US LNG exports surge but will buyers in China turn up?

Introduction & Market Context

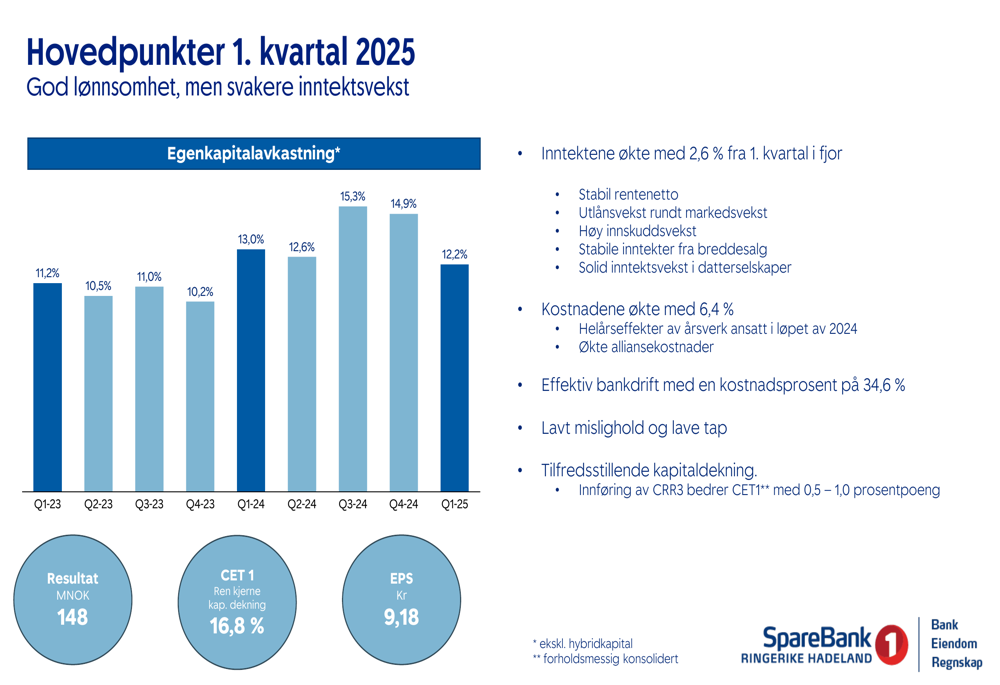

SpareBank 1 Ringerike Hadeland (RING) reported a 2% year-over-year increase in profit for Q1 2025, reaching 148 million NOK, according to the bank’s quarterly presentation released on May 8. The Norwegian regional bank maintained profitability above its target despite facing headwinds from slowing income growth and rising costs.

The stock traded down 1.85% following the presentation, with shares closing at 378 NOK, well above the 52-week low of 286 NOK but below the high of 415 NOK.

SpareBank 1 Ringerike Hadeland operates as a market leader in growing regions near Oslo, serving approximately 70,000 customers through its network of branches in Jevnaker, Gran, Nittedal, and headquarters in Hønefoss.

Quarterly Performance Highlights

The bank reported a return on equity of 12.2% for Q1 2025, exceeding its target of 11% but showing a decline from higher levels seen in previous quarters. Total (EPA:TTEF) income increased by 2.6% compared to Q1 2024, while costs rose at a faster rate of 6.4%, primarily due to new hires and increased alliance costs.

As shown in the following key highlights slide, the bank maintained efficient operations with a cost ratio of 34.6% and reported earnings per share of 9.18 NOK:

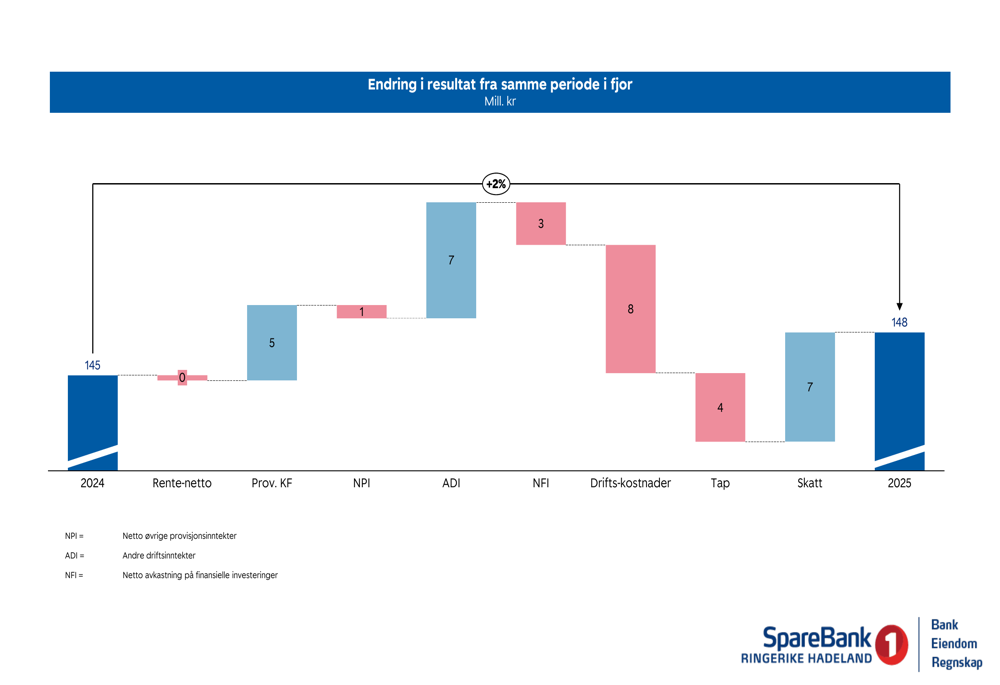

The year-over-year result change reveals the factors contributing to the modest profit growth. While net interest income (+5 million NOK) and other income categories showed improvements, these gains were partially offset by lower net return on financial investments (-8 million NOK) and higher operating costs (+4 million NOK):

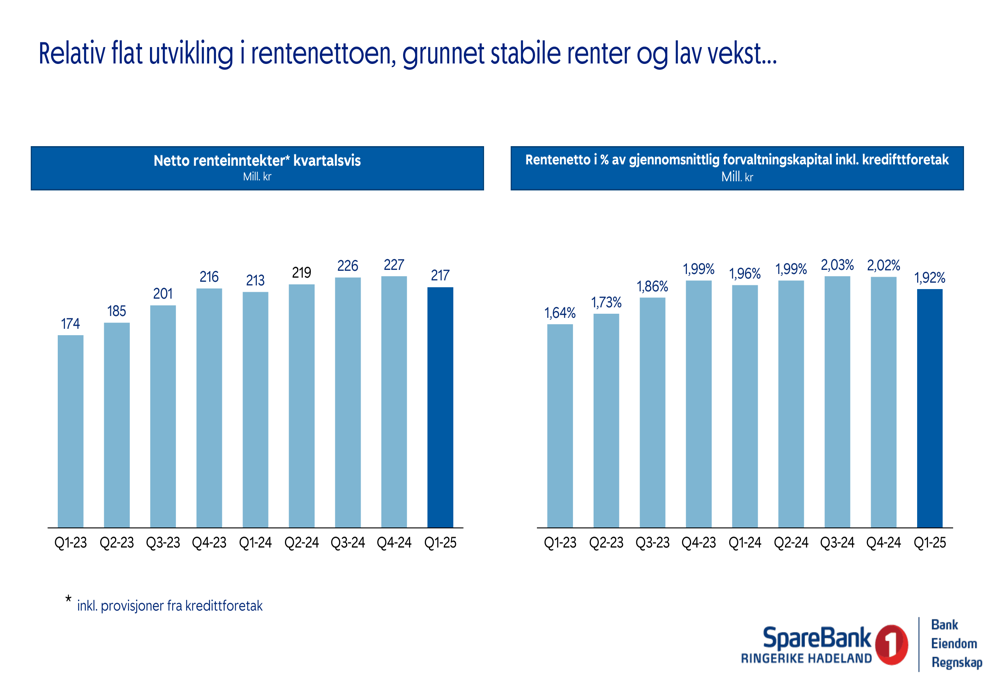

Net interest income remained relatively flat quarter-over-quarter, which the bank attributed to stable interest rates and low growth. The following chart illustrates this trend, showing net interest income and margins over the past nine quarters:

Detailed Financial Analysis

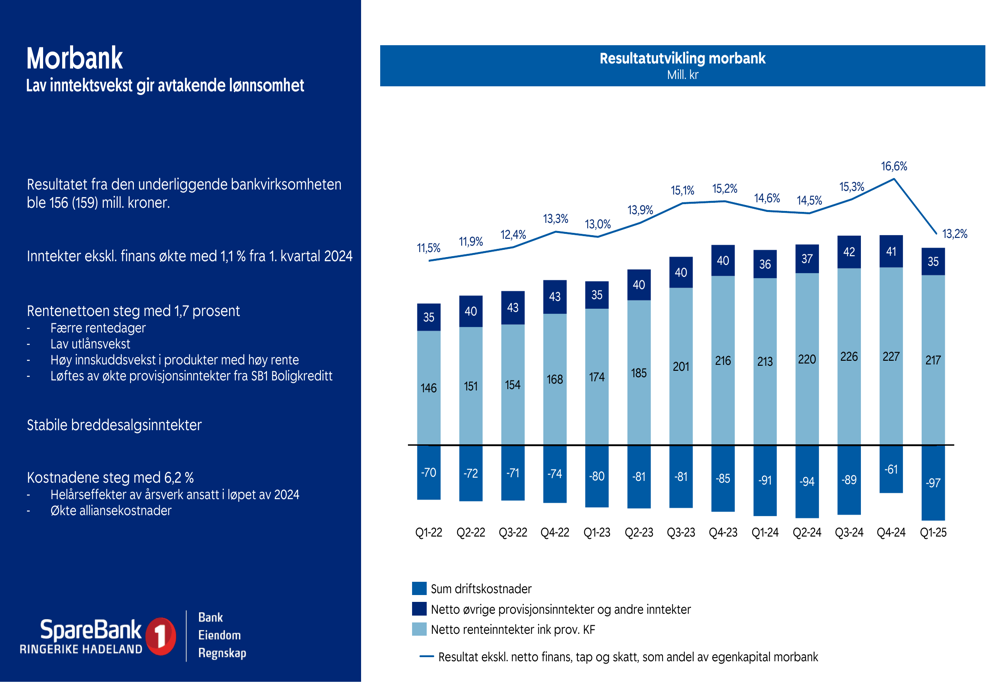

The parent bank (Morbank) reported profit before tax of 156 million NOK, with income before finance growing by just 1.1%. Net interest income increased by 1.7%, while costs grew by 6.2%, creating pressure on profitability:

A closer examination of the changes in net interest income reveals the complex factors affecting this key revenue driver. While lending growth (+8.2 million NOK) and deposit growth (+14.7 million NOK) positively impacted results, these gains were partially offset by the effects of deposit rates (-3.5 million NOK) and securities returns (-12.1 million NOK):

The bank reported loan growth of 2.8% including credit institutions, with personal market loans growing by 2.2% and business market loans by 3.8%. Deposit growth was strong at 7.0%, improving the bank’s funding position.

Credit quality remained strong with low default rates and minimal loan losses. The bank reported a loss cost of 0.05% of gross loans, reflecting the solid quality of its loan portfolio.

Strategic Initiatives & Regional Position

SpareBank 1 Ringerike Hadeland emphasized its strong market position in its primary region, where it holds 35% of the mortgage market, 53% of the business market, and facilitates 45% of real estate transactions. The bank highlighted the strategic advantages of its location in growing regions near Oslo with ongoing infrastructure improvements.

The presentation outlined significant growth potential in the region, noting over 10,000 acres available for business development, 12 industrial and business parks, and access to substantial renewable energy resources:

The bank’s financial goals show it is exceeding targets for both profitability and capital strength, while maintaining an investor-friendly dividend policy with a minimum payout ratio of 60% of the group’s profit:

Forward-Looking Statements

Management presented 10 reasons for optimism about the bank’s future prospects, highlighting its strong brand combining SpareBank 1’s national presence with 191 years of local tradition, cost-effective operations, and diversified income sources:

The outlook section noted high competition for mortgage customers with demand picking up slightly. Business sentiment shows muted optimism but with activity improving somewhat. The bank expects defaults and losses to remain low relative to the total portfolio but acknowledged they could increase due to persistent high interest rates and inflation.

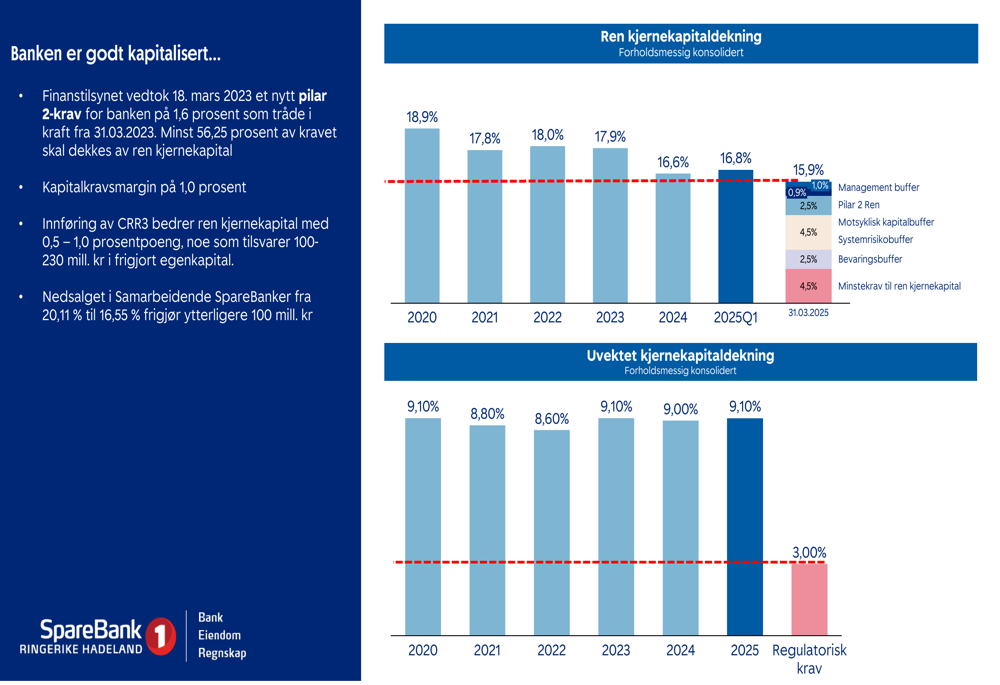

Capital position remains strong with a CET1 ratio of 16.8%, well above the target of 15.9%. The bank noted that the implementation of CRR3 regulations is expected to improve the CET1 ratio by 0.5-1.0 percentage points:

SpareBank 1 Ringerike Hadeland maintained its strategic priorities focused on customer service excellence, community building, and leveraging economies of scale through the SpareBank 1 Alliance. Management indicated they will continue to balance solidness, profitability, cost development, and growth going forward.

The bank’s presentation reflected cautious optimism, acknowledging near-term challenges with income growth while emphasizing its strong regional position and long-term growth opportunities in an economically developing area near Norway’s capital.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.