Nucor earnings beat by $0.08, revenue fell short of estimates

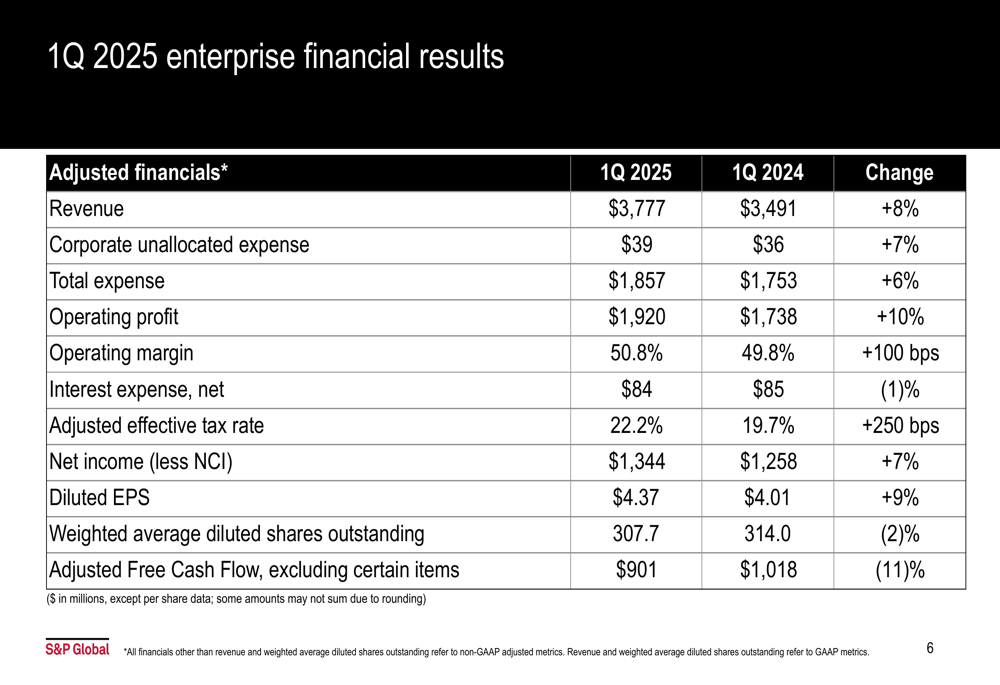

S&P Global Inc (NYSE:SPGI) reported robust first-quarter 2025 results on April 29, with revenue increasing 8% year-over-year to $3.78 billion, but simultaneously reduced its full-year guidance, suggesting potential headwinds for the remainder of the year.

Executive Summary

The financial information services provider delivered adjusted earnings per share of $4.37 in Q1, up 9% from the same period last year, while adjusted operating profit rose 10% to $1.92 billion. Operating margin expanded by 100 basis points to 50.8%.

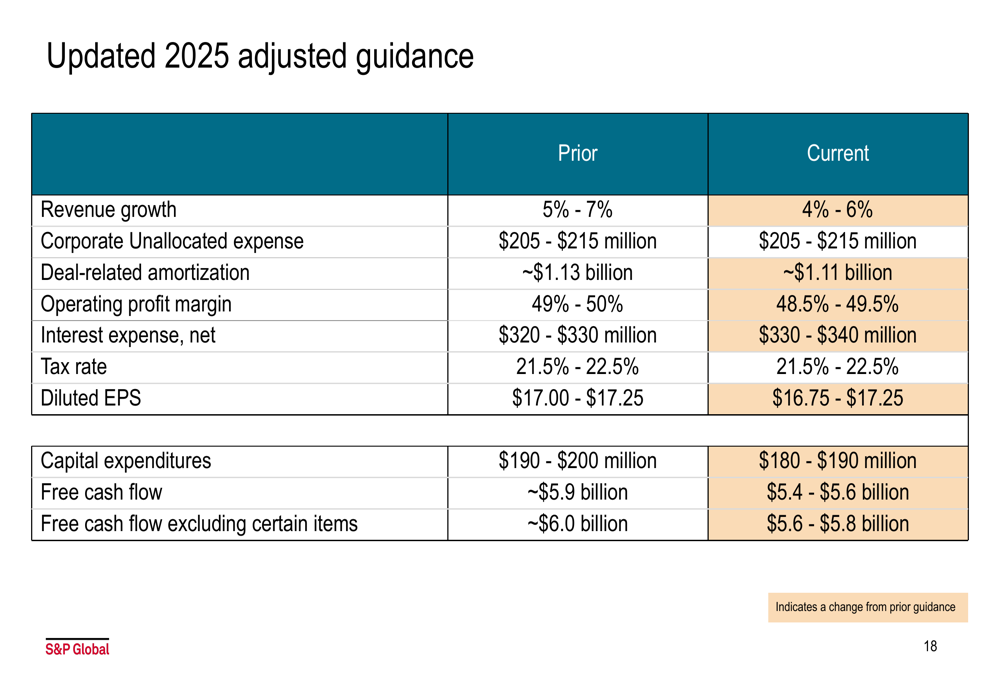

Despite these strong quarterly results, S&P Global lowered its full-year 2025 revenue growth forecast from 5-7% to 4-6% and reduced its free cash flow guidance from approximately $5.9 billion to $5.4-5.6 billion. The company maintained its adjusted EPS guidance range, though slightly adjusting it to $16.75-$17.25 from the previous $17.00-$17.25.

As shown in the following enterprise financial results:

Quarterly Performance Highlights

All five of S&P Global’s business segments delivered revenue growth in the first quarter, with S&P Dow Jones Indices leading the way with a 15% increase. The company’s recurring revenue remained strong across divisions, providing stability to the overall business model.

The Ratings division, which accounts for approximately 30% of total revenue, grew 8% year-over-year to $1.15 billion. This growth was primarily driven by structured finance and bank loan ratings in transaction revenue, which increased 7%, while non-transaction revenue rose 10%.

Market Intelligence, the company’s largest segment, posted a 5% revenue increase to $1.20 billion, with recurring revenue representing 95.3% of the segment’s total. Commodity Insights and Mobility both achieved 9% revenue growth, reaching $612 million and $420 million respectively.

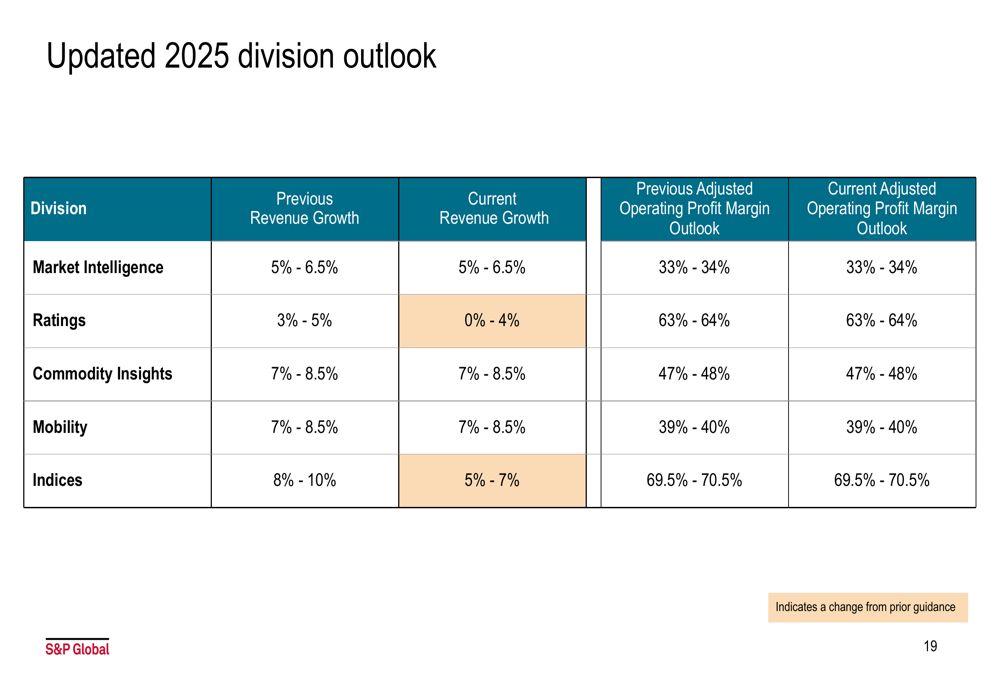

The company’s updated division outlook for 2025 shows significant revisions, particularly for Ratings and Indices:

Detailed Financial Analysis

S&P Global’s adjusted free cash flow declined 11% year-over-year to $901 million in Q1 2025. The company paid dividends of $295 million during the quarter and maintained a strong balance sheet with cash and cash equivalents of $1.47 billion.

The Ratings segment continued to demonstrate its high-margin profile with an operating margin of 66.2%, an improvement of 150 basis points from Q1 2024. S&P Dow Jones Indices maintained its position as the most profitable segment with a 72.9% operating margin.

Commodity Insights showed notable margin improvement, with operating margin expanding by 90 basis points to 48.1%. This segment benefited from double-digit increases in Advisory & Transactional Services, and Energy & Resources Data & Insights.

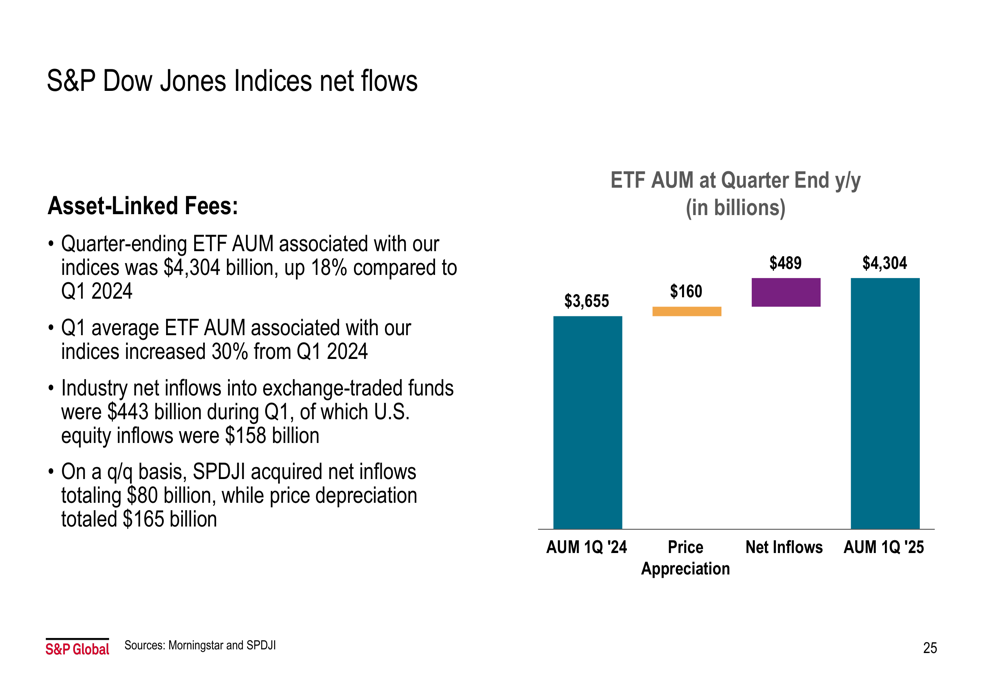

The ETF assets under management (AUM) associated with S&P Dow Jones Indices reached $4.30 trillion at the end of Q1, representing an 18% increase year-over-year. Net inflows into exchange-traded funds were $443 billion, with SPDJI capturing $80 billion of these inflows.

Market Context

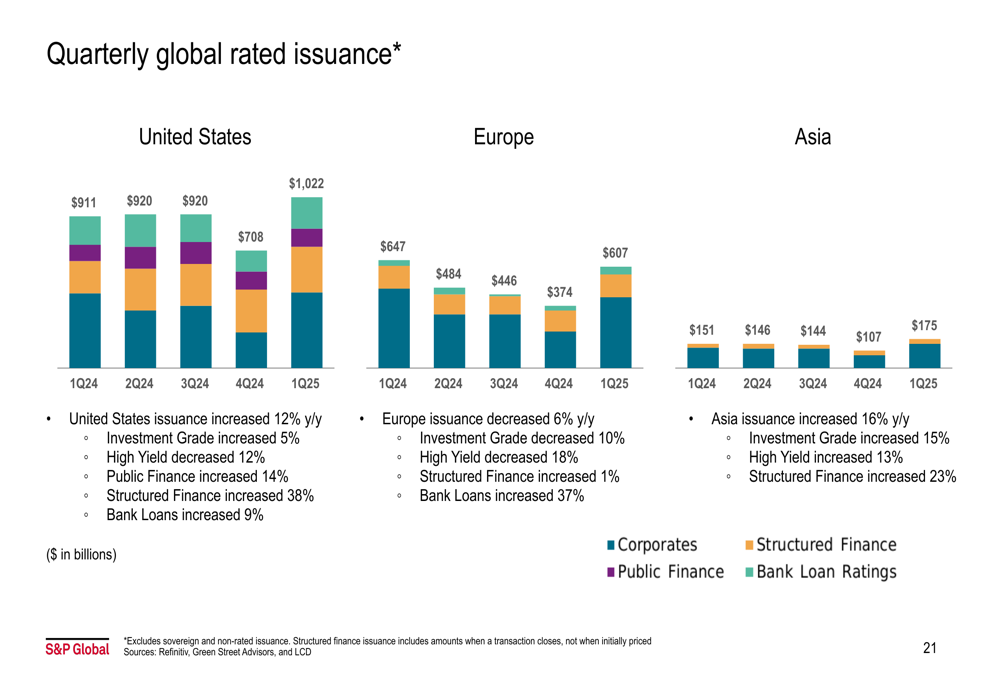

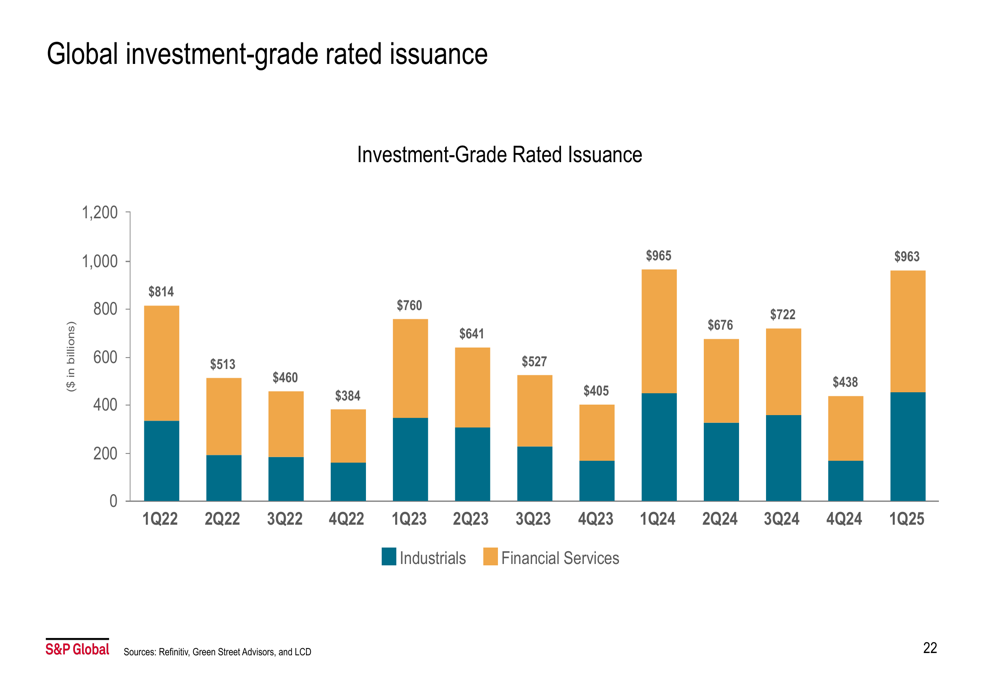

Global issuance trends varied by region in Q1 2025, with the United States and Asia showing growth while Europe experienced a decline. U.S. issuance increased 12% year-over-year, with investment-grade issuance rising 5%. Asian issuance grew 16%, with a 15% increase in investment-grade issuance. However, European issuance decreased 6%, with investment-grade issuance down 10%.

The following chart illustrates these regional issuance trends:

Investment-grade issuance showed continued strength, with both industrial and financial services sectors contributing to growth:

Forward-Looking Statements

S&P Global’s revised guidance for 2025 suggests caution about the remainder of the year despite the strong start. The company lowered its GAAP and adjusted revenue growth expectations and reduced its free cash flow projections.

The most significant revisions were in the Ratings and Indices divisions. Ratings revenue growth forecast was cut from 3-5% to 0-4%, while Indices was reduced from 8-10% to 5-7%. These adjustments suggest the company anticipates challenges in debt issuance activity and potentially slower growth in index-linked investment products for the remainder of 2025.

The updated adjusted guidance shows these changes in detail:

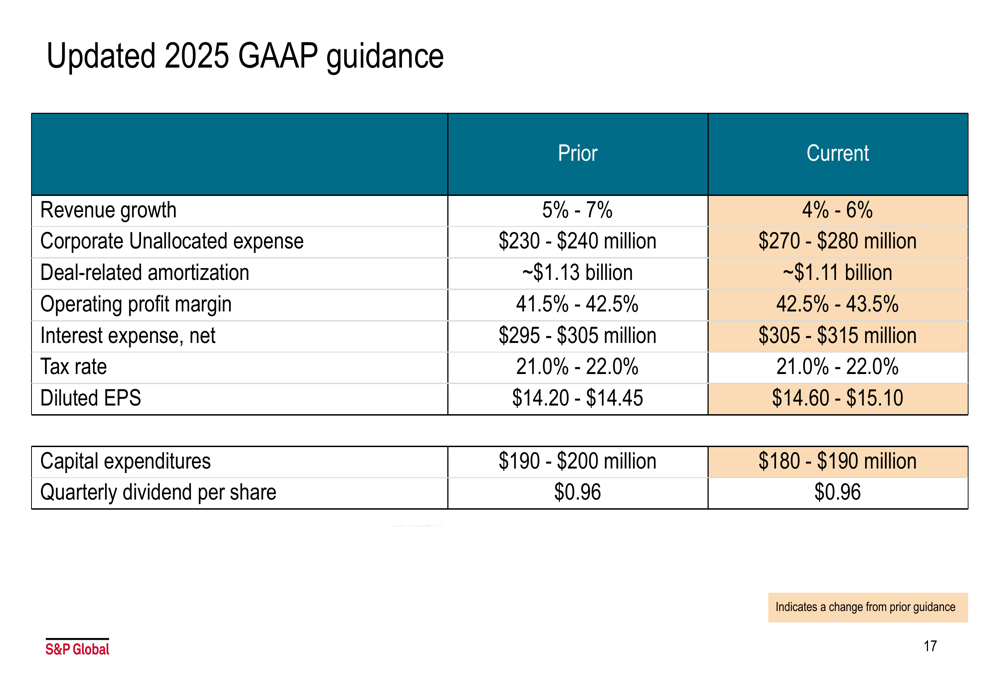

The GAAP guidance reflects similar adjustments, though with some improvements in operating profit margin:

Analyst Perspectives

The market’s premarket reaction to S&P Global’s earnings was positive, with shares trading up 2.92% at $493.39. This suggests investors may be focusing on the strong Q1 results rather than the reduced guidance.

The company’s performance should be viewed in the context of its previous quarter. In Q3 2024, S&P Global reported a 16% year-over-year increase in revenue, with the Ratings division’s transaction revenue surging over 80%. The current quarter’s more modest growth rates may reflect normalization after exceptional previous performance.

S&P Global’s consistent dividend history, having maintained payments for 54 consecutive years and raised dividends for 11 consecutive years, continues to make it attractive to income-focused investors despite the cautious outlook for the remainder of 2025.

The company’s ability to maintain strong margins across all business segments, even while revising revenue expectations downward, demonstrates operational efficiency and cost discipline that should help weather potential market challenges in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.