Tesla could be a $10,000 stock in a decade, says longtime bull Ron Baron

Introduction & Market Context

Finnish insurance group Sampo Oyj (HEL:SAMPO) presented its third-quarter 2025 results on November 5, showing robust performance across its business segments despite challenging market conditions. The company’s stock closed at €72.88, down 2.28% on the day, suggesting investors may have already priced in the positive results or remained cautious about broader market trends.

The presentation highlighted Sampo’s continued momentum in private and SME insurance lines, with particularly strong growth in the Nordic region and UK markets. This performance comes amid moderating claims inflation and what management described as "rational competition" in Nordic markets, while navigating a "softening" UK motor insurance environment.

Quarterly Performance Highlights

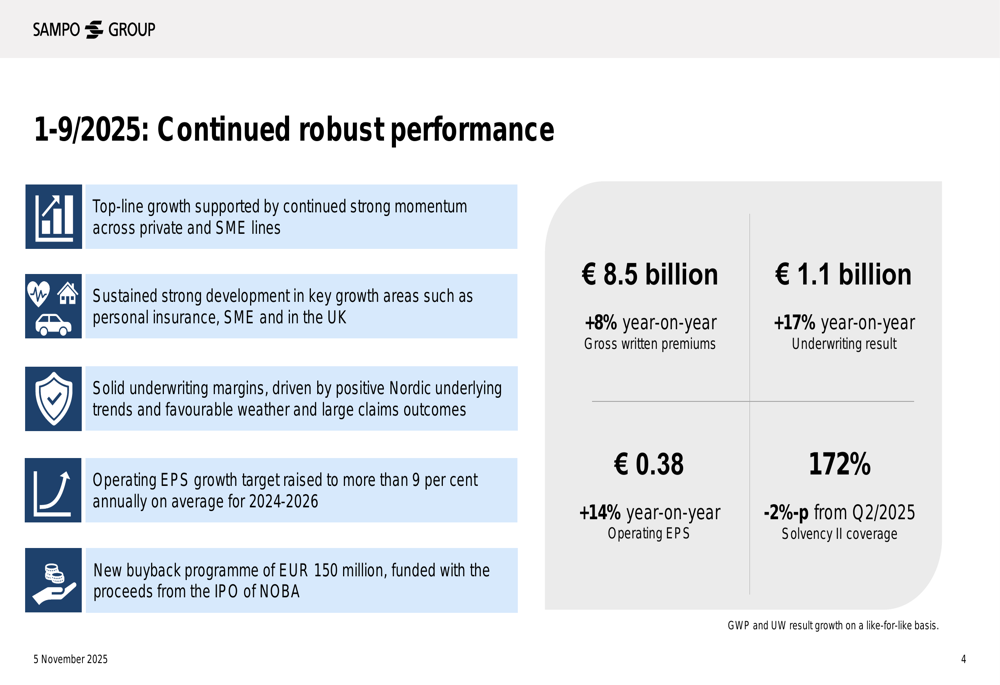

Sampo reported impressive financial metrics for the January-September 2025 period, with gross written premiums reaching €8.5 billion, an 8% year-on-year increase. The underwriting result grew by 17% to €1.1 billion, while operating earnings per share increased by 14% to €0.38.

As shown in the following chart of key financial highlights, the company demonstrated strong performance across its core metrics:

The company’s solvency ratio stood at 172%, slightly down by 2 percentage points from Q2 2025 but still indicating a strong capital position. This solid performance enabled Sampo to announce a new share buyback program of €150 million, funded by proceeds from the IPO of NOBA.

Segment Performance Analysis

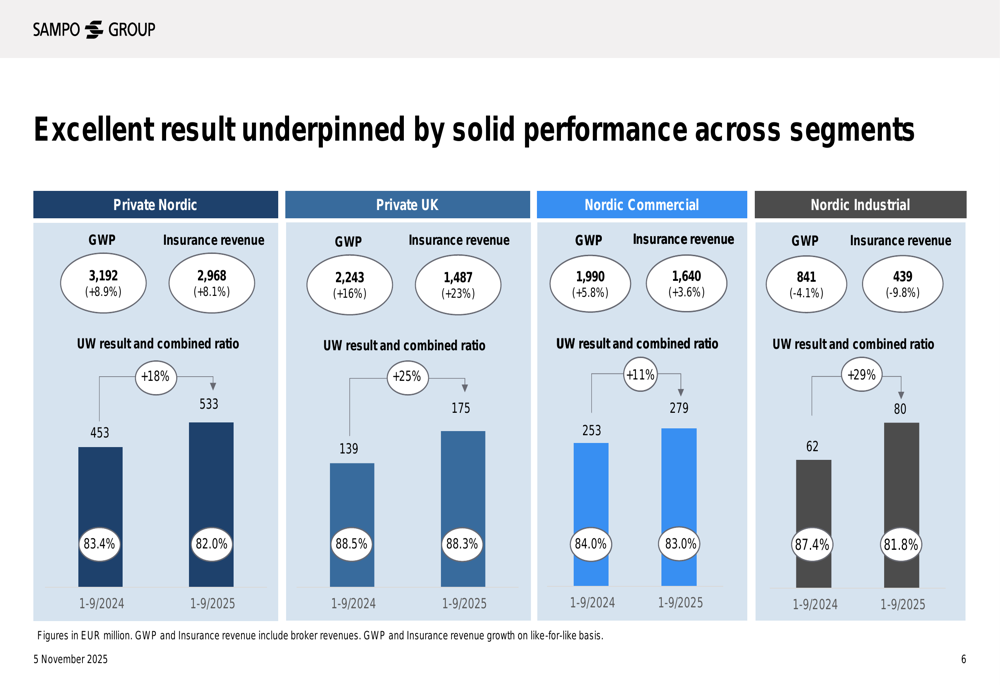

Sampo’s presentation provided a detailed breakdown of performance across its key business segments, all of which showed improvement in underwriting results and combined ratios.

The following chart illustrates the excellent performance across segments:

The Private Nordic segment showed particularly strong momentum with an 8.9% increase in gross written premiums and an 18% improvement in underwriting result. The combined ratio improved from 83.4% to 82.0%, indicating better profitability.

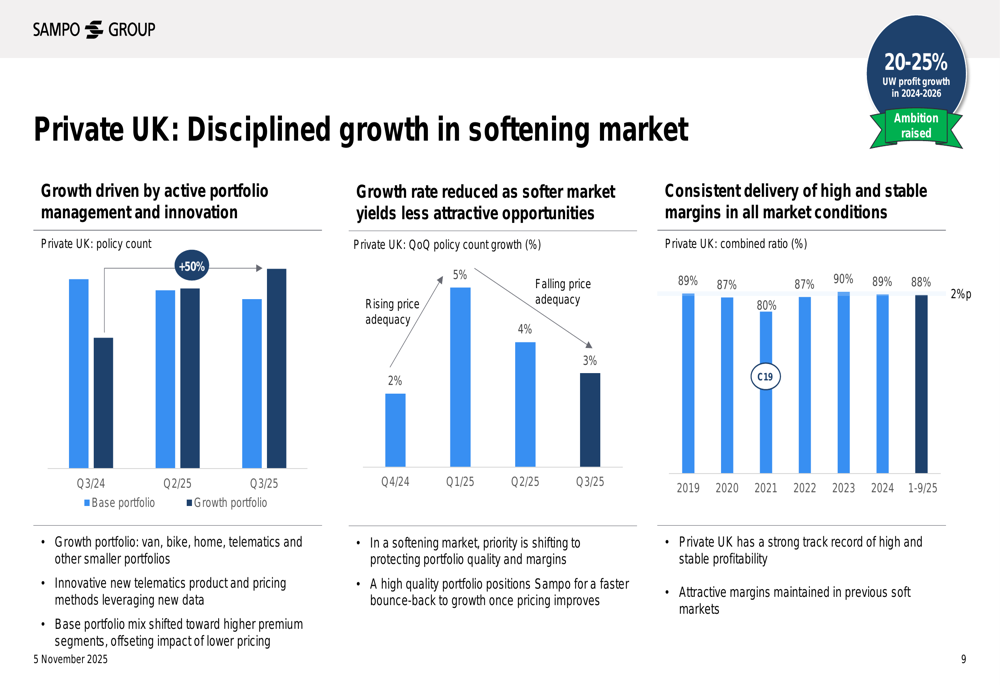

Private UK continued its impressive growth trajectory with a 16% increase in gross written premiums and a 25% jump in underwriting result. Despite operating in what management described as a "softening market," the segment maintained disciplined growth and improved its combined ratio slightly to 88.3%.

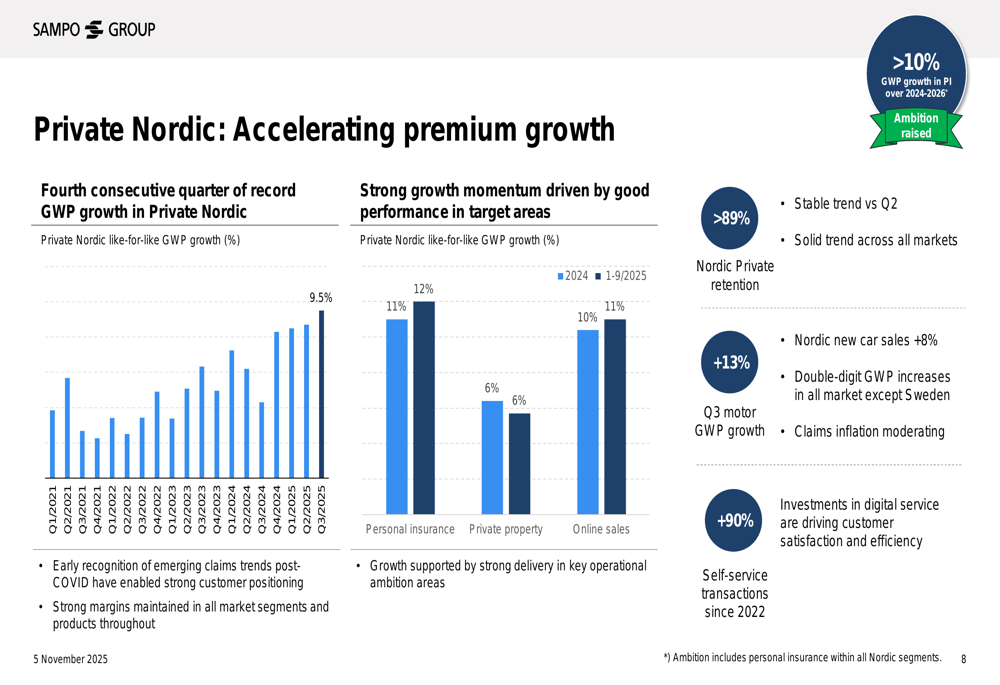

The following chart demonstrates Private Nordic’s accelerating premium growth:

In the UK market, Sampo has maintained disciplined growth despite challenging conditions, as illustrated in this chart:

Nordic Commercial also performed well with a 5.8% increase in gross written premiums and an 11% improvement in underwriting result. The combined ratio improved from 84.0% to 83.0%.

Perhaps most impressive was the Nordic Industrial segment, which achieved a 29% increase in underwriting result despite a 4.1% decline in gross written premiums, improving its combined ratio significantly from 87.4% to 81.8%.

Strategic Initiatives

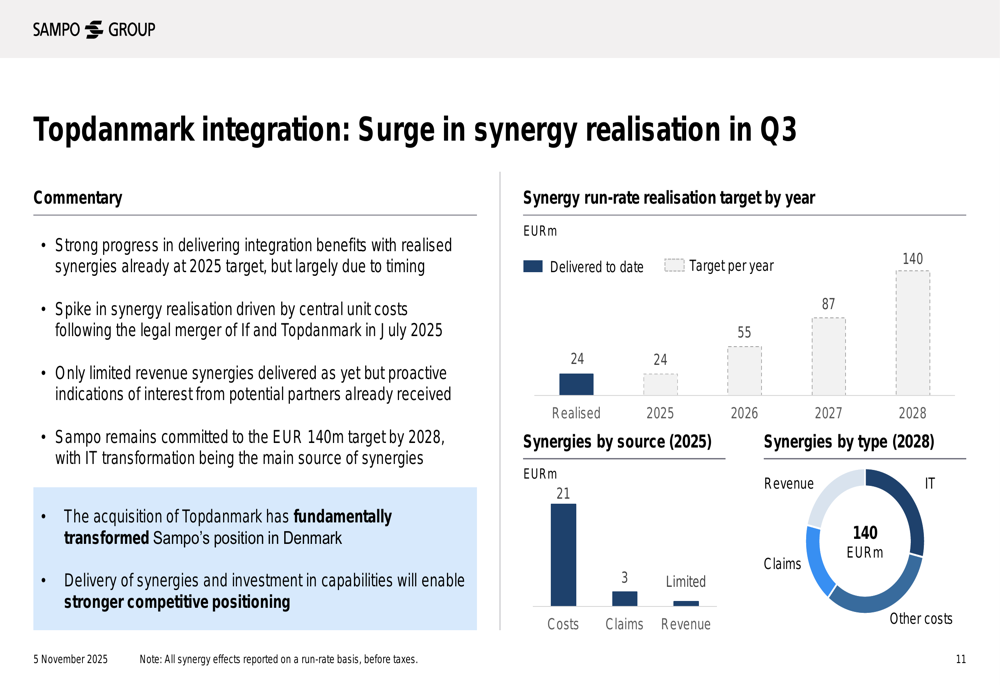

The presentation highlighted several strategic initiatives that contributed to Sampo’s strong performance. The integration of Topdanmark is progressing ahead of schedule, with synergy realization already reaching the 2025 target following the legal merger in July 2025.

The following chart illustrates the progress in Topdanmark integration:

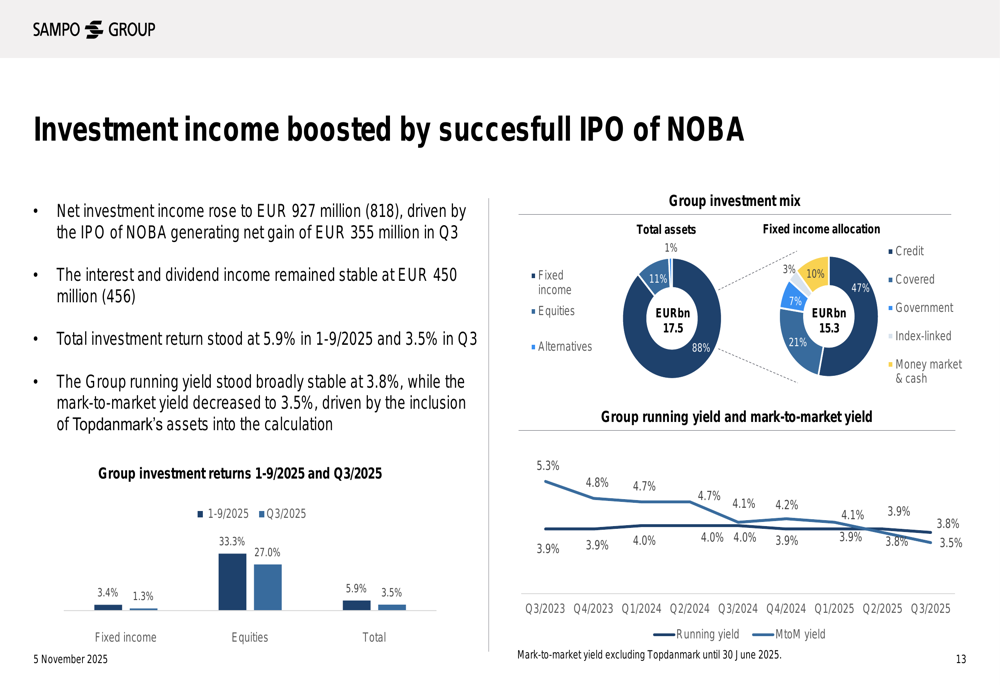

Another significant strategic development was the successful IPO of NOBA, which generated a €355 million gain for Sampo. This contributed to a substantial boost in investment income, which rose to €927 million. The company plans to use €150 million of these proceeds for share buybacks.

As shown in the following chart, the investment income was significantly boosted by the NOBA IPO:

Forward-Looking Statements

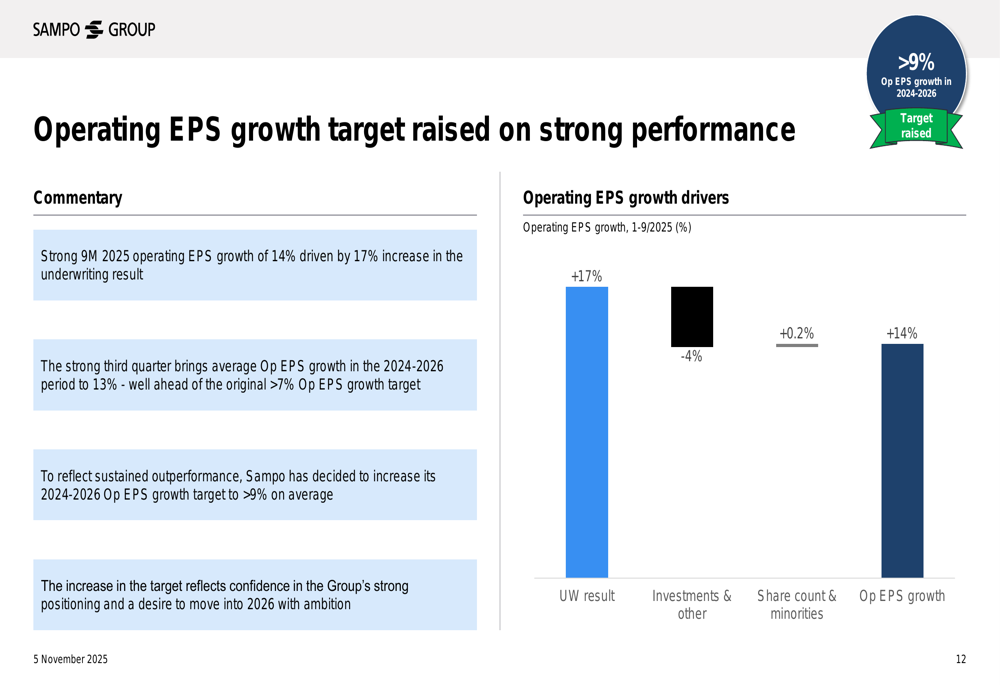

Based on its strong performance, Sampo has raised its operating EPS growth target for 2024-2026 to more than 9% annually on average, up from the previous target of more than 7%. This increase reflects management’s confidence in the company’s growth strategy and operational improvements.

The following chart illustrates the drivers behind the raised EPS growth target:

During the earnings call, CEO Morten Thorsrud expressed confidence in the company’s organic growth strategy, stating, "We are in a great position as a group. Our results show that we have an organic growth strategy that is working." He emphasized that the company is "only interested in growing, of course, at attractive margins."

Potential challenges mentioned during the call include the impact of Storm Amy, estimated at €30-40 million, and the declining pricing trends in the UK motor market. Despite these challenges, management remains optimistic about continued growth in both private and commercial segments.

With strong performance across segments, successful strategic initiatives, and raised guidance, Sampo appears well-positioned to continue its growth trajectory. However, investors will be watching closely to see if the company can maintain this momentum amid evolving market conditions and potential weather-related claims.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.