Texas Roadhouse earnings missed by $0.05, revenue topped estimates

Introduction & Market Context

Sealed Air Corporation (NYSE:SEE) presented its second quarter 2025 earnings results on August 5, 2025, revealing a mixed performance characterized by slight revenue decline but improved profitability metrics. The company’s stock responded positively to the results, rising 3.55% to $30.01 in pre-market trading, reflecting investor confidence in the company’s ability to maintain margins despite challenging market conditions.

The packaging solutions provider, known for brands including CRYOVAC and Bubble Wrap, demonstrated resilience in a quarter marked by volume pressures and pricing challenges, particularly in its Protective segment. The presentation, delivered by President and CEO Dustin Semach and Interim CFO Roni Johnson, highlighted the company’s focus on productivity improvements and disciplined capital allocation.

Quarterly Performance Highlights

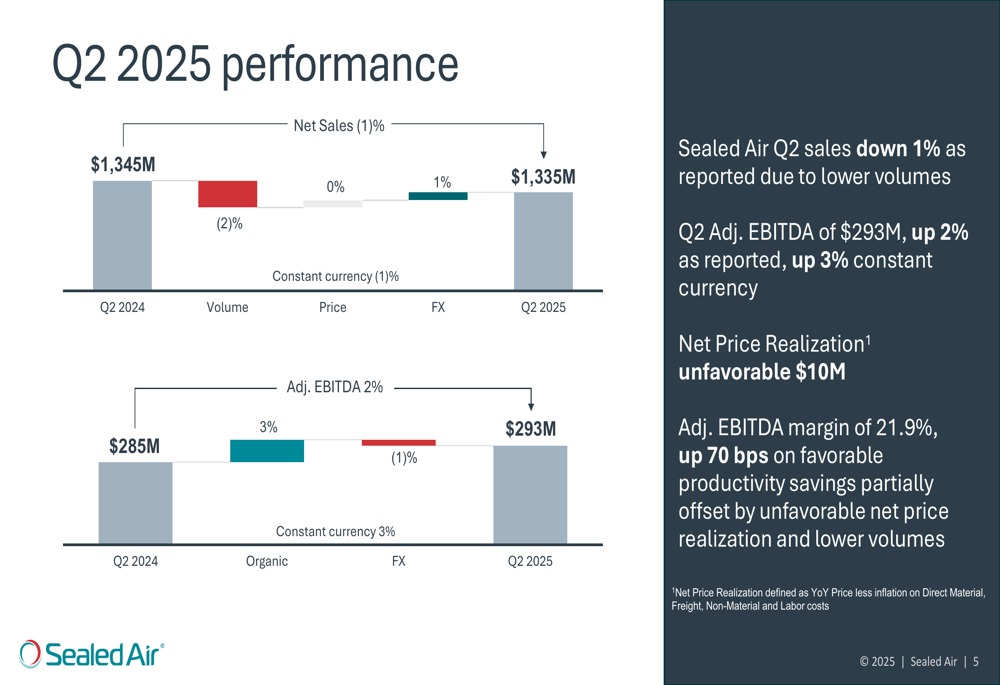

Sealed Air reported Q2 2025 revenue of $1.3 billion, down 1% both as reported and in constant currency compared to the prior year. Despite the revenue decline, the company achieved notable improvements in profitability metrics, with Adjusted EBITDA increasing to $293 million, up 2% as reported and 3% in constant currency.

As shown in the following summary of key financial results:

The company’s Adjusted EPS reached $0.89, representing a 7% increase as reported and 10% in constant currency. This result significantly exceeded analyst expectations of $0.71, marking a 25.35% positive surprise. The earnings growth came despite unfavorable net price realization of $10 million, as productivity savings helped drive margin expansion.

The following chart illustrates the factors affecting Q2 2025 performance:

Adjusted EBITDA margin improved to 21.9%, up 70 basis points from the prior year, driven primarily by favorable productivity savings that more than offset the impact of unfavorable pricing and lower volumes. This margin expansion demonstrates the company’s ability to enhance operational efficiency in a challenging market environment.

Segment Analysis

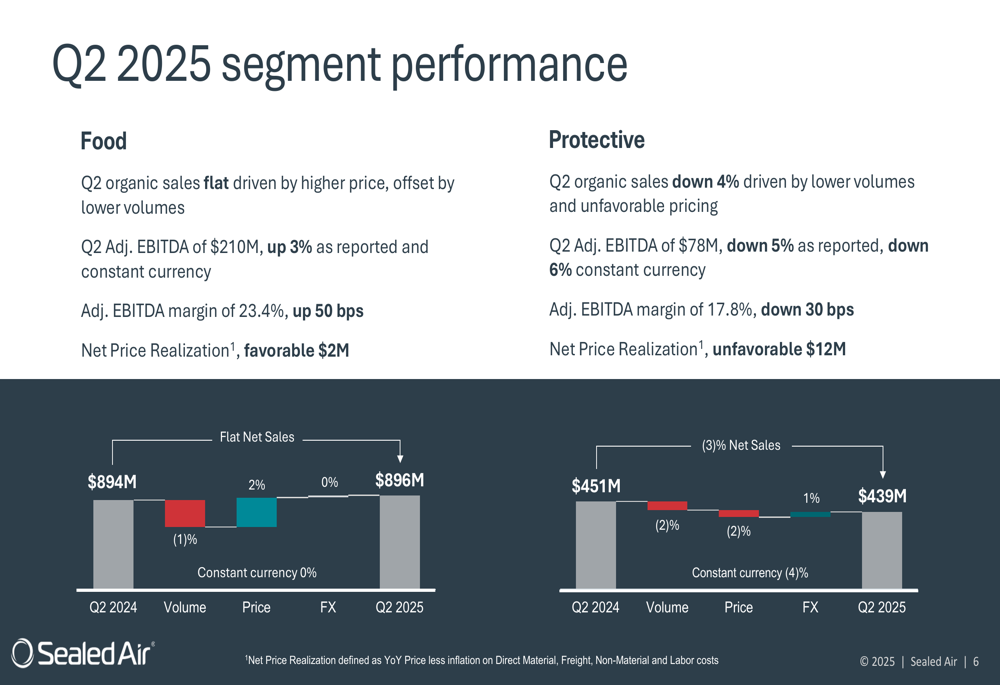

Sealed Air’s performance showed a clear divergence between its two main business segments. The Food segment demonstrated resilience with flat organic sales, as higher pricing offset volume declines. Meanwhile, the Protective segment faced more significant challenges with a 4% decline in organic sales driven by both lower volumes and unfavorable pricing.

The following segment breakdown provides further detail on this performance divergence:

The Food segment delivered an Adjusted EBITDA of $210 million, up 3% both as reported and in constant currency, with margin expanding to 23.4%, an improvement of 50 basis points. Net price realization was favorable by $2 million in this segment.

In contrast, the Protective segment reported Adjusted EBITDA of $78 million, down 5% as reported and 6% in constant currency, with margin contracting to 17.8%, a decline of 30 basis points. This segment faced unfavorable net price realization of $12 million, highlighting the pricing pressures in the protective packaging market.

Capital Allocation & Balance Sheet

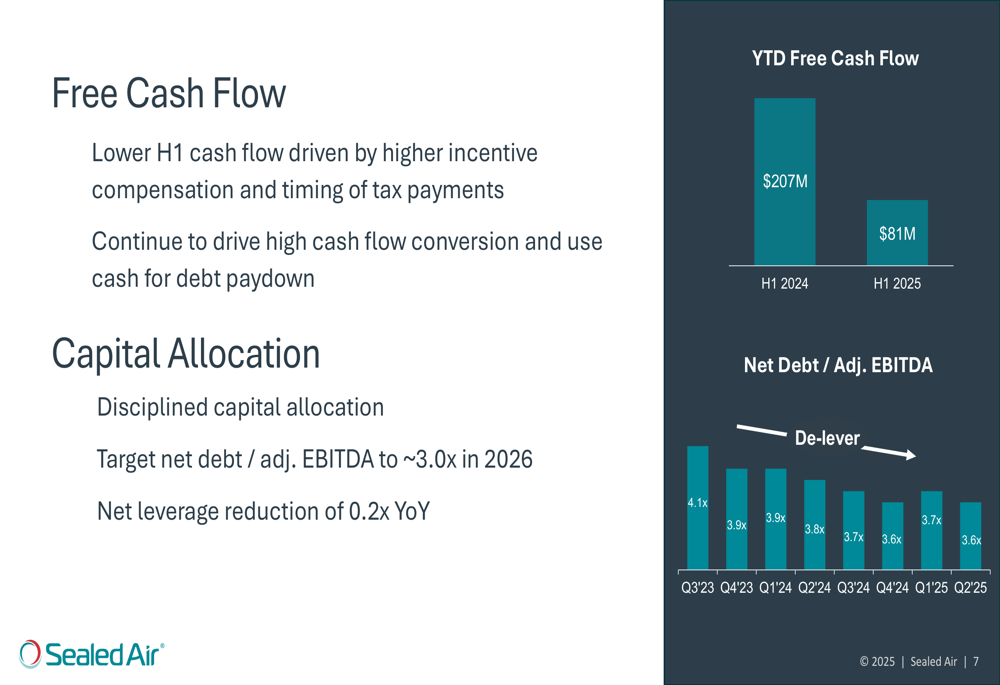

Sealed Air’s free cash flow generation showed significant year-over-year decline, with year-to-date free cash flow of $81 million compared to $207 million in the prior year period. Management attributed this decline to higher incentive compensation payments and the timing of tax payments.

The following chart illustrates the company’s free cash flow and leverage position:

The company maintained its focus on deleveraging, with a net debt to adjusted EBITDA ratio of 3.6x as of Q2 2025. Management reaffirmed its target of reducing this ratio to approximately 3.0x by 2026, representing a planned reduction of 0.2x year-over-year.

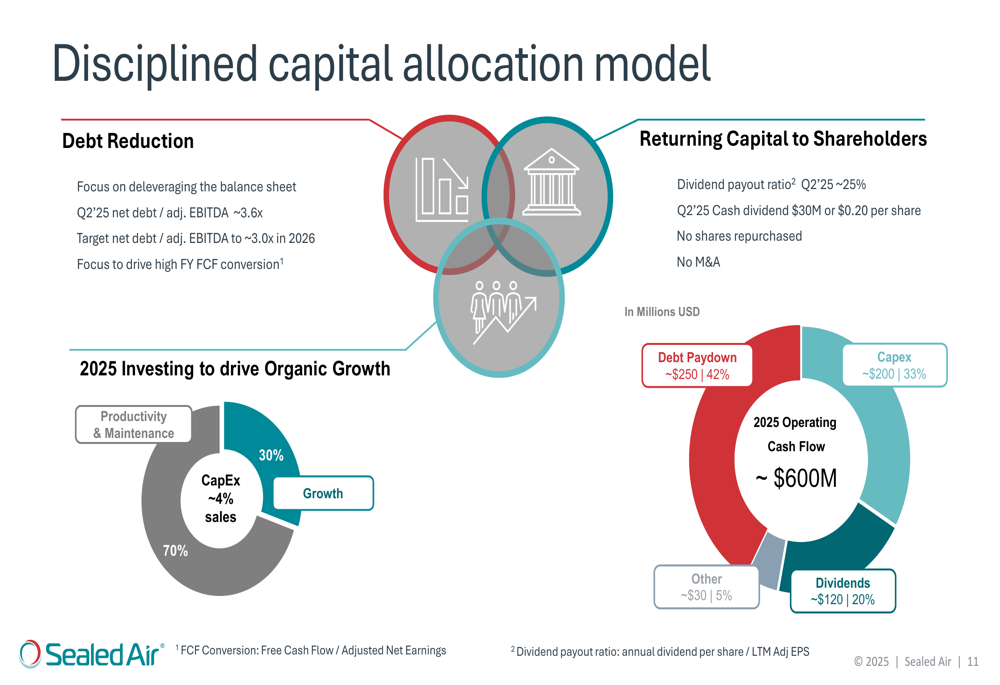

Sealed Air’s disciplined capital allocation strategy prioritizes debt reduction while maintaining shareholder returns through dividends. The company’s capital allocation model includes:

The model highlights Sealed Air’s balanced approach to financial management, with approximately $200 million allocated to capital expenditures (about 4% of sales), $120 million to dividends (representing a payout ratio of about 25%), and approximately $250 million dedicated to debt reduction.

Outlook & Forward Guidance

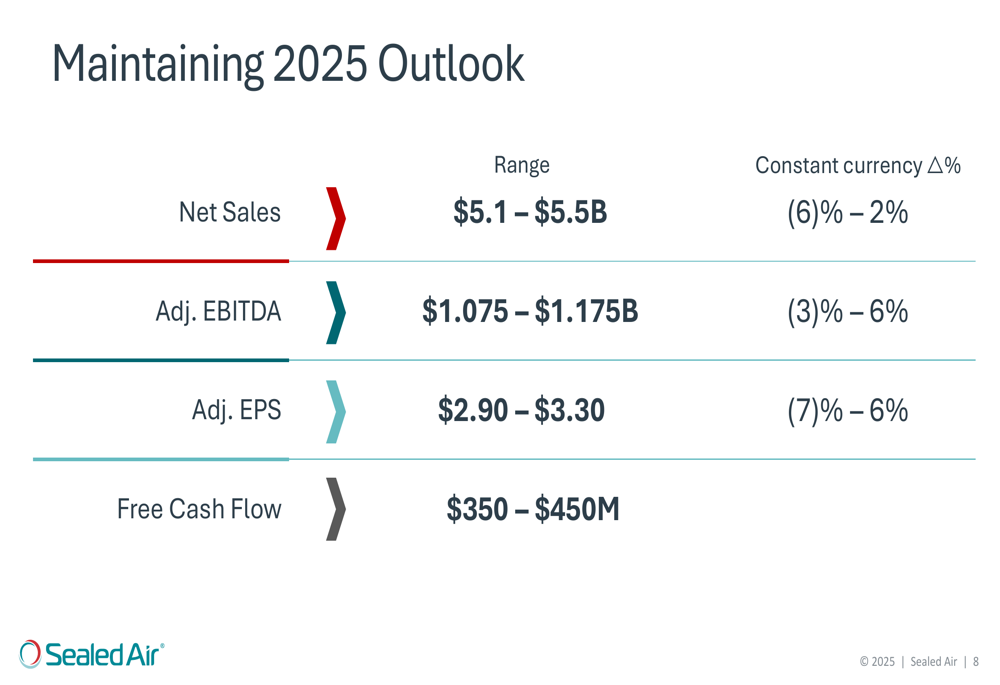

Despite the mixed quarterly results, Sealed Air maintained its full-year 2025 outlook across all key financial metrics. The company continues to project net sales between $5.1 billion and $5.5 billion, representing a constant currency change of -6% to +2%.

The following slide details the company’s maintained 2025 guidance:

Adjusted EBITDA is expected to range from $1.075 billion to $1.175 billion, with a constant currency change of -3% to +6%. Adjusted EPS guidance remains at $2.90 to $3.30, representing a constant currency change of -7% to +6%. Free cash flow is projected to be between $350 million and $450 million.

The maintained guidance suggests management’s confidence in the company’s ability to navigate ongoing market challenges through continued productivity improvements and disciplined cost management. This outlook aligns with the company’s broader strategy of focusing on operational efficiency while pursuing targeted growth opportunities in its Food segment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.