Asia FX moves little with focus on US-China trade, dollar steadies ahead of CPI

Introduction & Market Context

Selective Insurance Group Inc (NASDAQ:SIGI) released its first quarter 2025 investor presentation on April 24, highlighting a significant performance rebound after what management had previously described as a "challenging" 2024. The property and casualty insurer, ranked as the 34th largest in the United States, demonstrated improved profitability metrics while maintaining its disciplined growth strategy.

The presentation comes after Selective’s disappointing Q4 2024 results, when the company missed EPS forecasts by 18.6%, leading to a substantial stock decline. Current premarket trading shows SIGI down 1.87% at $89.20, reflecting continued investor caution despite the improved Q1 performance.

Quarterly Performance Highlights

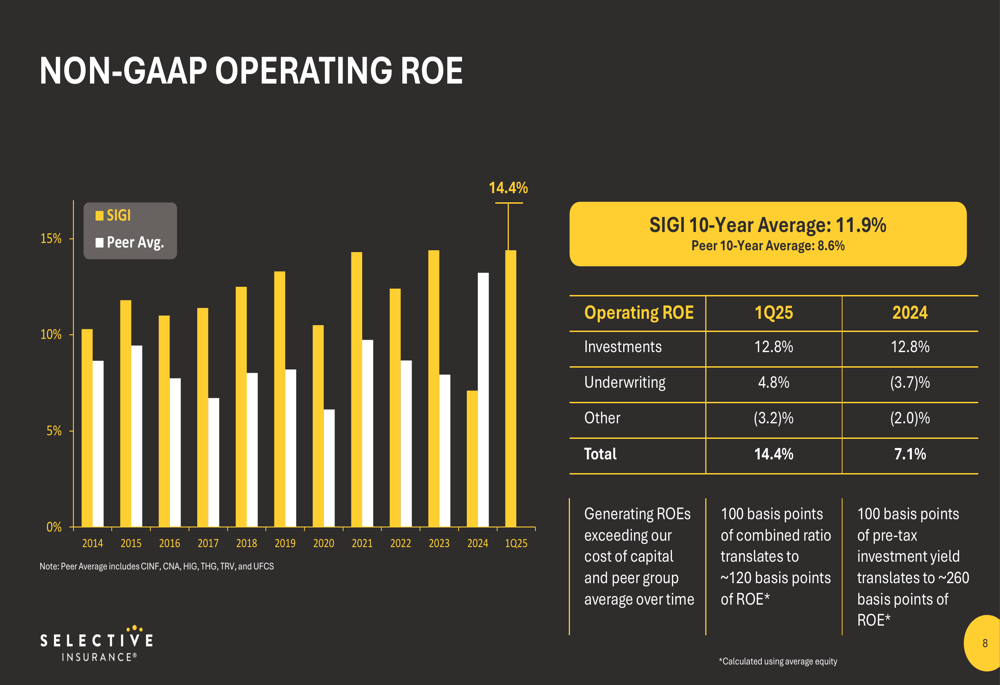

Selective reported a substantial improvement in its operating return on equity (ROE), reaching 14.4% in Q1 2025 compared to just 7.0% for full-year 2024. This represents a significant recovery toward the company’s historical averages of 11.1% over five years and 11.3% over ten years.

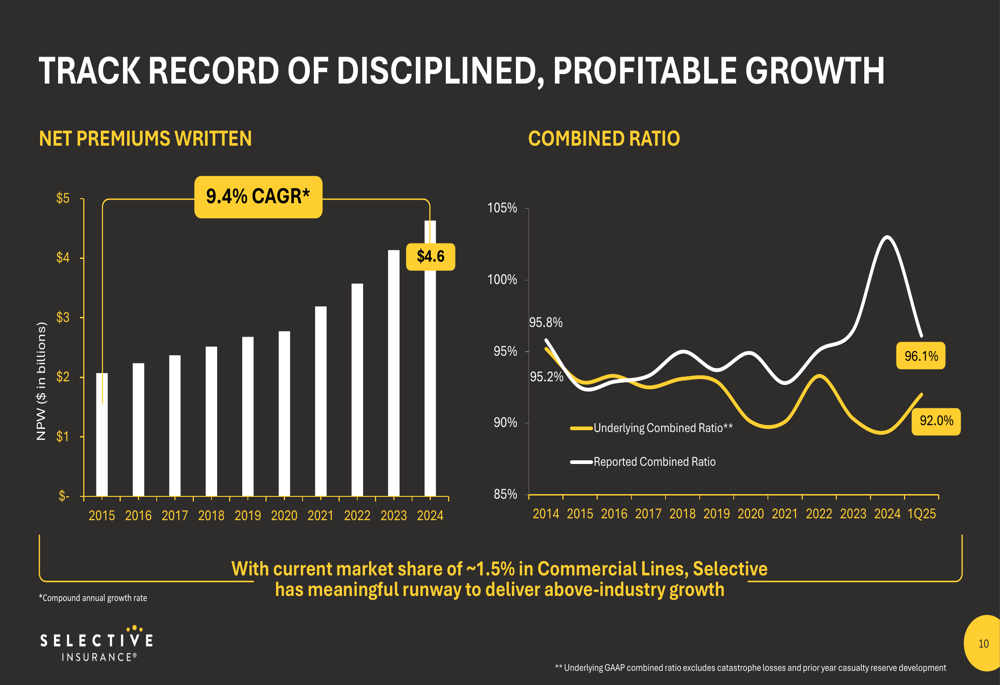

The company’s combined ratio, a key measure of underwriting profitability where lower is better, improved to 96.1% in Q1 2025 from 103.0% in 2024. This improvement indicates that Selective’s pricing and underwriting actions are beginning to yield positive results.

As shown in the following chart of Selective’s Non-GAAP Operating ROE compared to peers, the company has maintained superior returns over time:

The presentation highlighted Selective’s disciplined approach to profitable growth, with net premiums written reaching $4.6 billion in 2024, representing a 10-year compound annual growth rate of 9.4%. This growth has been achieved while maintaining underwriting discipline, as illustrated in the following chart:

Strategic Initiatives

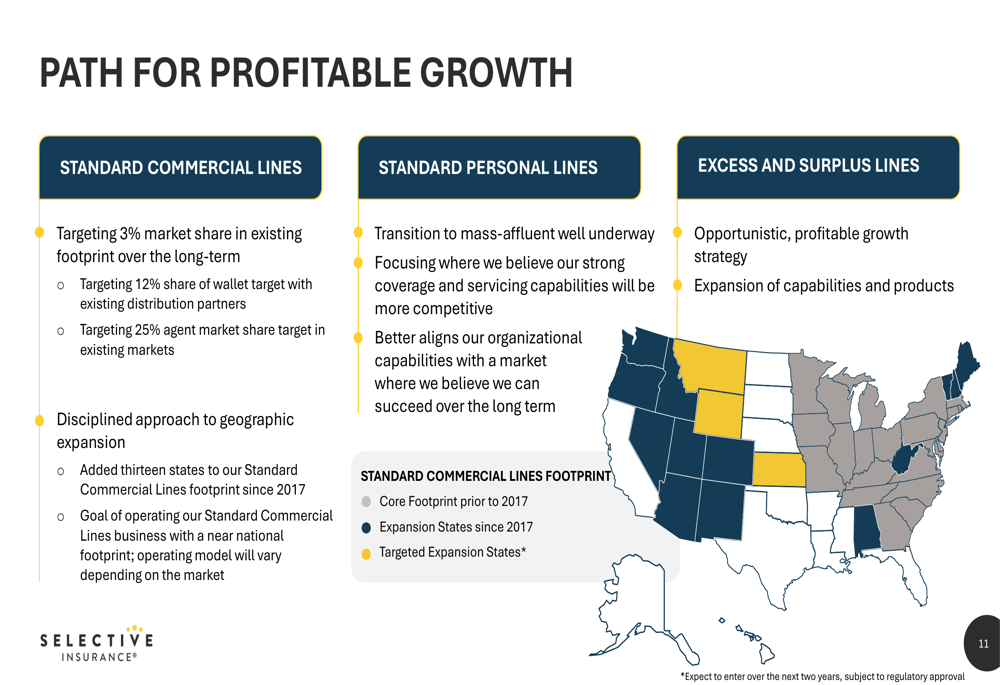

Selective outlined its strategic growth initiatives across its three main business segments. The Standard Commercial Lines segment, which comprises 79% of net premiums written, remains the company’s primary focus. The company is targeting a 3% market share in its existing footprint over the long term, up from approximately 1.5% currently.

In the Standard Personal Lines segment (9% of premiums), Selective is strategically shifting toward the mass-affluent market, where its strong coverage and service capabilities are expected to be more competitive. The Excess & Surplus Lines segment (12% of premiums) continues to pursue opportunistic growth with a focus on small and middle-market risks.

The company’s geographic expansion strategy is illustrated in the following map, showing both recent and targeted expansion states:

Selective emphasized its sustainable competitive advantages, including its unique operating model that places empowered decision-makers alongside customers and distribution partners, sophisticated risk selection tools, and strong relationships with 1,640 distribution partners.

Detailed Financial Analysis

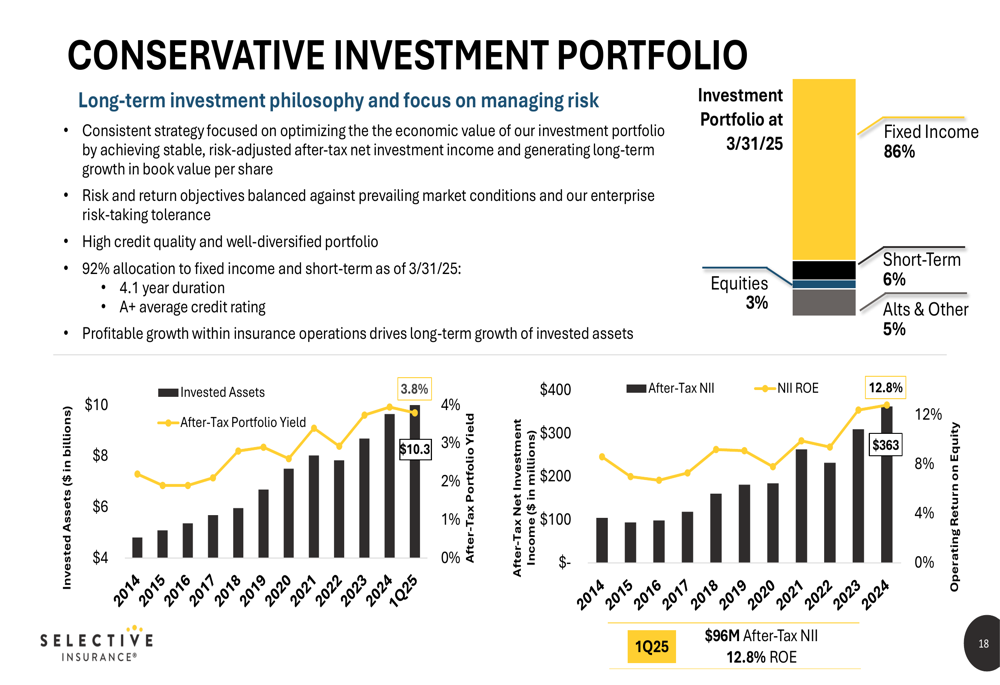

Selective maintains a conservative investment portfolio, with 92% allocated to fixed income and short-term investments as of March 31, 2025. Total (EPA:TTEF) invested assets reached $10.3 billion, generating after-tax net investment income of $96 million in Q1 2025, contributing 12.8% to ROE.

The company’s investment strategy and allocation are illustrated in the following chart:

From a capital perspective, Selective reported a strong position with $1.1 billion of operating cash flow generated in 2024, up from $759 million in 2023. The company’s NPW-to-Surplus ratio stood at 1.47x as of March 31, 2025, indicating solid capital adequacy. Selective maintains strong financial strength ratings, including A+ from both AM Best and Fitch.

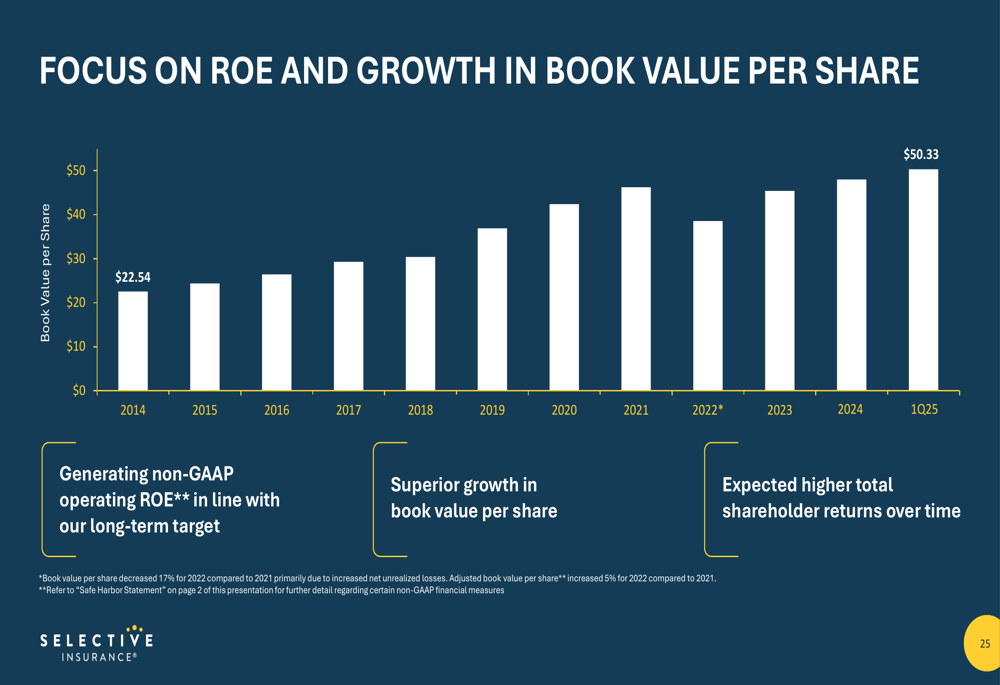

The company’s book value per share has shown consistent growth over time, increasing from $22.54 in 2014 to $50.33 in Q1 2025, as shown in the following chart:

Forward-Looking Statements

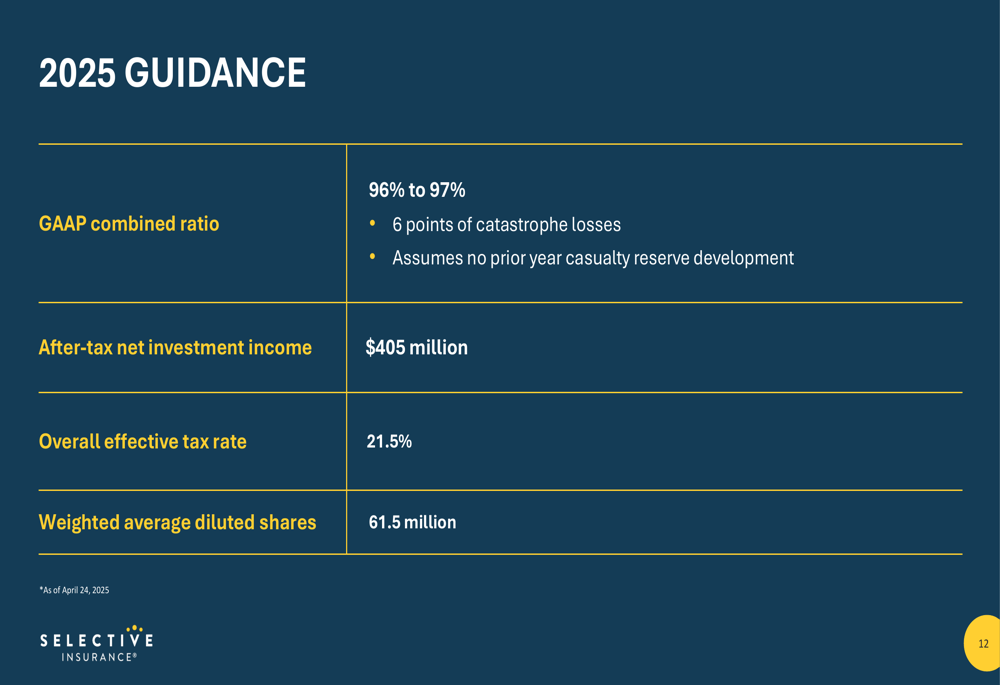

For 2025, Selective provided guidance that suggests continued improvement from 2024’s results:

The company expects a GAAP combined ratio between 96% and 97%, including 6 points of catastrophe losses and assuming no prior year casualty reserve development. After-tax net investment income is projected at $405 million, with an overall effective tax rate of 21.5%.

Selective’s enterprise risk management strategy focuses on maintaining a strong balance sheet with prudent reserving practices and catastrophe loss mitigation initiatives. The company has reduced its 1-in-250 probable maximum loss as a percentage of GAAP equity from 7% in 2023 to 4% in 2025, demonstrating improved risk management.

The company’s prudent reinsurance structure provides protection with a $1.4 billion exhaustion point and $100 million retention, helping to mitigate potential catastrophe losses.

While the Q1 2025 results show promising signs of recovery, investors will likely remain cautious given the volatility in Selective’s recent performance and the broader challenges facing the property and casualty insurance industry, including social inflation and elevated severity trends that management had previously identified as significant headwinds.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.