Texas Roadhouse earnings missed by $0.05, revenue topped estimates

Introduction & Market Context

Siemens AG (OTC:SIEGY) (ETR:SIE) presented its third quarter fiscal year 2025 results on August 7, 2025, showcasing a resilient performance amid ongoing economic uncertainties. The German industrial conglomerate reported robust order growth driven primarily by its Mobility segment, which helped offset weakness in Digital Industries.

The company’s stock was trading up 1.21% following the presentation, suggesting investors responded positively to the maintained full-year outlook despite mixed segment performance. This reaction contrasts with the market’s response to Siemens (ETR:SIEGn)’ Q1 results earlier this year, when the stock declined despite beating earnings expectations.

Quarterly Performance Highlights

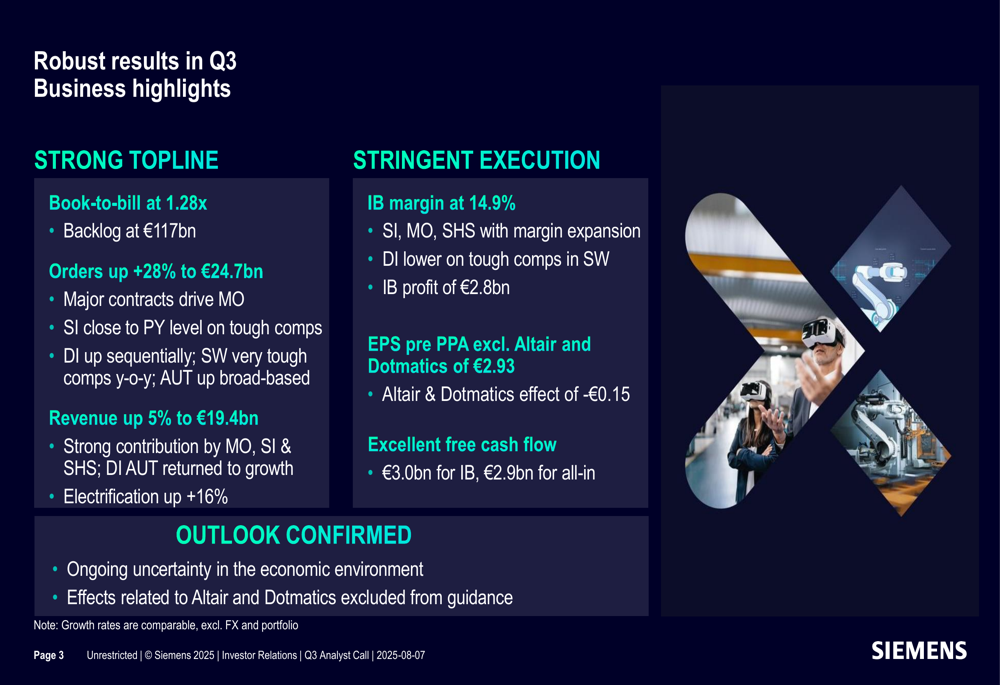

Siemens reported strong topline performance with orders increasing 28% year-over-year to €24.7 billion, resulting in a book-to-bill ratio of 1.28x and a substantial order backlog of €117 billion. Revenue grew 5% to €19.4 billion, with particularly strong contributions from Mobility, Smart Infrastructure, and Siemens Healthineers.

The company’s Industrial Business achieved a profit margin of 14.9%, generating €2.8 billion in profit. Earnings per share before purchase price allocation (PPA) and excluding the effects of recent acquisitions Altair and Dotmatics reached €2.93, with those acquisitions creating a €0.15 negative impact.

As shown in the following quarterly business highlights:

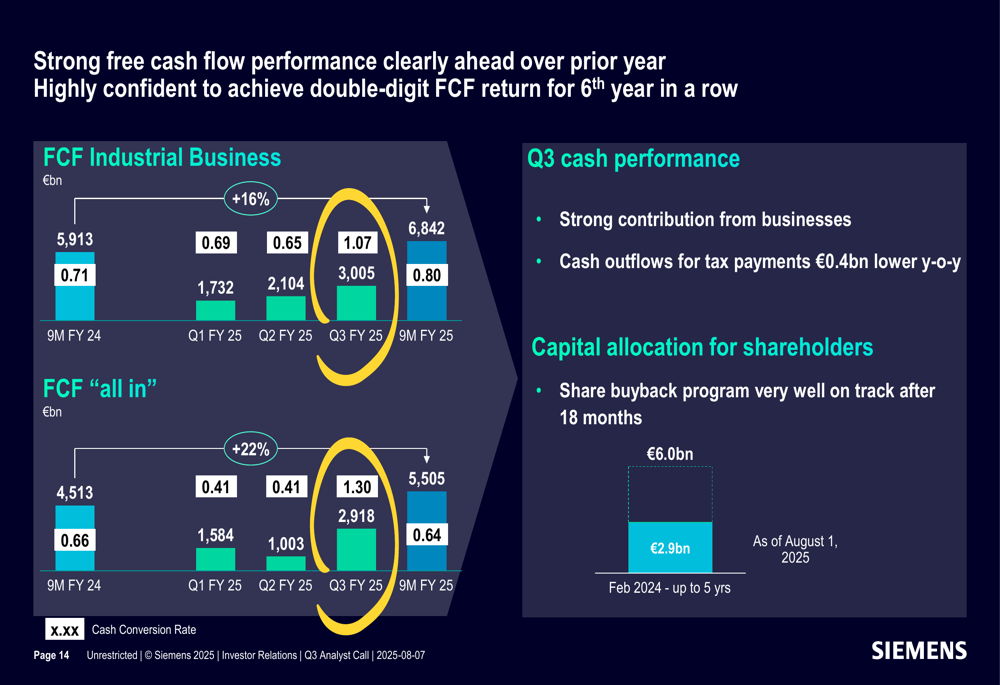

Free cash flow performance was particularly strong, with the Industrial Business generating €3.0 billion and total company cash flow reaching €2.9 billion. This represents significant improvement compared to previous periods and demonstrates the company’s ability to convert earnings into cash.

Segment Analysis

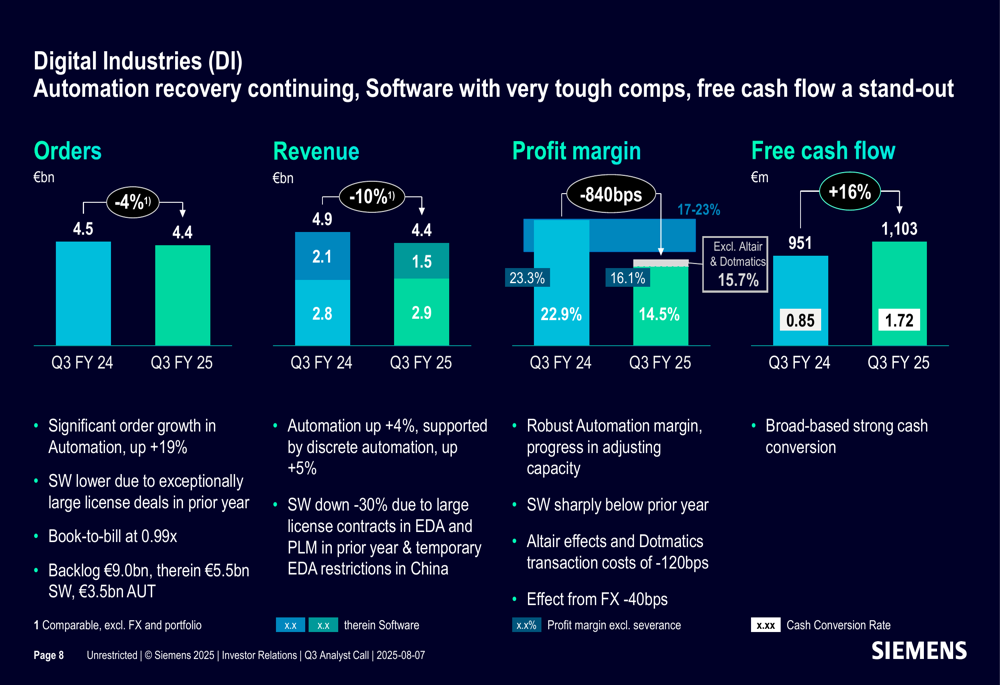

Digital Industries, Siemens’ automation and software division, experienced challenging conditions with orders decreasing 4% to €4.4 billion and revenue declining 10% to €4.4 billion. The segment’s profit margin contracted by 840 basis points, though free cash flow increased 16% to €1.1 billion. The company attributed the revenue decline to significantly lower software sales due to exceptionally large license deals in the prior year.

The following chart illustrates Digital Industries’ performance metrics:

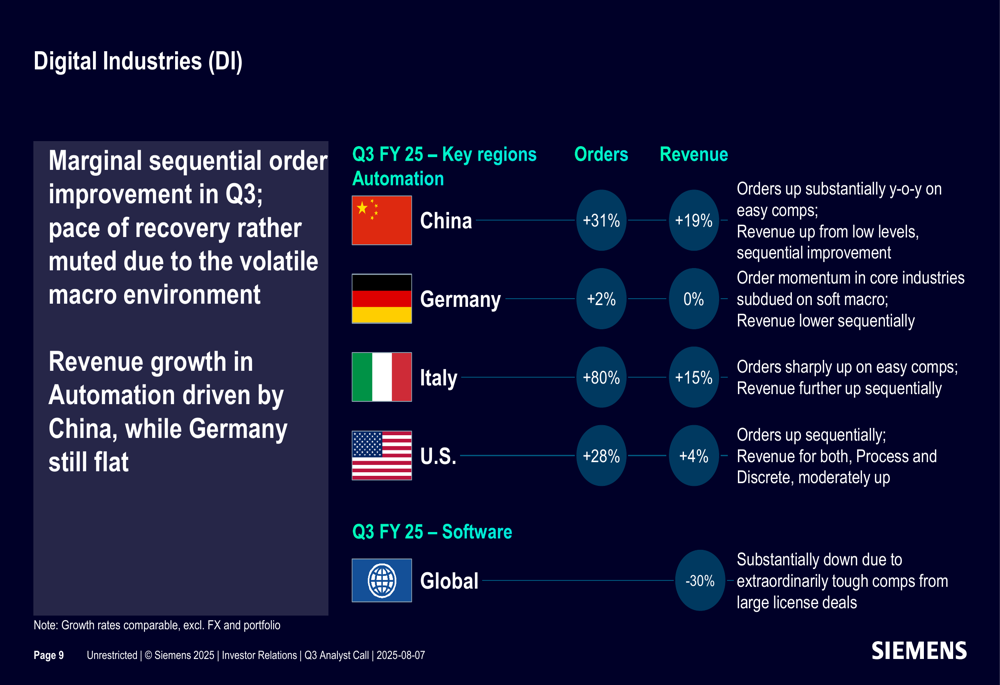

Regional performance within Digital Industries varied considerably, with China showing strong growth (orders +31%, revenue +19%) while software sales globally declined 30% due to tough comparisons with large license deals in the previous year.

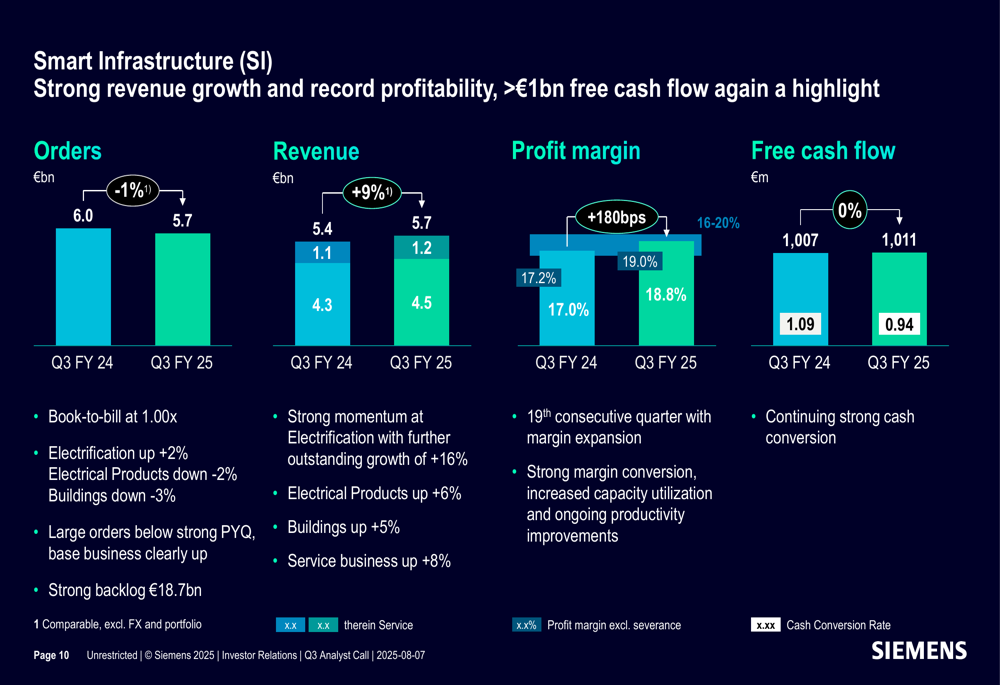

In contrast, Smart Infrastructure delivered solid results with revenue increasing 9% to €5.7 billion, though orders decreased slightly by 1% to €5.7 billion. The segment’s profit margin improved by 180 basis points, and free cash flow remained stable at approximately €1 billion.

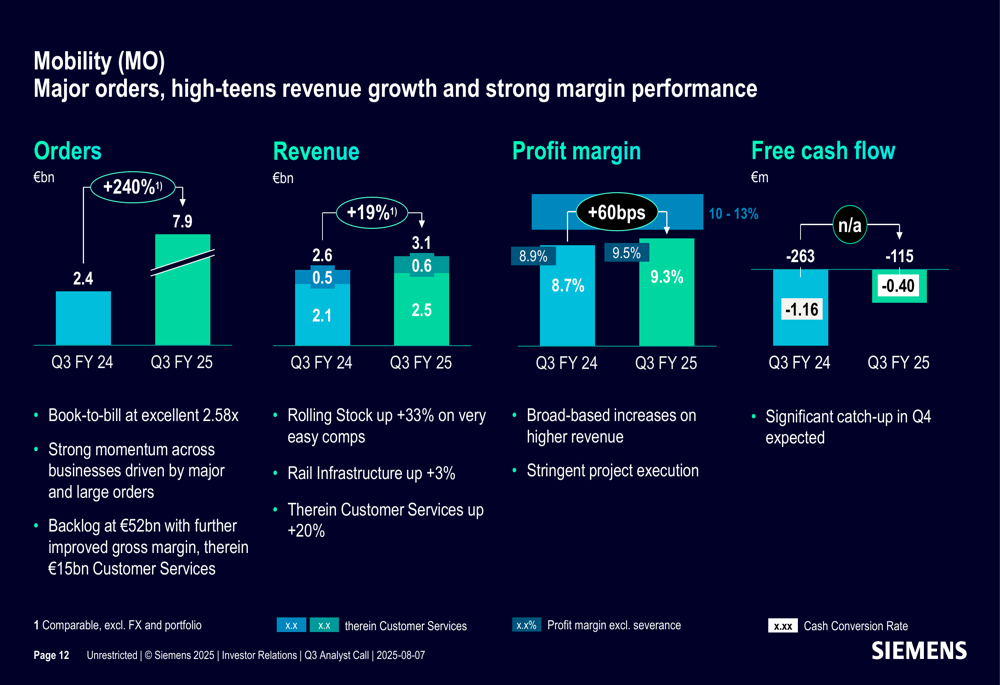

The standout performer was Mobility, which recorded exceptional order growth of 240% to €7.9 billion and revenue growth of 19% to €3.1 billion. Profit margin improved by 60 basis points, and free cash flow, while still negative at -€115 million, showed significant improvement from -€263 million in the prior year period. The segment now has a substantial backlog of €52 billion, providing strong visibility for future revenue.

Digital Transformation Progress

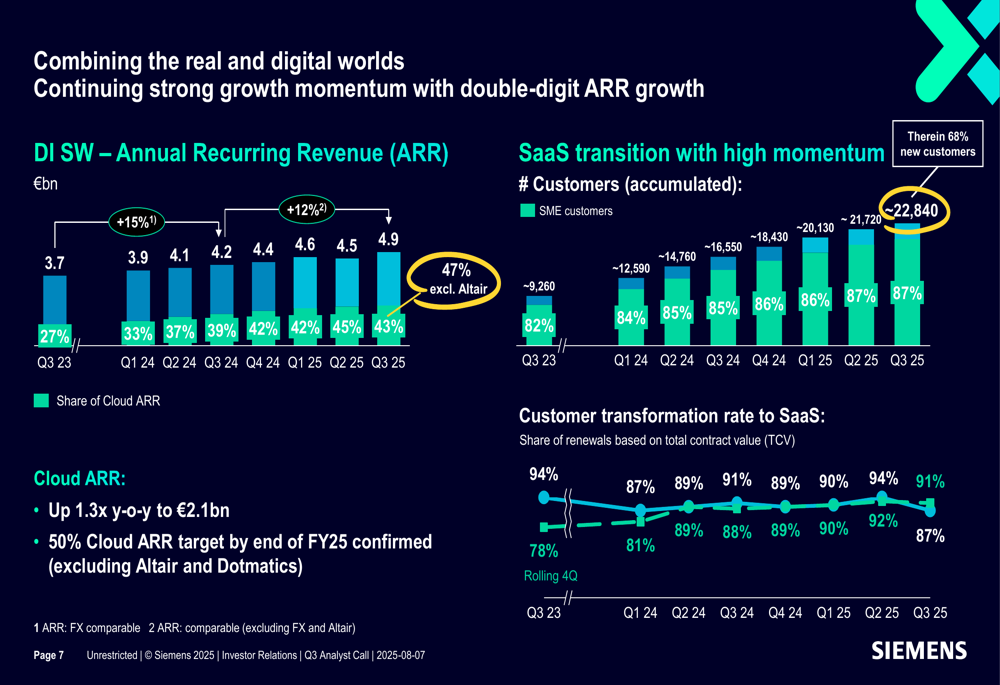

Despite the temporary revenue decline in Digital Industries, Siemens highlighted significant progress in its strategic shift toward software-as-a-service (SaaS) business models. Annual Recurring Revenue (ARR) for Digital Industries software increased from €3.7 billion in Q3 FY23 to €4.9 billion in Q3 FY25, with Cloud ARR growing 1.3 times year-over-year to €2.1 billion.

The company’s SaaS transition is gaining momentum, with the number of customers increasing from approximately 9,260 in Q3 FY23 to around 22,840 in Q3 FY25. Notably, 68% of these are new customers, indicating Siemens is successfully expanding its customer base through cloud offerings. The customer transformation rate to SaaS has improved from 78% in Q3 FY23 to 91% in Q3 FY25.

The following chart illustrates this digital transformation progress:

Siemens confirmed its target of reaching 50% Cloud ARR by the end of FY25, excluding the impact of Altair and Dotmatics acquisitions. This transition, while creating short-term revenue pressure due to the shift from upfront license sales to subscription models, is expected to generate more stable and predictable revenue streams over time.

Financial Position & Cash Flow

Siemens maintained a strong financial position with Industrial net debt to EBITDA ratio at 1.0x, indicating conservative leverage. The company noted that its capital structure will remain well within target corridors even after the closing of the Dotmatics acquisition.

The pension deficit remained at a historic low of €0.8 billion, and the company successfully completed a dual bond issuance of €4 billion and US$7 billion at attractive interest rates, demonstrating continued access to capital markets on favorable terms.

Free cash flow for the first nine months of FY25 reached €6.84 billion for the Industrial Business, compared to €5.91 billion in the same period of FY24. Total (EPA:TTEF) company free cash flow improved to €5.51 billion from €4.51 billion. The company also reported that its share buyback program was "very well on track" after 18 months.

Forward-Looking Statements

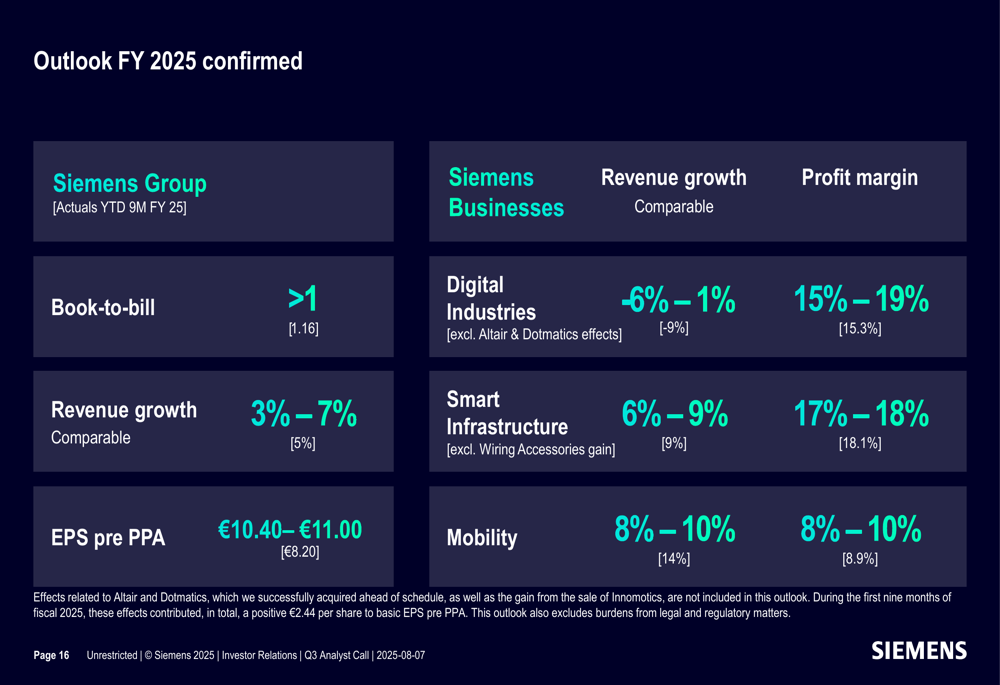

Siemens confirmed its outlook for fiscal year 2025 despite ongoing economic uncertainties. The company expects:

- Book-to-bill ratio greater than 1

- Revenue growth of 3-7%

- Earnings per share before PPA of €10.40-€11.00

For individual segments, Siemens forecasts:

- Digital Industries: Revenue growth between -6% and 1%, with profit margin of 15-19%

- Smart Infrastructure: Revenue growth of 6-9%, with profit margin of 17-18%

- Mobility: Revenue growth of 8-10%, with profit margin of 8-10%

The following slide details the company’s outlook:

The company’s "ONE Tech Company" program continues to focus on investments in strategic acquisitions and productivity improvements. Recent investments include the closing of the Dotmatics acquisition, acquisition of ebm-papst’s IDT business, and the opening of a high-tech train factory and service center in Munich.

Siemens also emphasized its sustainability initiatives, highlighting decarbonization efforts in freight locomotives in India, resource efficiency through modular edge data centers, and its EcoTech Label program which has certified 50,000 products with independently verified environmental impact.

In conclusion, Siemens’ Q3 FY25 results demonstrate the company’s ability to navigate challenging market conditions through its diversified portfolio, with exceptional performance in Mobility offsetting weakness in Digital Industries. The maintained full-year guidance suggests management confidence in the company’s trajectory despite ongoing economic uncertainties and the short-term revenue impact of the digital transformation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.