Beamr video compression achieves up to 50% improvement for AVs

Introduction & Market Context

Seacoast Banking Corporation of Florida (NASDAQ:SBCF) released its first quarter 2025 earnings presentation on April 25, showing solid deposit growth and margin expansion. Despite the positive operational metrics, the stock dropped 7.37% in premarket trading to $22.11, suggesting investors may have expected stronger results or were concerned about other factors not highlighted in the presentation.

The Florida-based bank, which ranks 15th in state market share, reported net income of $31.5 million or $0.37 per diluted share for the quarter, while continuing to expand its footprint through organic growth and strategic acquisitions.

Quarterly Performance Highlights

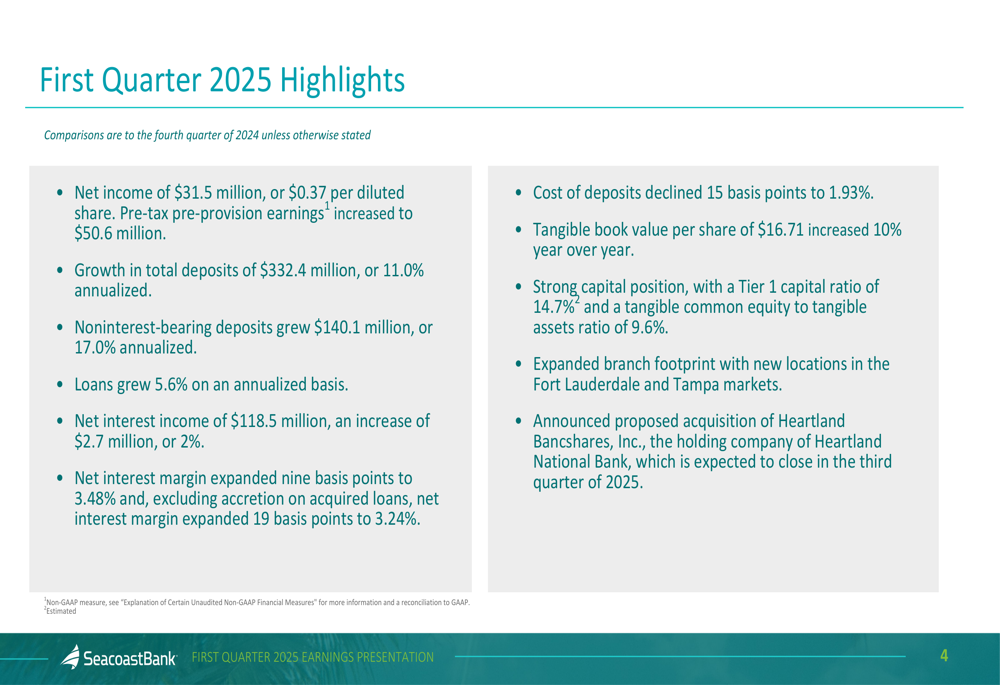

Seacoast reported several positive financial metrics for Q1 2025, including deposit growth, margin expansion, and continued loan growth. The bank achieved net income of $31.5 million ($0.37 per diluted share) while growing its balance sheet and maintaining strong capital levels.

As shown in the following summary of first quarter results:

Key achievements include total deposit growth of $332.4 million (11.0% annualized), with noninterest-bearing deposits growing $140.1 million (17.0% annualized). Loans increased at a more modest pace of 5.6% annualized. The bank’s net interest income reached $118.5 million, representing a 2% increase, while net interest margin expanded 9 basis points to 3.48%.

Tangible book value per share increased 10% year-over-year to $16.71, and the bank maintained a strong capital position with a 14.7% Tier 1 capital ratio.

Deposit Growth and Net Interest Margin

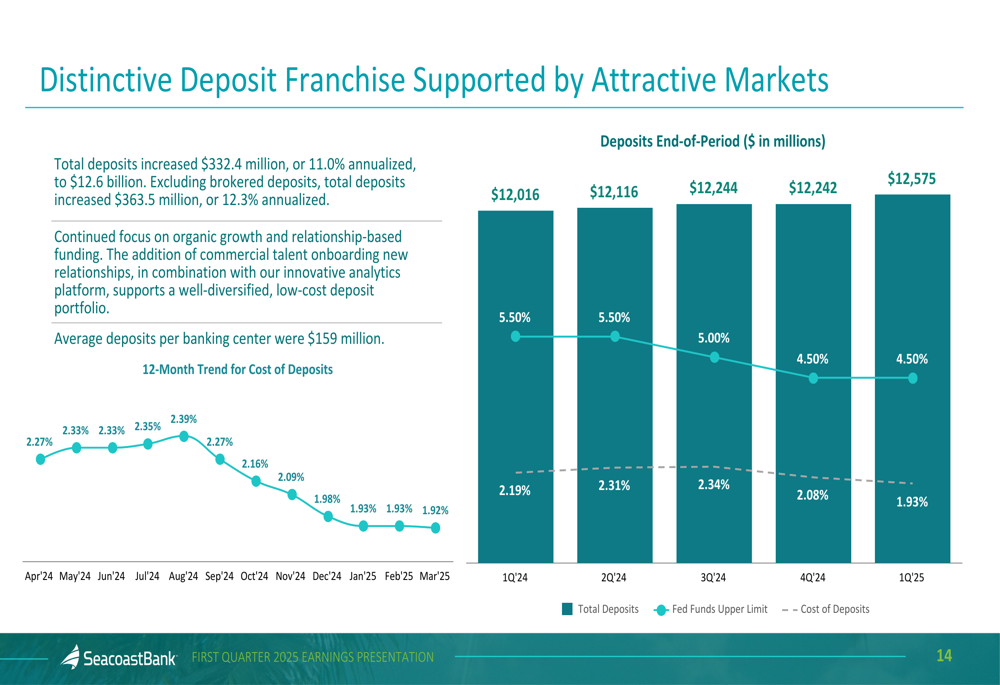

One of the most impressive aspects of Seacoast’s Q1 performance was its deposit growth. The bank’s total deposits increased to $12.6 billion, representing an 11.0% annualized growth rate from the previous quarter. This growth came alongside a 15 basis point reduction in the cost of deposits to 1.93%.

The following chart illustrates the bank’s deposit growth trajectory and cost trend:

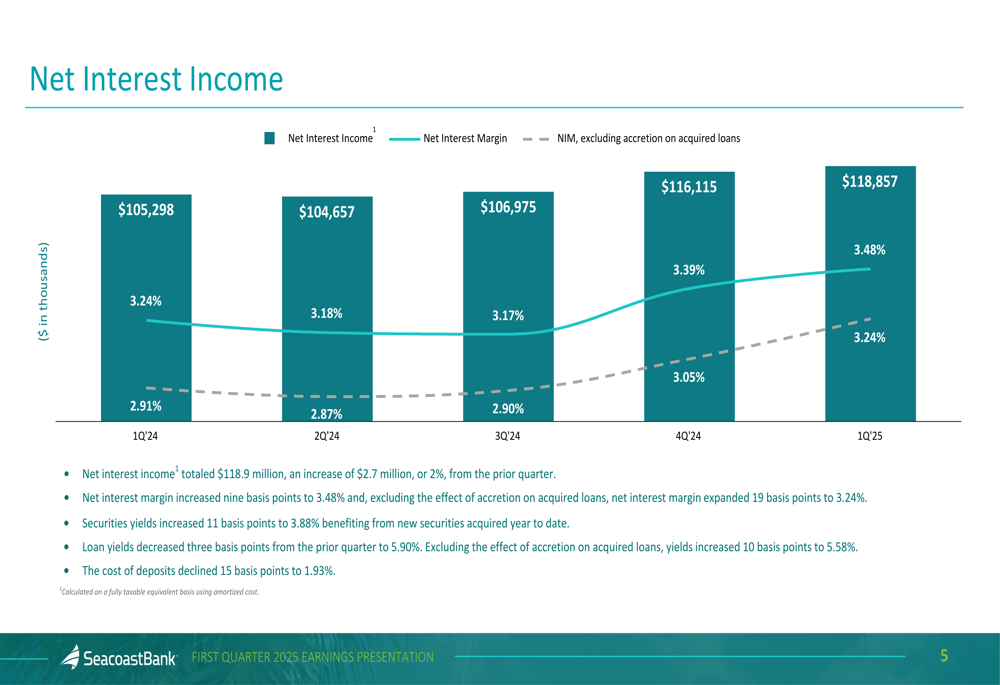

The bank’s net interest margin continued its upward trend, expanding to 3.48% in Q1 2025 from 2.91% in the same quarter last year. This improvement reflects the bank’s ability to manage funding costs while maintaining asset yields.

As shown in the net interest income and margin trend chart:

The margin expansion appears to be driven by both improved securities yields, which increased 11 basis points to 3.88%, and a decline in deposit costs. While loan yields decreased three basis points from the prior quarter to 5.90%, excluding the effect of accretion on acquired loans, yields actually increased 10 basis points to 5.58%.

Loan Portfolio and Credit Quality

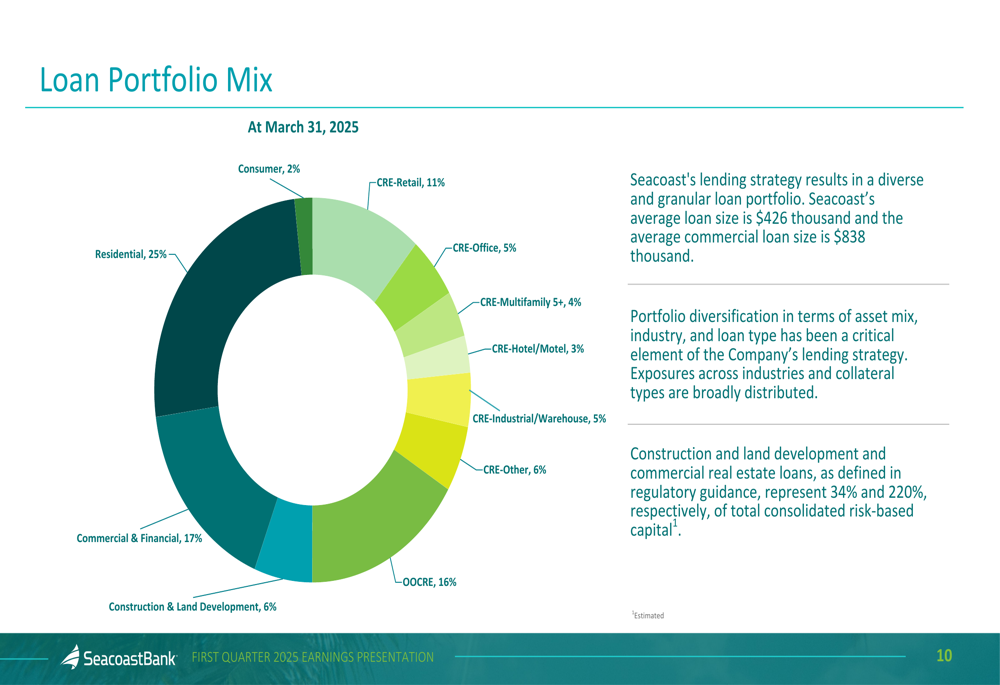

Seacoast’s loan portfolio grew by $143.1 million in Q1, representing a 5.6% annualized increase. The bank’s loan pipeline increased significantly, rising $288.2 million from the prior quarter to $981.6 million, suggesting potential for accelerated loan growth in coming quarters.

The bank maintains a diverse loan portfolio, with residential loans representing the largest category at 25%, followed by commercial and financial loans at 17%, and various commercial real estate categories comprising most of the remainder.

The following chart illustrates the bank’s loan portfolio diversification:

This diversification strategy results in a granular loan portfolio with an average loan size of $426 thousand and an average commercial loan size of $838 thousand, helping to mitigate concentration risk.

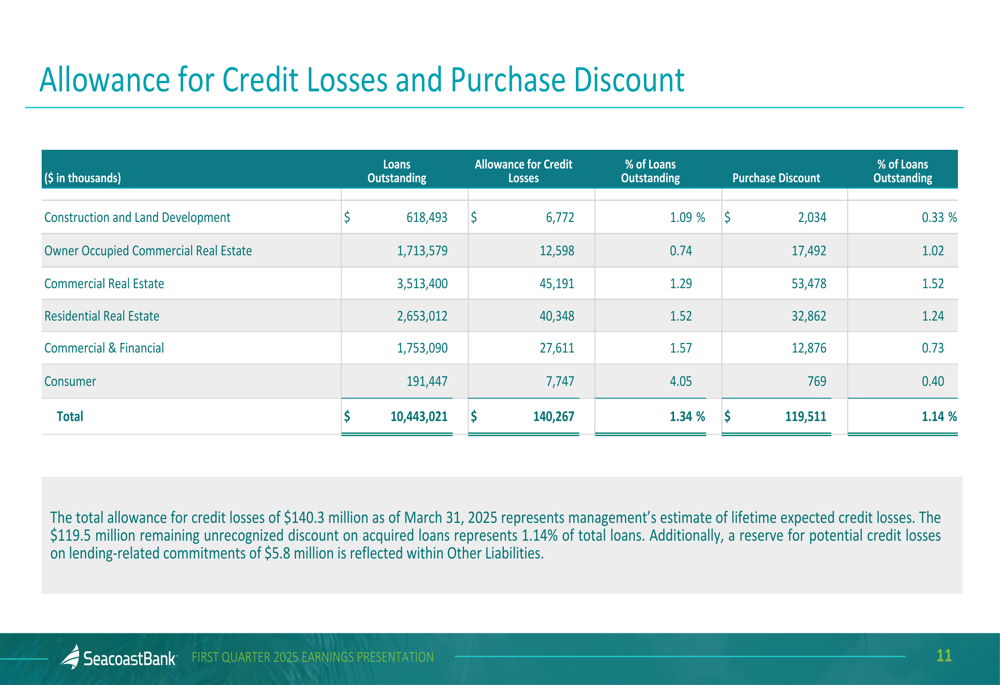

The bank’s allowance for credit losses stood at $140.3 million, representing 1.34% of total loans. When combined with the remaining purchase discount on acquired loans of 1.14%, the total credit protection reaches 2.48% of the loan portfolio.

The following table details the allowance for credit losses by loan category:

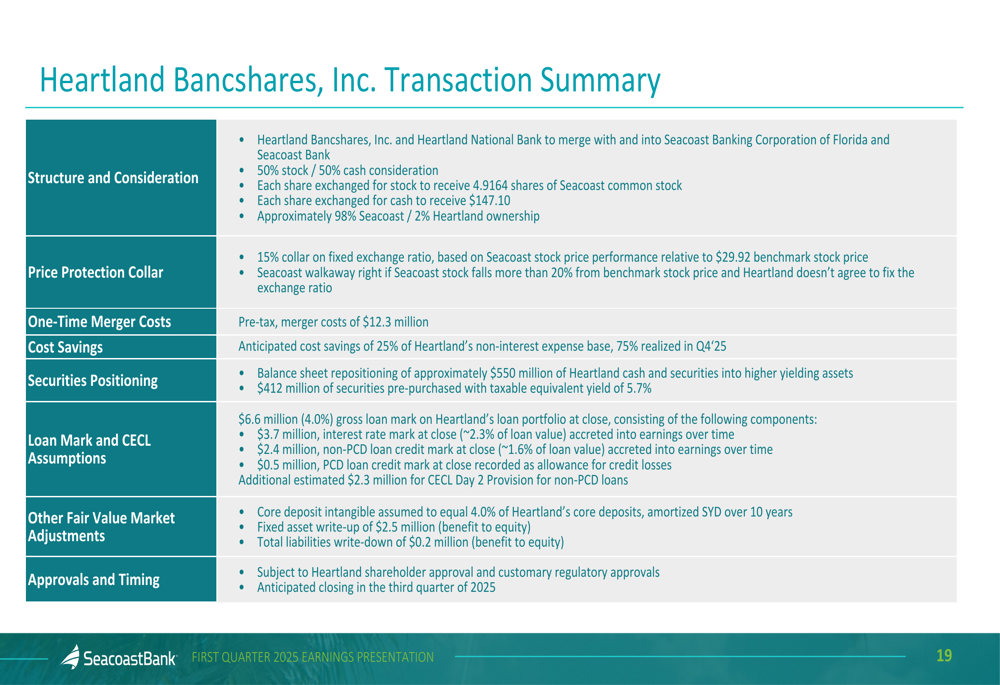

Strategic Expansion: Heartland Bancshares Acquisition

A significant development announced in the presentation is Seacoast’s proposed acquisition of Heartland Bancshares, Inc. The transaction, structured as 50% stock and 50% cash, is expected to close in the third quarter of 2025.

The following slide details the key terms and strategic benefits of the acquisition:

The acquisition is expected to generate cost savings of approximately 25% of Heartland’s non-interest expense base, with 75% of these savings realized by Q4 2025. The transaction also includes a balance sheet repositioning of approximately $550 million of Heartland’s cash.

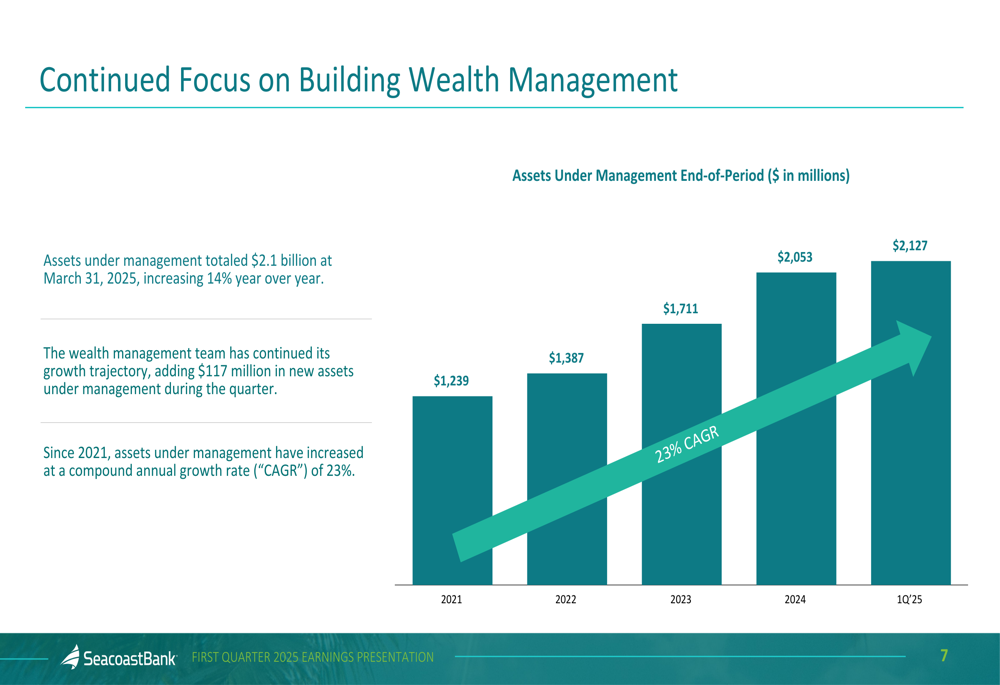

Wealth Management Growth

Beyond traditional banking services, Seacoast continues to grow its wealth management business. Assets under management reached $2.1 billion as of March 31, 2025, representing a 14% increase year-over-year. The wealth management team added $117 million in new assets during the quarter.

The following chart illustrates the consistent growth in assets under management, which have achieved a compound annual growth rate of 23% since 2021:

Forward-Looking Statements

Despite the positive operational metrics presented in the Q1 slides, investors appear concerned about some aspects of Seacoast’s performance or outlook, as evidenced by the 7.37% premarket drop following the release.

The bank’s focus on deposit growth, margin expansion, and strategic acquisitions suggests a continued emphasis on building scale in the competitive Florida banking market. With strong capital levels and a growing loan pipeline, Seacoast appears positioned to continue its expansion strategy, though investors may be looking for faster loan growth or improved efficiency to drive stronger earnings growth in future quarters.

The pending Heartland Bancshares acquisition represents a significant strategic move that could enhance Seacoast’s market position and potentially drive improved financial performance through cost synergies and balance sheet optimization in the latter part of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.