Sun Valley Gold sells Vista Gold (VGZ) shares worth $2.16 million

Introduction & Market Context

Snap-On Inc. (NYSE:SNA) released its third quarter 2025 financial results on October 16, showcasing solid performance across most business segments. The tool manufacturer and distributor reported earnings per share of $5.02, surpassing analyst expectations of $4.63 by 8.42%. Following the announcement, Snap-On’s stock rose 4.27% in regular trading, reaching $346.79, approaching its 52-week high of $373.90.

The company’s quarterly presentation highlighted its continued focus on productivity solutions and innovation as it celebrates its 105th anniversary. Against a backdrop of evolving automotive repair technologies, Snap-On has maintained its position as a leading provider of tools and diagnostic equipment for professional technicians.

Quarterly Performance Highlights

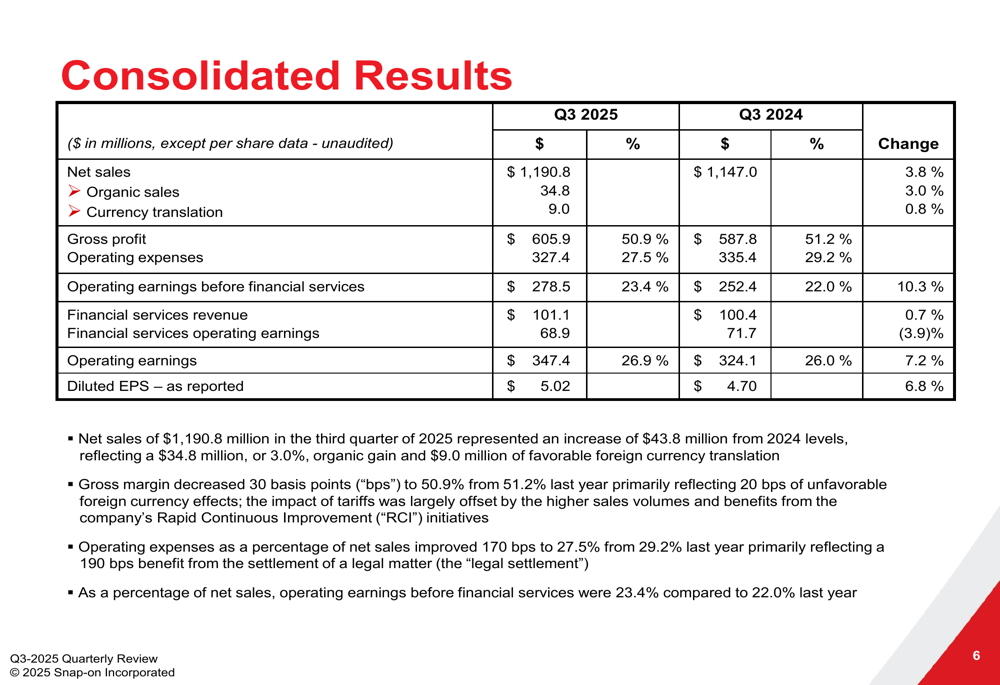

Snap-On reported consolidated net sales of $1,190.8 million in Q3 2025, representing a 3.8% increase from $1,147.0 million in the same period last year. Organic sales grew by 3.0%, with favorable currency translation contributing an additional 0.8%.

Operating earnings increased 7.2% to $347.4 million compared to $324.1 million in Q3 2024, while diluted earnings per share rose 6.8% to $5.02 from $4.70 in the prior year. The company maintained a strong gross profit margin of 50.9%, though slightly down from 51.2% in Q3 2024.

As shown in the following consolidated results chart:

"We believe our third quarter demonstrated encouraging momentum," said CEO Nick Pinchuk during the earnings call. He emphasized that "vehicle repairs never had a more promising future," highlighting the company’s strategic pivot toward faster payback items that has begun to yield positive results.

Segment Analysis

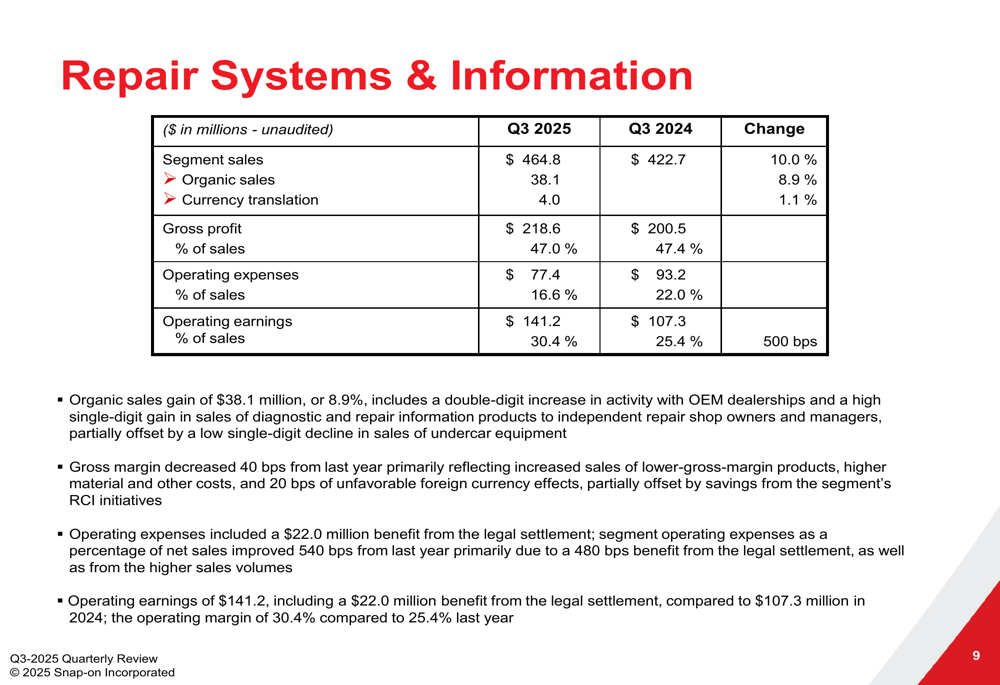

The Repair Systems & Information segment was the standout performer, with sales increasing 10.0% to $464.8 million, driven by higher activity with OEM dealerships and strong performance in diagnostic and repair information products. Operating earnings in this segment surged by 31.6% to $141.2 million, benefiting from a $22.0 million legal settlement. Even without this one-time benefit, the segment showed substantial organic growth.

The segment’s performance is illustrated in the following chart:

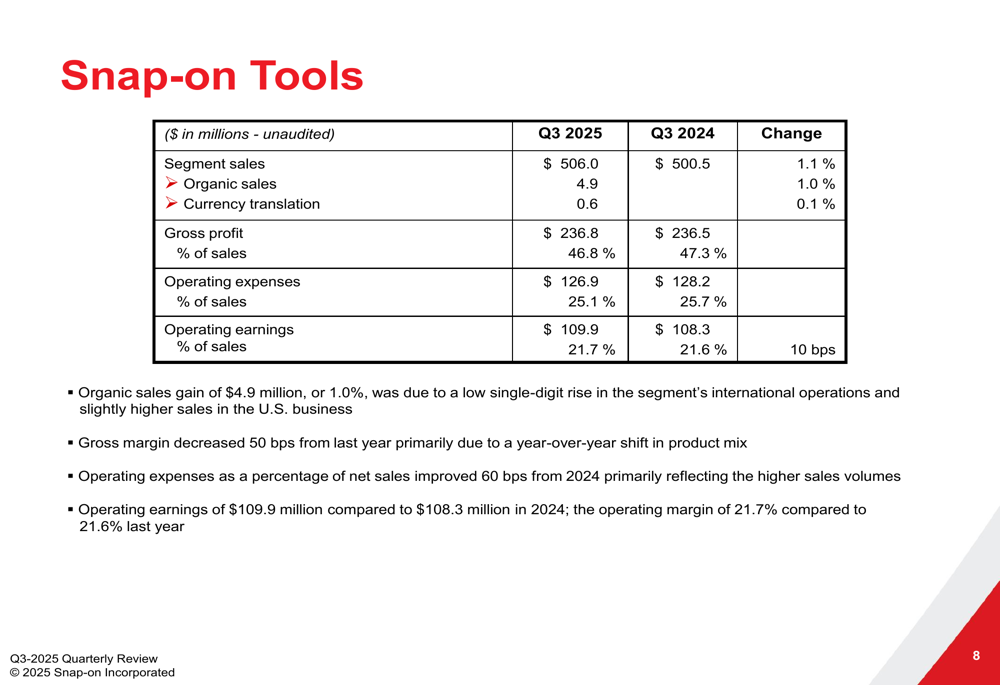

The Snap-on Tools segment, representing the company’s core business, posted a modest 1.1% sales increase to $506.0 million, with operating earnings rising slightly to $109.9 million. This growth was attributed to gains in both international operations and the U.S. business.

The detailed Snap-on Tools segment results are shown here:

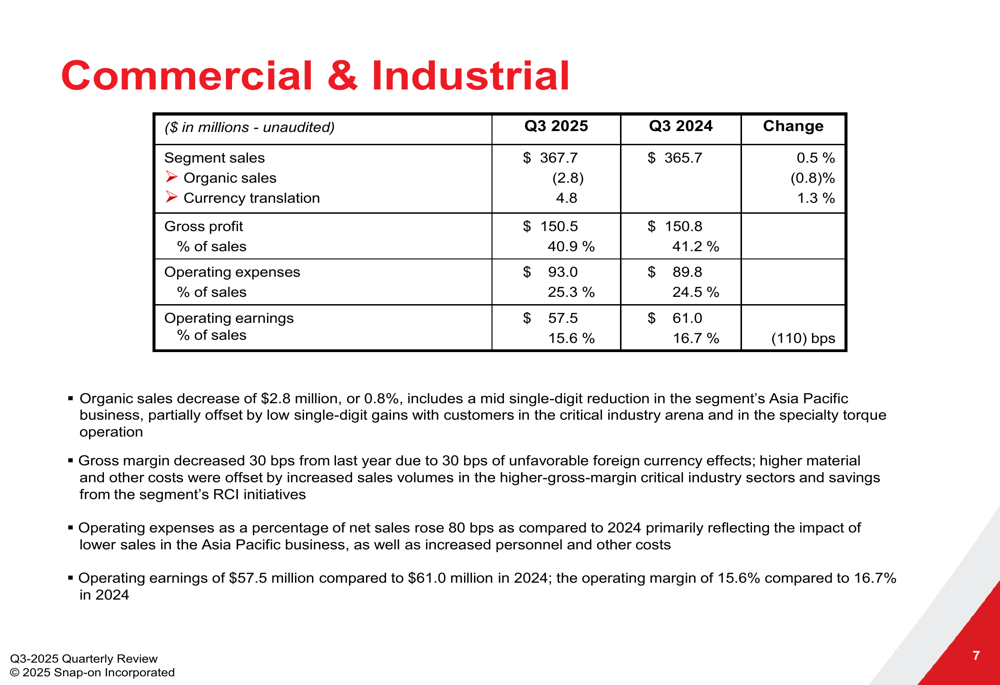

The Commercial & Industrial segment showed the most modest growth, with sales increasing just 0.5% to $367.7 million. Operating earnings declined to $57.5 million from $61.0 million in Q3 2024, with operating margin decreasing to 15.6% from 16.7%. This performance was impacted by lower sales in the Asia Pacific business.

The Commercial & Industrial segment results are presented below:

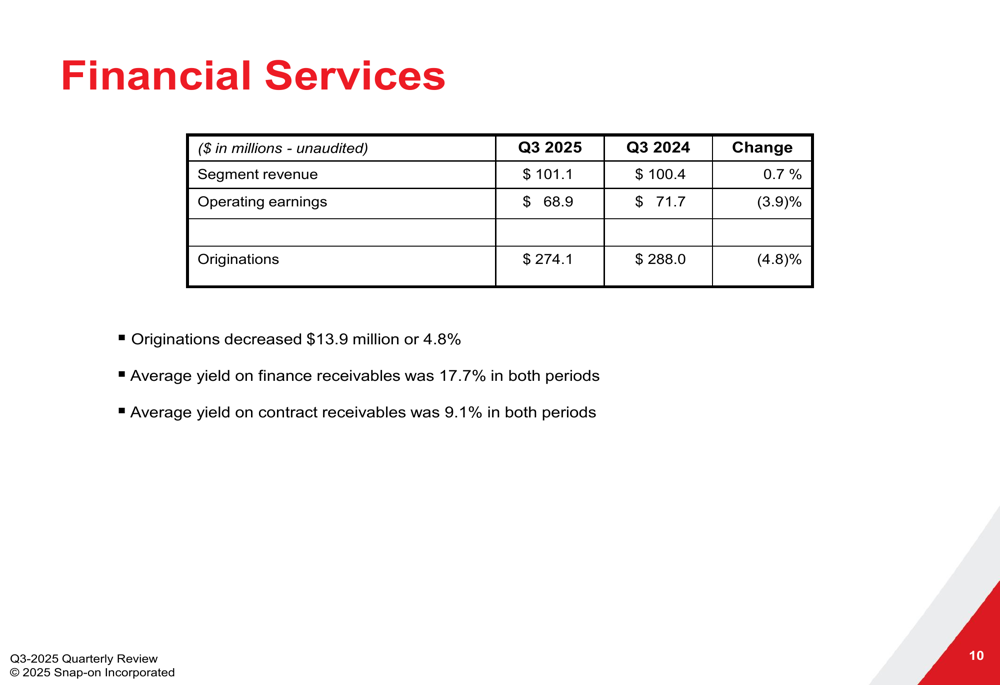

Financial Services revenue increased slightly by 0.7% to $101.1 million, though operating earnings decreased by 3.9% to $68.9 million. Originations declined by 4.8% to $274.1 million, indicating some challenges in this segment despite maintaining consistent yield rates.

Financial Position and Cash Flow

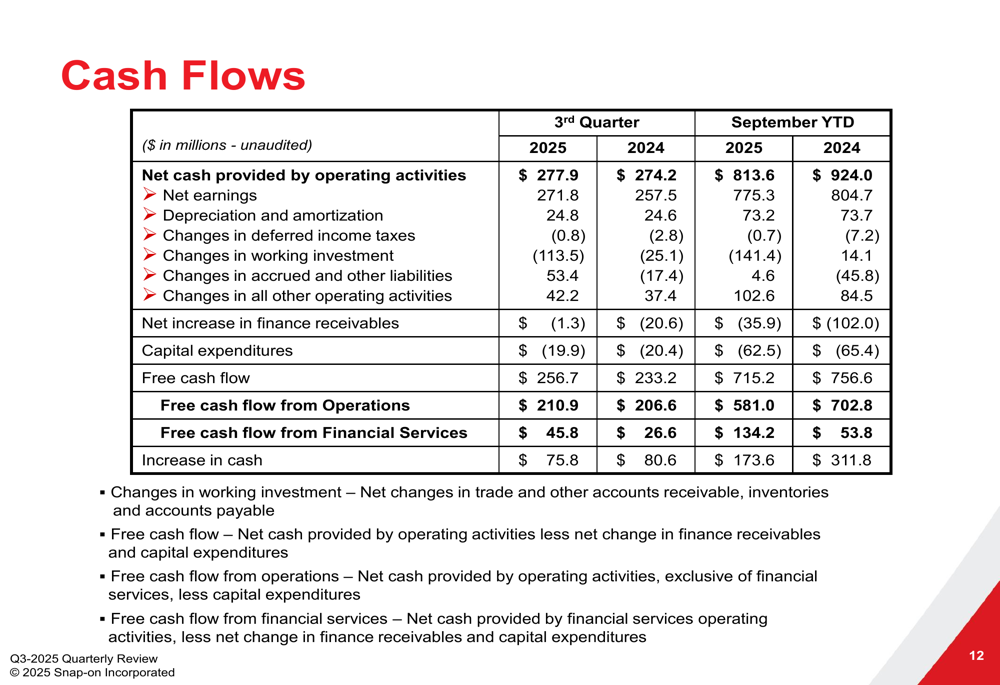

Snap-On continues to demonstrate strong cash generation capabilities, with Q3 2025 free cash flow of $256.7 million, up from $233.2 million in Q3 2024. Year-to-date free cash flow stands at $715.2 million, though slightly below the $756.6 million reported for the same period in 2024.

The company’s cash flow performance is detailed in the following chart:

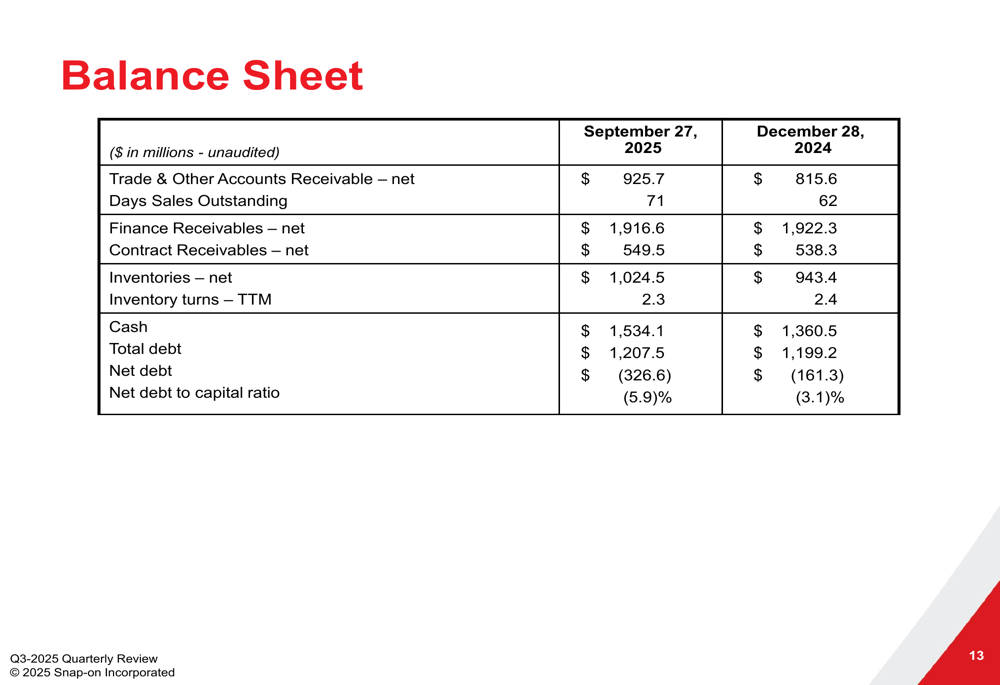

The balance sheet remains exceptionally strong, with cash of $1,534.1 million significantly exceeding total debt of $1,207.5 million, resulting in a negative net debt position of $(326.6) million. This translates to a net debt to capital ratio of (5.9)%, providing substantial financial flexibility for future investments, acquisitions, and shareholder returns.

The following balance sheet summary highlights Snap-On’s financial strength:

Inventory levels increased to $1,024.5 million from $943.4 million at the end of 2024, with inventory turns slightly decreasing to 2.3 from 2.4. Days Sales Outstanding increased to 71 days from 62 days, suggesting some lengthening in collection cycles that bears monitoring.

Forward Outlook

Looking ahead, Snap-On remains optimistic about its market opportunities. The company anticipates a full-year 2025 tax rate between 22-23% and plans capital expenditures of approximately $100 million. With 2025 being a 53-week fiscal year, the company is positioned to continue its growth trajectory.

Snap-On’s commitment to its core values and mission of being "the most valued productivity solutions in the world" continues to guide its strategic direction:

The company’s strong cash position and consistent performance support its 55-year history of dividend payments. Analysts have recently revised earnings estimates upward, reflecting confidence in Snap-On’s business model and execution capabilities.

While the company faces potential challenges including supply chain disruptions, market saturation in key segments, and macroeconomic pressures, its diversified business model and focus on essential professional tools position it well to navigate these headwinds. The continued growth in diagnostic and repair information products, particularly as vehicles become more technologically complex, provides a promising avenue for sustained growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.