S&P 500 slips, but losses kept in check as Nvidia climbs ahead of results

Introduction & Market Context

SoFi Technologies (NASDAQ:SOFI) shares jumped 6.47% in premarket trading to $22.38 following the release of its Q2 2025 investor presentation, which revealed accelerating growth across key metrics and raised full-year guidance. The fintech company, now valued at over $14 billion, continues its transformation from a lending-focused business to a diversified financial services platform with expanding profit margins.

The presentation highlighted SoFi’s seventh consecutive quarter of profitability, with record adjusted net revenue of $858 million representing a 44% year-over-year increase – the company’s highest growth rate in over two years. This acceleration follows the 33% year-over-year revenue growth reported in Q1 2025.

Quarterly Performance Highlights

SoFi reported record adjusted EBITDA of $249 million in Q2, representing a 29% margin, while GAAP net income reached $97 million (11% margin). The company achieved a record adjusted EPS of $0.08, continuing its profitability streak.

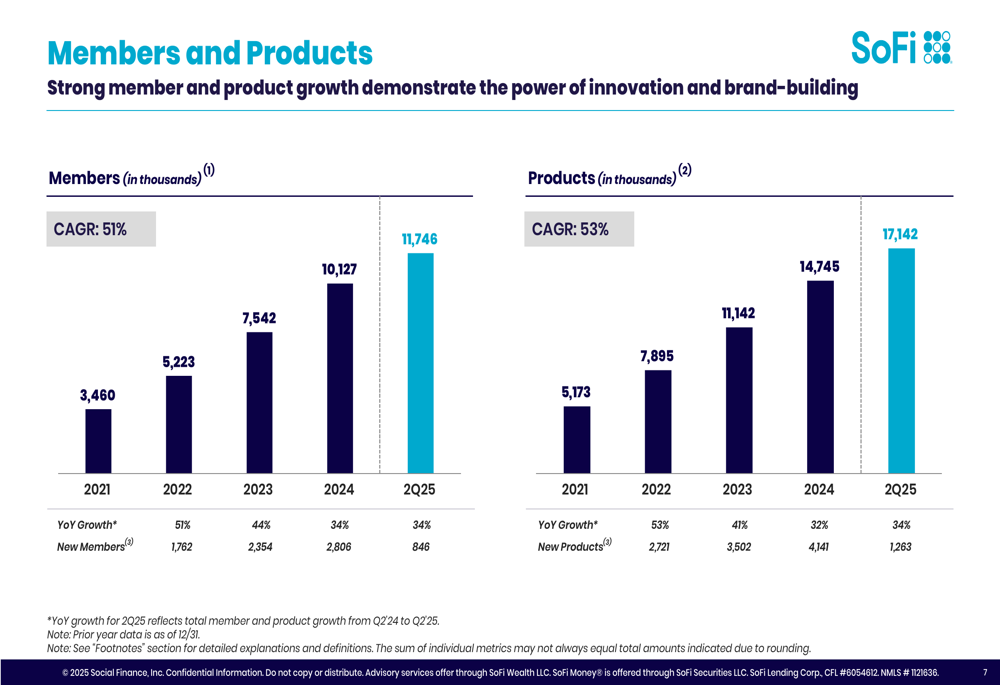

Member acquisition remained robust with 850,000 new members added during the quarter, bringing the total to 11.75 million – a 34% increase year-over-year. Product adoption was equally strong with 1.3 million new products added, reaching 17.14 million total products.

As shown in the following chart of SoFi’s member and product growth trajectory:

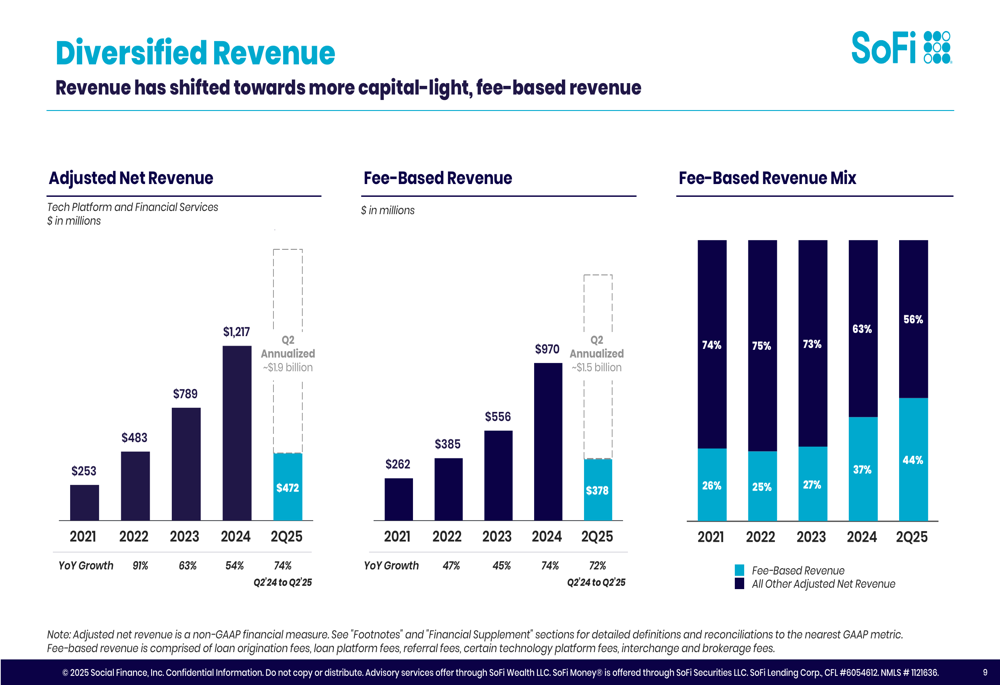

Fee-based revenue has become an increasingly important component of SoFi’s business model, growing 72% year-over-year to $378 million and now representing 44% of adjusted net revenue – up from 37% in 2024 and just 27% in 2023. This shift reflects the company’s strategic diversification beyond interest-based lending revenue.

The following chart illustrates SoFi’s revenue diversification and the growing contribution of fee-based revenue:

Detailed Financial Analysis

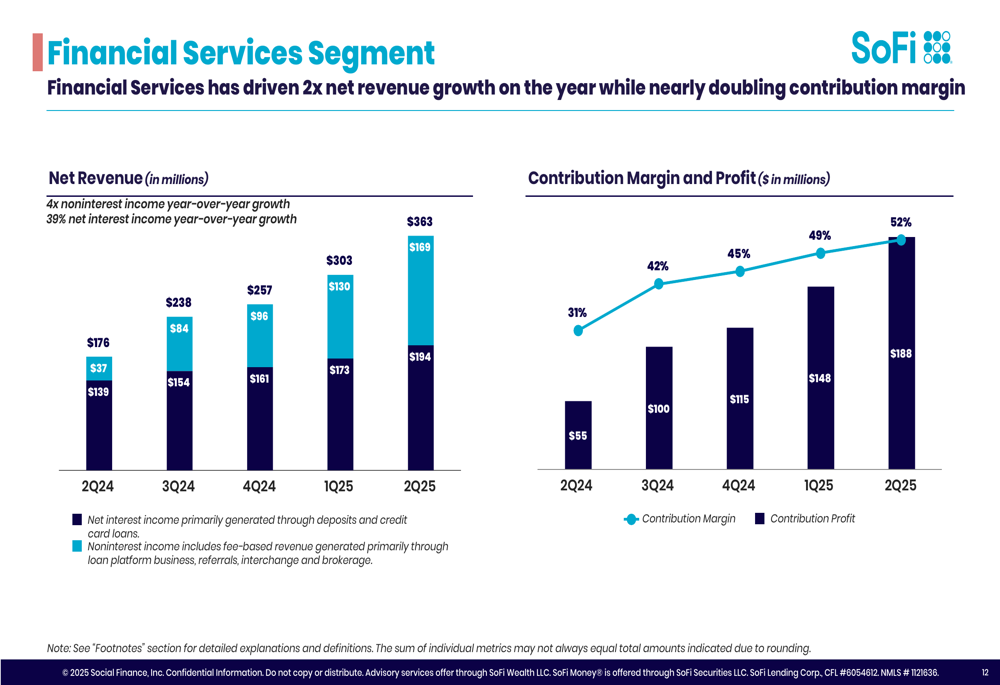

SoFi’s financial performance showed strength across all three business segments. The Financial Services segment nearly doubled its contribution margin year-over-year while delivering 2x net revenue growth. The segment generated $194 million in net revenue with a 49% contribution margin, producing $188 million in contribution profit.

As shown in the following segment performance chart:

The Lending segment continued to deliver strong results with adjusted net revenue of $373 million, up 32% year-over-year, and maintained a healthy 55% contribution margin generating $245 million in contribution profit. Loan originations reached a record $8.8 billion in the quarter.

The Technology Platform segment, which includes Galileo and Technisys, generated $110 million in revenue (15% year-over-year growth) with a 30% contribution margin.

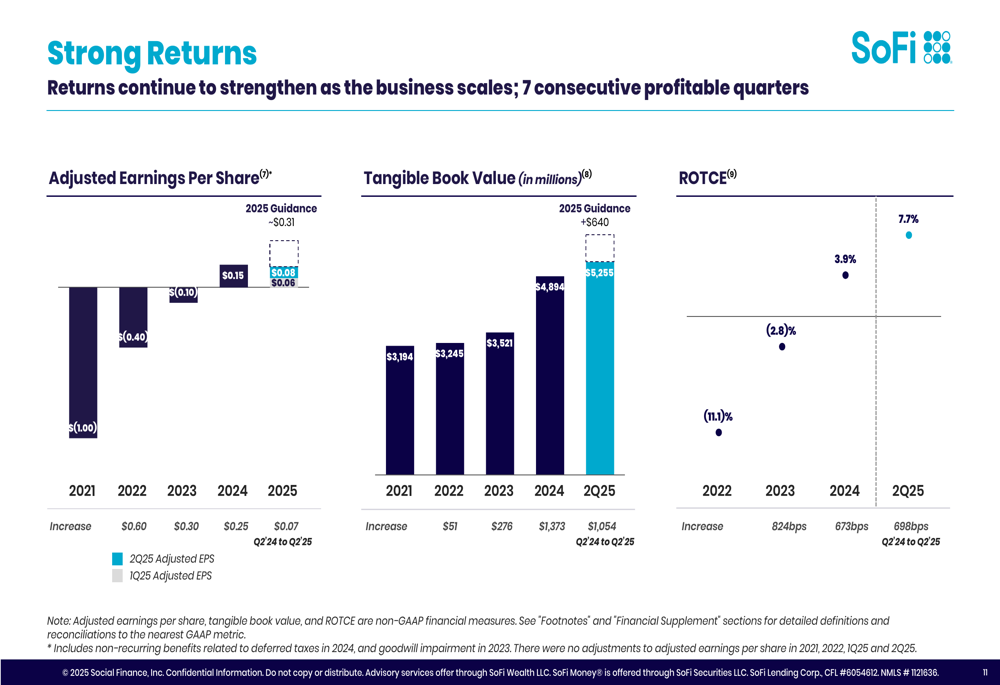

SoFi’s profitability metrics showed significant improvement, with adjusted EPS reaching $0.08 in Q2 2025, tangible book value growing to $5.26 billion, and return on tangible common equity (ROTCE) improving to 7.7%.

The following chart illustrates these improving profitability trends:

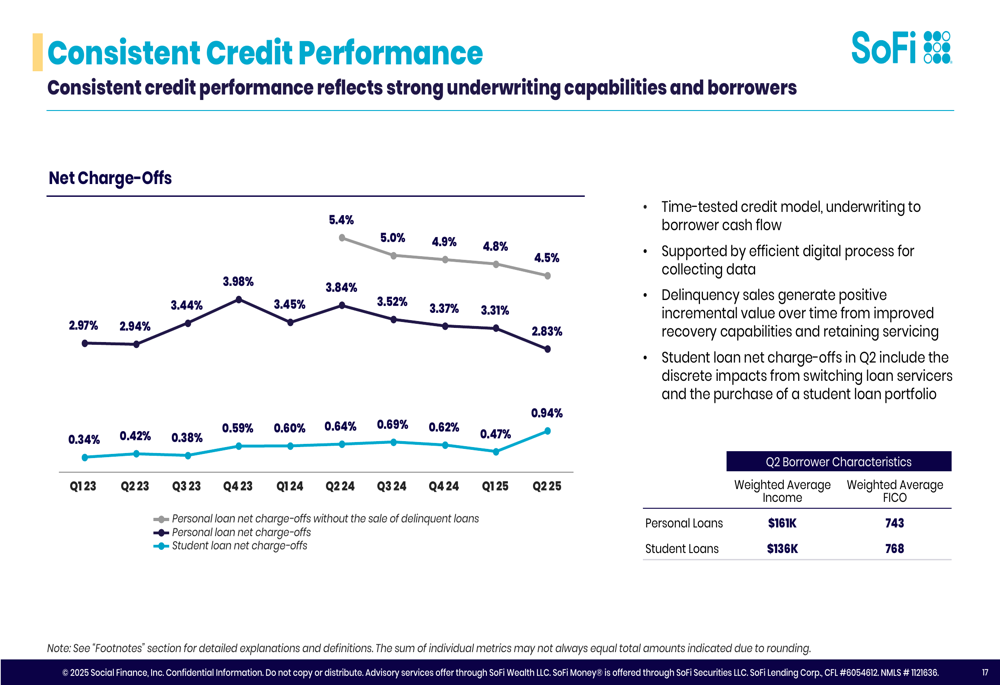

Credit quality remained strong despite the rapid growth in lending. Personal loan borrowers had a weighted average income of $161,000 and a weighted average FICO score of 743. Net charge-offs declined 48 basis points to 2.83%, while 90-day delinquencies for personal loans decreased 4 basis points sequentially to 42 basis points.

The following chart demonstrates SoFi’s consistent credit performance:

Strategic Initiatives

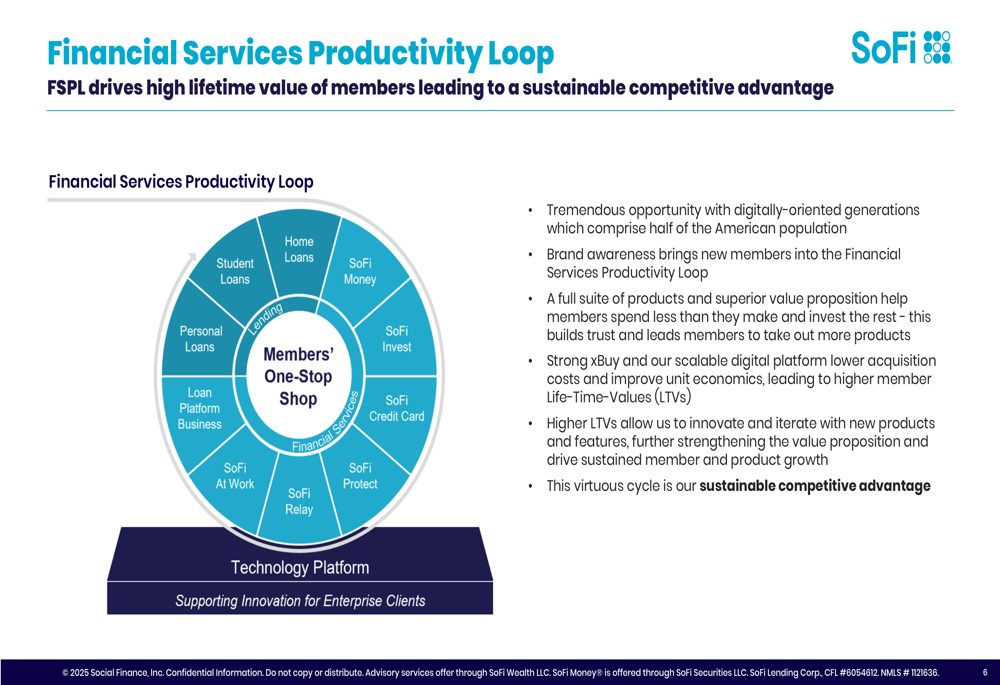

SoFi’s "Financial Services Productivity Loop" (FSPL) continues to be the cornerstone of its strategy, driving high lifetime value of members and creating a sustainable competitive advantage. The company emphasized how this integrated approach helps attract and retain customers across multiple product lines.

The following diagram illustrates SoFi’s Financial Services Productivity Loop:

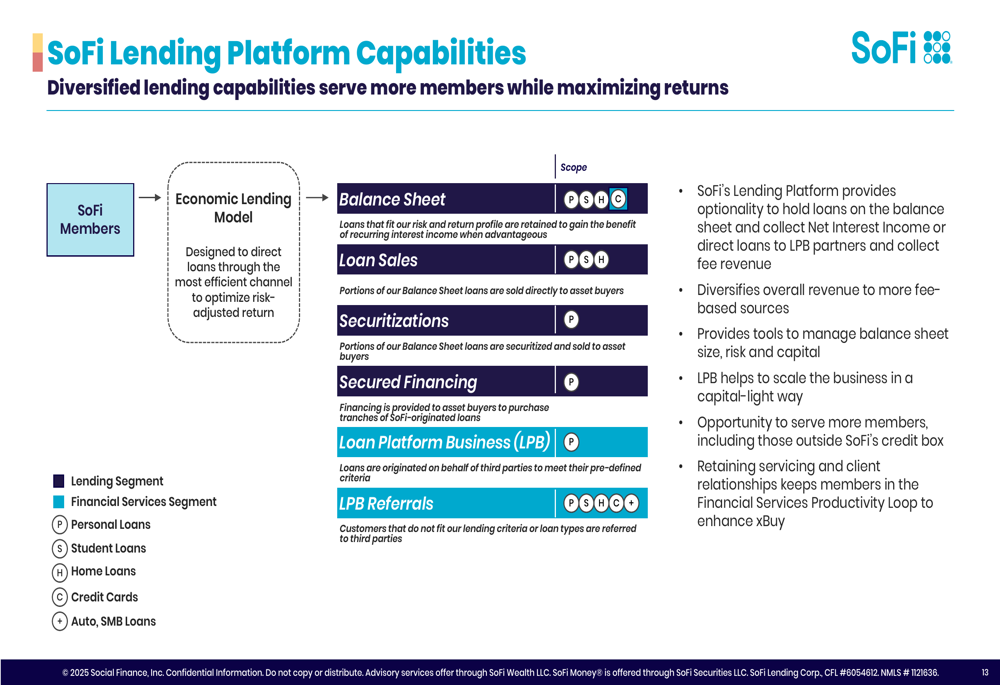

A key strategic initiative has been the expansion of SoFi’s Loan Platform Business (LPB), which allows the company to originate loans for third parties. This business is now running at an annualized pace of $9.5 billion in originations and over $500 million in high-margin, fee-based revenue. The LPB helps SoFi monetize more of the $100 billion in unmet loan demand that doesn’t fit its own credit box.

SoFi’s lending platform capabilities provide multiple options for managing loans:

The company has also focused on strengthening its deposit base, which now funds approximately 88% of its operations, up from just 43% in 2022 following its bank charter acquisition. This shift has reduced funding expenses by an estimated $552 million per year on an annualized basis while maintaining a strong net interest margin of 5.86%.

Forward-Looking Statements

SoFi raised its full-year 2025 guidance, now expecting:

- Adjusted net revenue of approximately $3,375 million (30% growth)

- Adjusted EBITDA of approximately $960 million (28% margin)

- Net income of approximately $370 million (11% margin)

- Diluted EPS of approximately $0.31

- Tangible book value growth of approximately $640 million

The company also expects to add at least 3 million new members in 2025, representing approximately 30% growth from 2024 levels.

SoFi’s capital position remains strong with a CET1 risk-based capital ratio of 14.3%, well above the 7.0% regulatory minimum, providing ample capacity for continued growth and potential capital returns in the future.

The Q2 2025 results and raised guidance suggest SoFi’s diversification strategy is paying off, with accelerating growth across multiple business lines and expanding profit margins. The company appears well-positioned to continue its transformation from a lending-focused business to a comprehensive digital financial services platform.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.