Gold prices tick higher on fresh U.S. tariff threats, Fed rate cut hopes

Introduction & Market Context

Simpson Manufacturing Co., Inc. (NYSE:SSD), a leading provider of structural connectors, fasteners, and building solutions, recently presented its February 2025 investor slides showcasing the company’s 30-year growth journey and strategic positioning. The presentation comes after Simpson reported strong Q1 2025 results, with earnings per share of $1.85 exceeding forecasts of $1.65 and revenue reaching $538.9 million, slightly above expectations.

Currently trading at $159.37, Simpson’s stock has shown resilience in a challenging construction market, with a 52-week range of $137.35 to $197.82. The company continues to navigate a complex housing market environment while maintaining industry-leading margins and executing on strategic growth initiatives.

30-Year Growth Story

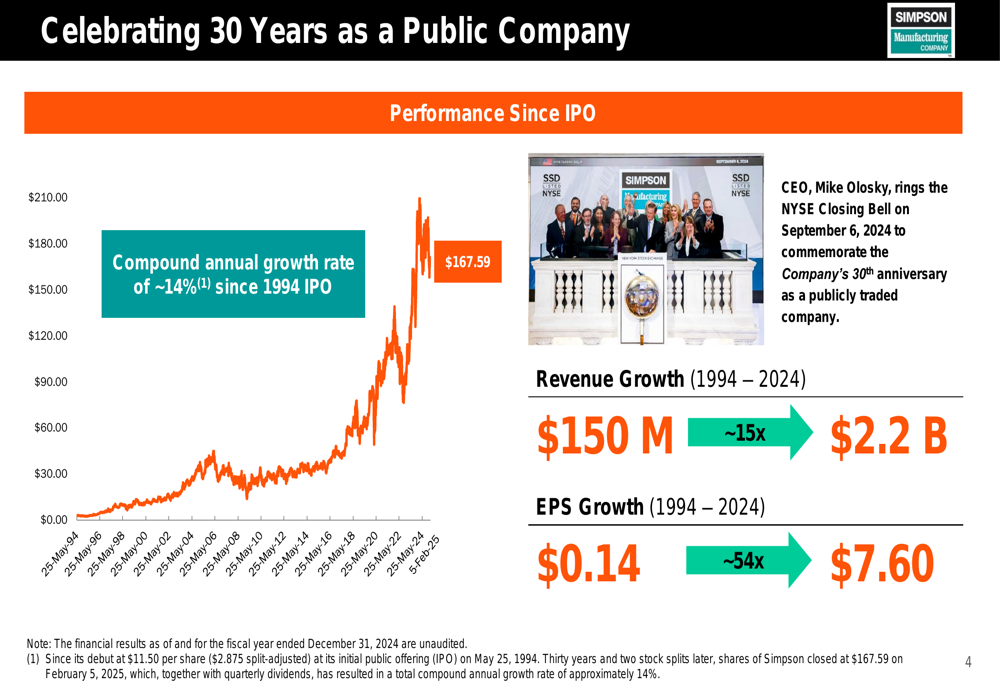

A significant highlight of the presentation was Simpson’s celebration of 30 years as a public company. Since its IPO in 1994, Simpson has achieved remarkable growth, with revenue expanding from $150 million to $2.2 billion (approximately 15x) and earnings per share growing from $0.14 to $7.60 (approximately 54x). This represents a compound annual growth rate of approximately 14% over three decades.

As shown in the following chart of Simpson’s long-term performance:

The company’s consistent growth trajectory has been supported by its innovation leadership, with a timeline of product developments spanning decades. Simpson maintains approximately 300 engineers, 8 accredited test labs, 120 code reports, and 500 patents worldwide, underscoring its commitment to technical leadership in the construction solutions space.

Market Positioning & Competitive Advantages

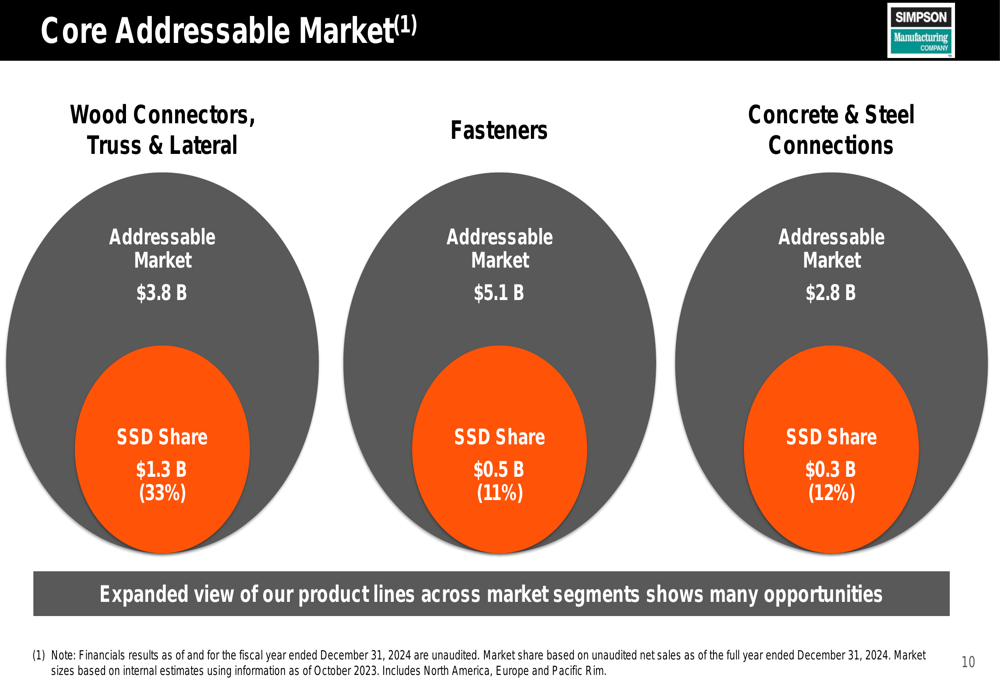

Simpson’s presentation emphasized its strong position in core addressable markets. The company holds a 33% share in the $3.8 billion wood connectors market, 11% of the $5.1 billion fasteners market, and 12% of the $2.8 billion concrete and steel connections market. This diversification provides multiple growth avenues while reducing dependence on any single market segment.

The company’s market share across key product categories is illustrated in this breakdown:

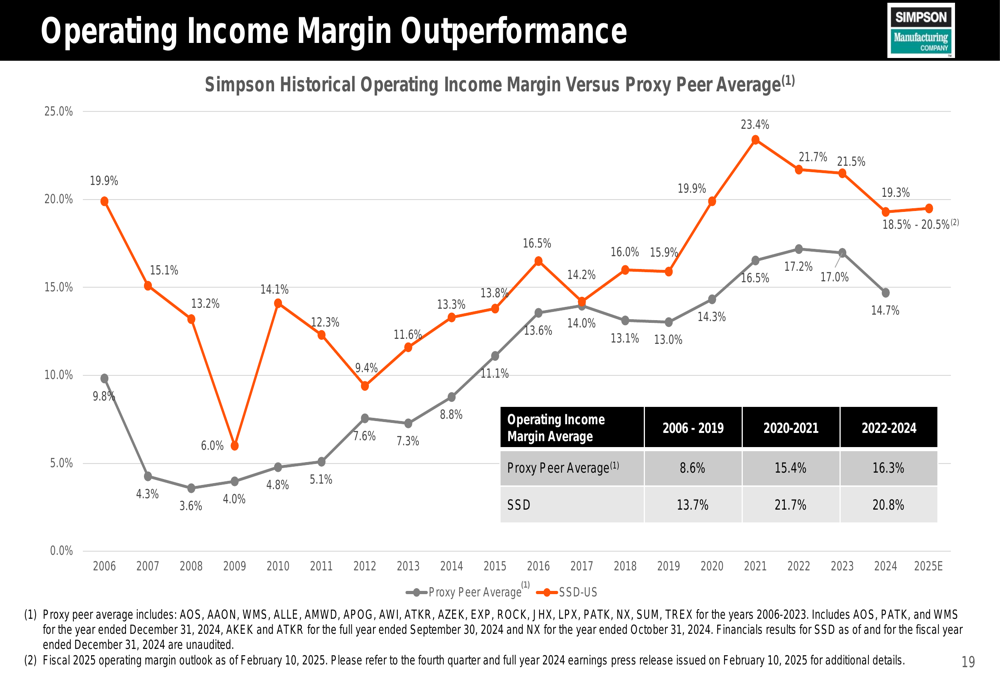

A key competitive advantage highlighted in the presentation is Simpson’s consistent operating income margin outperformance compared to industry peers. From 2022-2024, Simpson maintained an operating income margin of 20.8%, significantly above the proxy peer average of 16.3%.

This margin advantage is clearly demonstrated in the following comparative chart:

Financial Performance Highlights

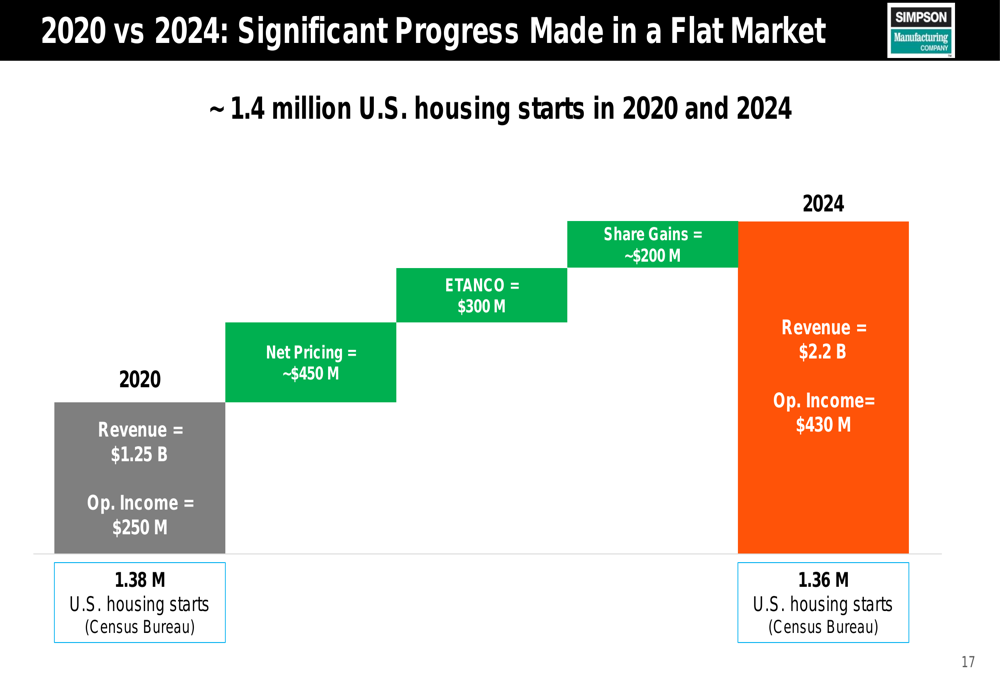

Simpson’s financial performance has remained strong despite market challenges. The presentation highlighted significant progress from 2020 to 2024, with revenue growing from $1.25 billion to $2.2 billion and operating income increasing from $250 million to $430 million. This growth is particularly impressive considering that US housing starts remained flat at approximately 1.4 million during this period.

The company’s growth drivers are broken down in this comparative analysis:

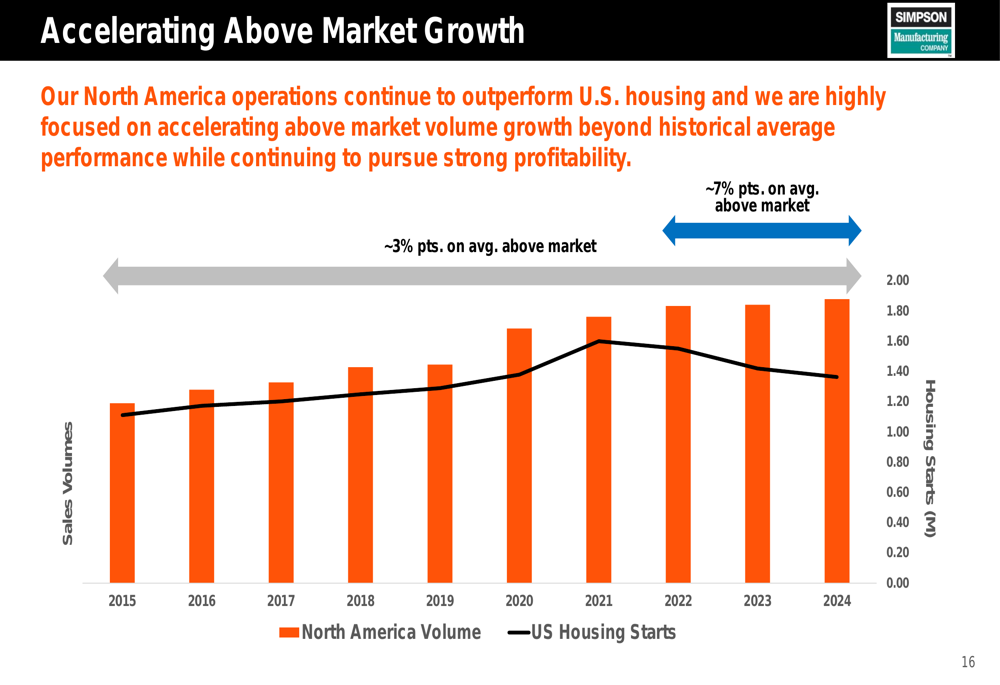

The presentation also showcased Simpson’s consistent above-market growth relative to US housing starts, averaging approximately 3 percentage points above market. This outperformance has accelerated in recent periods to approximately 7 percentage points above market, demonstrating the company’s ability to gain market share.

As illustrated in this comparative growth chart:

In its recent Q1 2025 earnings report, Simpson continued this trend of outperformance with EPS of $1.85 exceeding forecasts by 12.1%. While North American sales rose by 3.4%, European sales declined by 5.1%, highlighting some regional challenges that were acknowledged in the earnings call.

Strategic Growth Initiatives

Simpson outlined several strategic initiatives to drive future growth. The company is expanding its North American manufacturing operations with two major projects: an expansion of its Columbus (WA:CLC), OH facility expected to be completed in H1 2025, and a new greenfield facility in Gallatin, TN expected in H2 2025. These investments aim to increase capacity, improve safety and service, and vertically integrate fastener production.

The company is also focusing on digital solutions to drive growth by making it easier for customers to specify and order products. This includes developing a best-in-class online portal, using technology to strengthen partnerships with key customer groups, and providing software solutions that drive product specification.

Simpson’s European strategy centers on building strong brands in core businesses, with plans to maintain leadership in wood connectors, double structural fasteners, build on its strong position in facades, and offer complete product solutions. The company acknowledges challenges in the European market, which were reflected in the 5.1% sales decline noted in the Q1 2025 earnings report.

Capital Allocation & Shareholder Returns

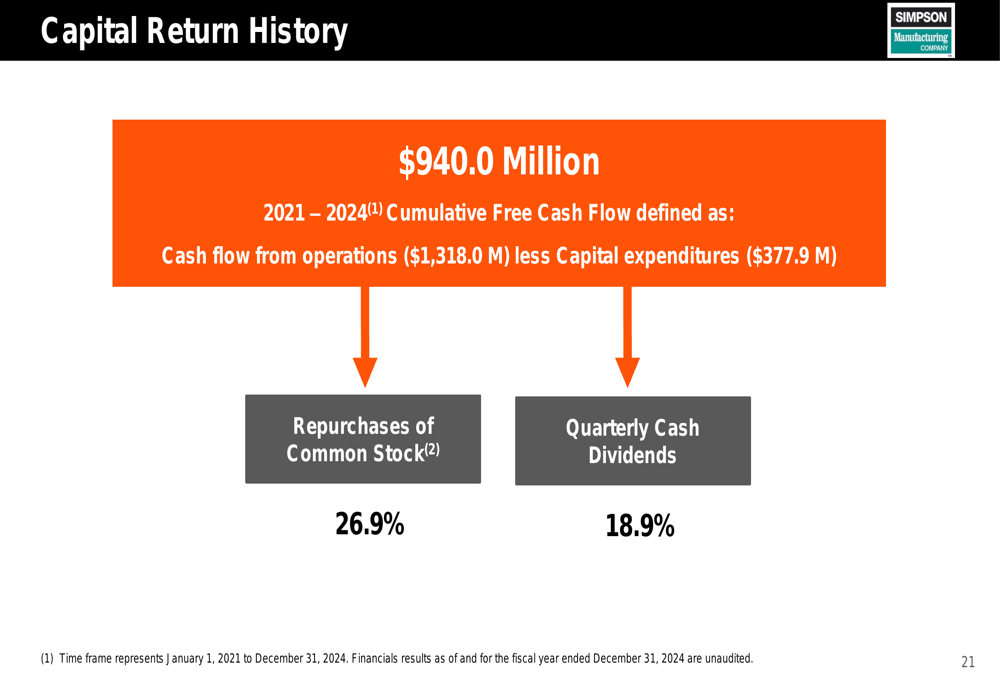

Simpson’s presentation highlighted its disciplined approach to capital allocation, with approximately 46% of free cash flow returned to stockholders since 2021. This exceeds the company’s 35% target and demonstrates its commitment to shareholder returns.

The company’s capital return history from 2021-2024 is broken down as follows:

Looking forward, Simpson outlined its priorities for cash use, including organic growth through facility expansions, strategic acquisitions, maintaining and raising quarterly cash dividends, debt repayment, and selective share repurchases. The company recently declared a quarterly dividend of $0.28 per share, payable on April 24, 2025.

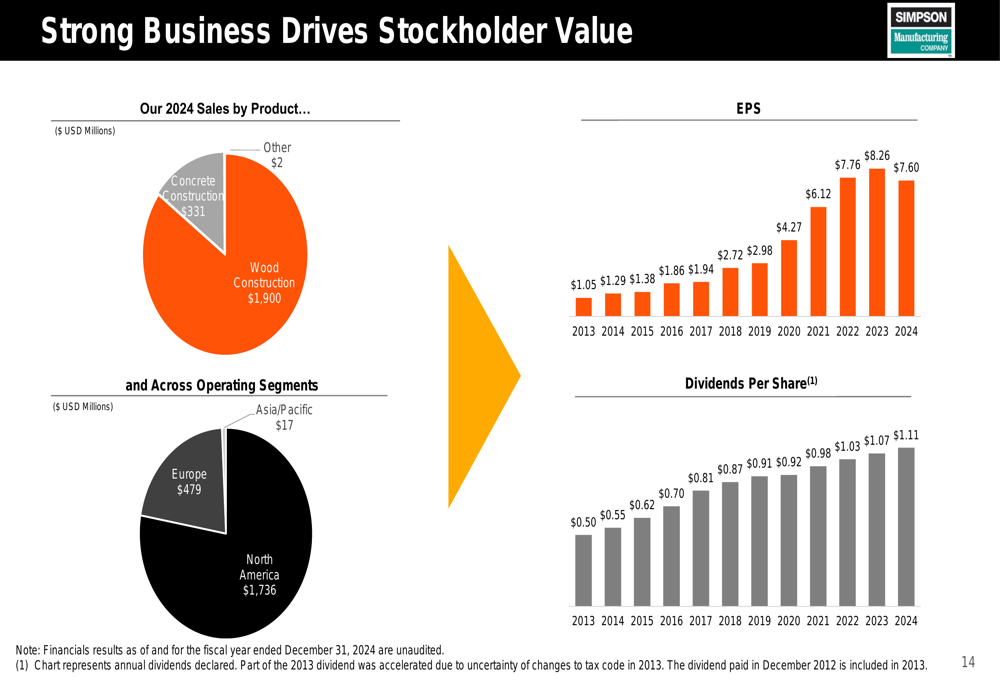

The company’s strong business performance has translated into consistent dividend growth, with dividends per share increasing from $0.50 in 2013 to $1.11 in 2024, as shown in this comprehensive financial overview:

Forward-Looking Statements

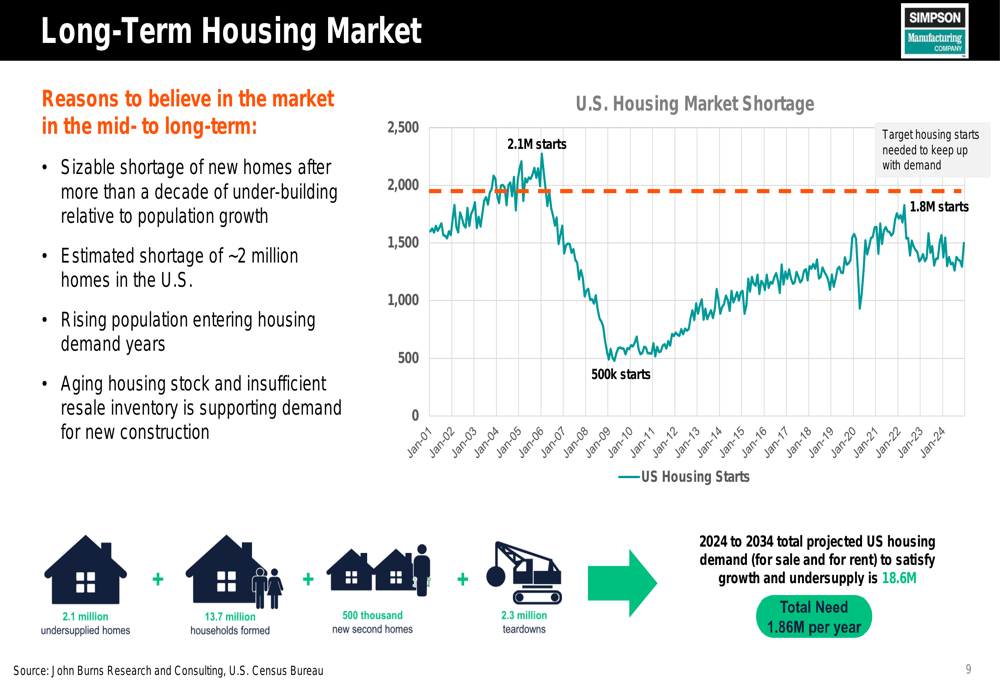

Simpson’s presentation provided an optimistic long-term housing market outlook, highlighting an estimated shortage of approximately 2 million homes in the US after more than a decade of under-building relative to population growth. The company projects total US housing demand of 18.6 million from 2024 to 2034, or approximately 1.86 million per year, supporting sustained demand for its products.

The long-term housing market opportunity is illustrated in this market analysis:

During the Q1 2025 earnings call, management maintained a positive outlook while acknowledging near-term challenges. CFO Matt Dunn emphasized, "We continue to believe Simpson is poised to execute our strategic plan for the balance of 2025 through ongoing macroeconomic uncertainty." The company forecasts EPS of $2.36 for Q2 2025 and $2.57 for Q3 2025, with analyst price targets ranging from $182 to $190, suggesting potential upside from current levels.

Simpson’s company ambitions include strengthening its values-based culture, being the business partner of choice, striving for innovation leadership, continuing above-market growth relative to US housing starts, maintaining operating income margins above 20%, and delivering EPS growth ahead of net revenue growth.

As the company enters its fourth decade as a public entity, Simpson Manufacturing remains well-positioned to capitalize on long-term construction market opportunities while navigating near-term challenges through its diversified product portfolio, strong balance sheet, and commitment to innovation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.