US stock futures flounder amid tech weakness, Fed caution

Introduction & Market Context

S&P Global Inc (NYSE:SPGI) presented its second quarter 2025 earnings results on July 31, showcasing solid performance across its business segments despite mixed market conditions. The financial information services provider reported 6% year-over-year revenue growth, building on the momentum established in the first quarter.

In premarket trading following the presentation, S&P Global shares rose 1.45% to $537, reflecting investor confidence in the company’s performance and updated outlook.

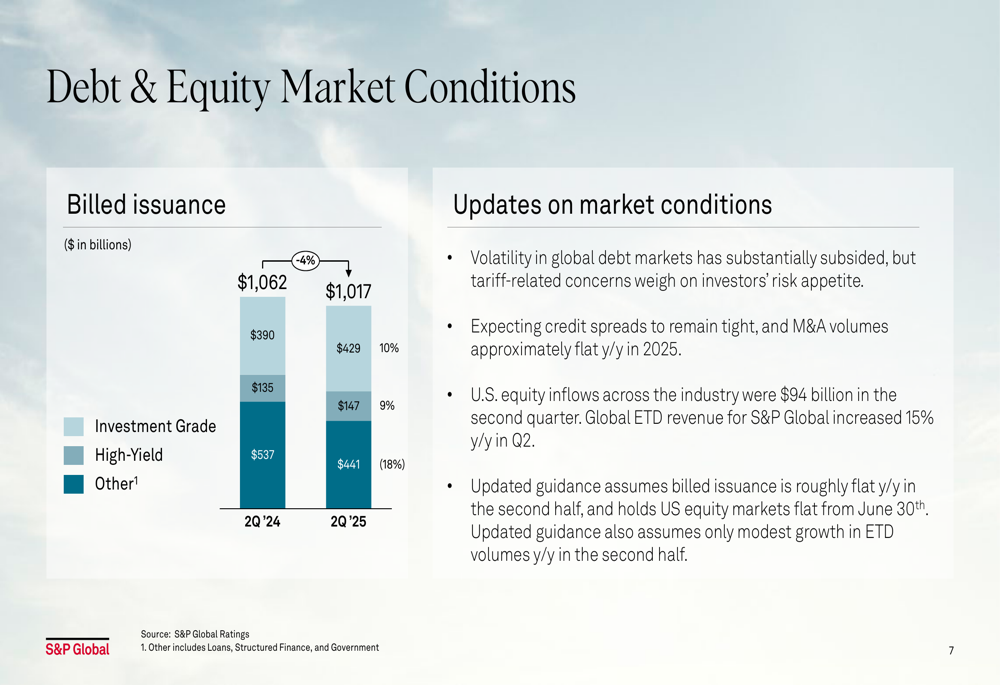

Market conditions presented a mixed backdrop for the quarter, with the company noting that volatility in global debt markets has substantially subsided, though tariff-related concerns continue to weigh on investor risk appetite.

As shown in the following chart detailing debt market conditions and billed issuance trends:

Quarterly Performance Highlights

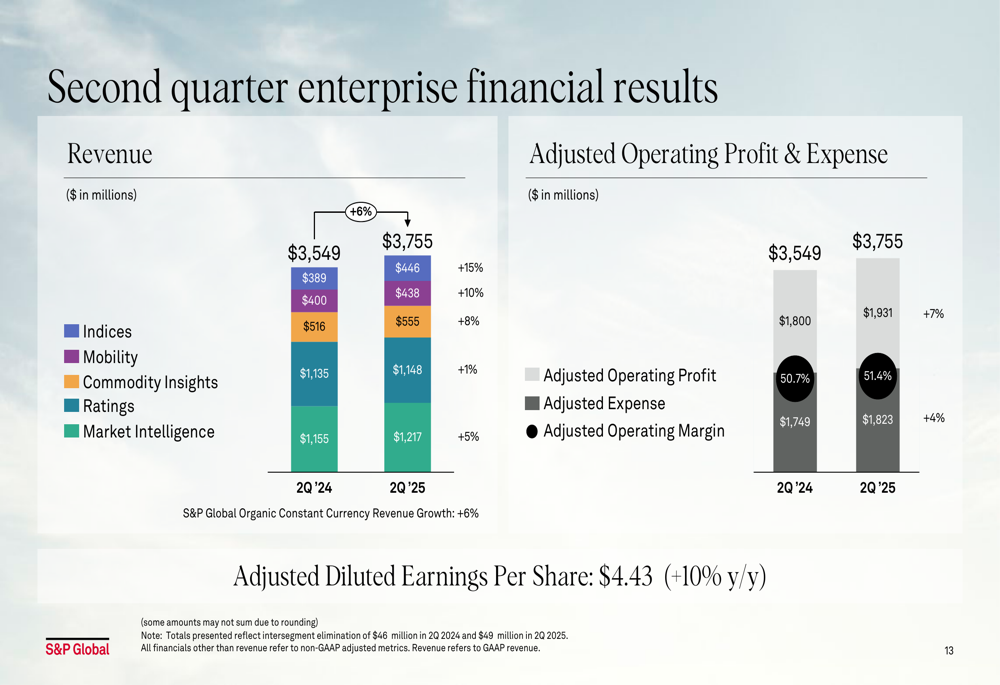

S&P Global reported strong financial results for Q2 2025, with revenue increasing 6% year-over-year to $3.76 billion. The company’s subscription products showed particularly robust growth at 7%, demonstrating the resilience of S&P Global’s recurring revenue streams.

Adjusted operating profit increased 7% compared to the same period last year, while trailing twelve-month adjusted operating margins expanded by 150 basis points to 49.5%. Adjusted diluted earnings per share grew 10% year-over-year to $4.43, exceeding analyst expectations.

The company also returned nearly $950 million to shareholders through dividends and share repurchases during the quarter.

The following slide summarizes the key financial and strategic highlights from the quarter:

A more detailed breakdown of the enterprise financial results shows the performance across revenue, adjusted operating profit, and earnings per share:

Divisional Performance Analysis

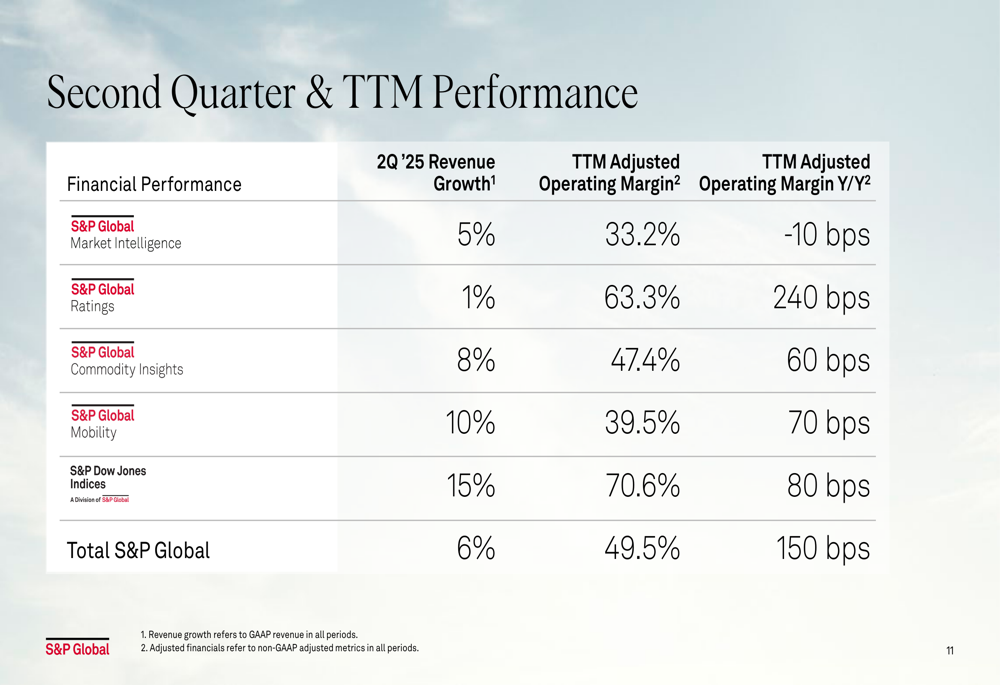

Performance varied across S&P Global’s business divisions, with S&P Dow Jones Indices leading the pack with 15% revenue growth, followed by Mobility at 10%, Commodity Insights at 8%, Market Intelligence at 5%, and Ratings at 1%.

The following table provides a comprehensive view of divisional performance metrics:

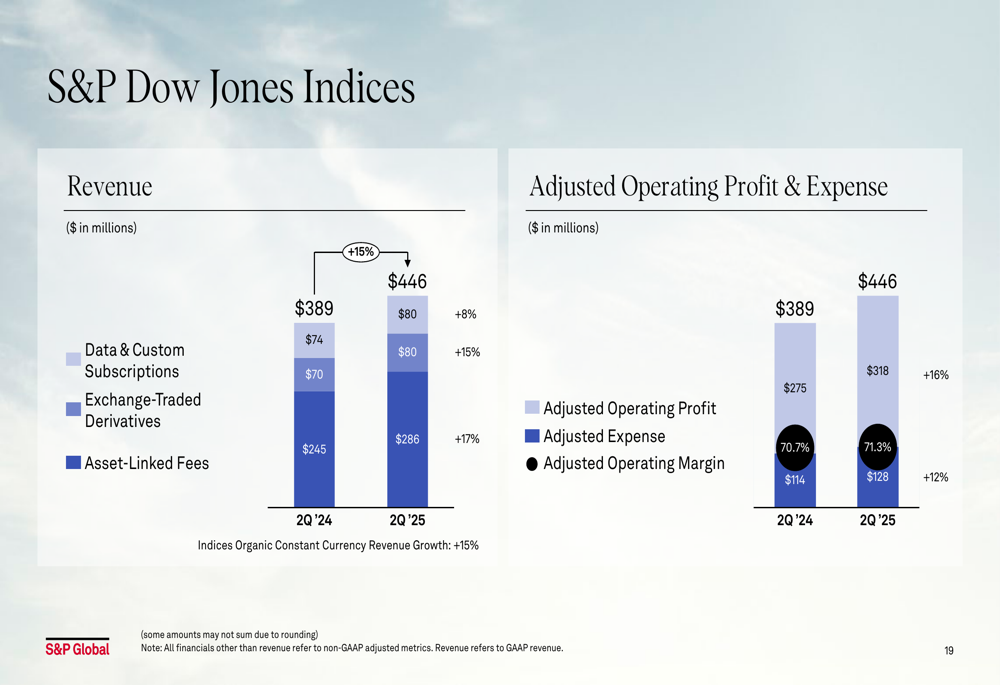

S&P Dow Jones Indices delivered exceptional results, with revenue increasing 15% to $446 million, driven by 17% growth in asset-linked fees and 15% growth in data and custom subscriptions. The division maintained an impressive adjusted operating margin of 71.3%.

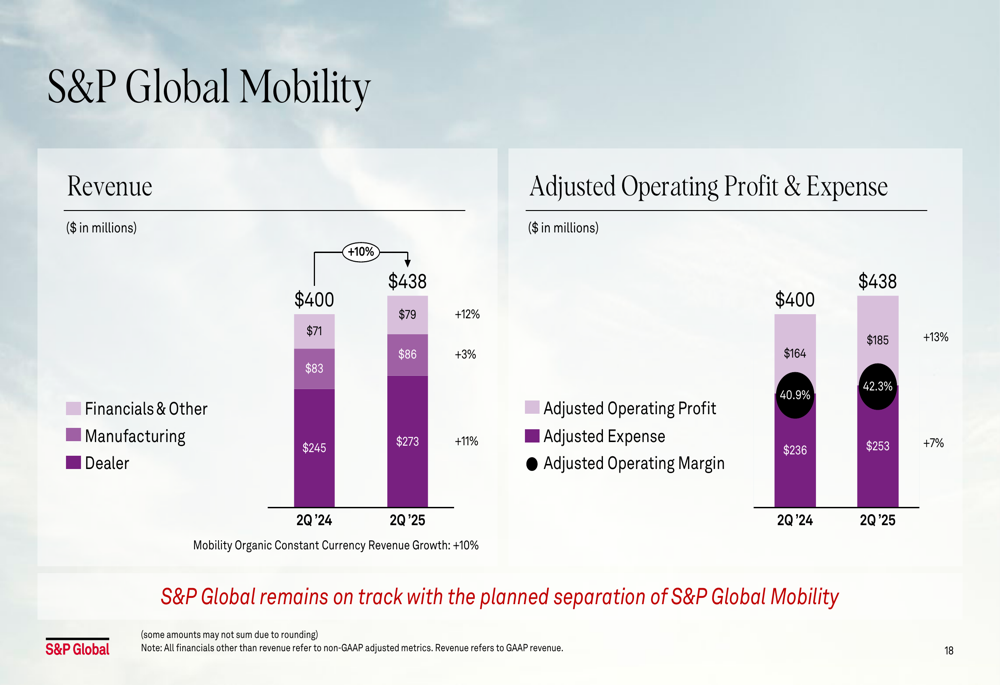

S&P Global Mobility continued its strong performance with 10% revenue growth to $438 million, with particularly strong results in the Dealer segment (11% growth) and Financials & Other (12% growth). The company confirmed that the planned separation of the Mobility division remains on track.

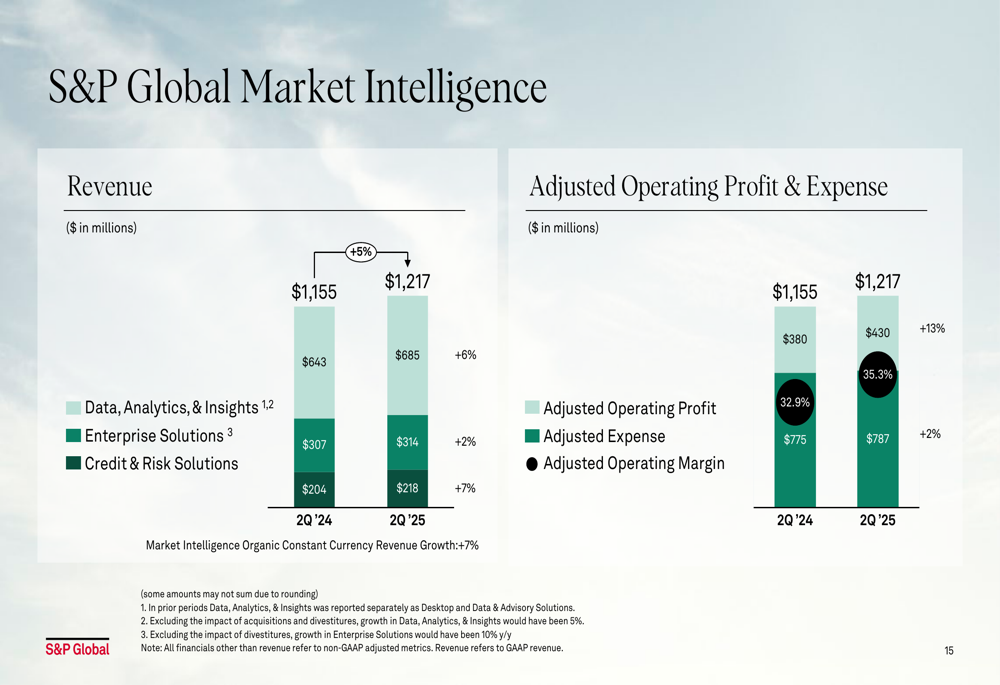

S&P Global Market Intelligence reported 5% revenue growth to $1.22 billion, with Data, Analytics, & Insights growing 6% and Credit & Risk Solutions growing 7%. The division showed significant margin improvement, with adjusted operating margin increasing from 32.9% to 35.3% year-over-year.

Strategic Initiatives

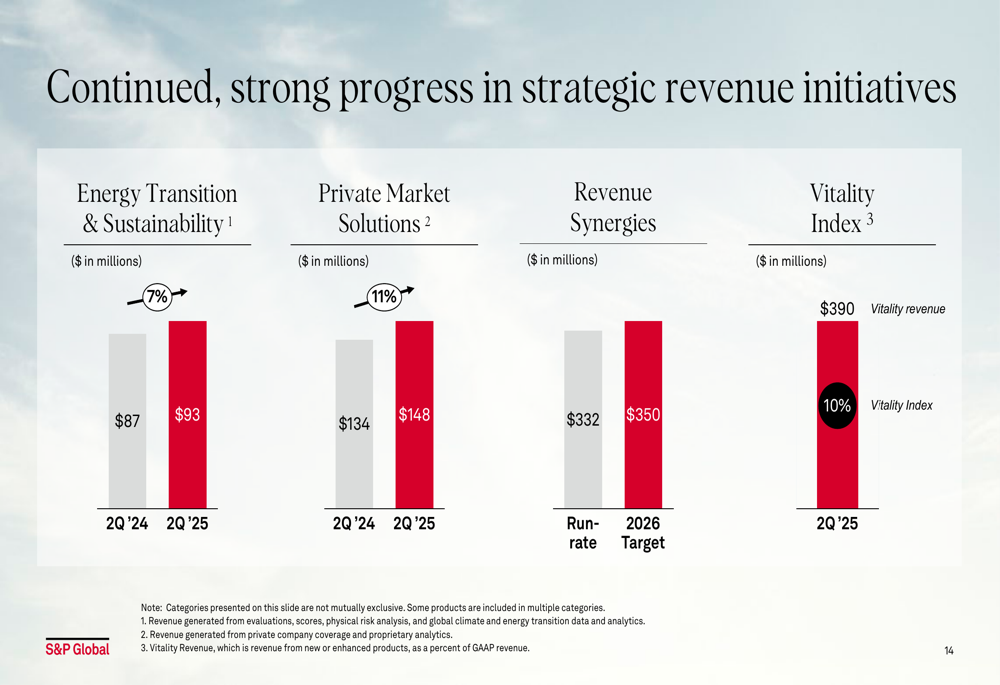

S&P Global highlighted several strategic initiatives driving growth, including enhanced commercial engagement, progress in private credit markets, and accelerating innovation in artificial intelligence.

The company reported strong momentum in its commercial initiatives through the Chief Client Office and Market Intelligence Revenue Transformation, focusing on strengthening customer relationships and optimizing go-to-market strategies:

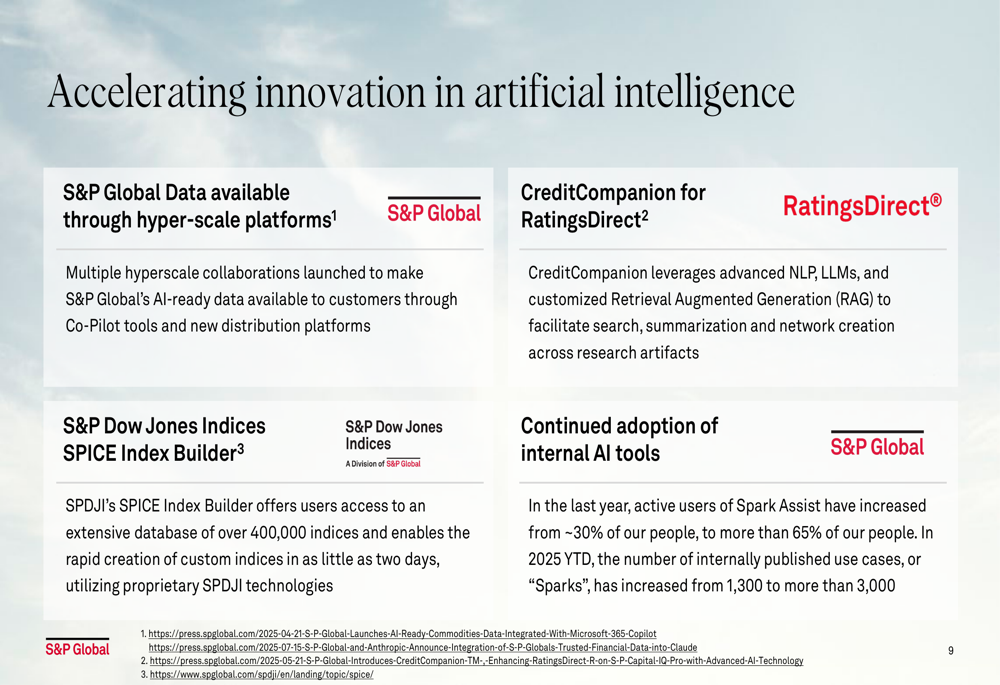

S&P Global is also making significant strides in artificial intelligence innovation, with multiple hyperscale collaborations to make its AI-ready data available to customers, the launch of CreditCompanion for RatingsDirect, and the SPICE Index Builder for rapid creation of custom indices:

The planned separation of the Mobility division continues to progress, with Bill Eager, the current CEO of CARFAX, appointed as Mobility President and CEO designate of the planned standalone public company.

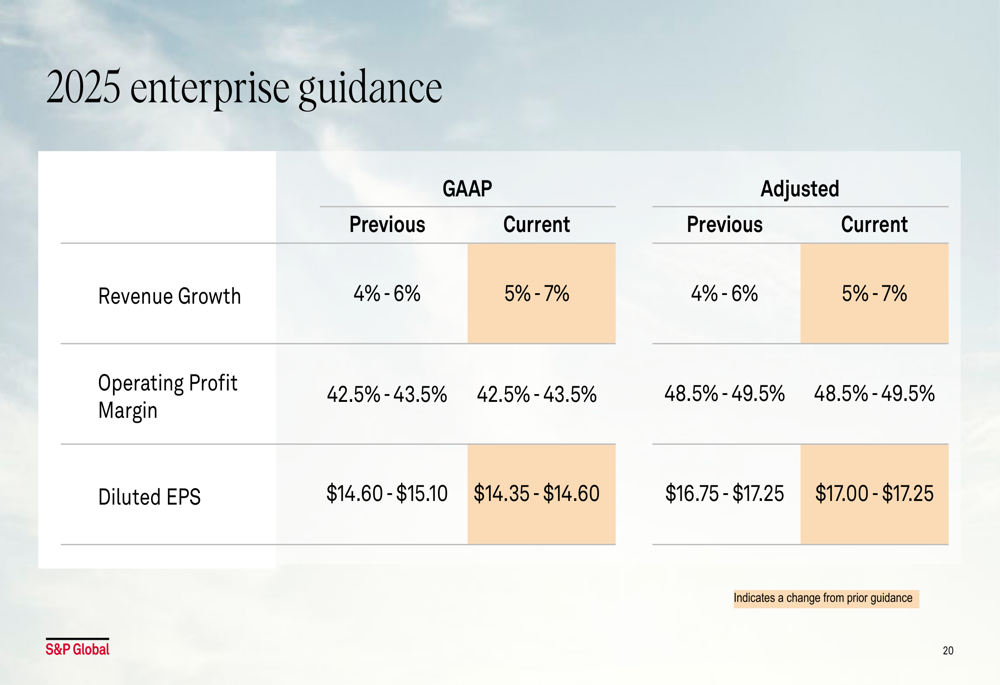

Updated Guidance & Outlook

Based on the strong performance in the first half of 2025, S&P Global raised its full-year revenue growth guidance to 5-7%, up from the previous 4-6%. The company maintained its adjusted operating profit margin guidance at 48.5-49.5% and narrowed its adjusted diluted EPS guidance to $17.00-$17.25, from the previous range of $16.75-$17.25.

The following slide details the updated enterprise guidance for 2025:

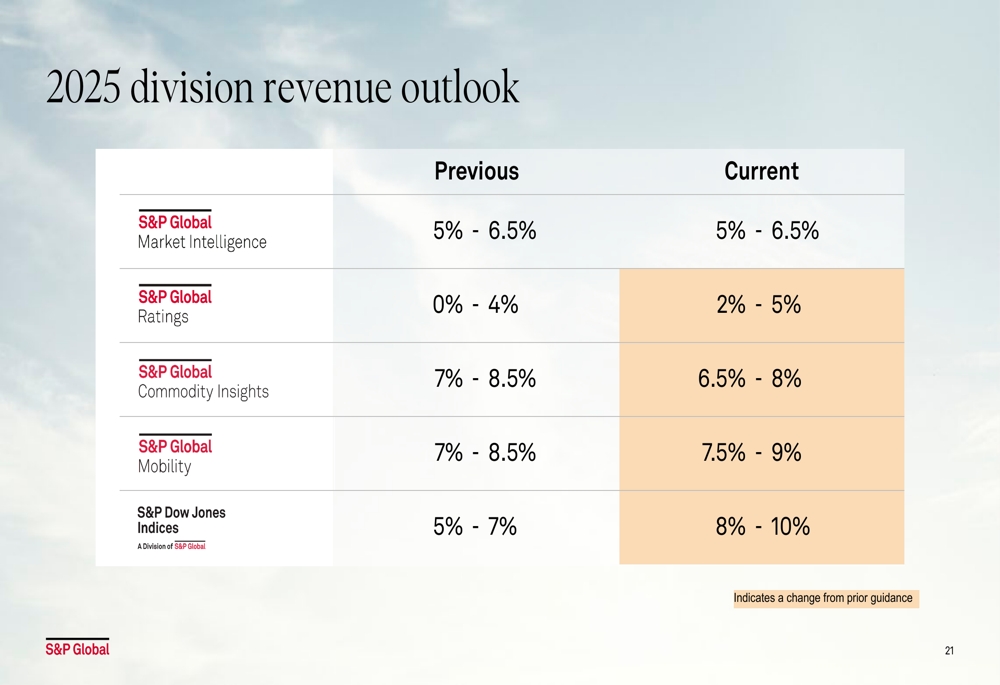

At the divisional level, S&P Global raised its revenue outlook for S&P Dow Jones Indices to 8-10% (from 5-7%) and S&P Global Ratings to 2-5% (from 0-4%), while slightly adjusting the outlook for other divisions:

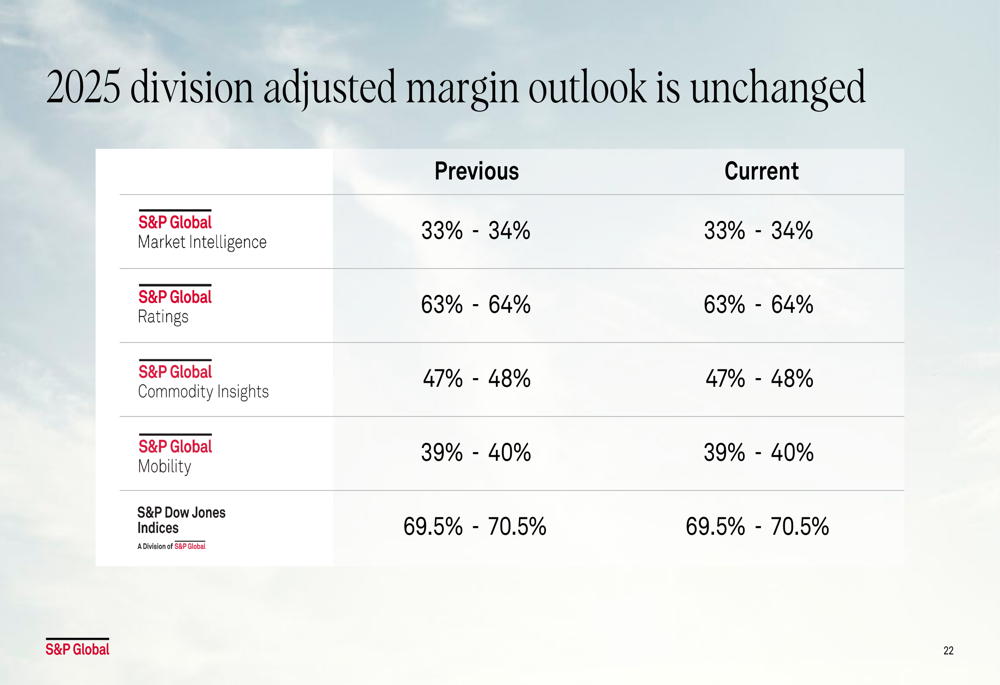

The company maintained its divisional adjusted margin outlook unchanged across all business segments:

S&P Global’s updated guidance assumes billed issuance will be roughly flat year-over-year in the second half of 2025, with U.S. equity markets remaining flat from June 30th levels, and only modest growth in exchange-traded derivatives volumes.

The company’s continued focus on strategic revenue initiatives, margin expansion, and innovation positions it well for sustained growth in the remainder of 2025 and beyond, despite ongoing macroeconomic uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.