Wall St futures flat amid US-China trade jitters; bank earnings in focus

Introduction & Market Context

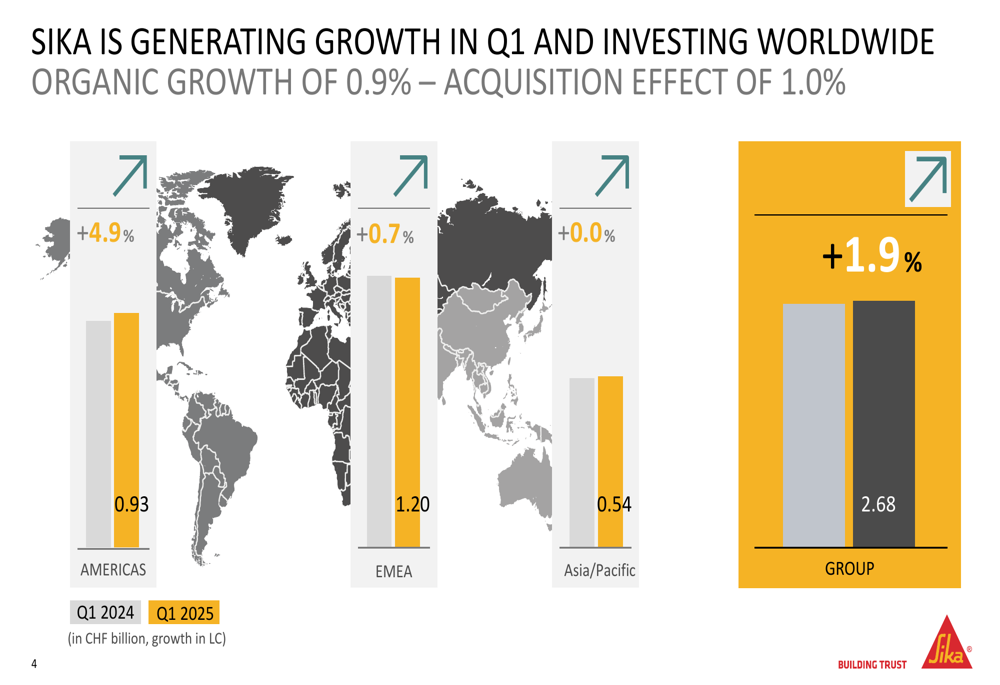

Sika (SIX:SIKA) AG reported modest growth in the first quarter of 2025, achieving sales of CHF 2,678.3 million, representing a 1.9% increase in local currencies and 1.1% growth in Swiss francs compared to the same period last year. Despite facing what the company described as "unpredictable markets," Sika maintained its investment strategy with new acquisitions and production facilities across multiple regions.

The construction materials specialist delivered organic growth of 0.9% in Q1, complemented by a 1.0% contribution from acquisitions. This performance comes after a strong 2024, when the company achieved record results with 7.4% growth in local currencies.

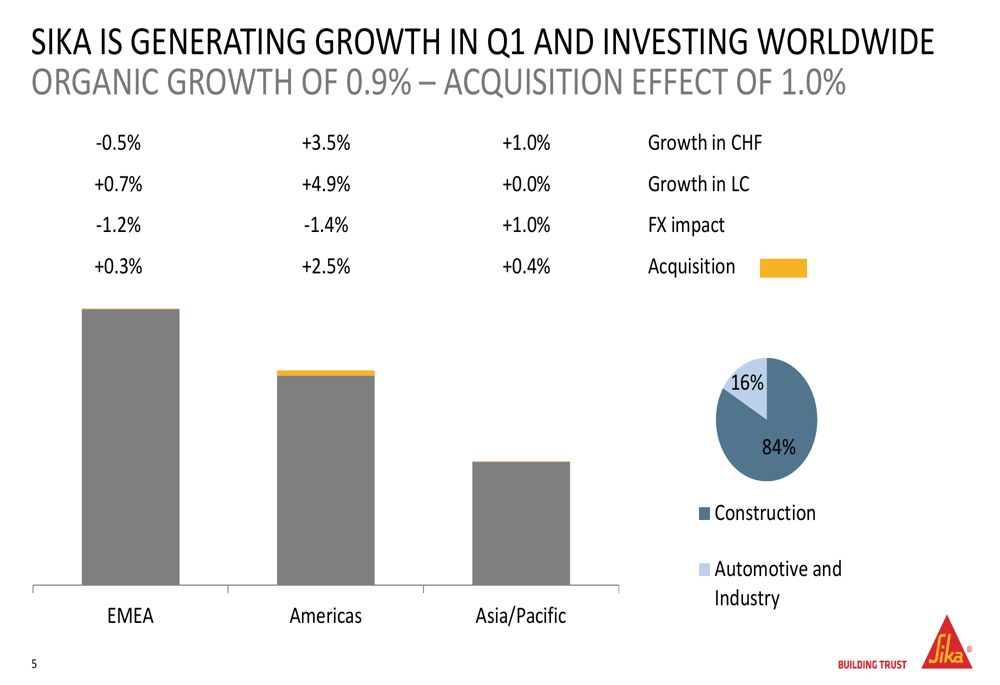

As shown in the following regional sales growth chart, performance varied significantly across markets, with the Americas region leading growth while Asia/Pacific remained flat:

Quarterly Performance Highlights

Regional performance in Q1 2025 showed notable variations, with the Americas delivering the strongest results at 4.9% growth in local currencies. The EMEA (Europe, Middle East, Africa) region posted modest growth of 0.7%, while Asia/Pacific recorded flat performance at 0.0%.

Currency effects impacted overall results, with negative FX impacts in EMEA (-1.2%) and Americas (-1.4%), while Asia/Pacific benefited from a positive currency effect of 1.0%. The following breakdown illustrates these regional differences and the company’s sales distribution by market segment:

Construction activities continue to dominate Sika’s business, accounting for 84% of sales, with automotive and industrial applications representing the remaining 16%. This distribution has remained relatively stable compared to previous periods.

Strategic Initiatives

Despite slowing growth, Sika has maintained an active investment strategy in early 2025, focusing on both organic expansion and strategic acquisitions. The company highlighted several key investments made between January and April 2025:

These investments align with Sika’s Strategy 2028, which emphasizes market penetration, innovation, and strategic acquisitions. The company has established a strong track record in M&A activities, completing 16 bolt-on acquisitions with an average size of CHF 50 million in sales (excluding the larger MBCC acquisition) between 2020 and 2024.

Sika’s acquisition strategy continues to be selective, as illustrated by its M&A funnel showing that only a small percentage of potential targets ultimately result in completed transactions:

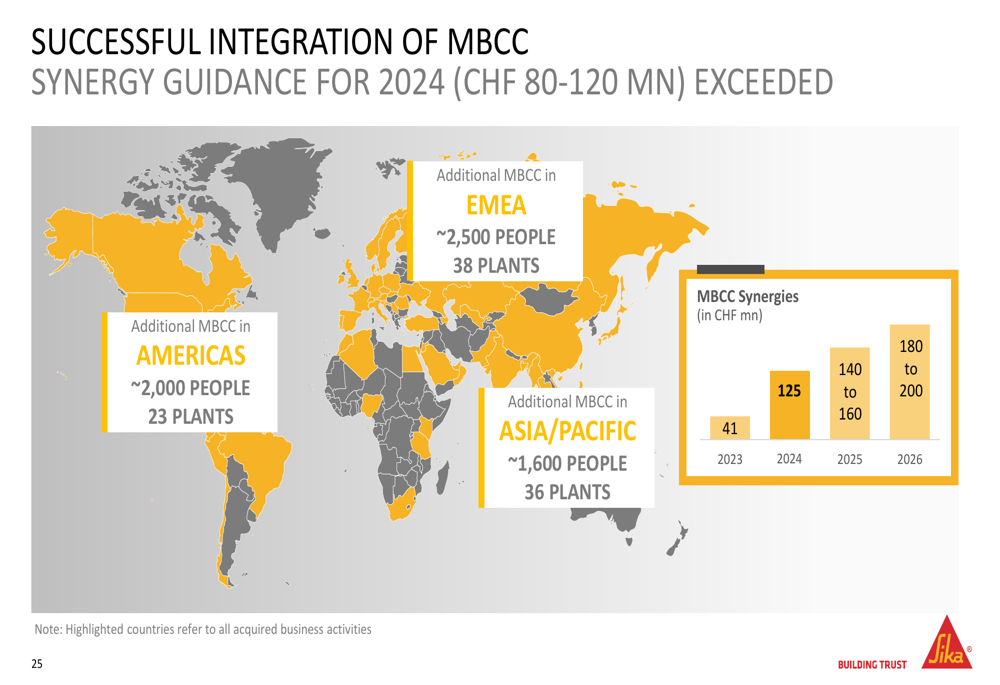

The integration of MBCC, Sika’s largest recent acquisition, has exceeded expectations. The company reported CHF 125 million in synergies for 2024, surpassing its guidance of CHF 80-120 million. Synergies are projected to reach CHF 140-160 million in 2025 and CHF 180-200 million by 2026.

Detailed Financial Analysis

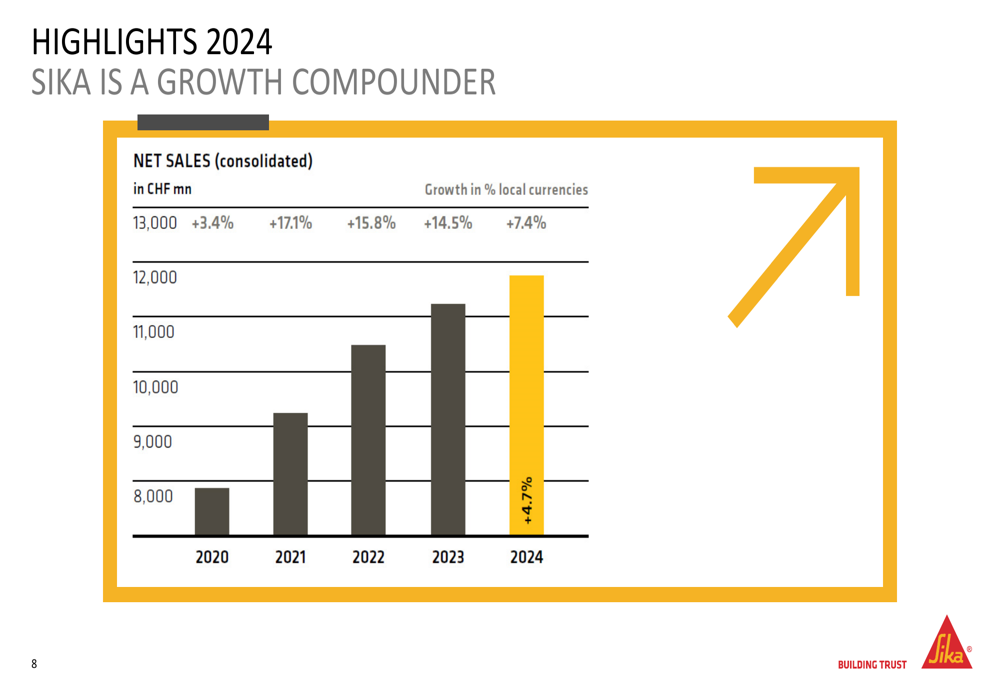

While Q1 2025 showed modest growth, Sika’s full-year 2024 performance demonstrated the company’s ability to deliver strong results. The following chart illustrates Sika’s consistent sales growth trajectory over the past five years:

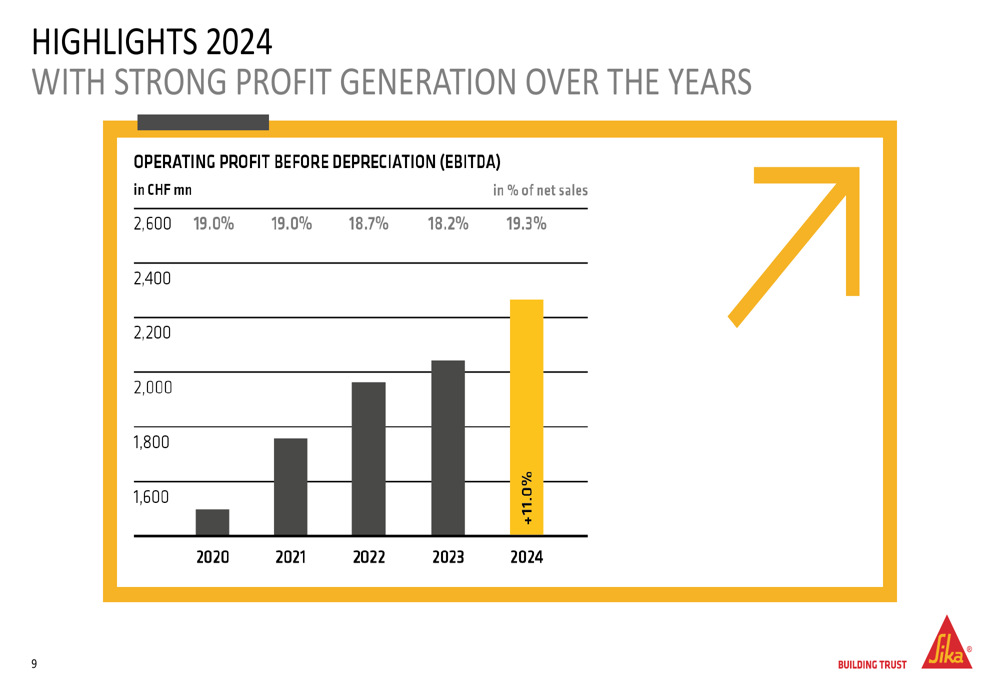

This sales growth has been accompanied by even stronger profit generation, with EBITDA increasing by 11.0% in 2024 to reach CHF 2,269.5 million, representing 19.3% of net sales (up from 18.2% in 2023):

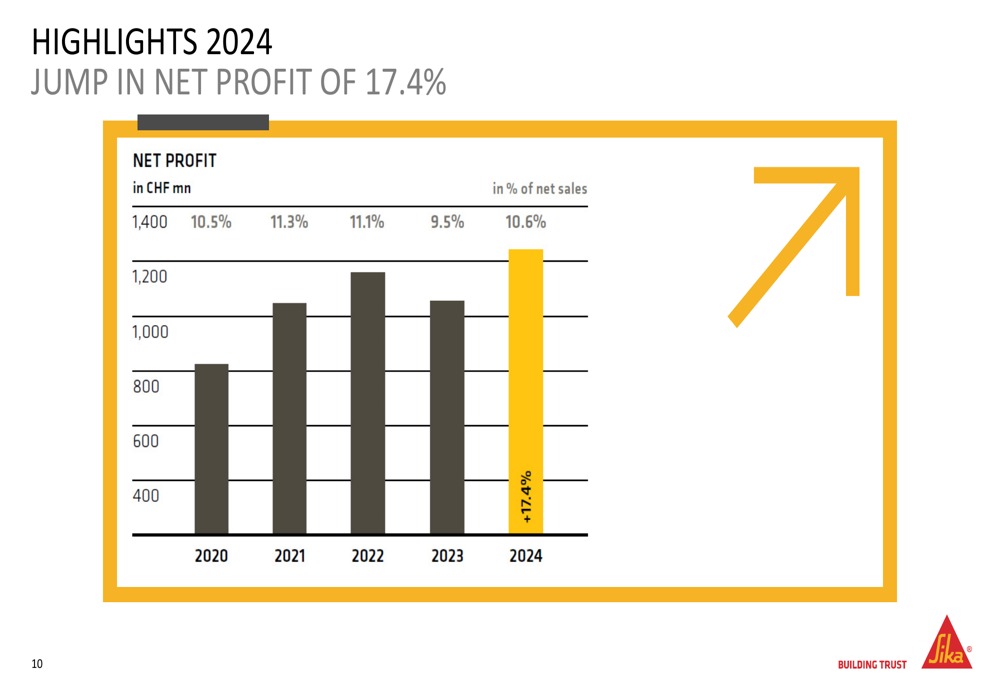

Net profit showed an even more impressive jump of 17.4% in 2024, reaching CHF 1,247.6 million:

This strong profit performance translated into earnings per share growth of 16.7% to CHF 7.76 in 2024, allowing the company to increase its dividend to CHF 3.60 per share (from CHF 3.30 in 2023).

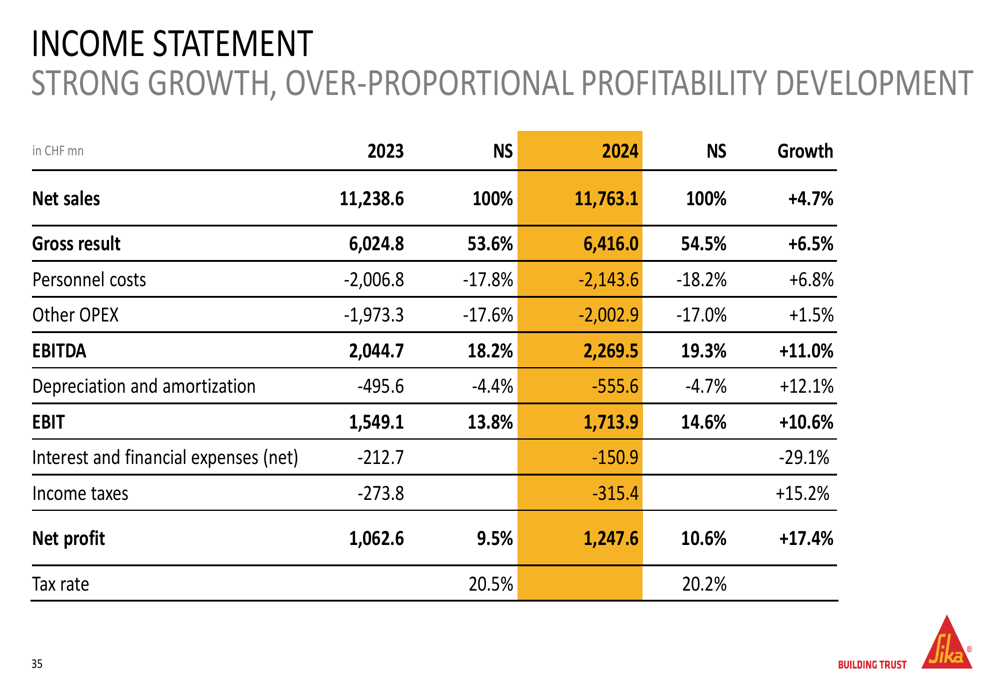

The following income statement highlights summarize Sika’s 2024 financial performance:

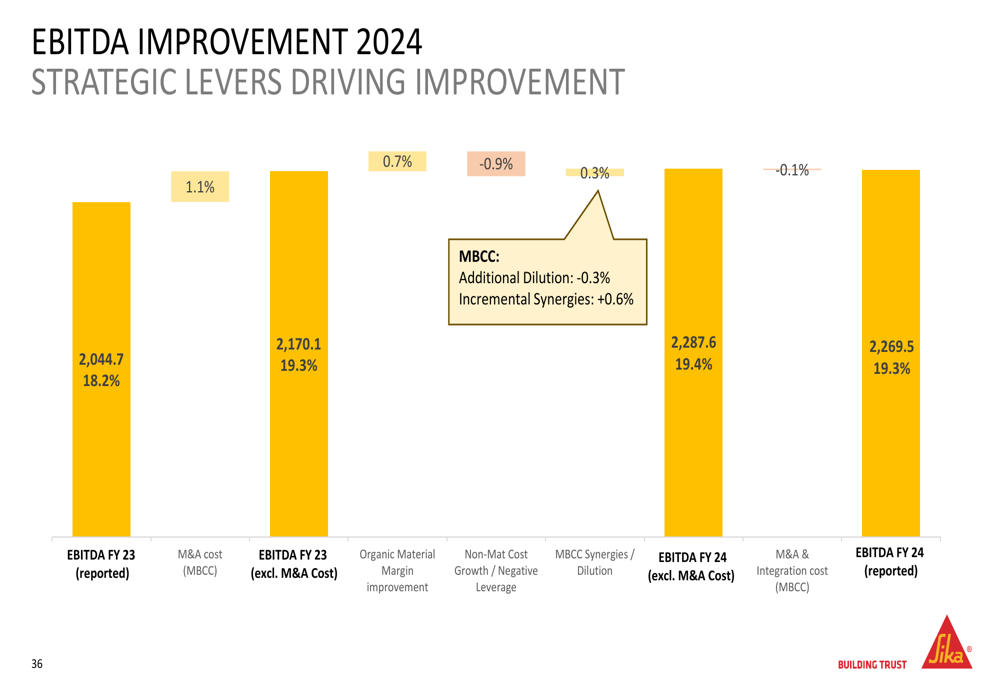

Several factors contributed to Sika’s EBITDA improvement in 2024, including material margin expansion, operational efficiencies, and synergies from the MBCC acquisition:

Forward-Looking Statements

Looking ahead to the remainder of 2025, Sika confirmed its outlook while acknowledging "increased market uncertainties arising from potentially prolonged trade conflicts." The company expects sales growth in local currencies of 3-6% for the full year 2025, with an over-proportional increase in EBITDA and expansion of the EBITDA margin to 19.5%-19.8%.

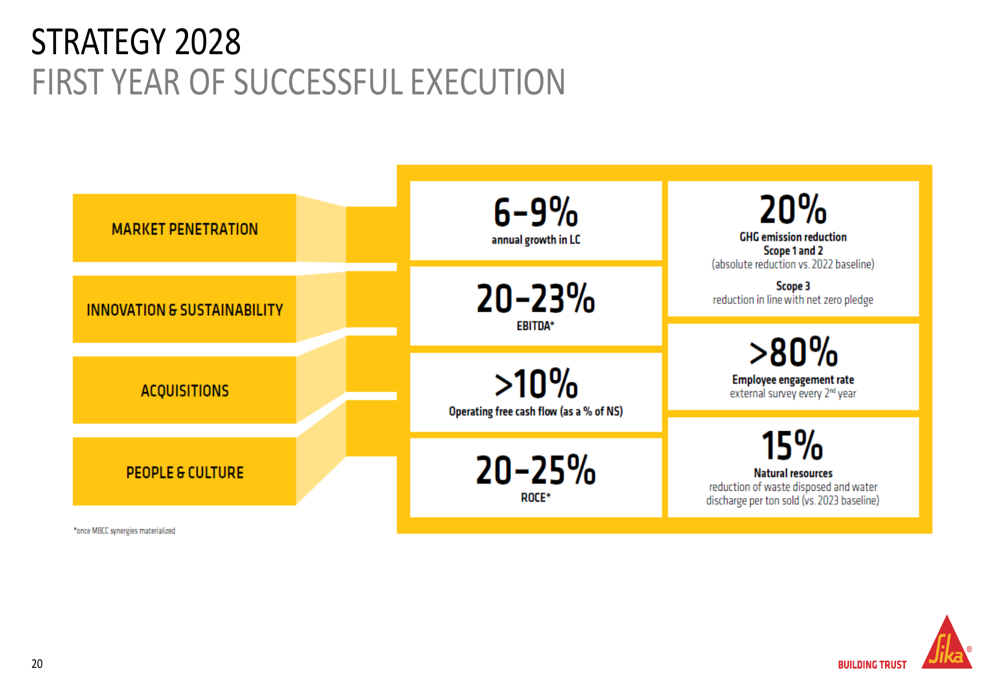

Sika also reaffirmed its commitment to its Strategy 2028, which targets:

- 6-9% annual growth in local currencies

- EBITDA margin of 20-23%

- Operating free cash flow above 10% of net sales

- Return on capital employed (ROCE) of 20-25%

- 20% reduction in greenhouse gas emissions (Scope 1 and 2)

- Employee engagement rate above 80%

- 15% reduction in waste disposed and water discharge

The company continues to focus on innovation as a key driver of future growth. Recent developments include new fiber technologies for reinforced concrete that improve durability and reduce CO2 emissions, concrete recycling solutions, self-healing membranes for modern flat roofs, conductive flooring systems, and cement-free tile adhesives with 50% lower carbon footprints.

Competitive Industry Position

Sika maintains that it is "gaining market share over the years" by consistently outgrowing its peers. The company has a balanced business mix across residential (20%), infrastructure (30%), commercial (35%), and automotive & industry (15%) segments, providing diversification against market fluctuations in any single sector.

The company highlighted its involvement in major infrastructure projects worldwide, including the Gordie Howe International Bridge between the USA and Canada (the world’s longest cable-stayed bridge in North America), the M2 Highway in Montenegro, and the Thames Tideway Tunnel in London.

Sika is also positioning itself to capitalize on the growing data center construction market, which is projected to see global investments of CHF 700 billion by 2028. The company emphasizes that its solutions can save approximately 13,000 tons of CO2 equivalent throughout the lifetime of a typical 25,000 m² data center.

Despite the current slowdown in growth, Sika’s CEO has expressed confidence in the company’s market position, stating in previous communications that "Sika is stronger than ever on multiple axes" and that the company has "the strongest portfolio in the industry by far."

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.