Softbank Group Q2 profit blows past expectations; sells Nvidia stake for $5.8 bln

Introduction & Market Context

StrongPoint ASA (OB:STRO) presented its second quarter 2025 results on July 11, showing continued revenue growth and improved profitability as the retail technology provider expands its footprint across European grocery markets. The company’s stock closed at NOK 11.60 on July 10, down 0.85% ahead of the earnings presentation, but remains well above its 52-week low of NOK 8.60.

The retail technology specialist, which serves grocery retailers across Europe with solutions ranging from e-commerce fulfillment to cash handling systems, reported solid growth figures despite acknowledging slower-than-anticipated progress in some areas. With approximately 500 employees and operations in 9 core countries, StrongPoint continues to position itself as a key technology partner for grocery retailers seeking efficiency improvements.

Quarterly Performance Highlights

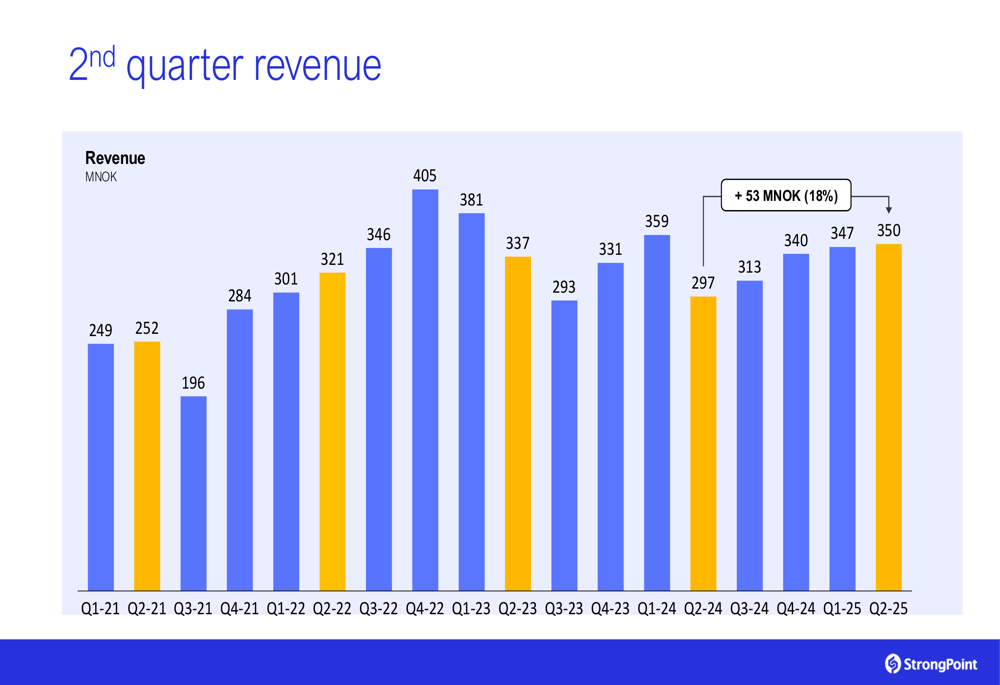

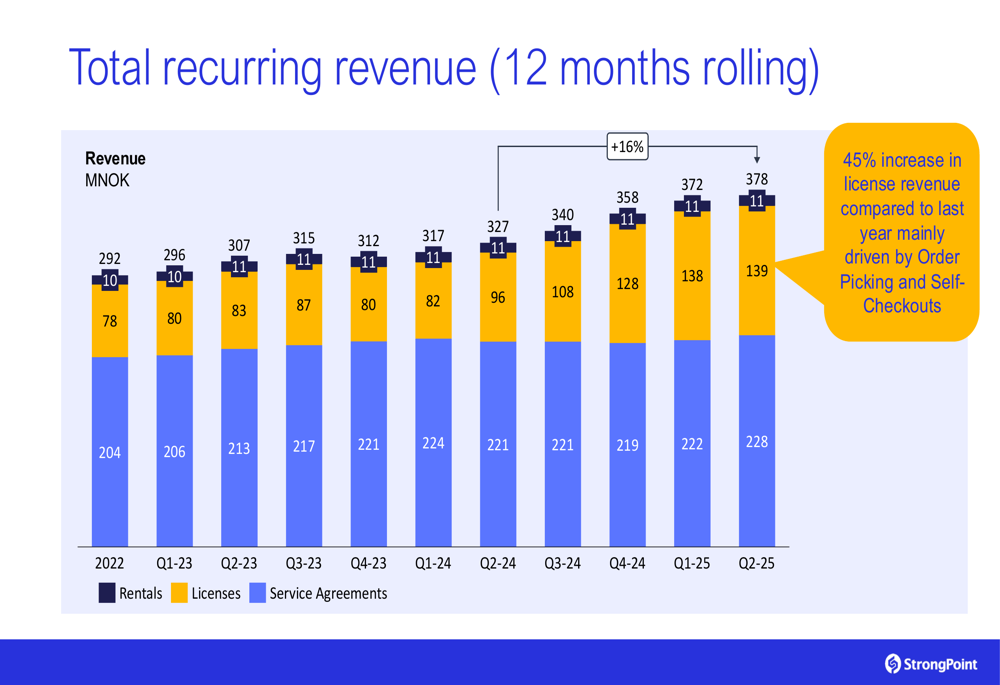

StrongPoint reported Q2 2025 revenue of NOK 350 million, representing an 18% increase compared to the same period last year. The company’s recurring revenue reached NOK 378 million on a rolling 12-month basis, up 16% year-over-year, with license revenue showing particularly strong growth of 45% driven by Order Picking and Self-Checkout solutions.

As shown in the following chart of quarterly revenue growth, StrongPoint has maintained a positive trajectory since Q2 2024:

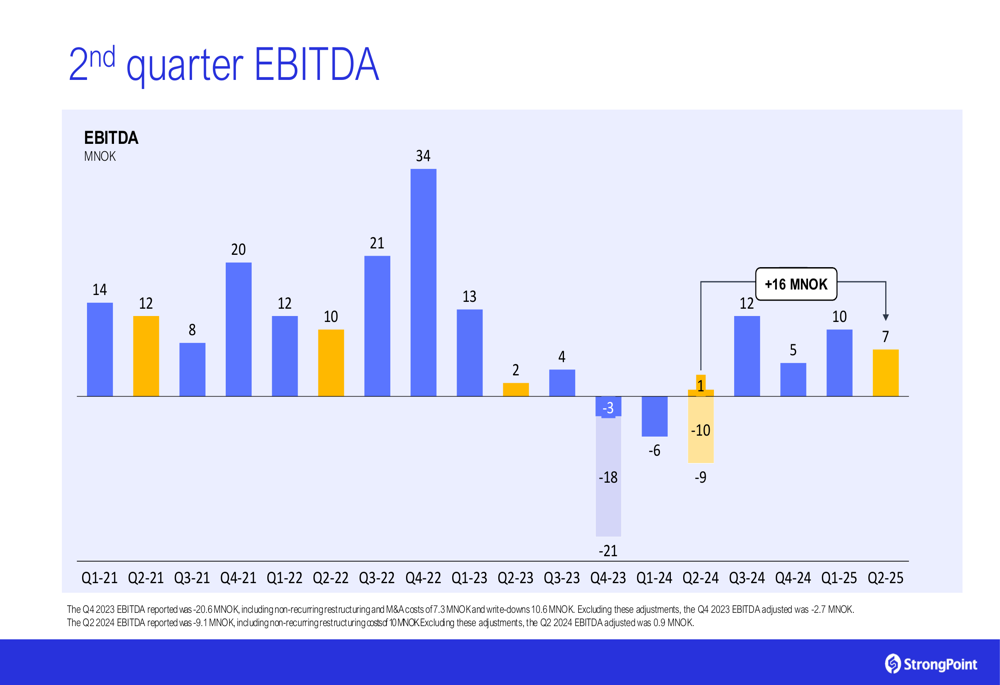

EBITDA for the quarter came in at NOK 7 million (2.1% margin), a significant improvement from the adjusted EBITDA of NOK 0.9 million in Q2 2024. The company noted that Q2 2024 reported EBITDA was negative NOK 9.1 million, which included NOK 10 million in non-recurring restructuring costs.

The EBITDA trend over recent quarters shows the company’s improving profitability profile:

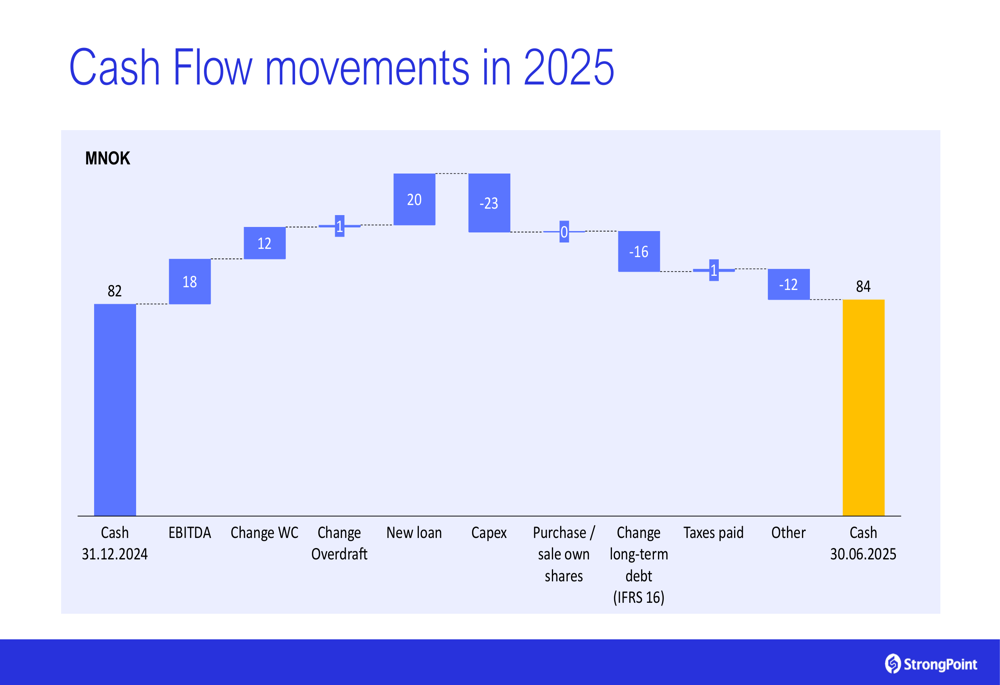

Cash flow from operations was positive at NOK 20 million, contributing to a stable financial position with disposable funds of NOK 84 million at the end of the quarter. Net interest-bearing debt stood at NOK 74 million, a slight increase from NOK 72 million in the previous quarter.

The company’s cash flow movements for 2025 show the balance between operational cash generation, capital expenditures, and financing activities:

Strategic Initiatives & Customer Wins

StrongPoint highlighted several significant customer wins during the quarter, reinforcing its position in the retail technology market. Carrefour (EPA:CARR) Belgium selected StrongPoint’s Order Picking solution for scheduled deliveries following a competitive RFP process, with implementation already underway and expected to be completed within months.

Additionally, a Nordic grocery retailer placed an order worth NOK 21 million for AI-powered weighing scales from StrongPoint partner DIGI. These scales feature instant product recognition technology to improve speed and accuracy for in-store customers. COOP Estonia also ordered 130 self-checkouts, continuing a long-standing partnership with StrongPoint.

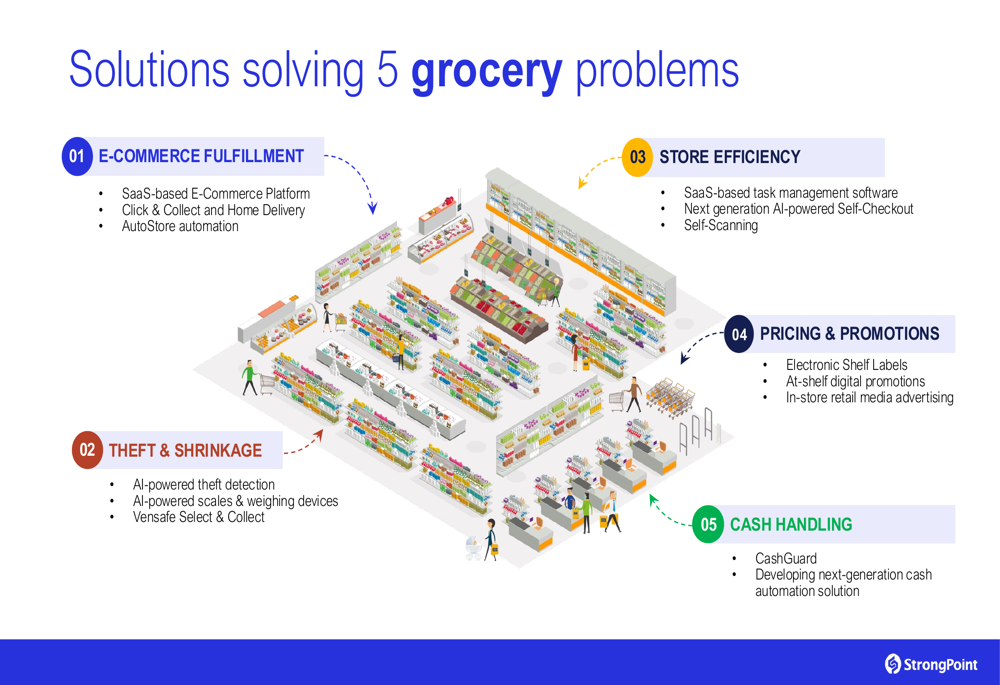

The company’s comprehensive solution portfolio addresses five key grocery retail challenges, as illustrated in this overview:

StrongPoint also provided updates on ongoing strategic projects. The Sainsbury (LON:SBRY)’s Order Picking solution rollout is planned for completion by summer 2026, with some stores going live before Christmas 2025 and regional training centers launching in early Q1 2026. The company’s next-generation CashGuard Connect solution is currently being tested in stores with real customers, with additional units being prepared for multi-checkout testing.

Financial Analysis

StrongPoint’s recurring revenue continues to be a key focus area, with service agreements, licenses, and rentals contributing to a stable revenue base. The composition of recurring revenue shows the growing importance of license revenue, which now accounts for a significant portion of the total:

Working capital management remains an area of attention, with inventory levels increasing by NOK 33 million in 2025, partially offset by changes in accounts receivable, accounts payable, and other current items. The company’s net interest-bearing debt has fluctuated over recent quarters but remains manageable at NOK 74 million:

Comparing to Q1 2025 results, StrongPoint has maintained revenue momentum with a slight increase from NOK 347 million to NOK 350 million quarter-over-quarter. However, EBITDA decreased from NOK 10 million in Q1 to NOK 7 million in Q2, suggesting some pressure on margins despite the revenue growth.

Forward-Looking Statements

StrongPoint’s outlook indicates continued improvement in EBITDA and recurring revenue, although management acknowledged this progress is slower than anticipated. For the long term, the company expects core fundamentals to strengthen, particularly with global SaaS E-Commerce opportunities.

The company maintains its target of healthy revenue growth and an EBITDA margin exceeding 10%, though no specific timeline was provided for achieving these goals. This represents a slight moderation of expectations compared to previous guidance, reflecting a more cautious approach to near-term performance projections.

StrongPoint’s comprehensive approach to retail technology, illustrated in this company overview, continues to be the foundation of its growth strategy:

With its expanding customer base and growing recurring revenue streams, StrongPoint appears well-positioned to capitalize on the ongoing digital transformation in retail, despite acknowledging some challenges in the pace of improvement. Investors will be watching closely to see if the company can accelerate its EBITDA margin expansion in coming quarters while maintaining its revenue growth momentum.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.