Procore signs multi-year strategic collaboration agreement with AWS

Introduction & Market Context

Sartorius Group (FRA:SRT) presented its H1 2025 financial results on July 22, 2025, reporting a 6.1% constant currency sales growth and significant margin expansion despite continued softness in the equipment market. The company’s performance demonstrates a strong recovery in its recurring business, particularly in consumables, which has helped offset ongoing industry-wide reluctance to invest in new equipment.

The biotech supplier’s stock closed at €188.40 on July 21, down 2.66% ahead of the earnings presentation, with the share price currently trading well above its 52-week low of €145.80 but still below its high of €234.70.

Quarterly Performance Highlights

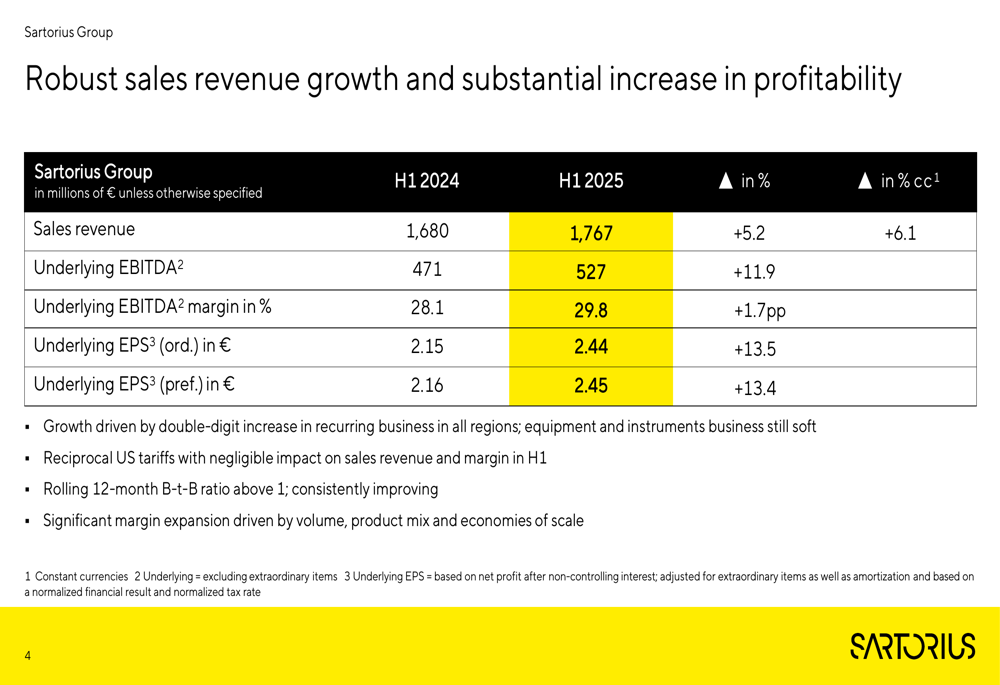

Sartorius reported sales revenue of €1,767 million for H1 2025, representing a 5.2% increase (6.1% in constant currency) compared to H1 2024. More impressively, the company’s underlying EBITDA grew by 11.9% to €527 million, with the EBITDA margin expanding by 1.7 percentage points to 29.8%.

As shown in the following financial highlights table, underlying earnings per share also saw double-digit growth:

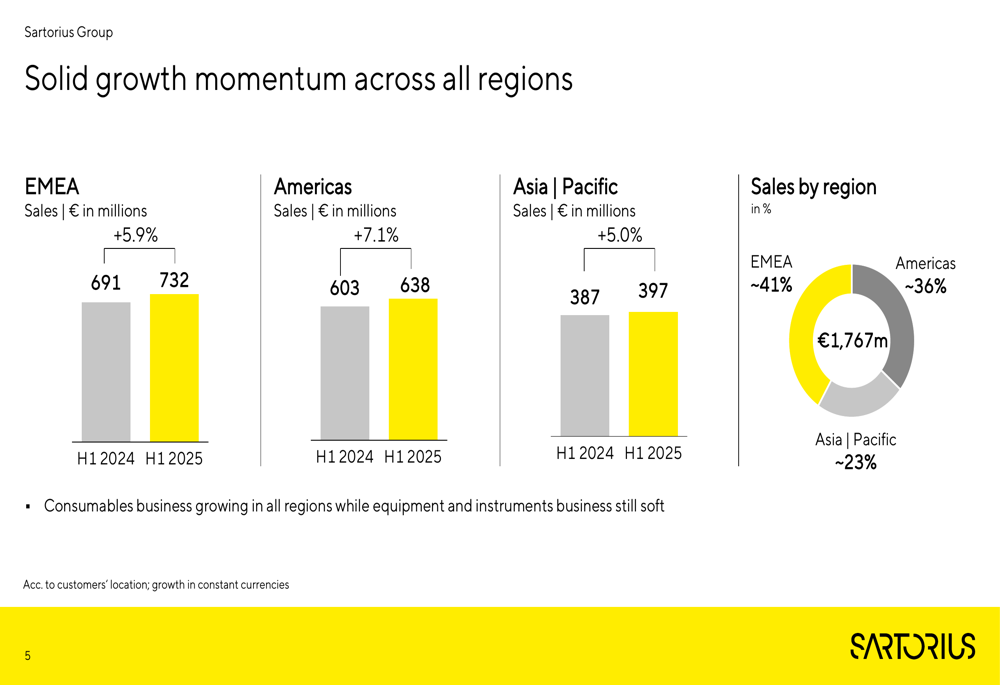

The company achieved growth across all major regions, with the Americas leading at 7.1% growth, followed by EMEA at 5.9% and Asia/Pacific at 5.0%. This regional performance reflects the global nature of the recovery in Sartorius’ recurring business.

The following chart illustrates the regional sales distribution and growth rates:

CEO Michael Grosse highlighted during the presentation that the book-to-bill ratio remained consistently above 1, indicating healthy demand momentum, while the reciprocal US tariffs had only a negligible impact on the company’s performance.

Segment Analysis

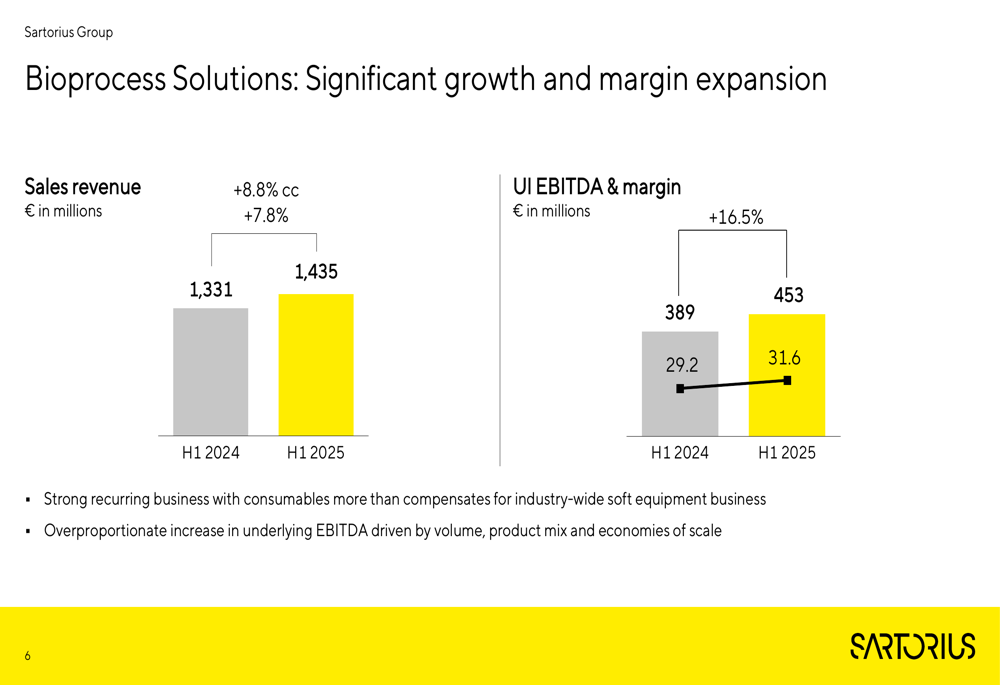

Sartorius’ two main business segments showed divergent performance in H1 2025. The Bioprocess Solutions segment, which represents about 81% of total sales, delivered strong results with 7.8% sales growth (8.8% in constant currency) to €1,435 million. The segment’s underlying EBITDA increased by 16.5% to €453 million, with the margin expanding significantly from 29.2% to 31.6%.

The following chart details the Bioprocess Solutions segment’s performance:

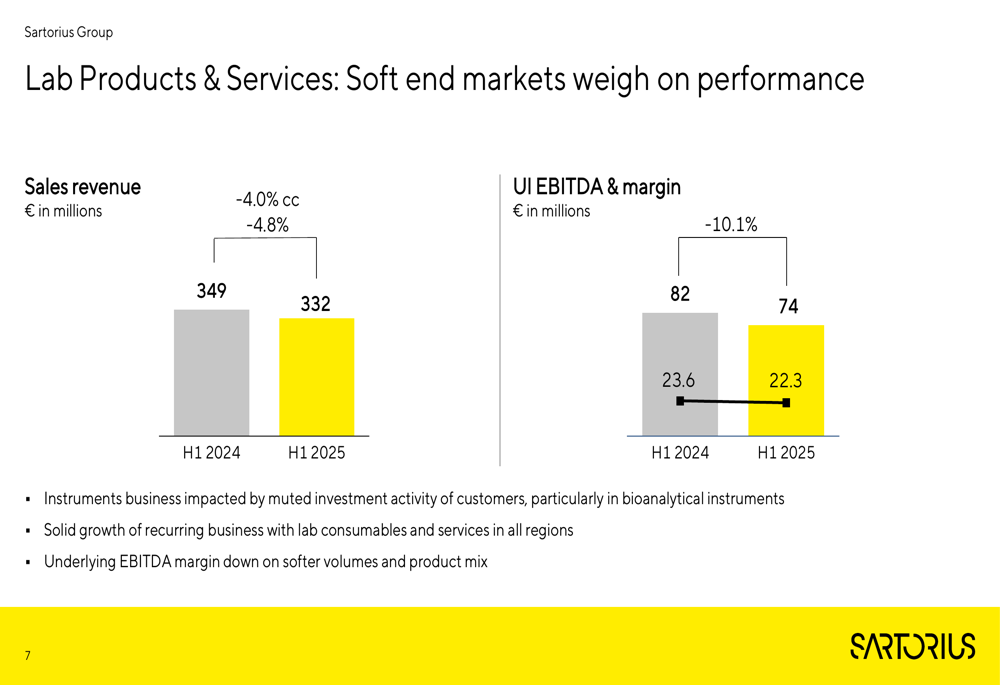

In contrast, the Lab Products & Services segment faced challenges, with sales declining by 4.8% (4.0% in constant currency) to €332 million. The segment’s underlying EBITDA decreased by 10.1% to €74 million, with the margin contracting from 23.6% to 22.3%.

The company attributed this decline to soft end markets and muted investment activity affecting instrument sales, although it noted solid growth in recurring business with lab consumables and services across all regions.

The following chart illustrates the Lab Products & Services segment’s performance:

Financial Health and Cash Flow

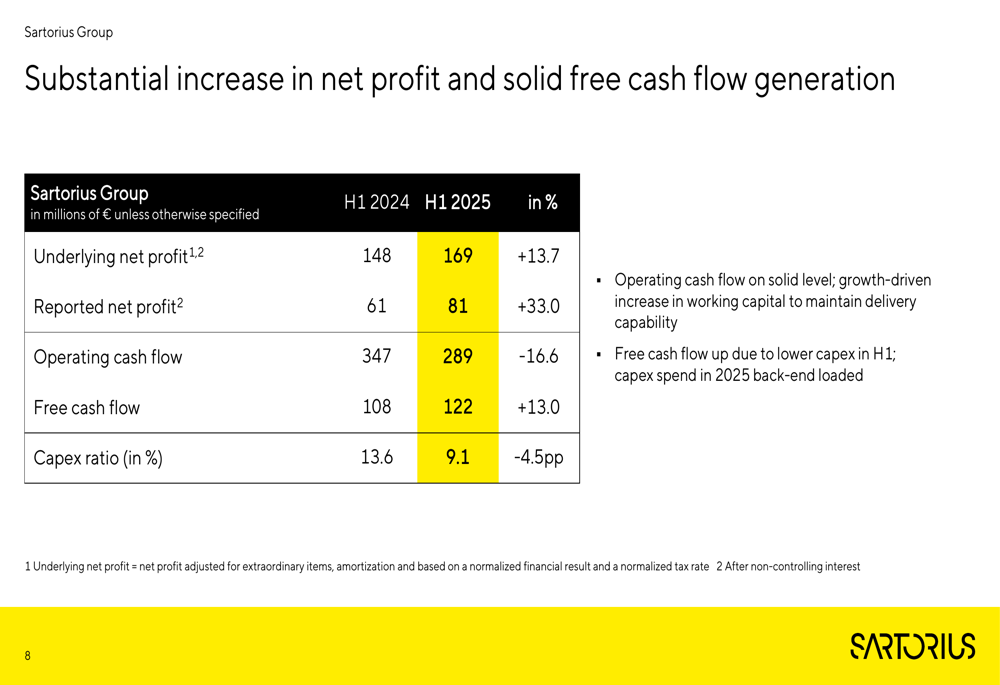

Sartorius reported a substantial 13.7% increase in underlying net profit to €169 million for H1 2025, while reported net profit rose even more dramatically by 33.0% to €81 million. Free cash flow improved by 13.0% to €122 million, despite a 16.6% decrease in operating cash flow to €289 million.

The company’s improved free cash flow was primarily due to lower capital expenditure in the first half of the year, with the capex ratio decreasing from 13.6% to 9.1%. Management indicated that capital spending is expected to be back-end loaded in 2025.

The following table provides a detailed breakdown of the company’s profitability and cash flow metrics:

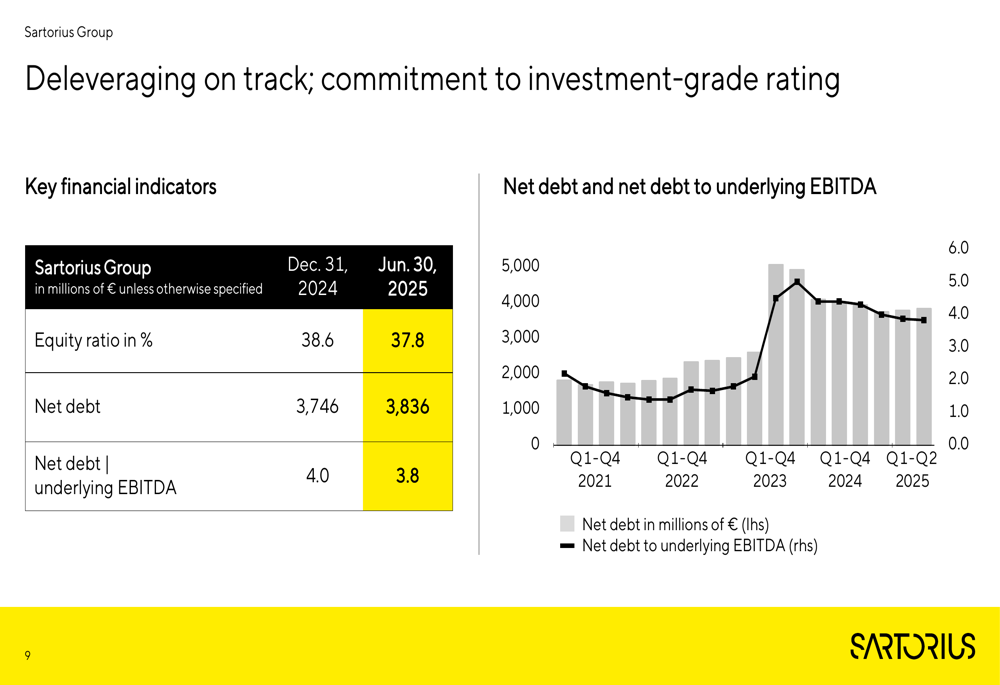

Sartorius continued to make progress on its deleveraging goals, with the net debt to underlying EBITDA ratio improving from 4.0 at the end of 2024 to 3.8 by June 30, 2025. This improvement reflects the company’s commitment to strengthening its financial position and maintaining its investment-grade rating.

The following chart shows the company’s deleveraging progress over time:

Sartorius Stedim (EPA:STDM) Biotech Performance

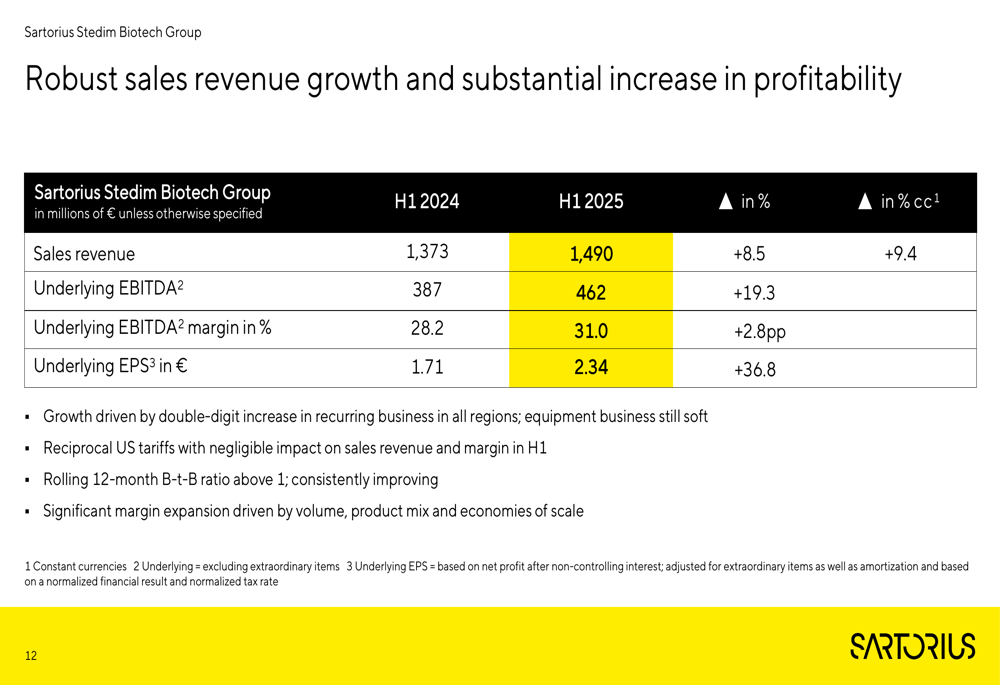

Sartorius Stedim Biotech (EPA:DIM), the group’s listed subsidiary, outperformed the parent company with sales growth of 8.5% (9.4% in constant currency) to €1,490 million and an underlying EBITDA increase of 19.3% to €462 million. The subsidiary’s EBITDA margin expanded by 2.8 percentage points to 31.0%.

The following table highlights Sartorius Stedim Biotech’s key financial metrics:

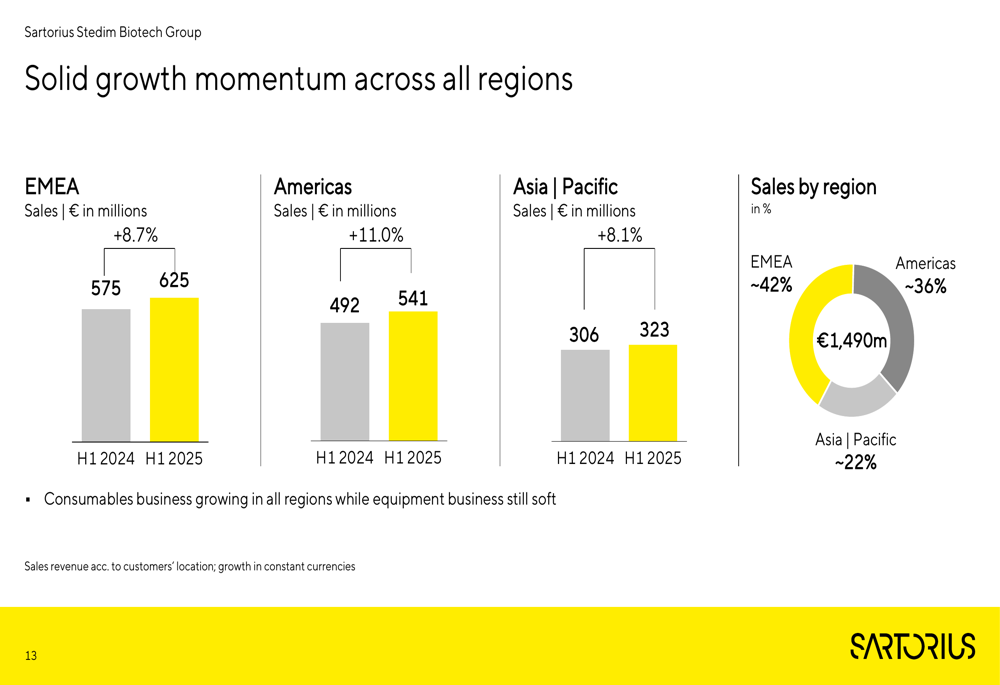

Similar to the parent company, Sartorius Stedim Biotech achieved growth across all regions, with the Americas showing the strongest performance at 11.0% growth, followed by Asia/Pacific at 8.1% and EMEA at 8.7%.

Forward-Looking Statements

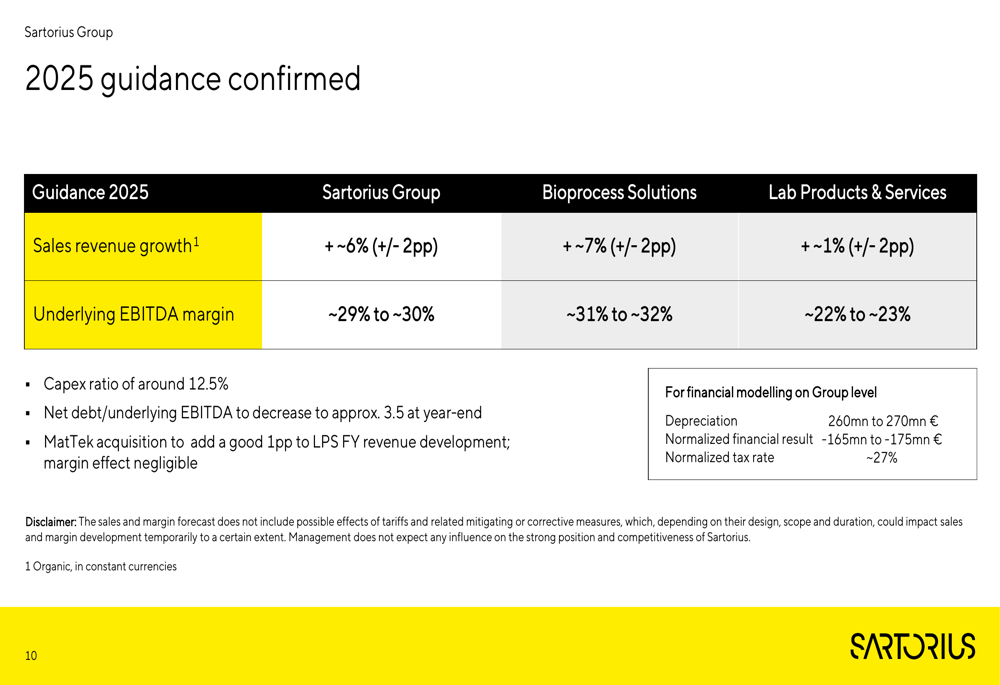

Sartorius confirmed its full-year guidance for 2025, projecting sales growth of approximately 6% (±2 percentage points) for the group, with the Bioprocess Solutions segment expected to grow by around 7% and the Lab Products & Services segment by approximately 1%.

The company anticipates an underlying EBITDA margin of 29-30% for the full year, with Bioprocess Solutions expected to achieve a margin of 31-32% and Lab Products & Services 22-23%. The capex ratio is projected to be around 12.5%, with net debt to underlying EBITDA expected to decrease to approximately 3.5 by year-end.

The following table details the company’s 2025 guidance:

The recently completed acquisition of MatTek is expected to add approximately 1 percentage point to the Lab Products & Services segment’s revenue development for the full year, with a negligible effect on margins.

In the Q1 earnings call earlier this year, CEO Joachim Krejtsburg had expressed optimism about the company’s trajectory, stating, "We think we are off to a good start, a very good start into the year 2025." The H1 results appear to validate this optimism, with the company maintaining its full-year guidance despite ongoing challenges in certain market segments.

The presentation confirms that while equipment orders remain soft across the industry, the recovery in consumables business and the company’s focus on operational efficiency are enabling Sartorius to deliver solid financial results and make progress on its strategic objectives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.