US stock futures inch lower after Wall St marks fresh records on tech gains

Introduction & Market Context

Standard BioTools Inc (NASDAQ:LAB) presented its first quarter 2025 financial results on May 6, showing continued revenue challenges but significant progress on cost reduction initiatives. The company’s stock closed at $1.15 on the day of the presentation and edged up 0.94% to $1.07 in aftermarket trading, still well below its 52-week high of $2.74.

The life sciences company, which completed its merger with SomaLogic in January 2024, continues to navigate a challenging market environment while executing on its strategic pivot toward proteomics and operational efficiency. This quarter’s results reflect ongoing implementation of the Standard BioTools Business System (SBS) and integration synergies from the SomaLogic merger.

Quarterly Performance Highlights

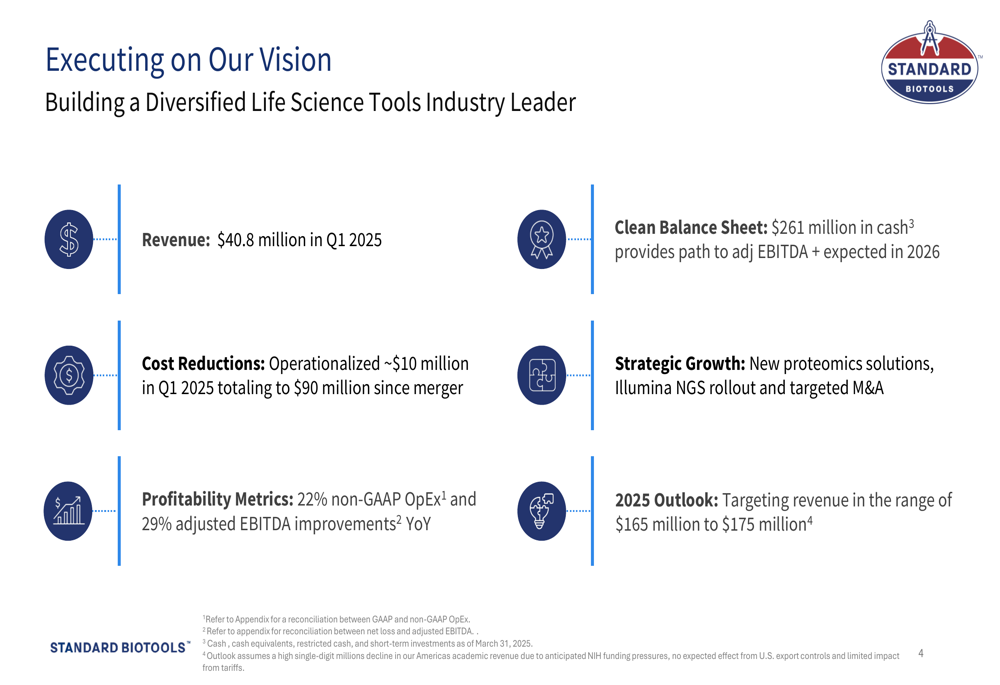

Standard BioTools reported Q1 2025 revenue of $40.8 million, representing a 10% year-over-year decline, continuing the downward trend seen in Q4 2024. Despite the revenue challenges, the company highlighted significant cost reductions and operational improvements.

As shown in the following financial highlights slide:

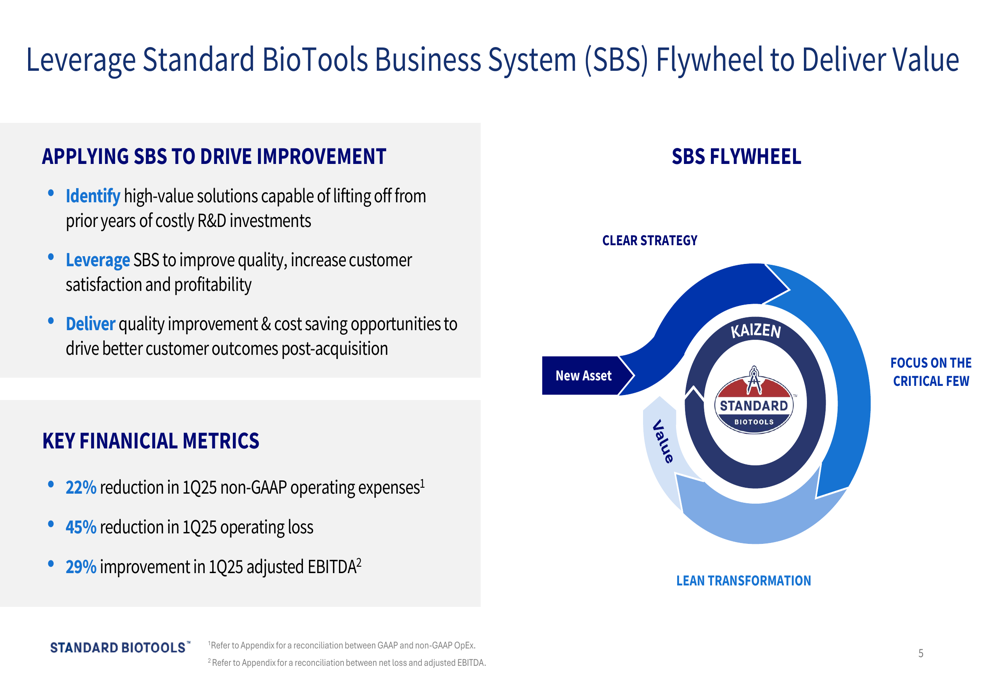

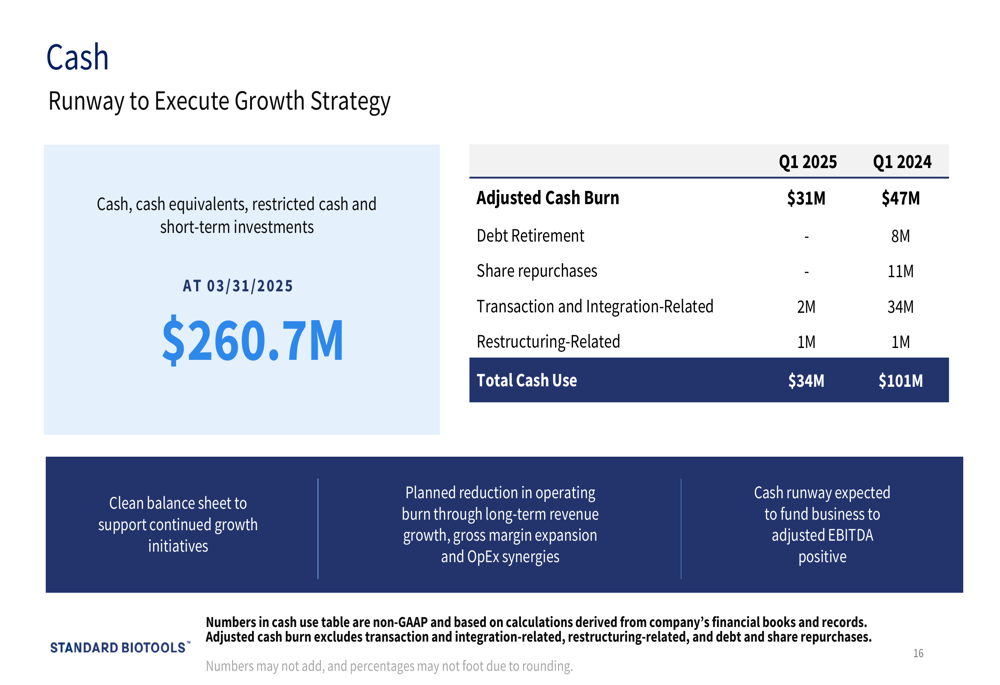

The company operationalized approximately $10 million in cost reductions during Q1 2025, contributing to a 22% reduction in non-GAAP operating expenses and a 29% improvement in adjusted EBITDA year-over-year. Standard BioTools maintained a strong balance sheet with $261 million in cash as of March 31, 2025.

CEO Michael Egholm emphasized the company’s progress in implementing the Standard BioTools Business System (SBS), which has been instrumental in driving operational efficiencies:

Detailed Financial Analysis

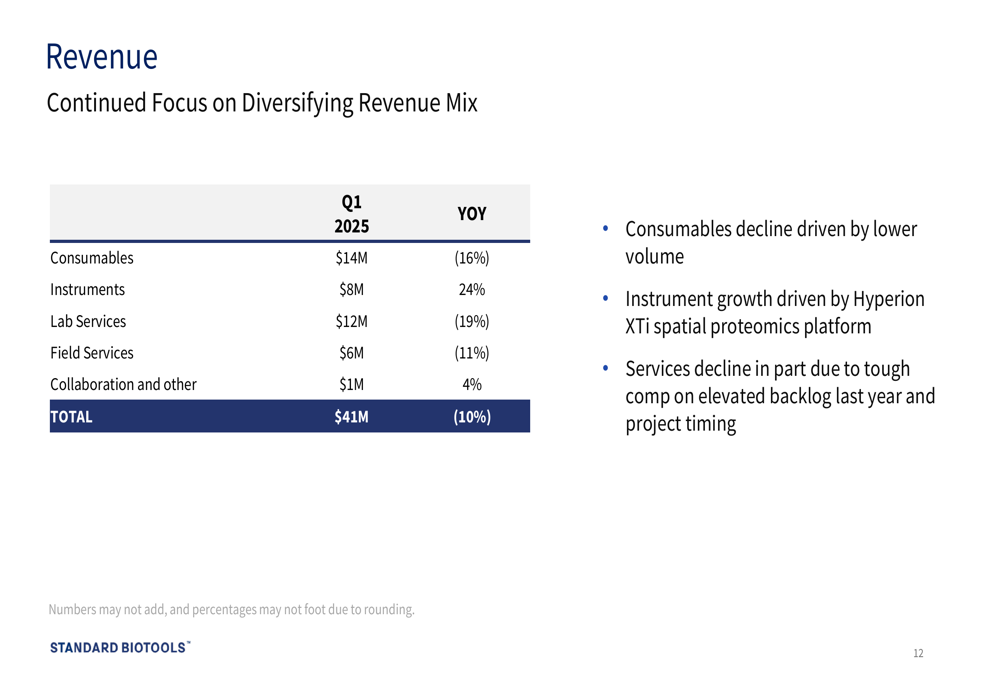

The company’s revenue breakdown reveals mixed performance across product categories. While instruments showed growth, other segments experienced declines:

Instrument revenue grew 24% year-over-year to $8 million, driven by the Hyperion XTi spatial proteomics platform. However, consumables revenue declined 16% to $14 million due to lower volume, and lab services fell 19% to $12 million, partly attributed to tough comparisons with elevated backlog from the previous year.

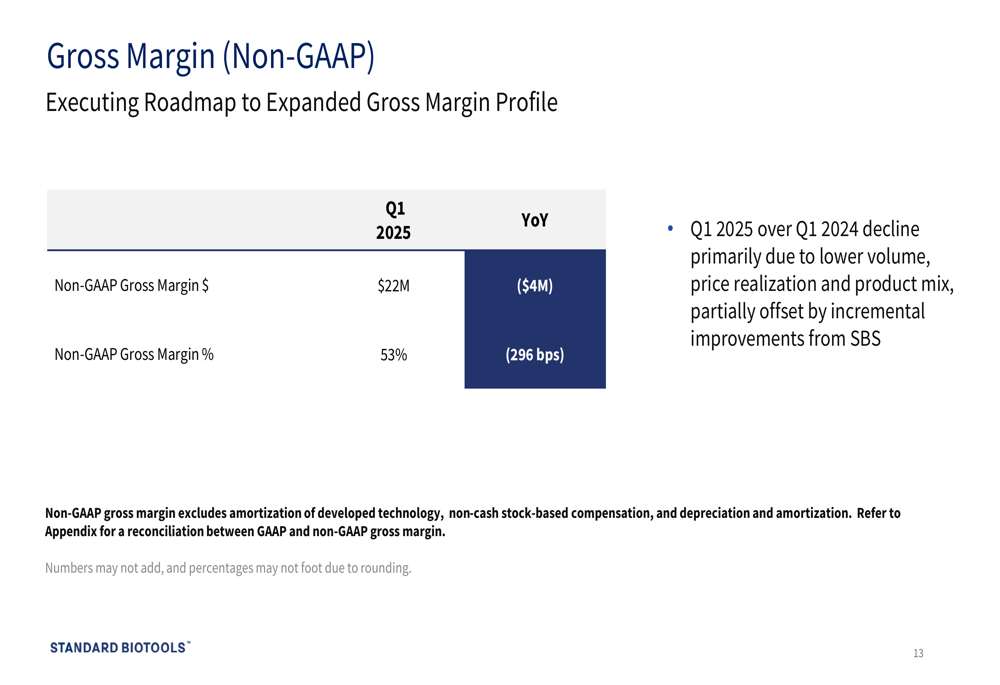

Gross margin performance also showed some pressure:

The non-GAAP gross margin was 53% in Q1 2025, with the decline primarily attributed to lower volume, price realization, and product mix. This represents a continuation of the margin pressure seen in Q4 2024, when gross margin was 52.5%, down from 55.4% the previous year.

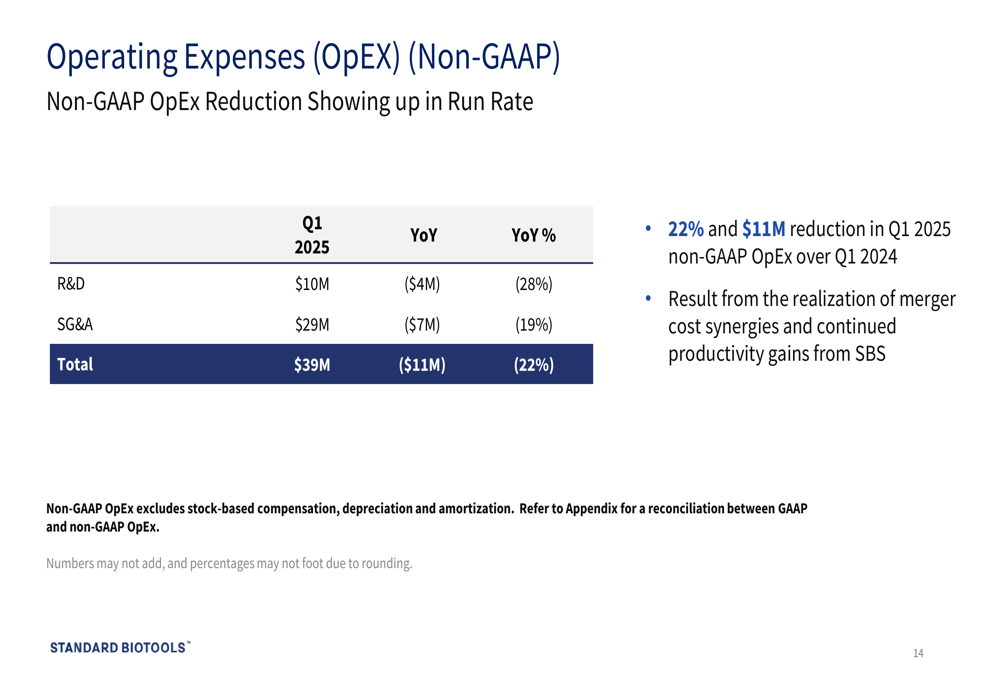

Operating expenses showed significant improvement:

Non-GAAP operating expenses totaled $39 million in Q1 2025, a 22% reduction from the prior year. This included a 28% reduction in R&D expenses to $10 million and a 19% reduction in SG&A expenses to $29 million. These reductions reflect the realization of merger cost synergies and productivity gains from the SBS implementation.

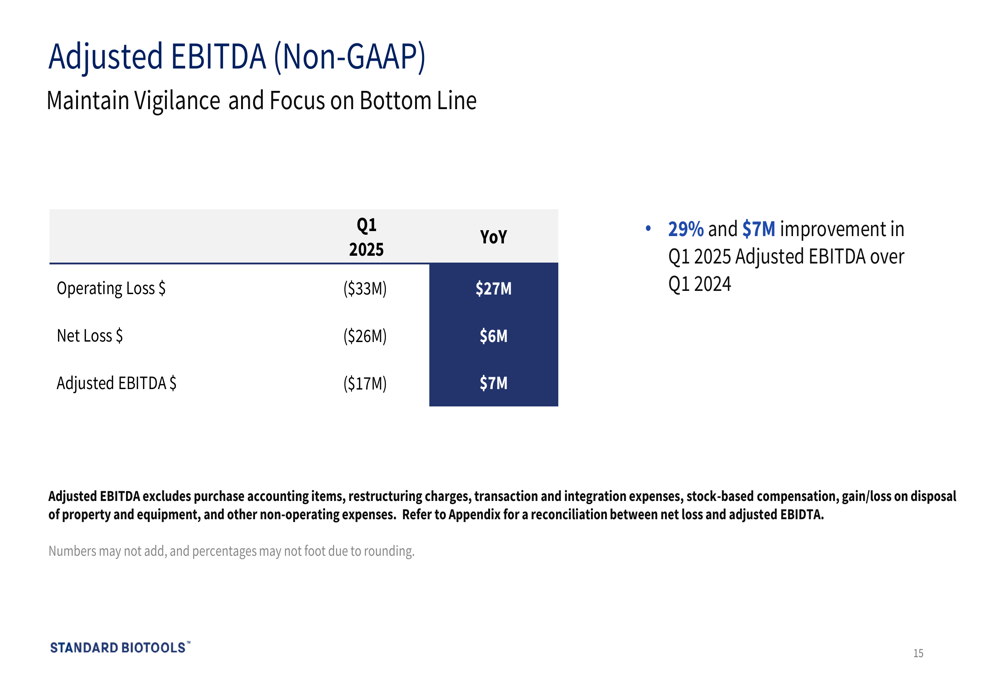

The company’s adjusted EBITDA showed improvement despite revenue challenges:

Adjusted EBITDA for Q1 2025 was -$17 million, representing a 29% improvement compared to Q1 2024. This improvement was driven by the significant cost reductions implemented across the organization.

Cash management also showed improvement:

Strategic Initiatives

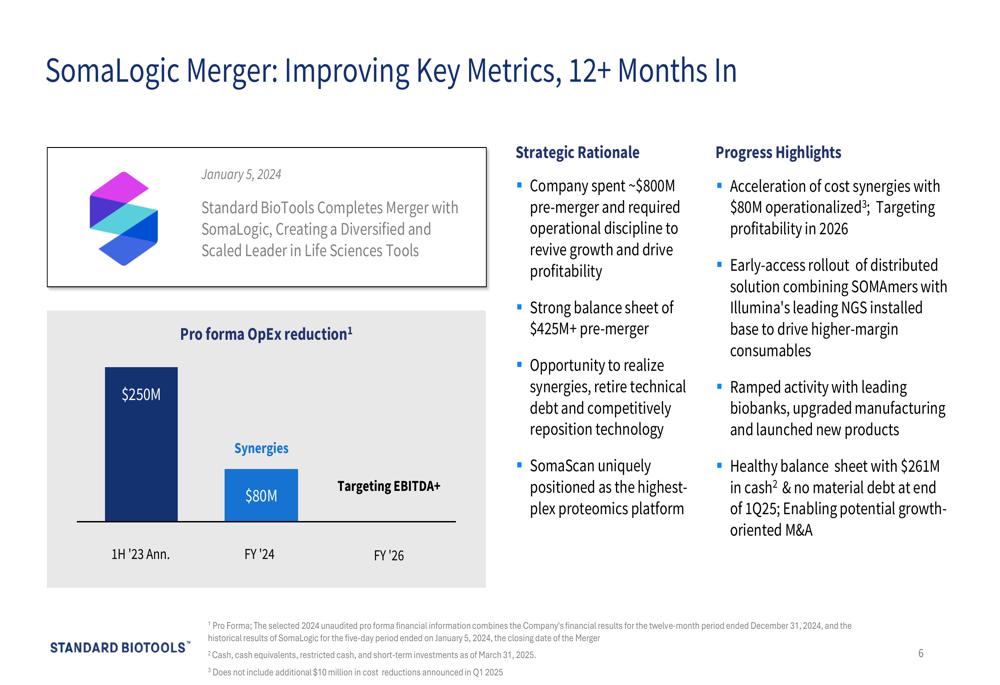

Standard BioTools highlighted significant progress in integrating the SomaLogic acquisition and realizing synergies. The company has operationalized $80 million in cost synergies, accelerating its path to profitability targeted for 2026:

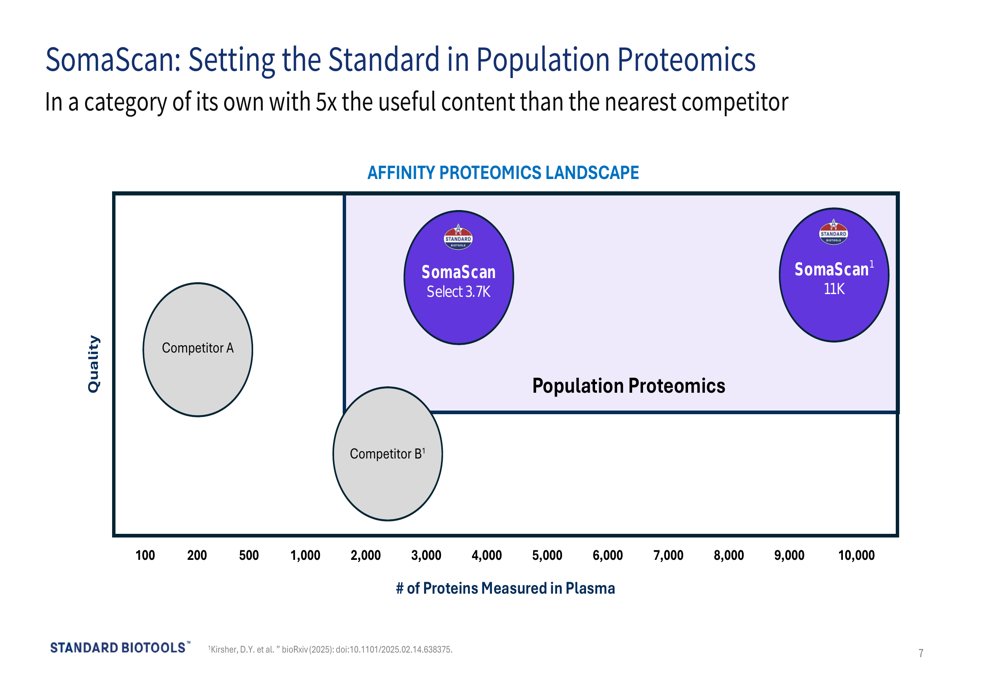

A key strategic focus for Standard BioTools is its SomaScan proteomics platform, which the company positions as having a significant competitive advantage in the market:

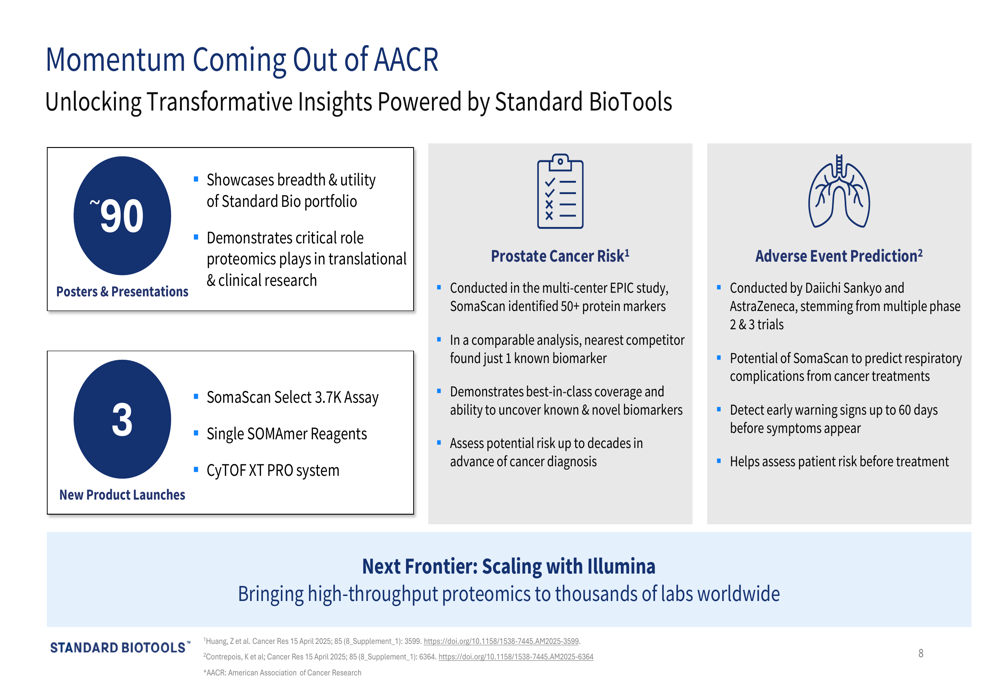

The company also highlighted momentum from the American Association for Cancer Research (AACR) conference, where approximately 90 posters and presentations showcased Standard BioTools’ portfolio:

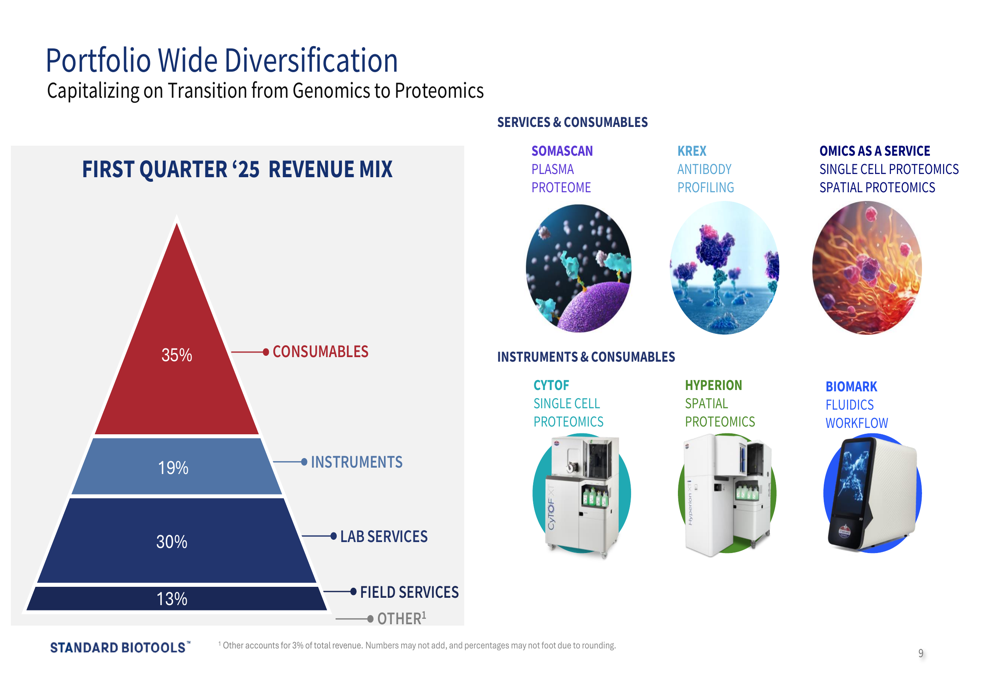

Standard BioTools is diversifying its revenue mix, with a strategic transition from genomics to proteomics:

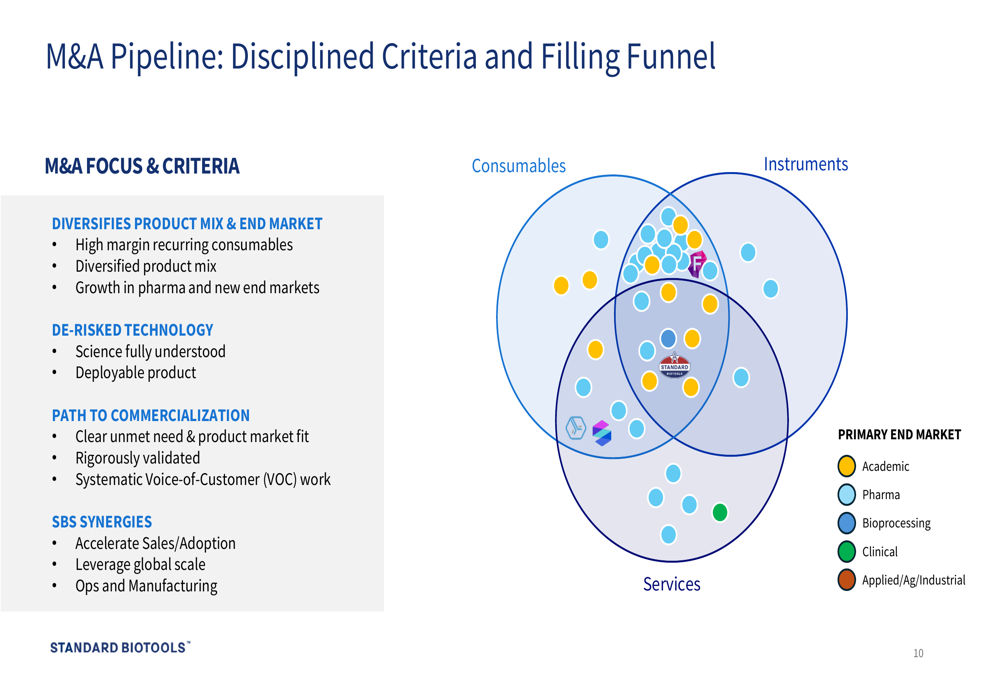

The company is also actively pursuing M&A opportunities with disciplined criteria:

Forward-Looking Statements

Standard BioTools provided revenue guidance of $165-175 million for fiscal year 2025, which represents a flat to slightly down outlook compared to the $175.1 million reported for 2024. The company continues to target adjusted EBITDA breakeven by 2026.

CFO Alex Kim emphasized the company’s strong balance sheet and planned reduction in operating burn through long-term revenue growth, gross margin expansion, and OpEx synergies. The cash runway is expected to fund the business until it reaches adjusted EBITDA positive.

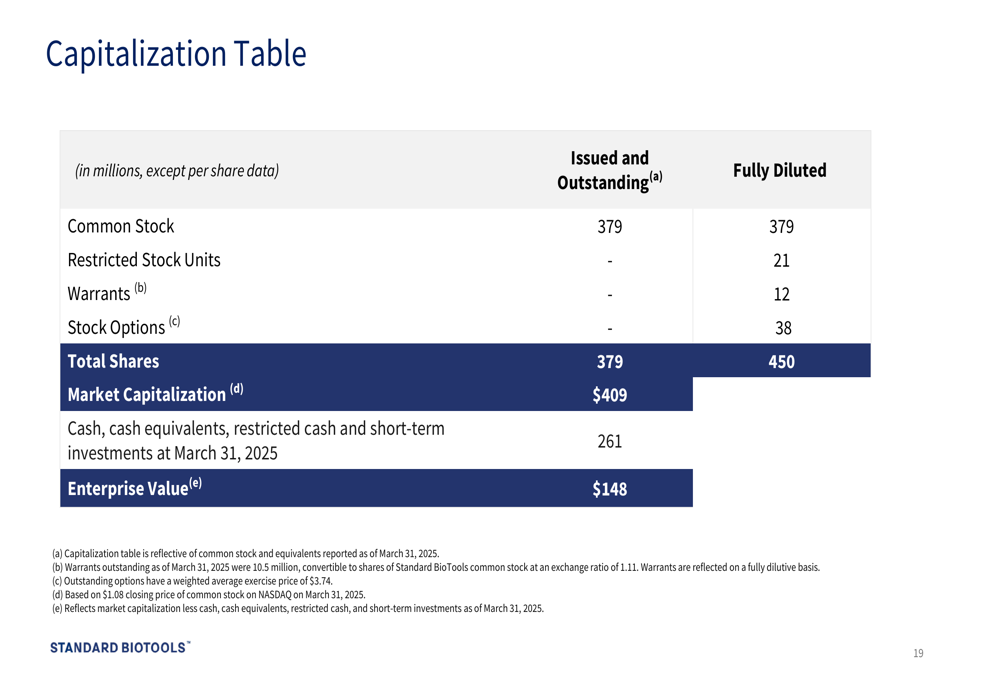

The company’s capitalization structure provides context for its market position:

With a market capitalization of $409 million and an enterprise value of $148 million, Standard BioTools is trading at a significant discount to its cash position of $261 million, reflecting investor caution about the company’s path to profitability despite the progress in cost reductions.

Standard BioTools faces ongoing challenges in a difficult market environment, but its strategic pivot to proteomics, operational efficiency improvements, and strong cash position provide a foundation for its targeted return to profitability. Investors will be watching closely to see if revenue stabilizes and begins to grow in upcoming quarters as the company continues to execute on its strategic initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.