U.S. stocks edge higher after weekly jobless claims; Salesforce gains

Introduction & Market Context

Shelly Group SE (SHLY) presented its H1 2025 trading update on August 15, 2025, showcasing continued strong performance with revenue exceeding targets despite currency headwinds. The smart home technology provider reported €54 million in H1 revenue, marking its 30th consecutive quarter of growth and reinforcing its position in the increasingly competitive IoT market.

The company continues its strategic pivot toward a Software-as-a-Service (SaaS) business model while expanding from its DIY roots into professional markets. With operations in over 100 countries and a growing installed base of devices, Shelly Group is positioning itself as a leader in smart connectivity solutions for homes and businesses.

Quarterly Performance Highlights

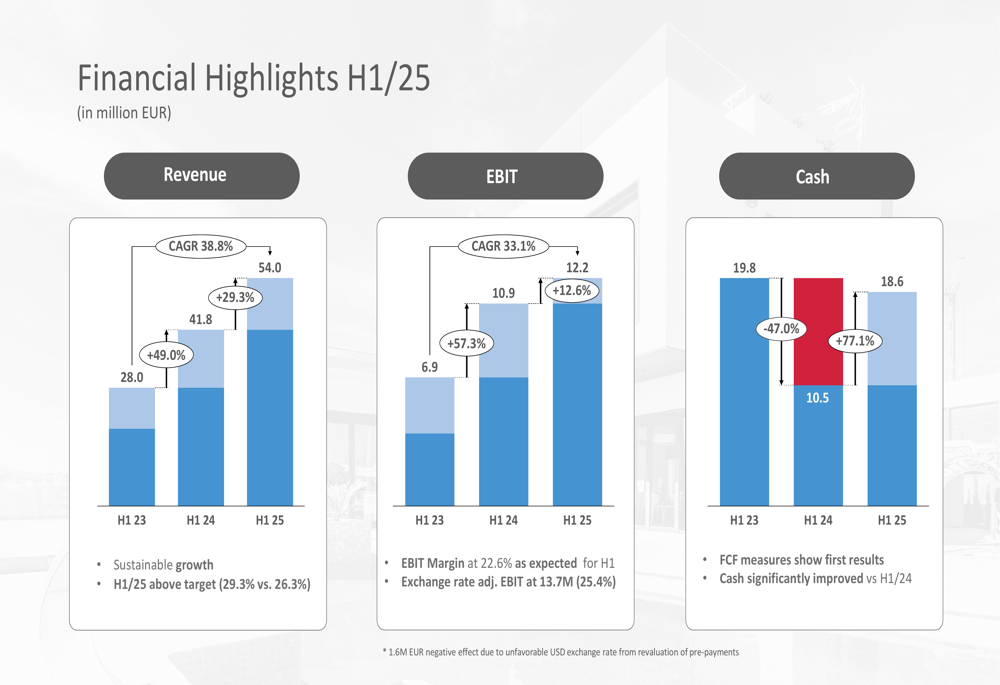

Shelly Group reported H1 2025 revenue of €54.0 million, representing 29.3% year-over-year growth and exceeding the company's target of €52.8 million. EBIT reached €12.2 million with a 22.6% margin, while cash position improved significantly to €18.6 million, up 77.1% from H1 2024.

As shown in the following financial highlights chart:

The company maintained a stable gross margin of 55.8% in H1 2025, demonstrating consistent profitability despite increased investments in sales, marketing, and general administrative expenses. Currency-adjusted EBIT would have reached 25.4%, but was impacted by unfavorable USD/EUR exchange rates that created a €1.6 million negative effect from revaluation of pre-payments.

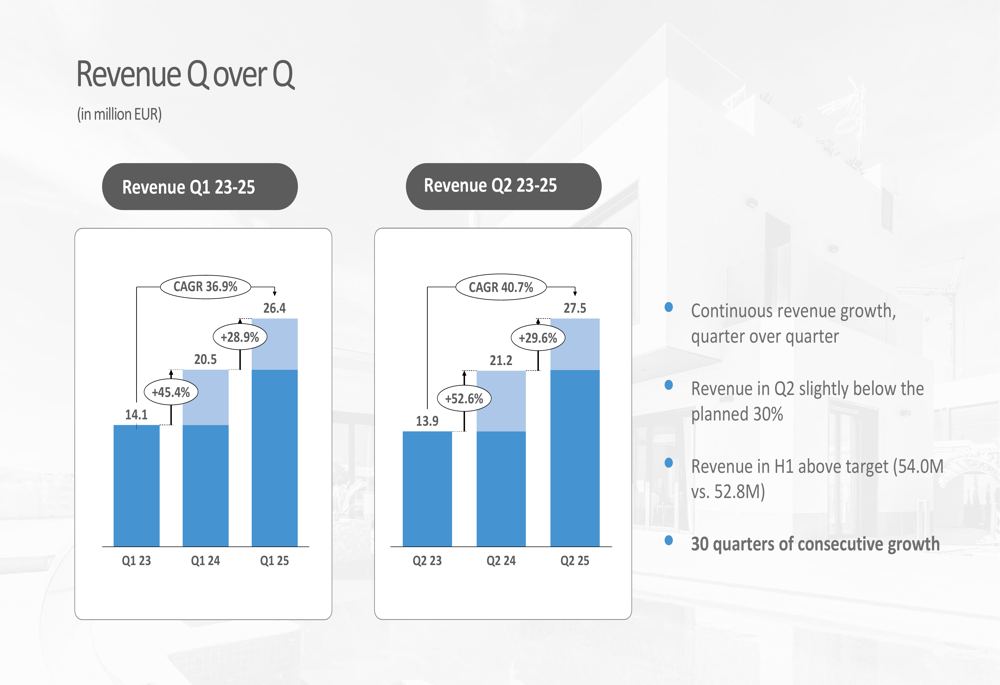

Quarter-over-quarter performance shows steady growth, with Q2 2025 revenue reaching €27.5 million, up 29.6% from Q2 2024:

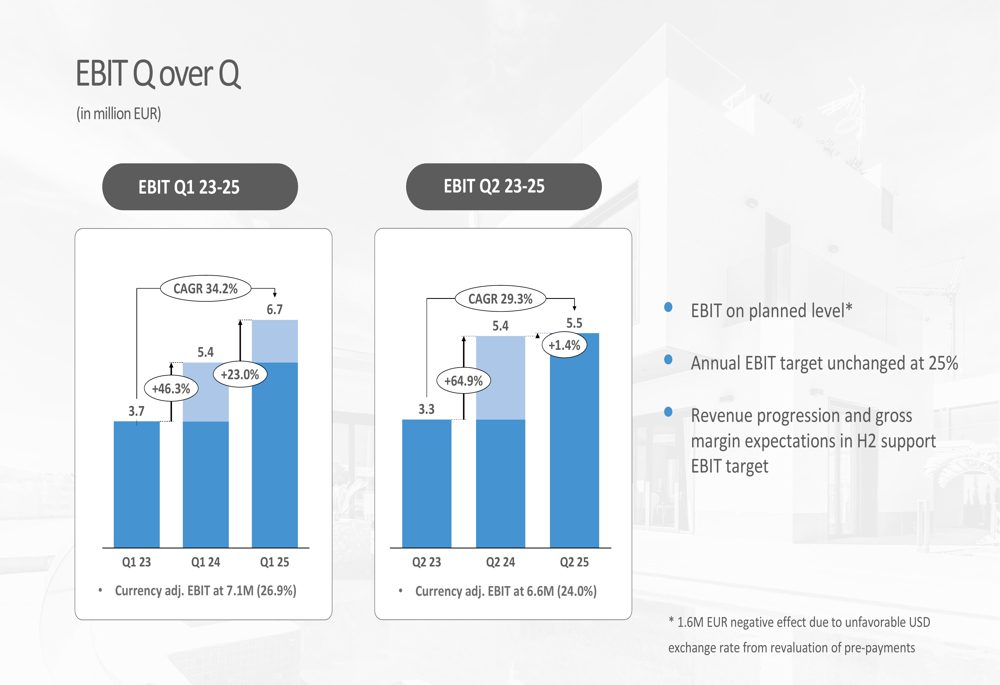

EBIT growth was more modest in Q2 at just 1.4% year-over-year, primarily due to the aforementioned currency effects:

Strategic Initiatives

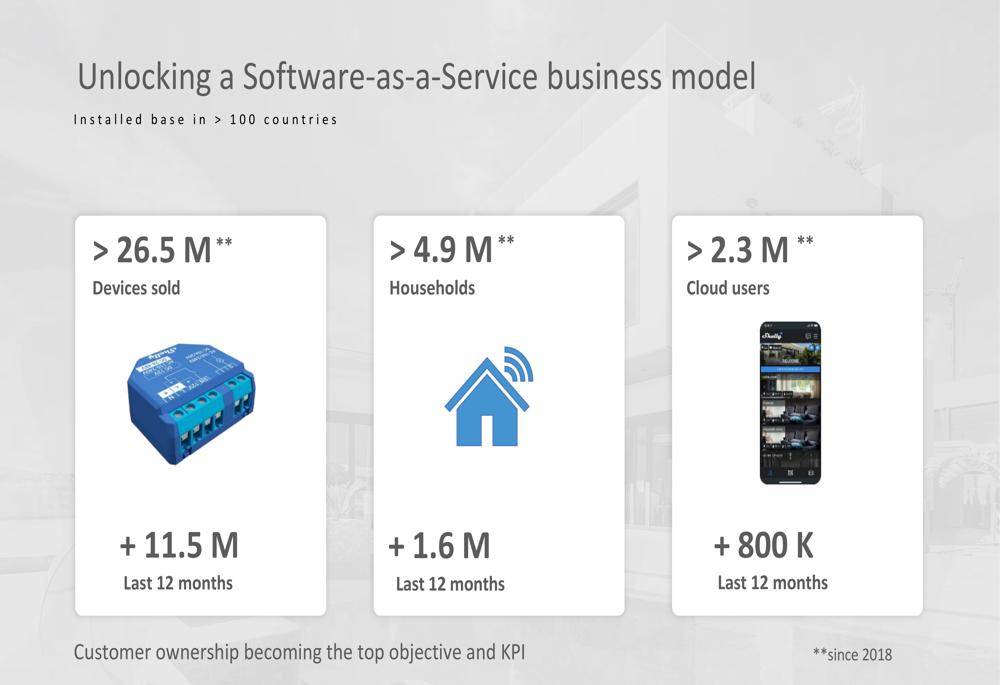

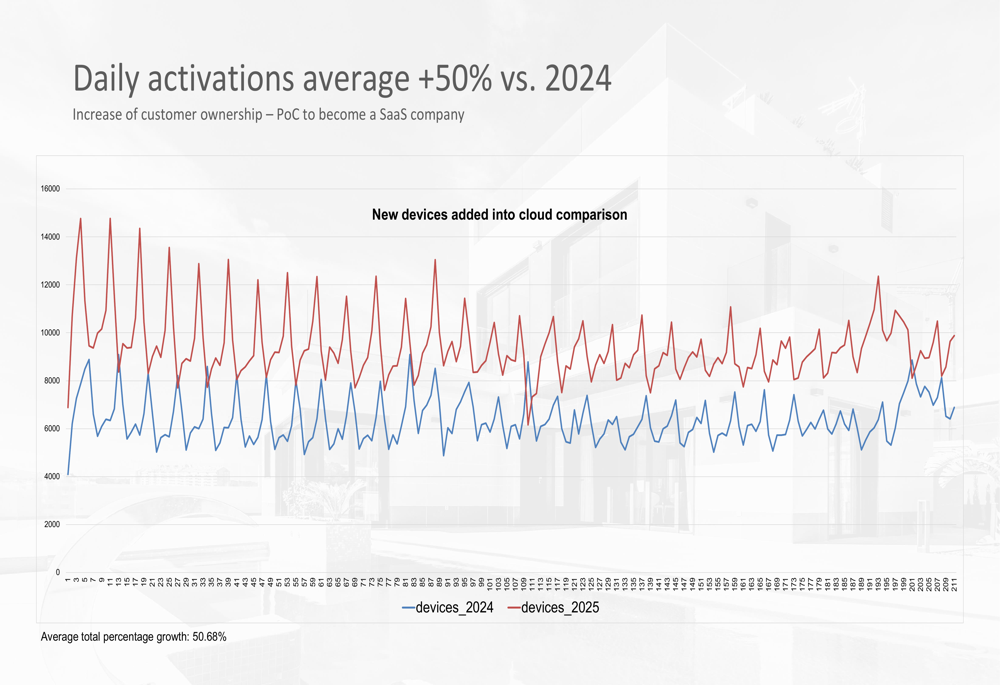

Shelly Group continues to advance its transformation into a SaaS company, with significant progress in building its customer ownership metrics. The company has sold over 26.5 million devices (with 11.5 million in the last 12 months alone), reaching more than 4.9 million households and 2.3 million cloud users.

The following slide illustrates this growing installed base:

Daily cloud activations have increased by 50% compared to 2024, demonstrating strong momentum in the company's software platform adoption:

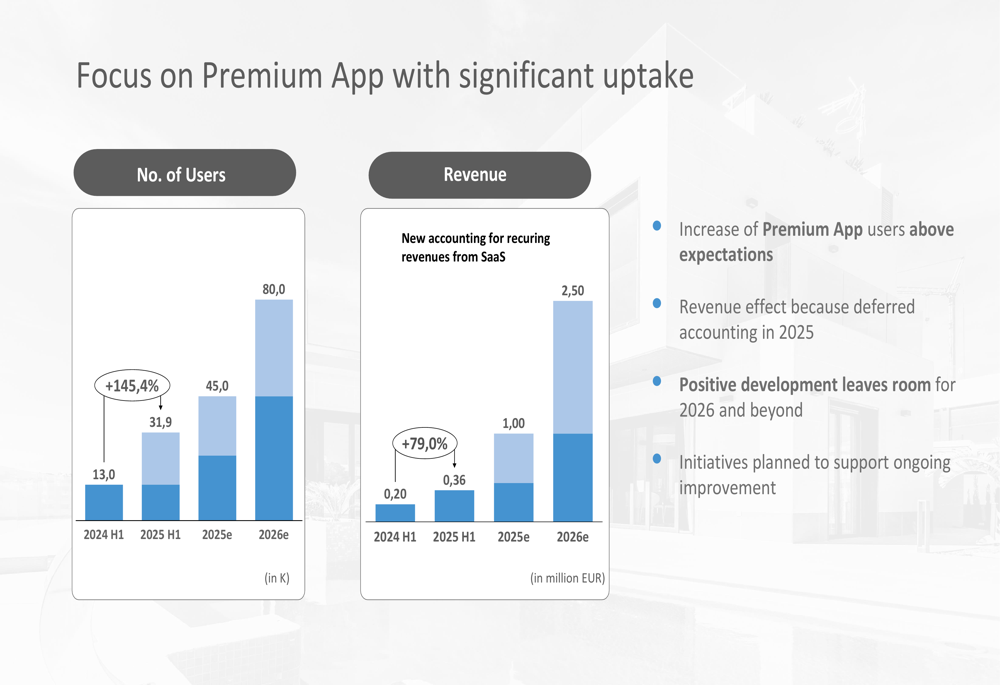

A key element of Shelly's SaaS strategy is its Premium App, which has shown remarkable growth with user numbers increasing 145.4% year-over-year to 31.9 thousand in H1 2025. This subscription service is expected to generate €1 million in revenue for full-year 2025, with projections reaching €2.5 million in 2026:

The company also announced its first co-branded product initiative with Ecoflow, focusing on Smart Home Power Management solutions:

Detailed Financial Analysis

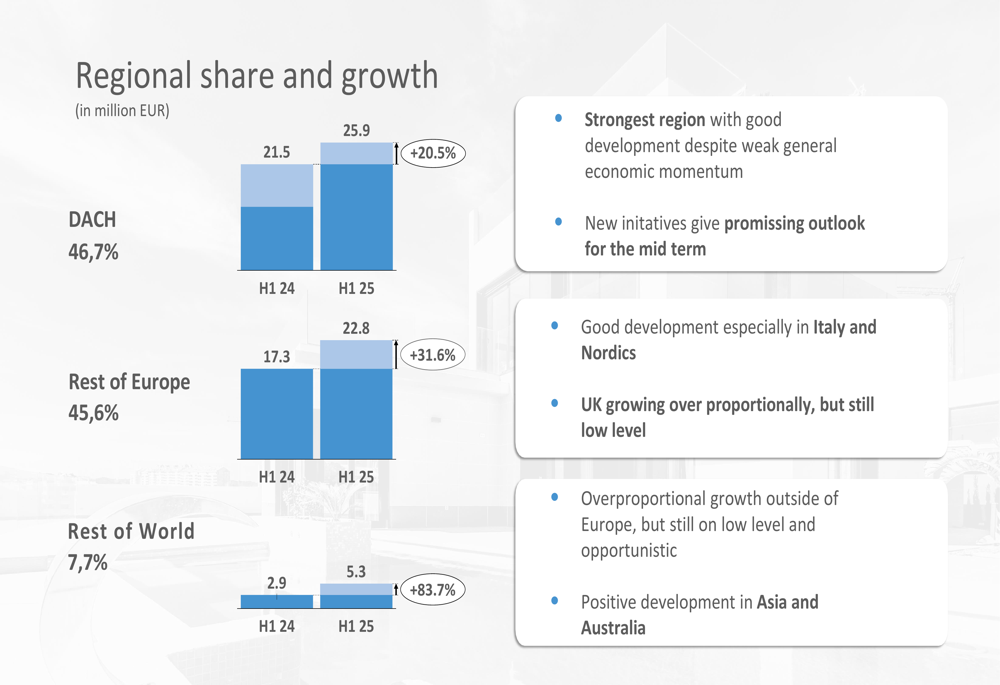

Regional performance shows growth across all markets, with particularly strong results outside Europe. The DACH region (Germany, Austria, Switzerland) remains Shelly's largest market at 46.7% of revenue, growing 20.5% year-over-year. Rest of Europe contributed 45.6% of revenue with 31.6% growth, while Rest of World, though still a small portion at 7.7%, showed impressive 83.7% growth:

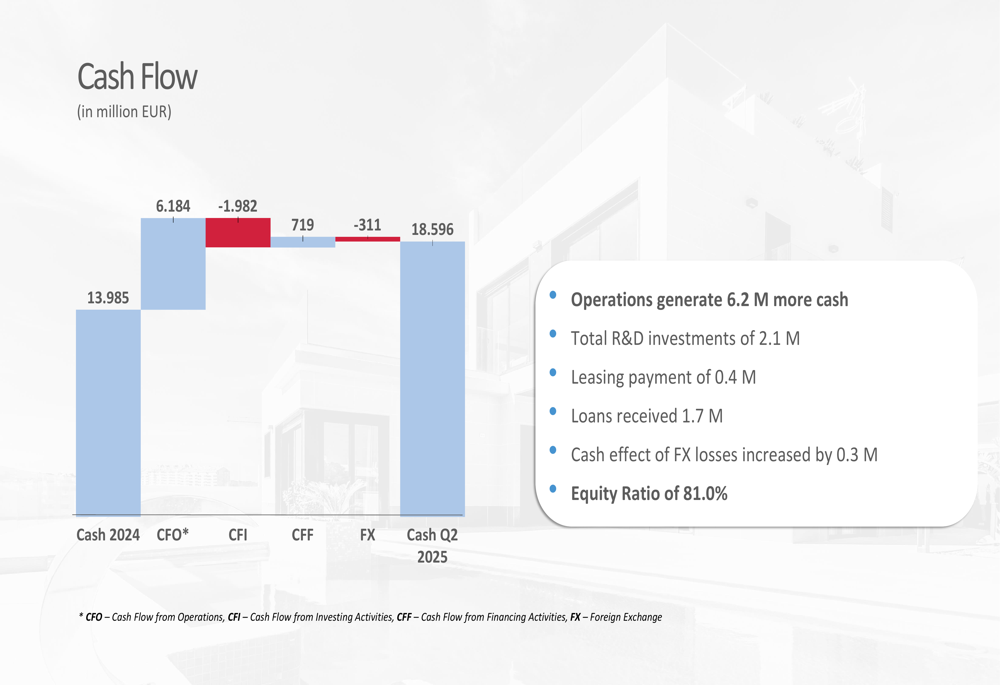

Cash flow has improved significantly, with operations generating €6.2 million more cash compared to the previous year. The company maintains a strong equity ratio of 81.0%:

Working capital optimization initiatives include reducing stock range from 4-5 months to 3-4 months, improving supplier payment terms, implementing more restrictive customer payment terms, and considering factoring options. Margin improvement measures focus on procurement efficiency, increased sea freight usage, and better stock control.

Forward-Looking Statements

Shelly Group's product pipeline is robust, with numerous launches planned throughout 2025. The company is shifting toward newer product generations, with Gen3 and Gen4 products comprising 53% of the portfolio in H1 2025, up from 21% in 2024.

The product roadmap includes significant launches in the second half of 2025, supporting projected revenue growth of 40% in Q3 and 50% in Q4:

Geographic expansion continues with new offices planned in the UK and BeNeLux in Q3 2025, followed by an IBERIA office in Q4. The company is also exploring new verticals including Motors, Insurance, Security Systems, and Energy Contracts to grow its share of wallet and household ownership.

Despite short-term challenges including component shortages, currency effects, and certification complexities, Shelly Group has confirmed its guidance for 2025 and 2026. The company expects to maintain its growth trajectory through expanded distribution channels, new product categories, and continued development of its SaaS business model.

Executive Summary

Shelly Group's H1 2025 results demonstrate continued strong performance with revenue exceeding targets at €54.0 million (+29.3% YoY) and EBIT reaching €12.2 million. The company's strategic shift toward a SaaS model is gaining traction with Premium App subscribers up 145.4% and daily cloud activations increasing 50% year-over-year.

While facing some short-term challenges including currency headwinds and component shortages, the company maintains a positive outlook with an ambitious product roadmap and geographic expansion plans. With 30 consecutive quarters of growth and a strong financial position, Shelly Group appears well-positioned to continue its transformation from a hardware provider to a comprehensive smart home ecosystem company.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.