Oil prices hold sharp losses with focus on secondary India tariffs

SmartRent Inc. (NYSE:SMRT) presented its Q1 FY 2025 earnings results on May 7, 2025, highlighting a strategic shift toward recurring software revenue despite an overall decline in total revenue. The company’s stock, which closed at $0.88 on May 8, had risen 6.27% in pre-market trading following the earnings announcement, suggesting investor confidence in the company’s long-term strategy despite missing earnings expectations.

Executive Summary

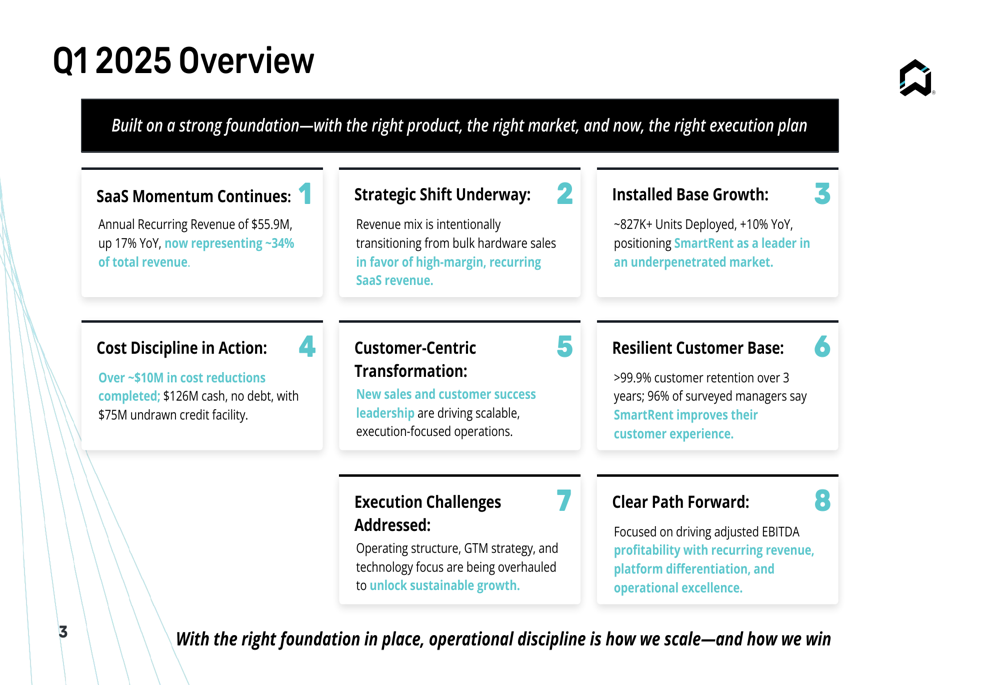

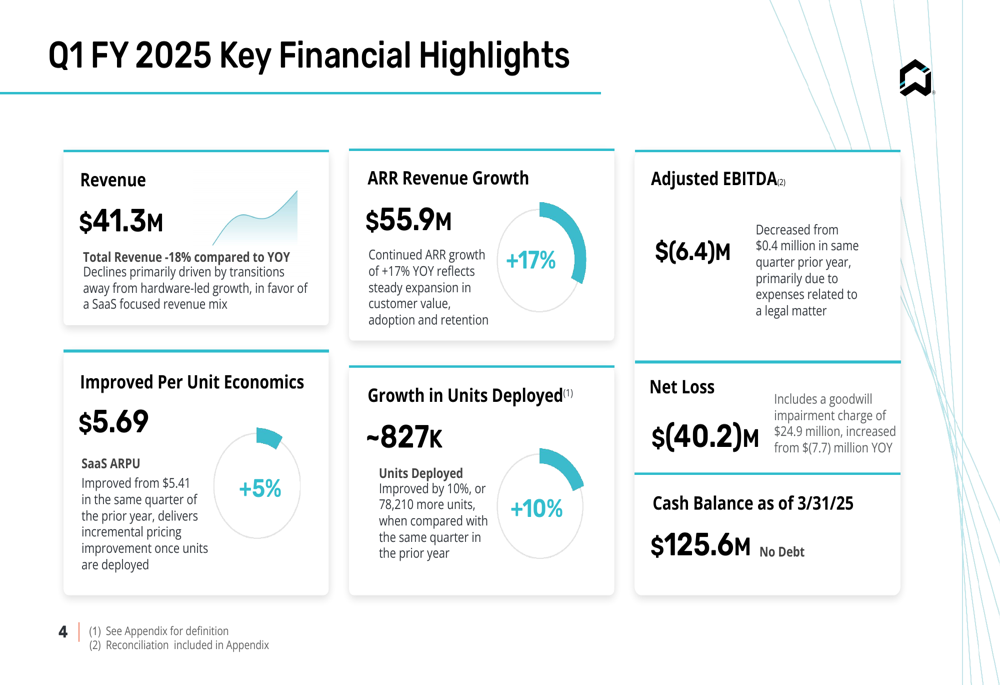

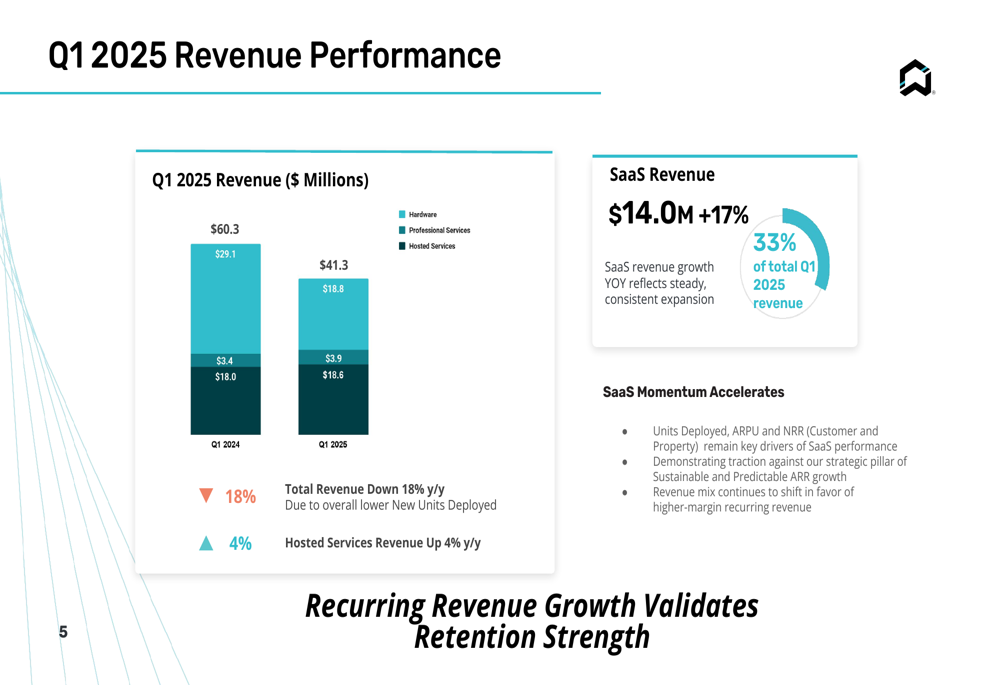

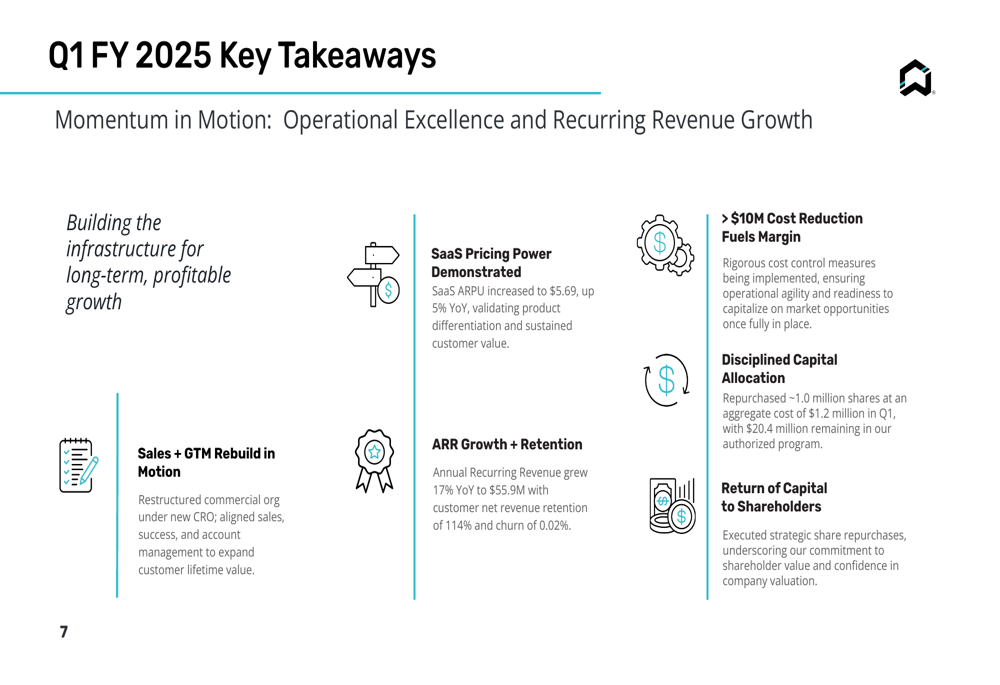

SmartRent reported total revenue of $41.3 million for Q1 2025, representing an 18% year-over-year decrease as the company transitions away from hardware-led growth. Despite this overall decline, the company’s Annual Recurring Revenue (ARR) grew 17% year-over-year to $55.9 million, now representing approximately 34% of total revenue. This shift underscores SmartRent’s strategic pivot toward higher-margin, recurring SaaS revenue.

The company reported a net loss of $40.2 million, which included a $24.9 million goodwill impairment charge. Adjusted EBITDA was negative $6.4 million, down from positive $0.4 million in the same quarter last year, partly due to legal matter expenses. Despite these challenges, SmartRent maintained a strong cash position of $125.6 million with no debt, and an additional $75 million undrawn credit facility.

Quarterly Performance Highlights

SmartRent’s Q1 2025 results reflect its ongoing transition from hardware to software solutions. While total revenue declined, SaaS revenue grew to $14.0 million, a 17% increase year-over-year, now accounting for 33% of total revenue. This growth in recurring revenue is a key element of the company’s strategy to improve long-term profitability.

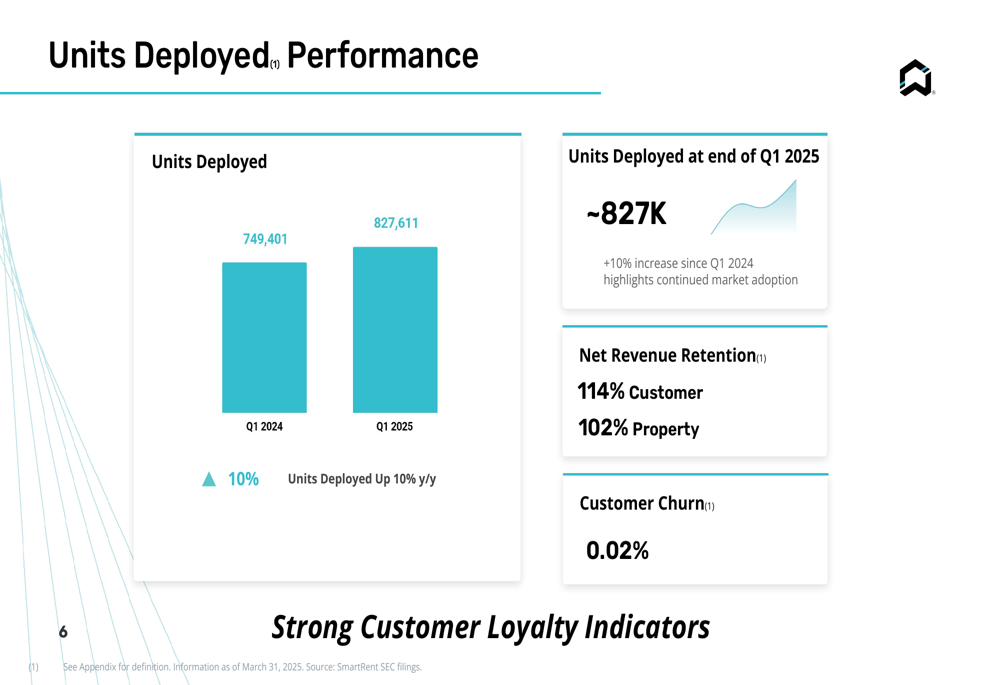

The company’s installed base continued to expand, with units deployed reaching approximately 827,000, a 10% increase from the same period last year. SaaS ARPU (Average Revenue Per Unit) improved to $5.69, up 5% from $5.41 in Q1 2024, demonstrating pricing power and improved unit economics once units are deployed.

As shown in the following revenue breakdown, the company’s revenue mix is shifting toward higher-margin SaaS revenue:

Customer metrics remained strong, with net revenue retention of 114% for customers and 102% for properties, indicating that existing customers are expanding their use of SmartRent’s solutions. The company also reported an impressively low customer churn rate of just 0.02%, suggesting high customer satisfaction and product stickiness.

The following chart illustrates SmartRent’s consistent growth in units deployed over the past year:

Strategic Initiatives

SmartRent’s presentation emphasized several strategic initiatives aimed at improving profitability and driving sustainable growth. The company has completed over $10 million in cost reductions as part of its disciplined approach to expense management. These cost-cutting measures are expected to fuel margin improvements in coming quarters.

The company is also undergoing a customer-centric transformation, with new sales and customer success leadership driving execution-focused operations. This includes a restructured commercial organization and alignment of sales, success, and account management functions to better serve clients and drive growth.

As part of its capital allocation strategy, SmartRent repurchased approximately 1.0 million shares at a cost of $1.2 million during the quarter, leaving $20.4 million in authorized buybacks. This share repurchase program underscores management’s confidence in the company’s long-term value and commitment to returning capital to shareholders.

Forward-Looking Statements

Looking ahead, SmartRent is focused on building infrastructure for long-term, profitable growth. The company aims to achieve adjusted EBITDA profitability through a combination of recurring revenue growth, platform differentiation, and operational excellence.

The company’s strategy centers on leveraging its strong customer retention and growing SaaS revenue base to drive sustainable growth. With a customer retention rate exceeding 99.9% over three years and 96% of surveyed property managers reporting that SmartRent improves their customer experience, the company has a solid foundation for future expansion.

However, challenges remain. The earnings article noted that SmartRent missed EPS expectations by a significant margin, reporting -$0.21 against a forecast of -$0.03. Additionally, the company faces potential tariff exposure of approximately $2 million in the second half of 2025, and is currently conducting a CEO search, which could impact strategic continuity.

Detailed Financial Analysis

SmartRent’s financial position remains solid despite operational challenges. The company’s $125.6 million cash balance and debt-free status provide financial flexibility to navigate its strategic transition. The $75 million undrawn credit facility offers additional liquidity if needed.

The decline in gross margin from 38.5% to 32.8% year-over-year reflects ongoing cost pressures and the transitional nature of the company’s business model shift. As SaaS revenue continues to grow as a percentage of total revenue, gross margins should theoretically improve given the higher-margin nature of software versus hardware.

The company’s adjusted EBITDA decline from $0.4 million to negative $6.4 million year-over-year indicates that SmartRent is still working through its transition period. Management attributes part of this decline to legal matter expenses, but the significant EPS miss suggests broader operational challenges that the company is working to address through its cost reduction initiatives and strategic realignment.

SmartRent’s emphasis on SaaS metrics like ARR growth, customer retention, and SaaS ARPU improvements indicates confidence that the foundation for future profitability is being established, even as near-term financial results reflect the costs of this transition. The company’s clear focus on execution challenges and operational discipline suggests management is taking a pragmatic approach to addressing current shortfalls while positioning for future growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.