CVS Group profit drops 7.4% as revenue rises on Australia expansion, asset sale

Introduction & Market Context

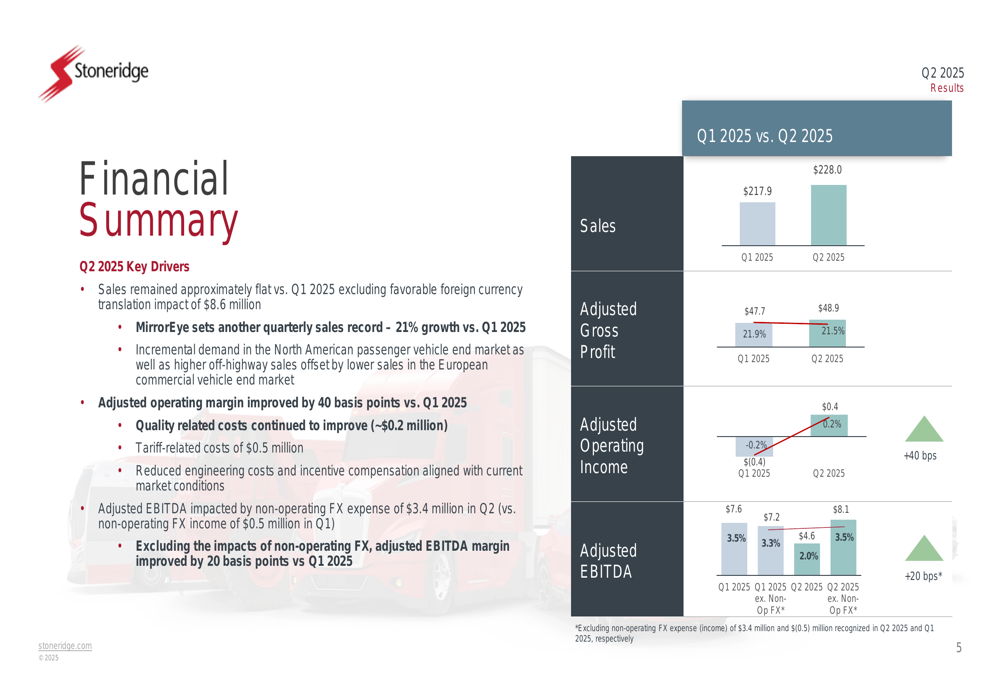

Stoneridge, Inc. (NYSE:SRI) released its Q2 2025 earnings presentation on August 7, 2025, revealing plans to explore strategic alternatives for its Control Devices segment while reporting improved cash flow and significant new business awards. The automotive and commercial vehicle supplier reported sales of $228.0 million, representing 4.6% sequential growth from Q1 2025.

The company’s stock has shown significant recovery in recent months, trading at $7.63 as of August 6, up from $4.84 after its Q1 earnings release when shares surged 25.38%. This continued investor confidence comes as Stoneridge demonstrates operational improvements and strategic focus on its higher-margin electronics business.

Quarterly Performance Highlights

Stoneridge reported Q2 2025 sales of $228.0 million, up 4.6% sequentially from Q1, while adjusted operating income improved to $0.4 million (0.2% margin), a 40 basis point improvement over the previous quarter. Adjusted EBITDA reached $7.6 million (3.3% margin), maintaining stable margins despite significant foreign exchange headwinds.

As shown in the following financial summary, the company’s operational performance improved sequentially despite challenges:

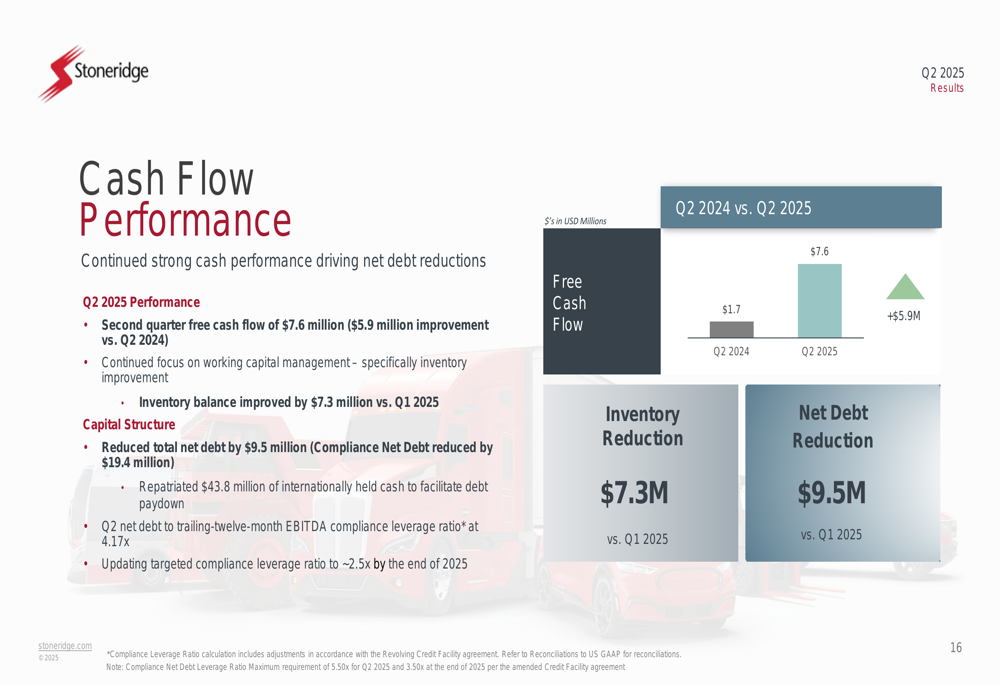

Free cash flow was a particular bright spot at $7.6 million, representing a $5.9 million improvement compared to Q2 2024. This cash generation helped Stoneridge reduce net debt by $9.5 million compared to Q1 2025, with inventory reduction of $7.3 million contributing significantly to working capital improvements.

The company’s cash flow performance demonstrates continued progress in financial stabilization:

Strategic Initiatives

The most significant strategic announcement was Stoneridge’s decision to review strategic alternatives for its Control Devices segment, with a focus on a potential sale. Management indicated this move would allow the company to focus resources on high-technology electronic solutions for commercial vehicle markets while using sale proceeds to improve the balance sheet through debt reduction.

"Reviewing strategic alternatives for Control Devices to maximize the value of each of our businesses," the company stated in its presentation, noting the remaining portfolio would focus on "high-technology electronic solutions for commercial vehicle end markets."

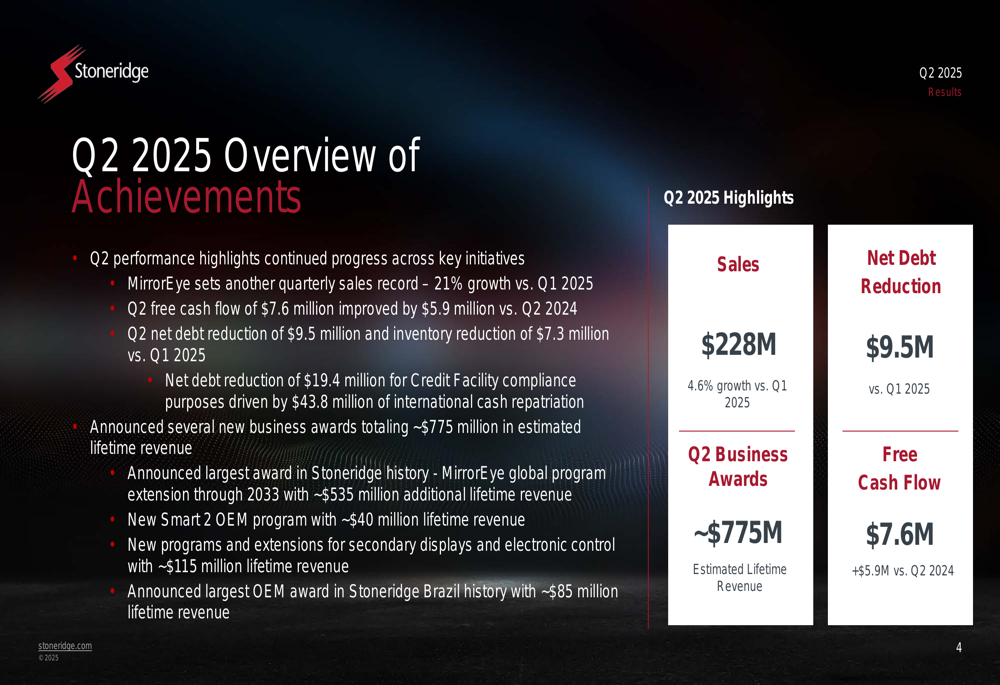

Stoneridge announced approximately $775 million in new business awards during the quarter, including its largest award in company history – a MirrorEye global program extension through 2033 worth approximately $535 million in additional lifetime revenue. The company’s MirrorEye camera-based mirror replacement system continues to gain traction, setting another quarterly sales record with 21% growth compared to Q1 2025.

The following slide highlights the significant MirrorEye program extension:

Other major awards included a new Smart 2 OEM program worth approximately $40 million in lifetime revenue, new programs and extensions for secondary displays and electronic controls worth approximately $115 million, and the largest OEM award in Stoneridge Brazil history worth approximately $85 million in lifetime revenue.

Detailed Financial Analysis

Segment performance showed mixed results across Stoneridge’s three business units. The Control Devices segment, which is now under strategic review, showed improved performance with operating margin expanding 180 basis points to 4.0%, primarily due to manufacturing performance improvements. Sales increased 1.9% sequentially to $71.2 million, driven by higher production volumes in the North American passenger vehicle market.

The Electronics segment, which includes the growing MirrorEye business, reported sales of $149.6 million, relatively in line with Q1 2025 excluding favorable foreign currency translation impacts. While MirrorEye set another quarterly sales record with 21% growth versus Q1, adjusted operating income declined to $4.2 million (2.8% margin) from $6.9 million (4.9% margin) in Q1, primarily due to unfavorable sales mix and higher material costs.

Stoneridge Brazil continued its strong performance with sales of $15.3 million, up 6.0% from Q1 2025, while operating income improved by approximately 230 basis points to 6.3% margin. The company noted that local OEM business in Brazil remains strong, with the segment recently securing its largest OEM award in history.

Forward-Looking Statements

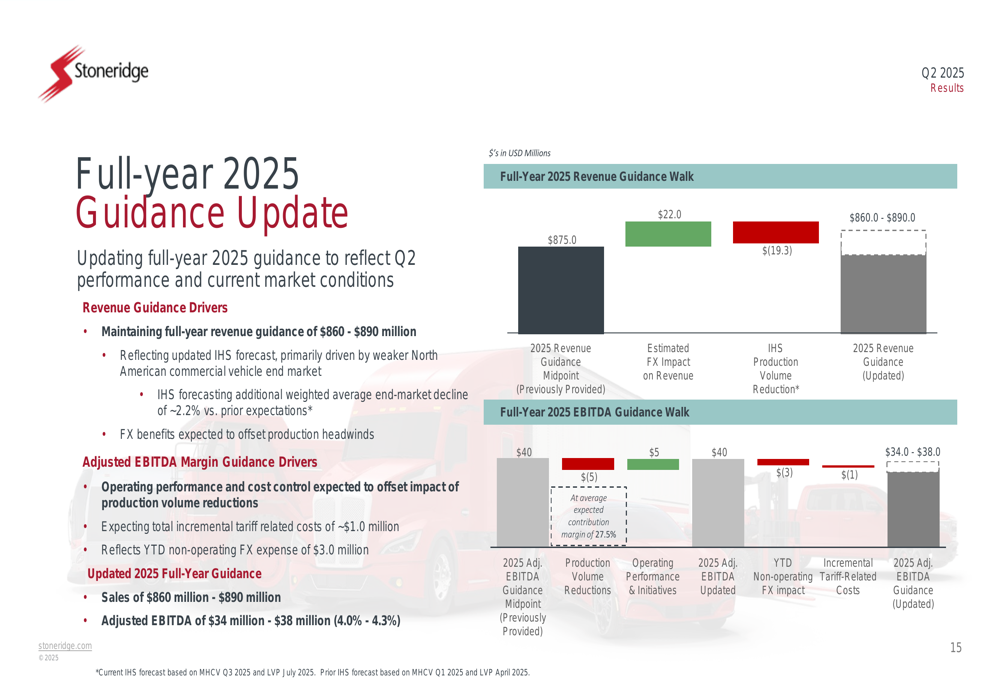

Stoneridge maintained its full-year 2025 revenue guidance of $860-$890 million despite updated IHS forecasts showing an additional weighted average end-market decline of approximately 2.2% versus prior expectations. The company expects foreign exchange benefits to offset production headwinds.

The company updated its adjusted EBITDA guidance to $34-$38 million (4.0%-4.3% margin), reflecting year-to-date non-operating foreign exchange expense of $3.0 million and expected incremental tariff-related costs of approximately $1.0 million. Management expects operating performance and cost control to offset the impact of production volume reductions.

As shown in the following guidance update, Stoneridge is maintaining revenue expectations while adjusting EBITDA projections:

The company is targeting a compliance leverage ratio of approximately 2.5x by the end of 2025, down from the current 4.17x, highlighting its focus on debt reduction. A successful sale of the Control Devices segment would likely accelerate this deleveraging process.

Summary

Stoneridge’s Q2 2025 presentation reveals a company in transition, strategically pivoting toward its higher-growth electronics business while working to improve its financial position through operational improvements and potential portfolio restructuring. The quarter showed meaningful progress in cash flow generation and debt reduction, while significant new business awards – particularly for the MirrorEye product line – provide visibility for future growth.

As summarized in the company’s Q2 overview, Stoneridge achieved several key milestones during the quarter:

The strategic review of the Control Devices segment represents a potentially transformative move that could accelerate Stoneridge’s evolution into a more focused, higher-margin business while strengthening its balance sheet. Investors will be watching closely for updates on this process, as well as continued execution on operational improvements and new business wins in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.