5 big analyst AI moves: Apple lifted to Buy, AI chip bets reassessed

Introduction & Market Context

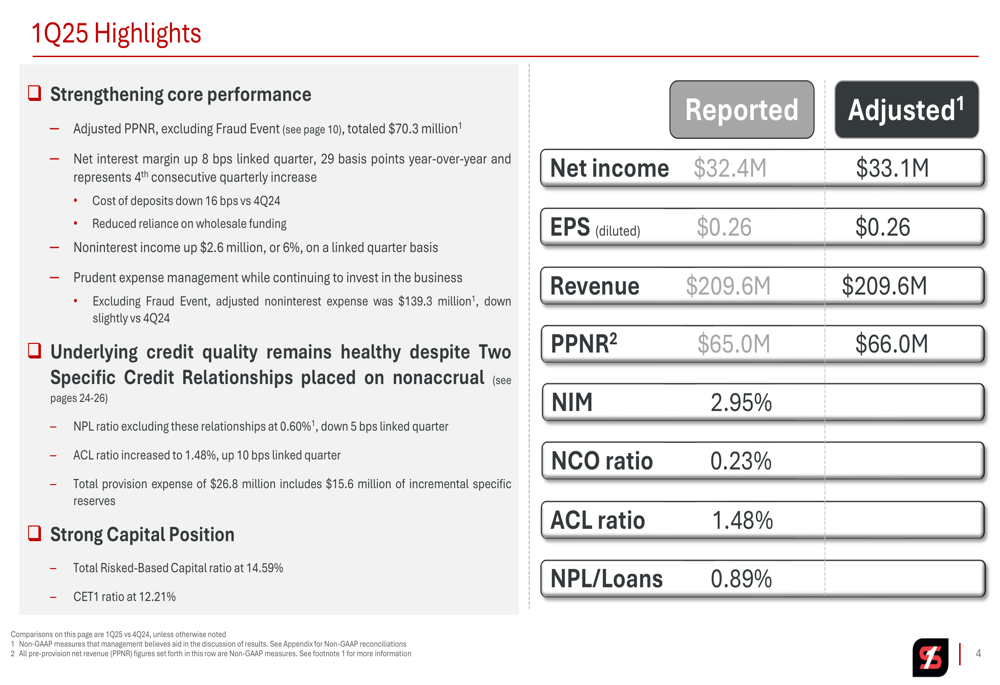

Simmons First National Corporation (NASDAQ:SFNC) released its first quarter 2025 earnings presentation on April 16, highlighting mixed results that included credit quality challenges alongside improving core operating metrics. The company reported earnings per share of $0.26, missing analyst expectations of $0.358, while revenue slightly exceeded forecasts at $209.58 million versus the expected $209.14 million.

The stock reacted negatively to the results, declining 0.93% in the regular session following the announcement and dropping a further 0.61% in premarket trading, bringing the price to $18. As of the latest trading data, SFNC shares have fallen 3.15% to $17.54, reflecting investor concerns about the credit quality issues highlighted in the presentation.

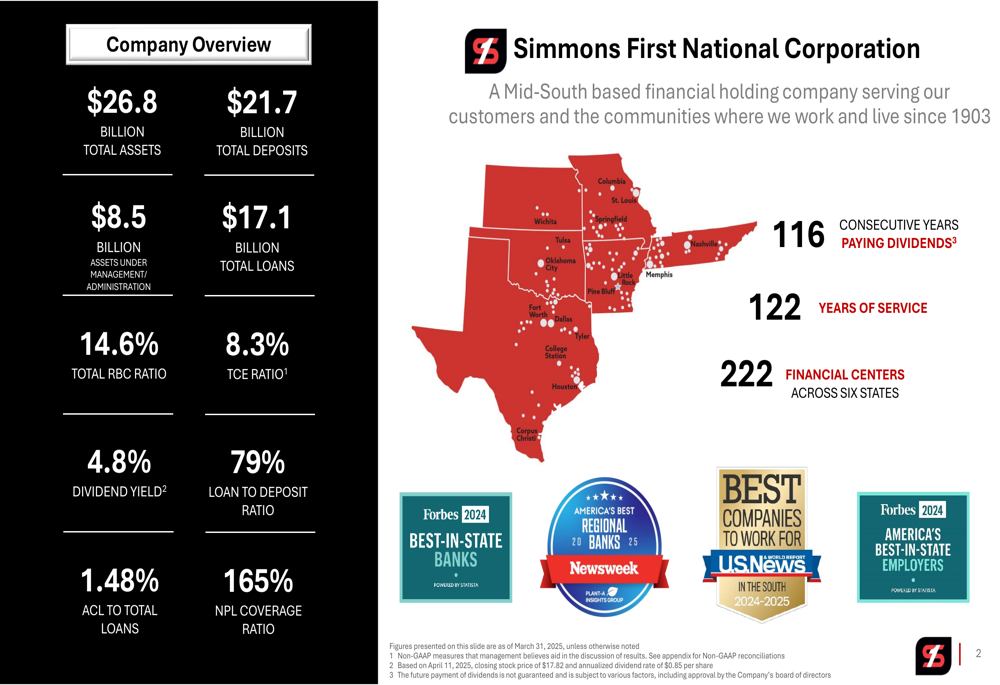

As shown in the following company overview, Simmons First National maintains a substantial footprint across six states with $26.8 billion in total assets:

Quarterly Performance Highlights

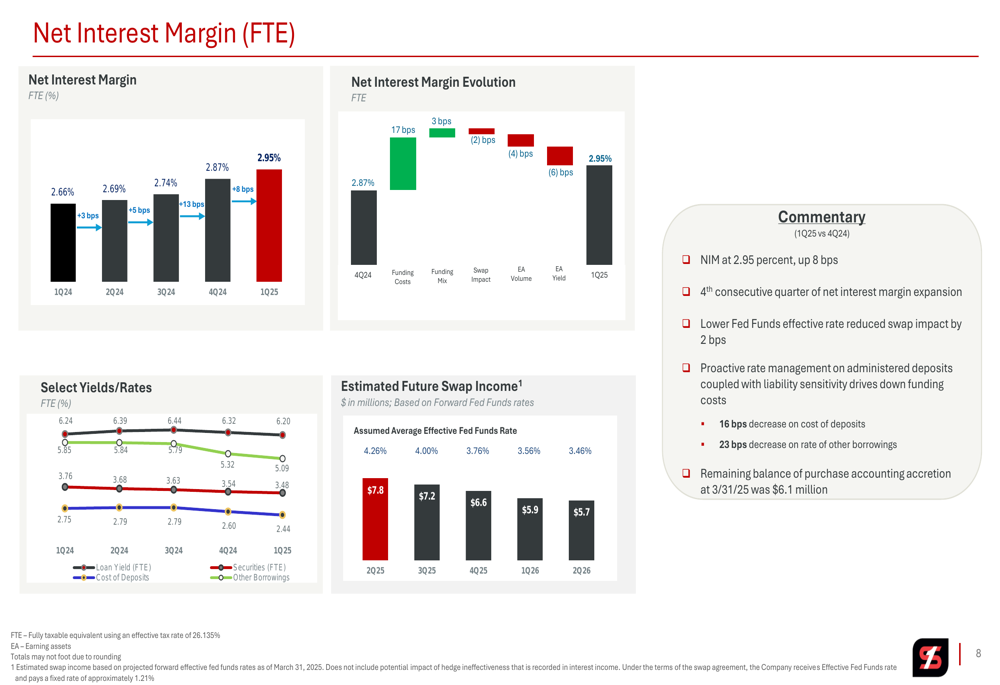

Despite the earnings miss, Simmons First National reported several positive core operating trends in the first quarter. Net interest margin (NIM) improved to 2.95%, up 8 basis points from the previous quarter and 29 basis points year-over-year. The company also saw a 6% increase in noninterest income and a 16 basis point reduction in deposit costs compared to Q4 2024.

The following slide highlights key financial metrics for Q1 2025, including the reported net income of $32.4 million and pre-provision net revenue (PPNR) of $65.0 million:

Net interest margin expansion has been a bright spot for the bank, driven by favorable asset repricing and improvements in funding mix. As illustrated in the following chart, NIM has steadily increased from 2.69% in Q1 2024 to 2.95% in Q1 2025:

During the earnings call, Jay Brogdon, President of Simmons First National, emphasized the positive trajectory of core performance: "This was our fourth consecutive quarter delivering top line adjusted revenue growth and net interest margin expansion."

Credit Quality Concerns

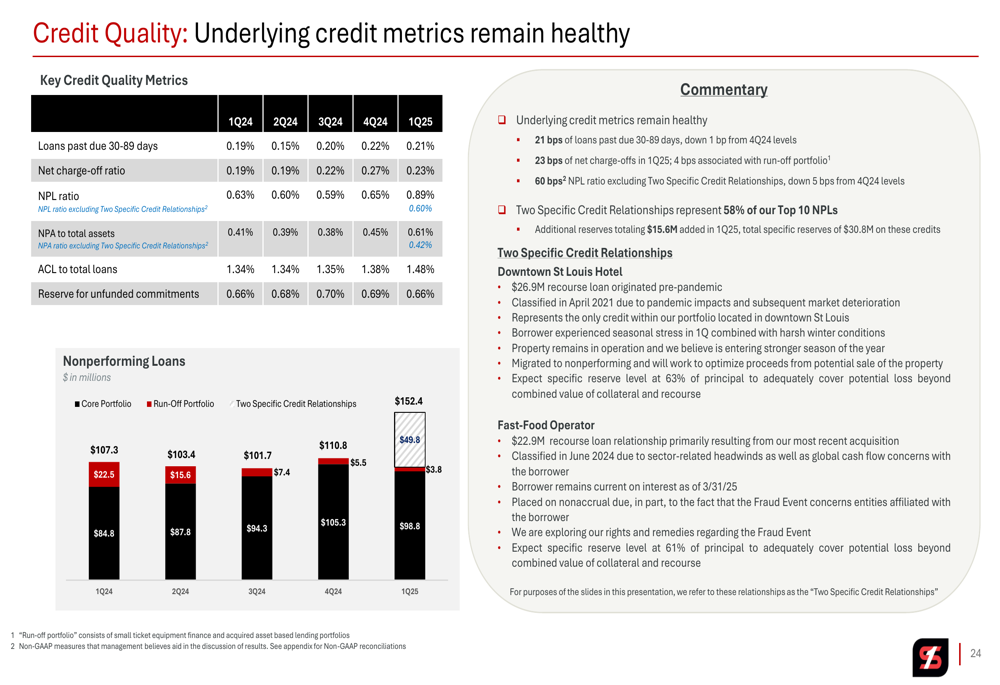

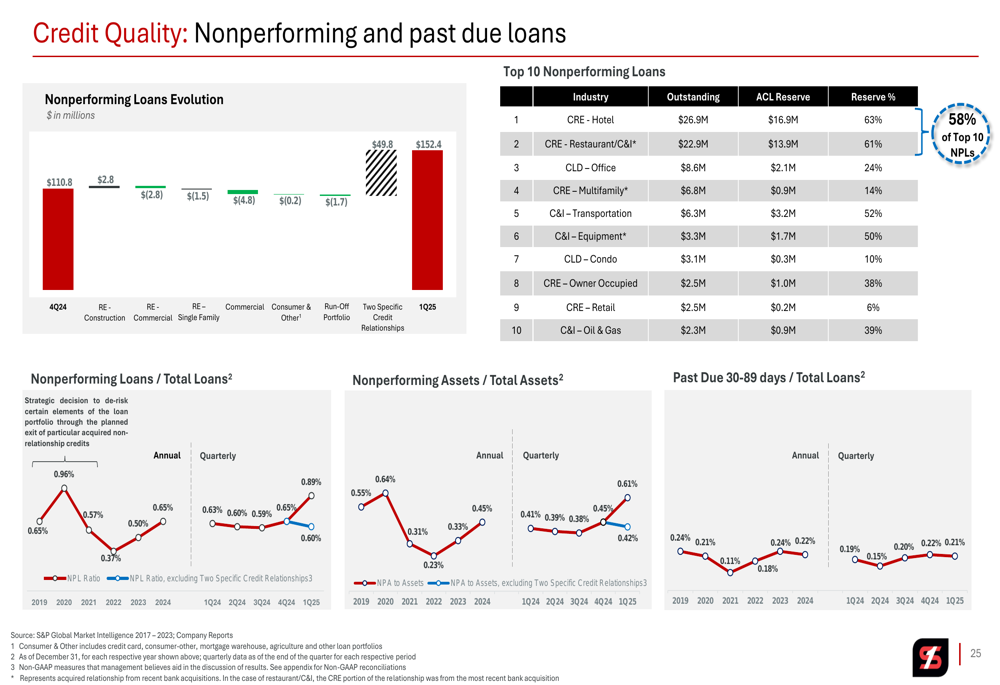

The primary factor impacting Q1 results was the deterioration of two specific credit relationships that were placed on nonaccrual status. The first involves a $27 million loan for a hotel property in Downtown St. Louis that has been classified since early 2021, primarily due to pandemic-related challenges and subsequent deterioration of business activity in that area.

The second is a $23 million relationship with a fast food franchise operator, which was primarily acquired through the company’s most recent acquisition. This relationship was complicated by a $4.3 million fraud event involving deposit accounts of entities affiliated with the borrower.

The company increased specific reserves on these loans from approximately 30% to 60%, resulting in additional provision expense of $15.6 million in the quarter. Total (EPA:TTEF) provision expense was $26.8 million, causing the allowance for credit losses (ACL) ratio to increase to 1.48% from 1.38% in the previous quarter.

The following slide shows key credit quality metrics, including the impact of these two relationships on nonperforming loans:

Management emphasized that these credit issues appear isolated, noting that excluding the two specific relationships, nonperforming loans would have declined 5 basis points linked quarter to 0.60%. Past due loans improved to 21 basis points as of March 31, down from 22 basis points at December 31.

As shown in the following chart of nonperforming loans evolution, the impact of these two relationships is clearly visible in the Q1 2025 results:

Balance Sheet Management

Simmons First National reported total period-end loans of $17.1 billion, up 2% on a linked quarter annualized basis. The commercial loan pipeline increased 43% linked quarter and reached its highest level since Q2 2022, suggesting potential for continued loan growth in coming quarters.

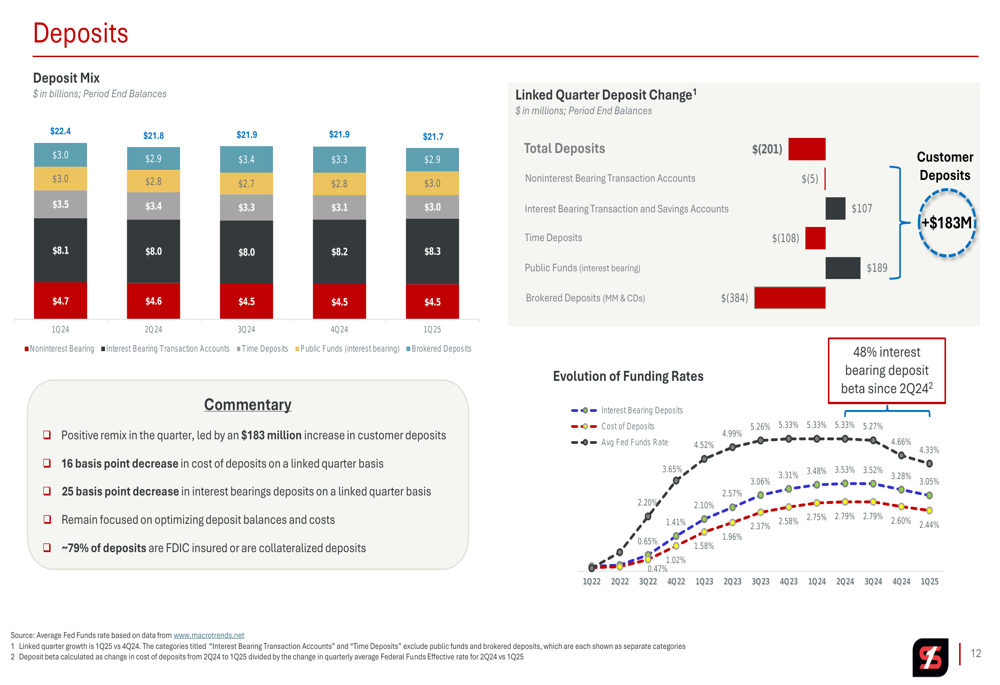

On the funding side, total deposits were $21.7 billion, down slightly from the previous quarter due to reductions in brokered funding. However, customer deposits grew by $183 million during the quarter, representing approximately 4% linked quarter annualized growth.

The following slide illustrates the deposit mix and evolution of funding rates:

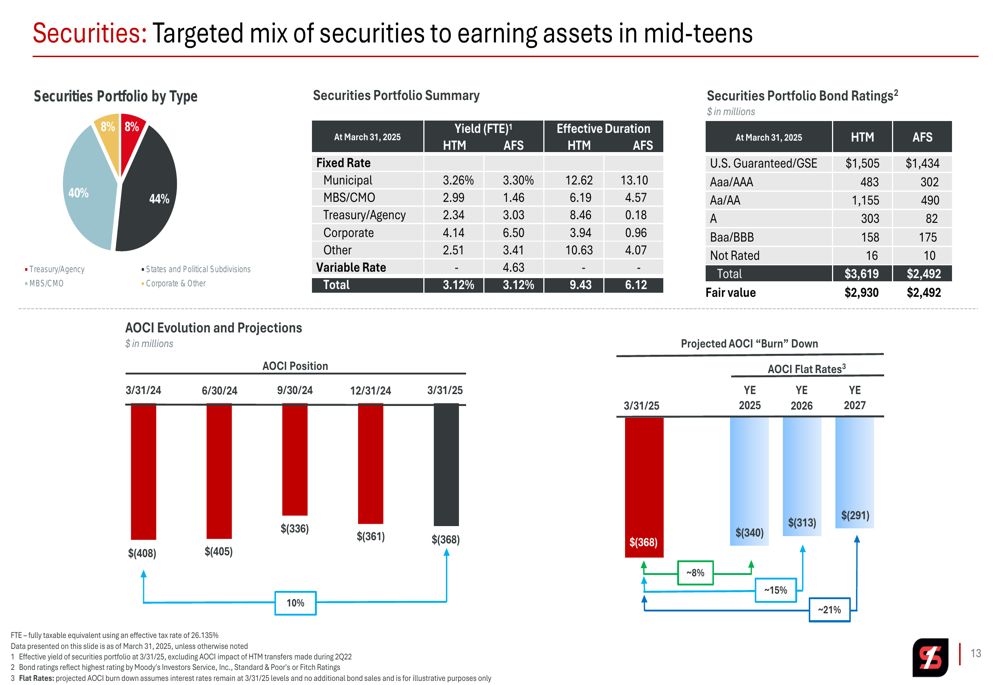

The company continues to optimize its securities portfolio, with a targeted mix of securities to earning assets in the mid-teens. The securities portfolio is being gradually reduced as part of the overall balance sheet strategy:

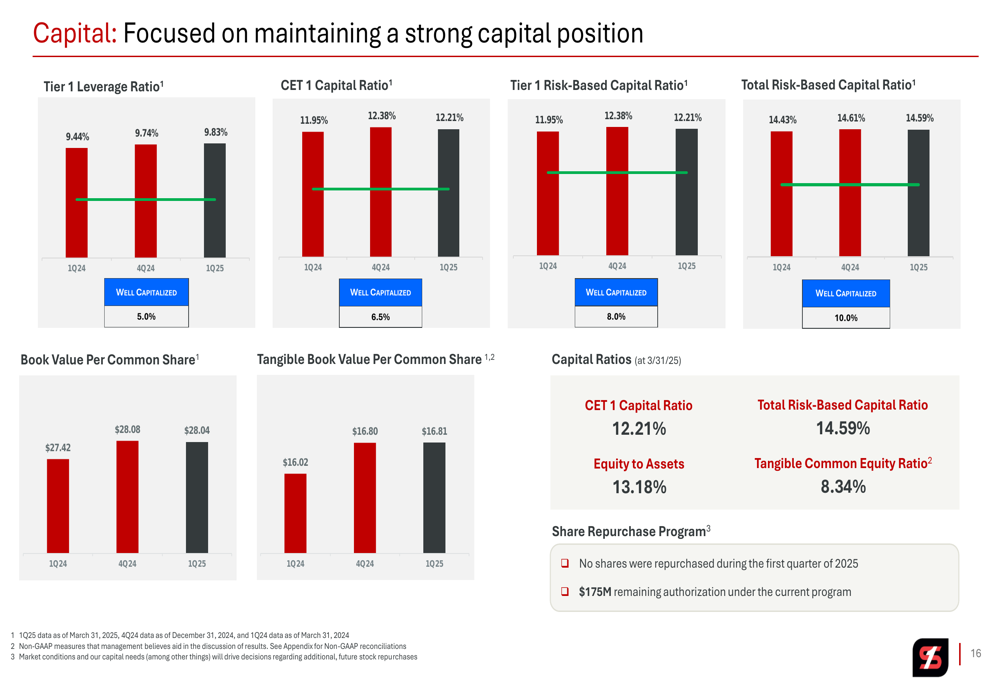

From a capital perspective, Simmons First National maintains strong ratios with a CET1 Capital Ratio of 12.21% and Total Risk-Based Capital Ratio of 14.59% as of March 31, 2025:

Forward Outlook

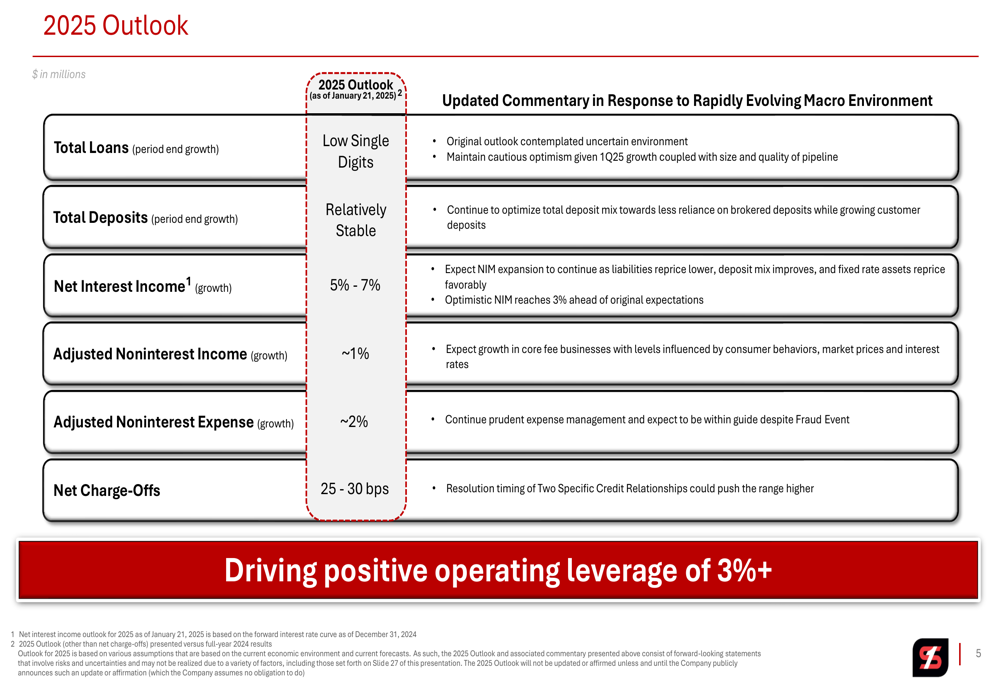

Despite the credit challenges in Q1, management reiterated its 2025 outlook, which includes:

- Low single-digit growth for total loans

- Relatively stable total deposits

- 5%-7% growth for net interest income

- Approximately 1% growth in adjusted noninterest income

- Approximately 2% growth in adjusted noninterest expense

- Net charge-offs of 25-30 basis points

The company remains focused on achieving positive operating leverage of 3% or more for the full year and expects net interest margin to potentially cross 3% sooner than originally anticipated.

As shown in the following outlook slide, management maintains a cautiously optimistic stance while acknowledging the evolving macroeconomic environment:

During the earnings call, Jay Brogdon expressed confidence in the company’s positioning: "Our original 2025 outlook that calls for 3% plus positive operating leverage and implies mid-teens year-over-year growth in PPNR remains intact." He also noted, "We feel very good about our asset quality outlook for the remainder of the year. We’re confident in our level of reserves based on today’s circumstances."

Chairman and CEO George Macris concluded the call with a measured perspective: "For the time being, we’re well positioned to wait for greater clarity," echoing Federal Reserve Chair Jerome Powell’s recent comments on the economic outlook.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.