Texas Roadhouse earnings missed by $0.05, revenue topped estimates

Introduction & Market Context

Skagi hf. (ICEX:SKAGI) presented its Q1 2025 financial results on April 29, showing strong revenue growth in its core business units that was overshadowed by significant investment losses. The Icelandic financial group, currently trading at 19.3 ISK per share (up 1.55% recently), reported that weak equity markets both domestically and internationally heavily impacted its overall performance.

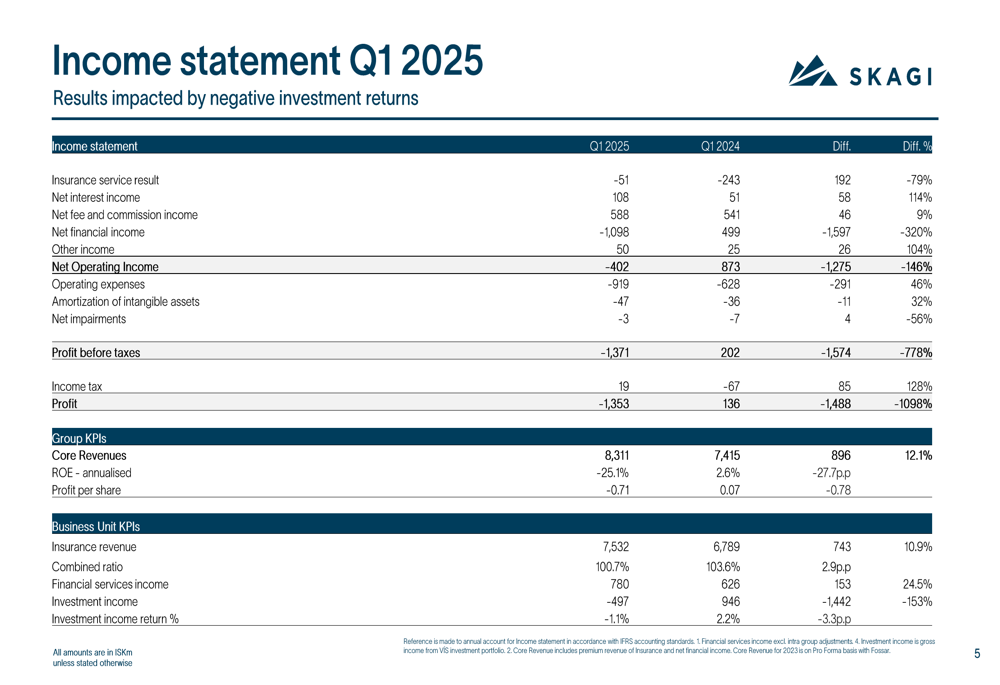

The company, which recently completed a period of corporate restructuring including mergers and subsidiary transfers, saw its core revenue grow by 12.1% year-over-year to 8,311 million ISK. However, this positive development was offset by negative investment returns, resulting in a quarterly loss of 1,353 million ISK compared to a profit of 136 million ISK in Q1 2024.

Quarterly Performance Highlights

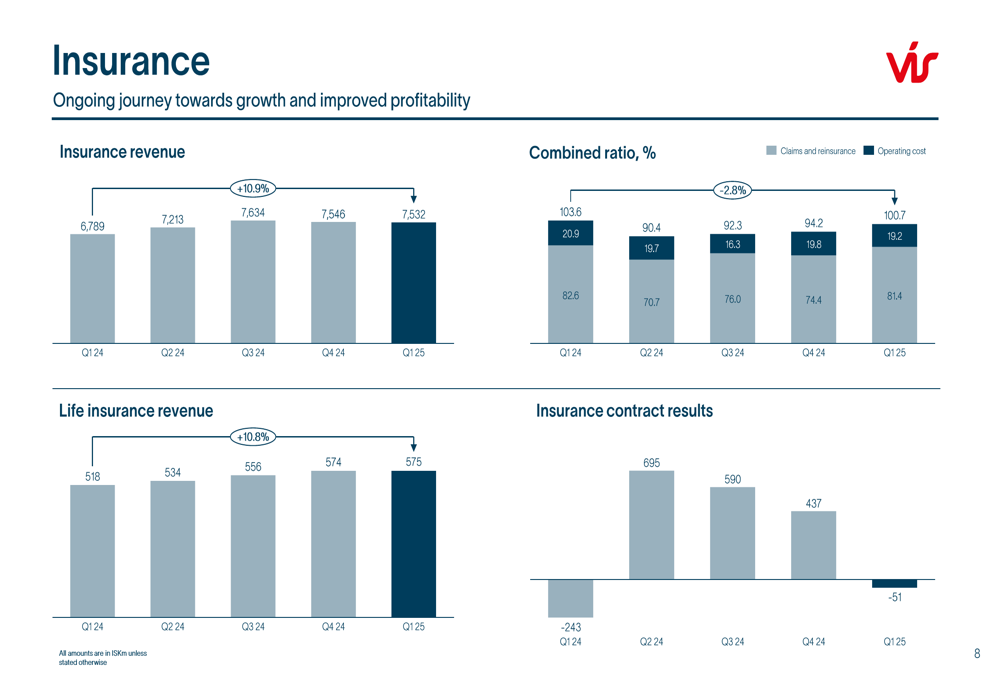

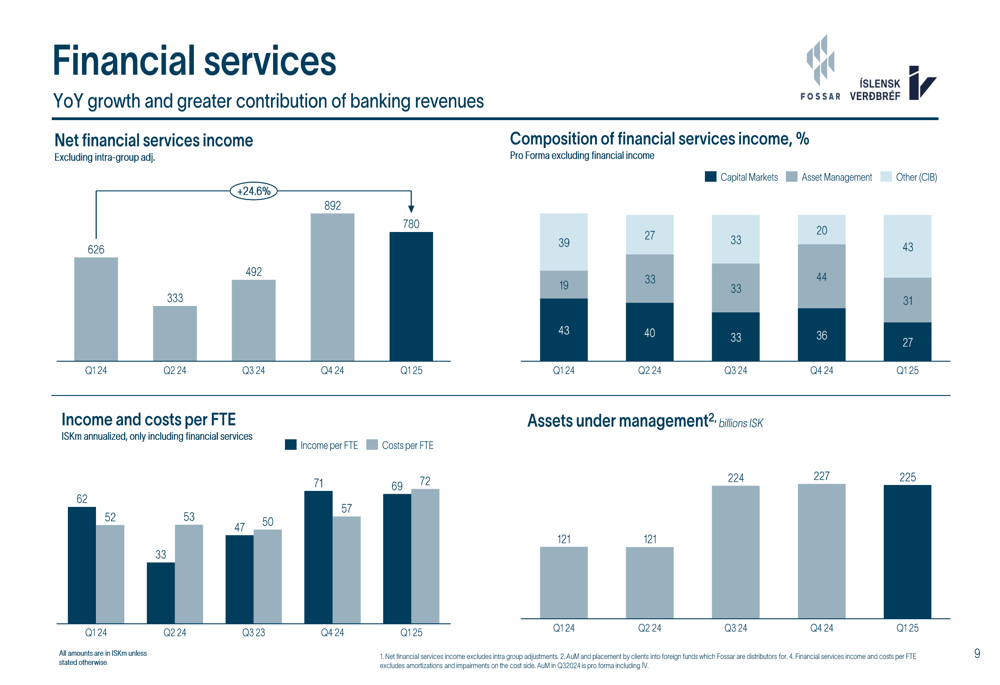

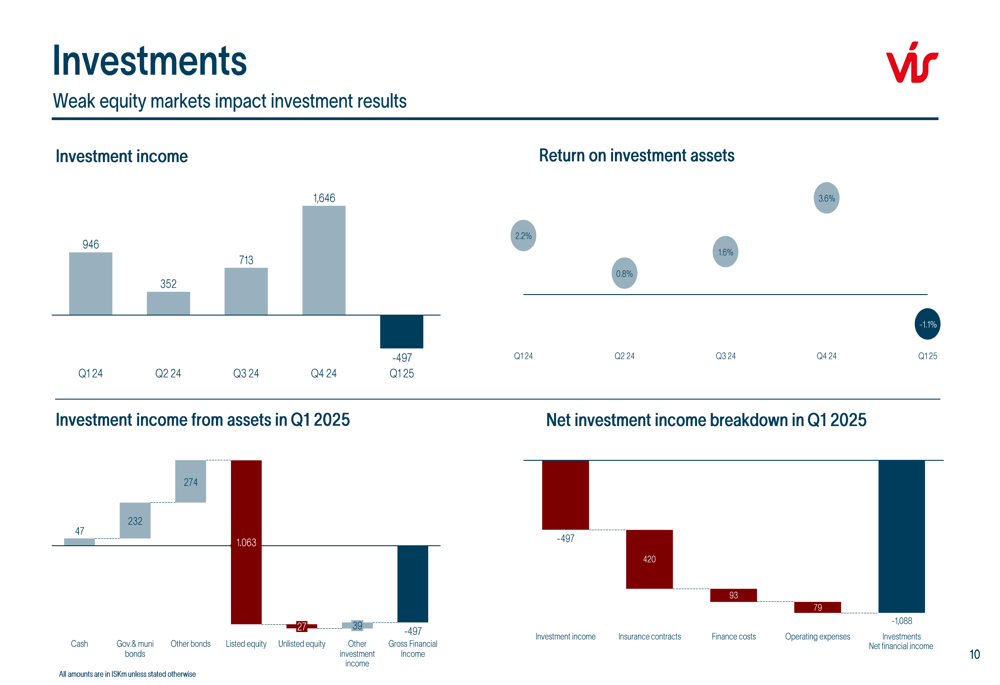

Skagi’s performance varied significantly across its three main business units. The Insurance segment continued its growth trajectory with a 10.9% year-over-year revenue increase to 7,532 million ISK, while the Financial Services unit saw revenues climb 24.5% to 780 million ISK. However, the Investment unit posted a negative return of -1.1%, though this still outperformed its benchmark of -1.6%.

As shown in the following key financial results summary:

The company’s combined ratio in insurance improved to 100.7% from 103.6% in Q1 2024, with the cost ratio declining to 19.2% from 20.9%. Despite these operational improvements, the group reported an annualized ROE of -25.1% and earnings per share of -0.71 ISK for the quarter.

Detailed Financial Analysis

Skagi’s income statement reveals the stark contrast between operational performance and investment results. While insurance service results improved by 79% year-over-year and net interest income grew by 114%, net financial income plummeted to -1,098 million ISK from 499 million ISK in Q1 2024, representing a 320% decline.

The detailed income statement highlights these contrasts:

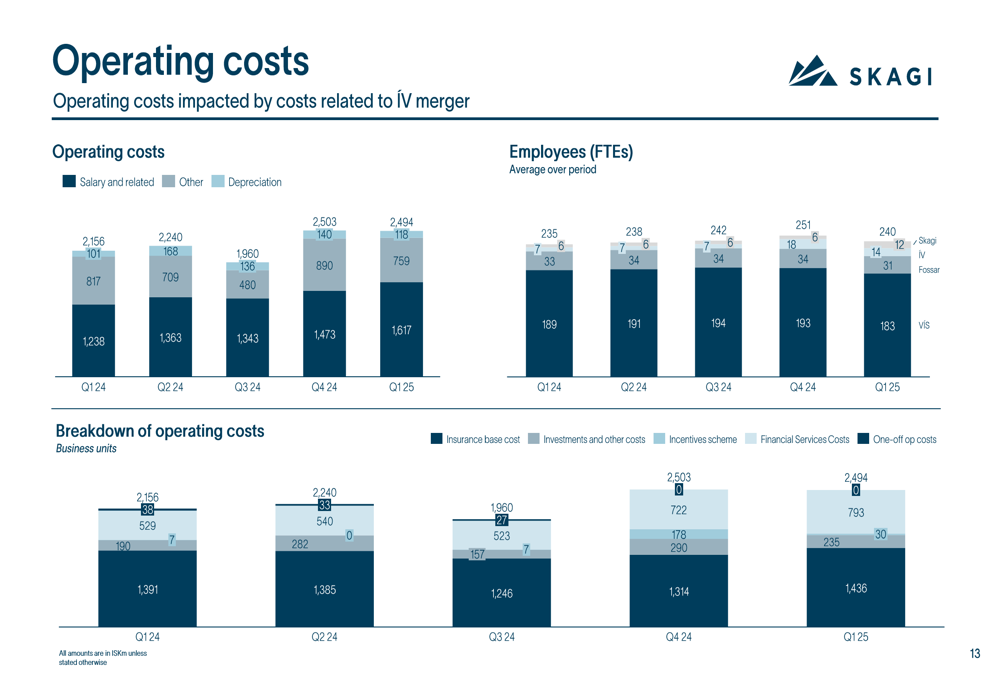

Operating expenses increased by 46% year-over-year to 919 million ISK, partly due to one-off expenses related to the IV merger with Fossar. The company’s balance sheet grew by 4% compared to December 2024, with total assets reaching 82,493 million ISK. Insurance liabilities increased by 7%, while equity declined by 6% to 20,927 million ISK.

The insurance business unit showed consistent improvement in its metrics over recent quarters, with insurance contract results improving from -243 million ISK in Q1 2024 to -51 million ISK in Q1 2025:

Meanwhile, the Financial Services unit demonstrated strong growth in both revenue and assets under management, which reached 225 billion ISK in Q1 2025 compared to 121 billion ISK in Q1 2024:

The investment portfolio, which heavily impacted overall results, shifted more toward bonds prior to the quarter’s end. The negative performance was primarily driven by weak equity markets:

Strategic Initiatives

Skagi reported that it has completed its implementation period, which included the merger of IV with Fossar and SIV, as well as the transfer of VÍS insurance to a subsidiary. The company stated that its corporate structure is now in place, and it is looking ahead at a period of growth, implementing multiple groupwide growth and synergy initiatives.

The company is also preparing for an Íslandsbanki partnership, which it describes as "well underway." Additionally, Fossar has introduced a refreshed brand with an increased focus on retail investors.

Operating costs have increased as the company has grown, with a breakdown showing various components:

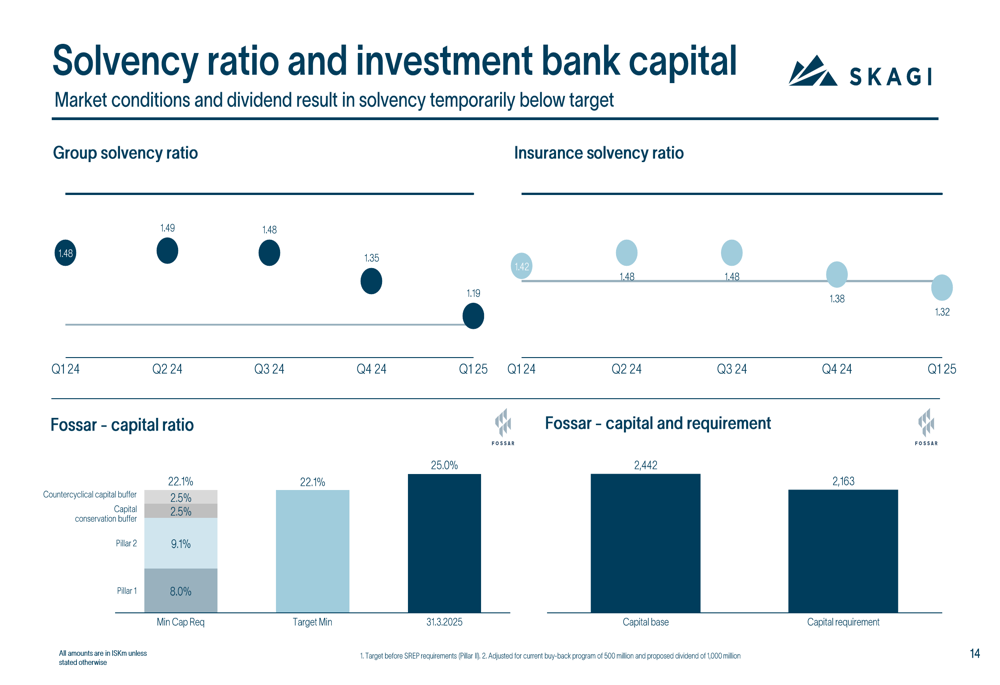

Despite the challenging quarter, Skagi maintains solid solvency positions, though ratios have declined compared to the previous year:

Forward-Looking Statements

Skagi outlined changes to its financial reporting approach, emphasizing more timely publication of financial information with more concise interim statements. The company provided a calendar of upcoming financial releases, including Q2 results on July 17, 2025, Q3 results on October 28, 2025, and full-year 2025 results on February 17, 2026.

In its key takeaways, Skagi characterized the quarter as showing insurance and financial services on track but with market volatility impacting overall results:

The company maintains its focus on ongoing positive momentum in insurance revenue, improved combined ratio performance, and continued growth in financial services, while acknowledging the significant impact of weak equity market performance during the quarter.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.