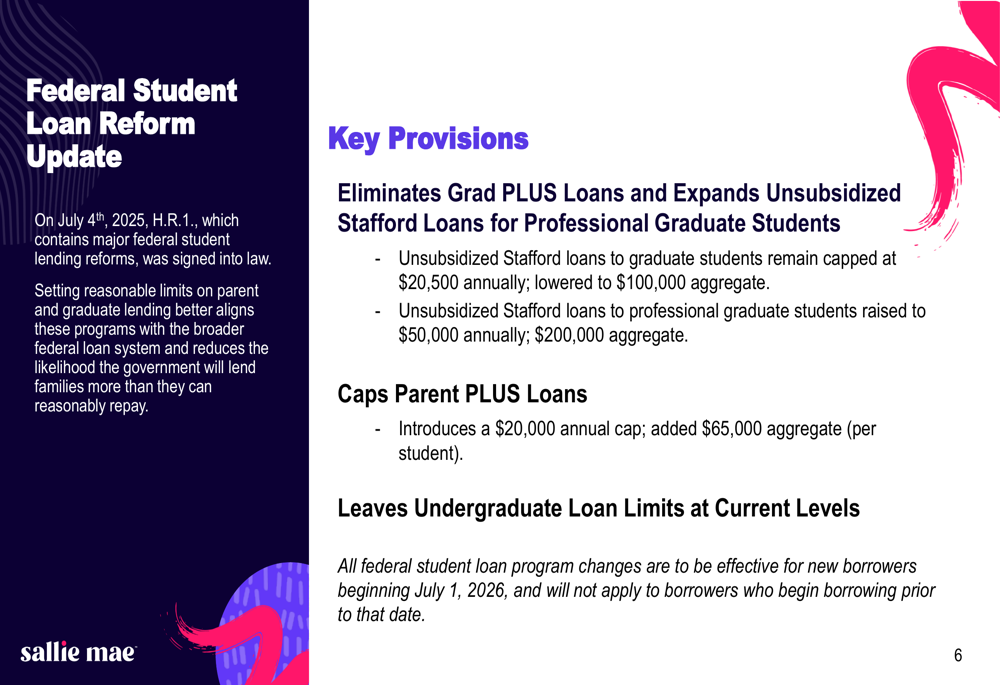

A significant development highlighted in the presentation is the Federal Student Loan Reform, with H.R.1 signed into law on July 4, 2025. This legislation introduces substantial changes to federal student lending programs, potentially creating opportunities for private lenders like Sallie Mae.

The reform’s key provisions include:

These changes, effective for new borrowers beginning July 1, 2026, could drive increased demand for private education loans as federal loan options become more restricted, particularly for graduate students and parents. This regulatory shift represents a potential long-term growth catalyst for Sallie Mae’s core business.

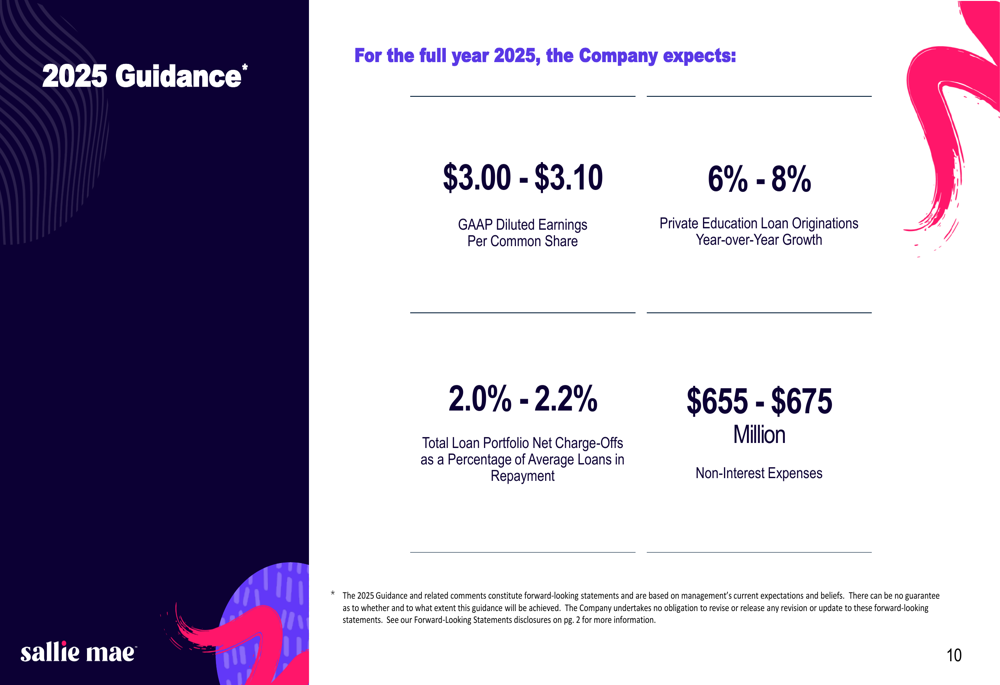

2025 Guidance and Outlook

Despite the quarterly performance fluctuations, Sallie Mae maintained its full-year 2025 guidance:

The company expects GAAP diluted earnings per common share to be between $3.00 and $3.10, with private education loan originations projected to grow between 6% and 8% year-over-year. Total (EPA:TTEF) loan portfolio net charge-offs as a percentage of average loans in repayment are expected to range between 2.0% and 2.2%, while non-interest expenses are projected to be between $655 and $675 million.

This maintained guidance suggests management’s confidence in the company’s ability to navigate the current economic environment despite the significant drop in quarterly earnings. The company’s financial position is further detailed in the quarterly financial highlights:

Credit Quality Assessment

Sallie Mae’s credit performance metrics provide insight into the quality of its loan portfolio and potential future risks. The detailed breakdown of delinquency rates and forbearance status shows:

The total allowance for credit losses as a percentage of private education loan exposure remained relatively stable at 5.95%, slightly down from the previous quarter. This suggests the company is maintaining consistent underwriting standards despite economic uncertainties.

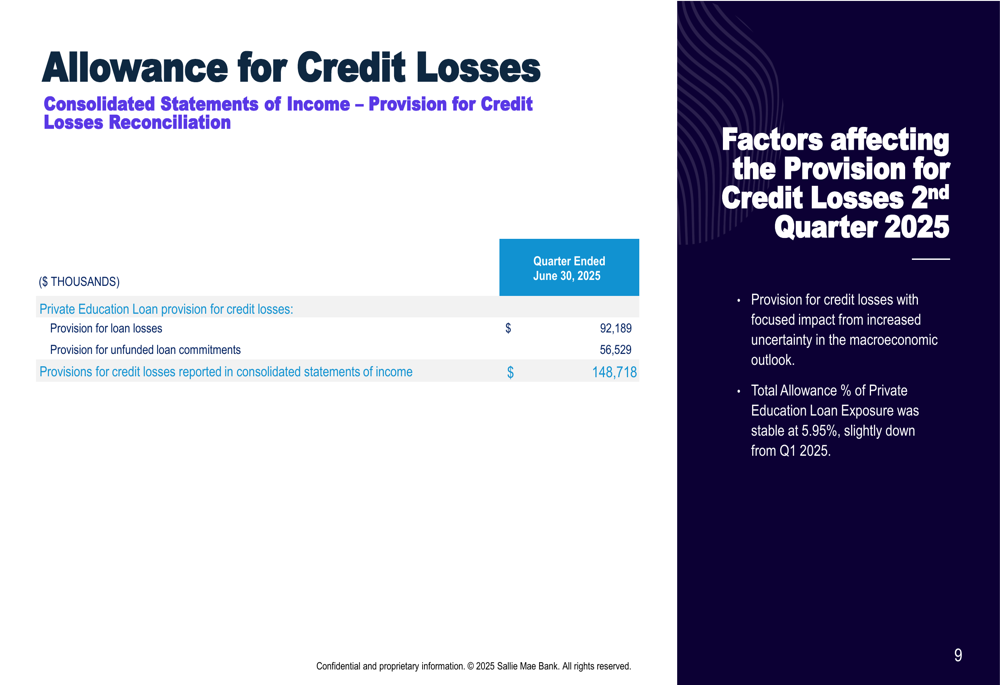

The company’s approach to credit loss provisions is further explained in the following slide:

The $148.7 million provision for credit losses in Q2 2025 reflects increased uncertainty in the macroeconomic outlook, a factor that likely contributed to the significant decline in quarterly net income compared to the previous quarter.

While Sallie Mae’s Q2 2025 results show a substantial decline in net income from the previous quarter, the company’s maintained guidance and stable loan originations suggest management views this as a temporary fluctuation rather than a long-term trend. The upcoming federal student loan reforms may provide tailwinds for private education lenders like Sallie Mae in the coming years, potentially offsetting current challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.