US LNG exports surge but will buyers in China turn up?

Introduction & Market Context

Saratoga Investment Corp . (NYSE:SAR) released its fiscal year-end and fourth quarter 2025 presentation on May 8, 2025, revealing mixed financial results with declining quarterly income metrics but maintained portfolio quality. The business development company’s stock faced downward pressure, with premarket trading showing a 7.01% decline to $22.95, following the previous day’s close of $24.68.

The presentation highlighted Saratoga’s continued focus on credit quality and long-term performance metrics, even as quarterly earnings showed signs of pressure. While the company maintained its dividend at $0.74 per share, investors appeared concerned about the declining net investment income per share, which fell to $0.56 in Q4 from $0.90 in the previous quarter.

Quarterly Performance Highlights

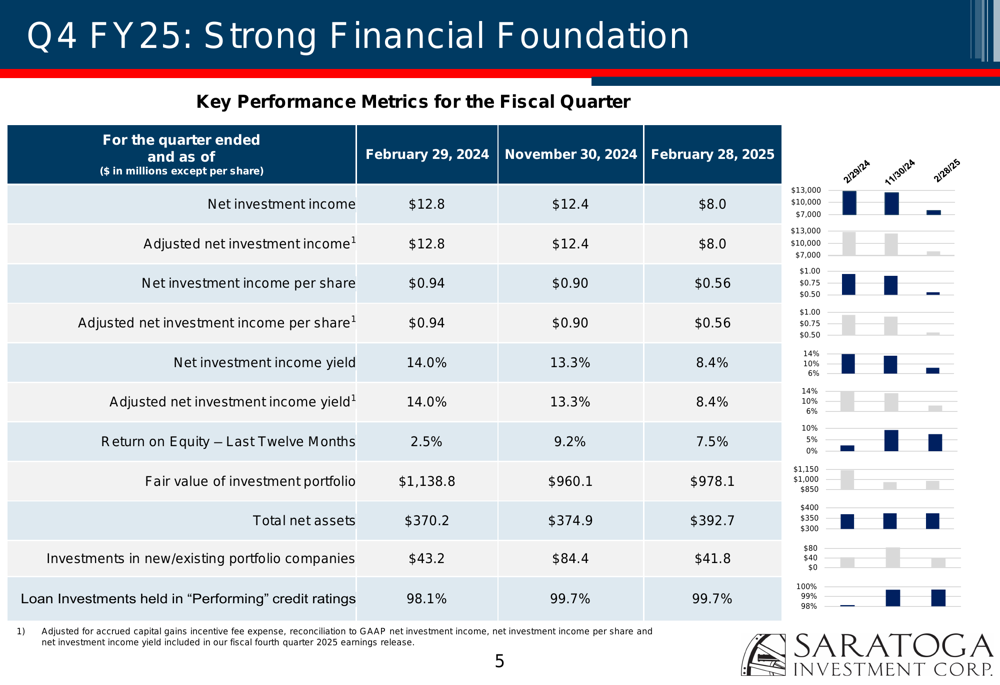

Saratoga reported adjusted net investment income (NII) of $8.0 million for Q4 FY25, down 35.4% from the previous quarter, with adjusted NII per share of $0.56, representing a 37.8% quarterly decline. The adjusted NII yield dropped to 8.4%, down 490 basis points from the previous quarter.

As shown in the following detailed quarterly performance metrics:

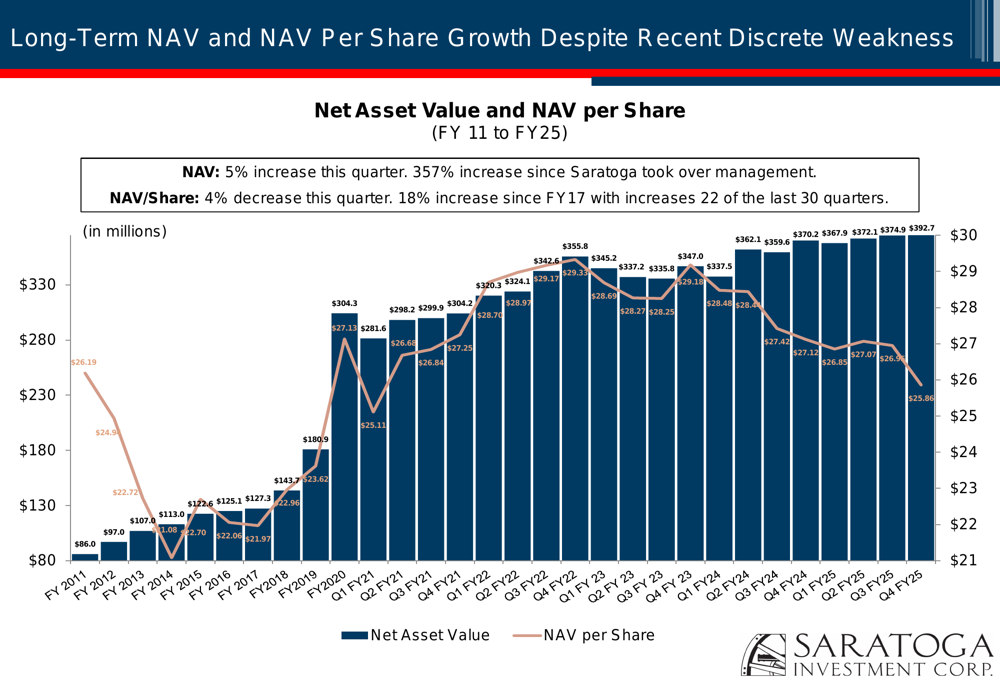

Despite the quarterly decline in NII, Saratoga’s net asset value (NAV) increased to $392.7 million, up $17.8 million or 4.7% from the previous quarter, though NAV per share decreased to $25.86, down $1.09 or 4.0%. The company maintained strong liquidity with $204.7 million in cash at quarter-end, providing significant dry powder for future investments.

The company’s long-term NAV and NAV per share growth chart illustrates the overall positive trajectory despite recent pressure:

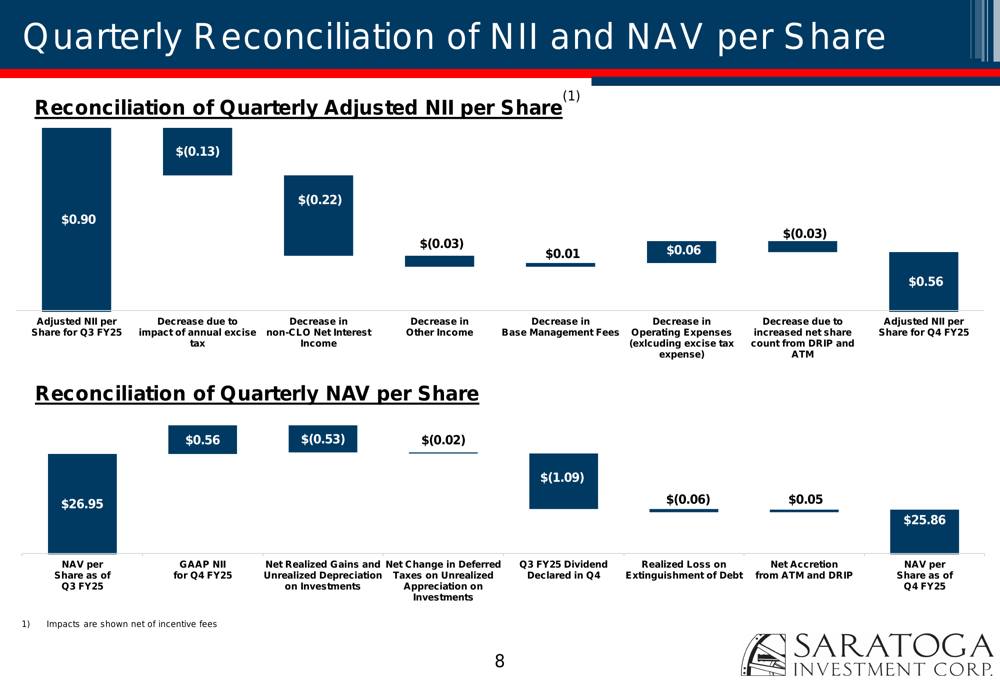

The quarterly reconciliation of NII and NAV per share provides insight into the factors affecting performance:

Portfolio Quality and Composition

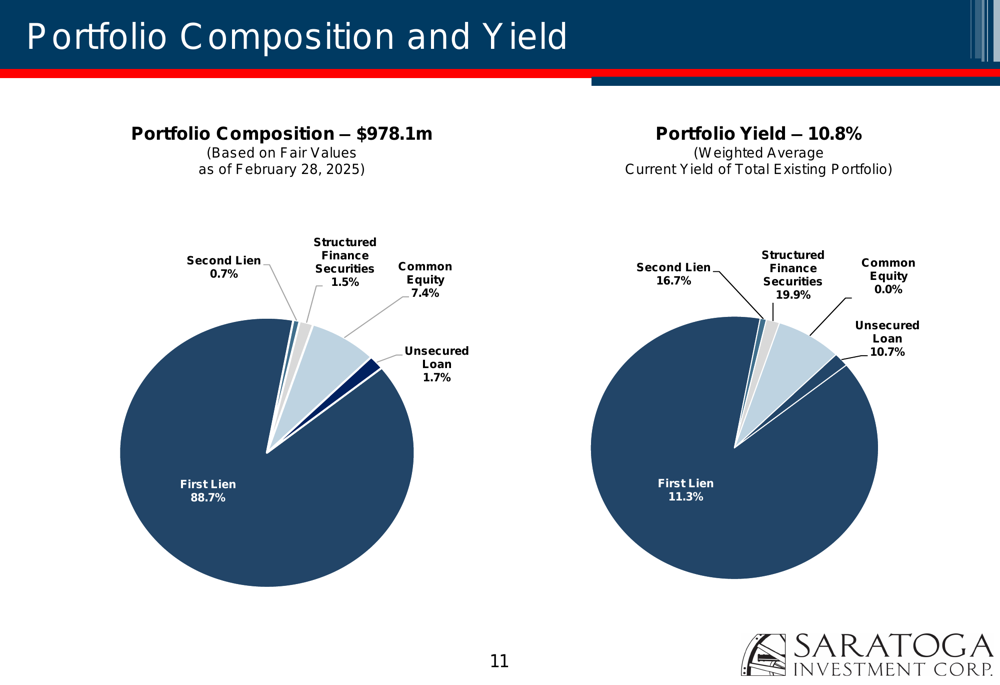

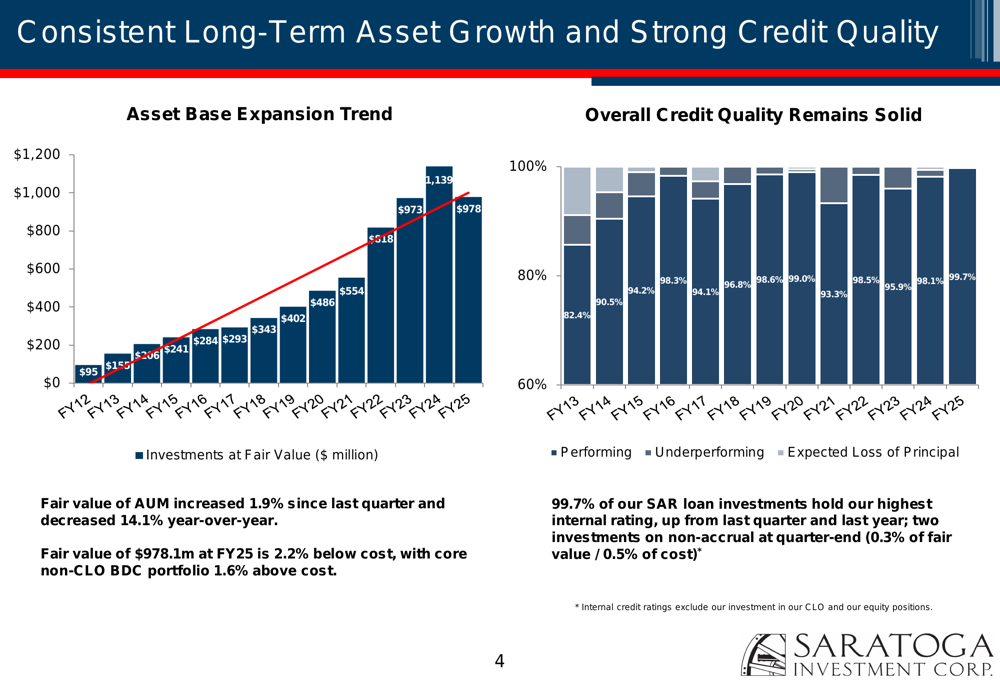

A key strength highlighted in Saratoga’s presentation was the exceptional quality of its investment portfolio. The company reported that 99.7% of loan investments maintained the highest internal rating, indicating minimal credit concerns despite broader market challenges.

Saratoga’s portfolio composition remains conservative, with 88.7% of investments in first lien debt, providing significant downside protection. The portfolio generated a weighted average yield of 10.8%, reflecting the company’s focus on quality income-generating assets.

The following chart illustrates the portfolio composition and yield:

The company has maintained strong asset growth over time while preserving credit quality, as demonstrated in this long-term chart:

Competitive Industry Position

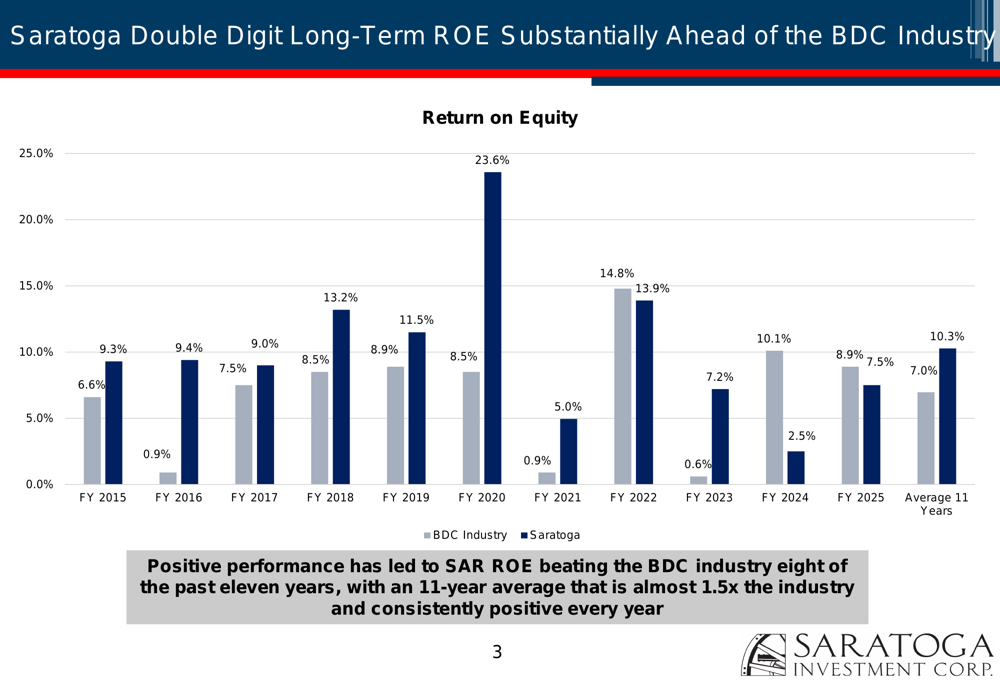

Saratoga emphasized its long-term outperformance compared to the broader BDC industry. The company’s 11-year average return on equity (ROE) stands at 10.3%, significantly above the industry average of 7.2%. This long-term outperformance has been consistent, with Saratoga exceeding the BDC industry average in eight of the past eleven years.

The following chart highlights this competitive advantage:

In terms of total returns, Saratoga has outperformed the BDC index with a 26% return over the last twelve months compared to 13% for the index. The company’s five-year total return of 239% also substantially exceeds the BDC index’s 168%.

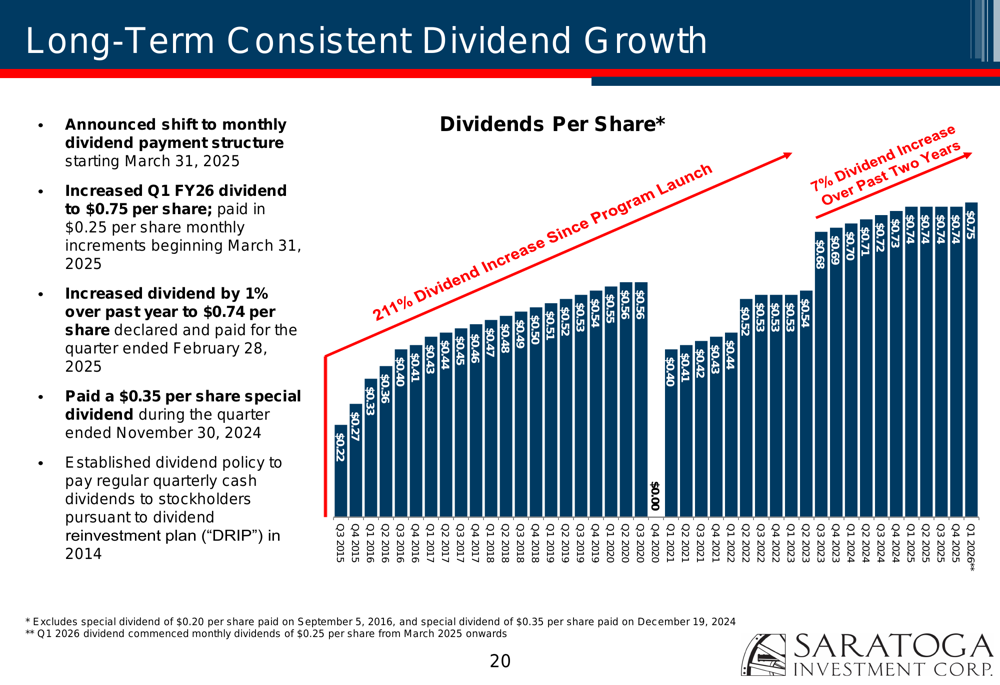

Saratoga has maintained consistent dividend growth over time, with a 211% increase since the program launch and a 7% increase over the past two years:

Forward-Looking Statements

Looking ahead, Saratoga’s management outlined several strategic priorities, including expanding the asset base without sacrificing credit quality and increasing capacity to source and manage investments. The company’s significant liquidity position of $428.2 million at quarter-end provides substantial flexibility to pursue these objectives.

Management highlighted that the company is well-positioned for potential interest rate changes, with a strong balance sheet and diversified portfolio across 40 distinct industries. The pipeline for new investments remains healthy despite market slowdowns, with 612 deals sourced in the last twelve months ending Q1 2025, up from 484 in 2024.

Saratoga’s focus on first lien investments (88.7% of the portfolio) and high-quality credits (99.7% with top internal ratings) suggests a continued conservative approach to navigate market uncertainties while pursuing growth opportunities.

Despite the quarterly decline in NII, Saratoga’s long-term performance metrics and portfolio quality indicate resilience in a challenging market environment. Investors will be watching closely to see if management can leverage the company’s strong liquidity position to generate improved returns in coming quarters while maintaining the portfolio’s exceptional credit quality.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.