Hedge funds are buying these two big tech stocks while selling two rivals

Introduction & Market Context

Sun Life Financial Inc (NYSE:SLF) released its third quarter 2025 presentation on November 6, showcasing a 3% year-over-year increase in underlying net income to $1.047 billion, despite facing headwinds in certain business segments. The company's stock fell 3.65% to $61.43 in premarket trading despite beating earnings expectations, with reported EPS of $1.86 surpassing the forecast of $1.82.

The global financial services organization highlighted its diversified business model and strong capital position as key factors in delivering consistent shareholder value. With $1.62 trillion in assets under management and operations in 28 markets worldwide, Sun Life continues to leverage its scale while pursuing strategic growth initiatives.

Quarterly Performance Highlights

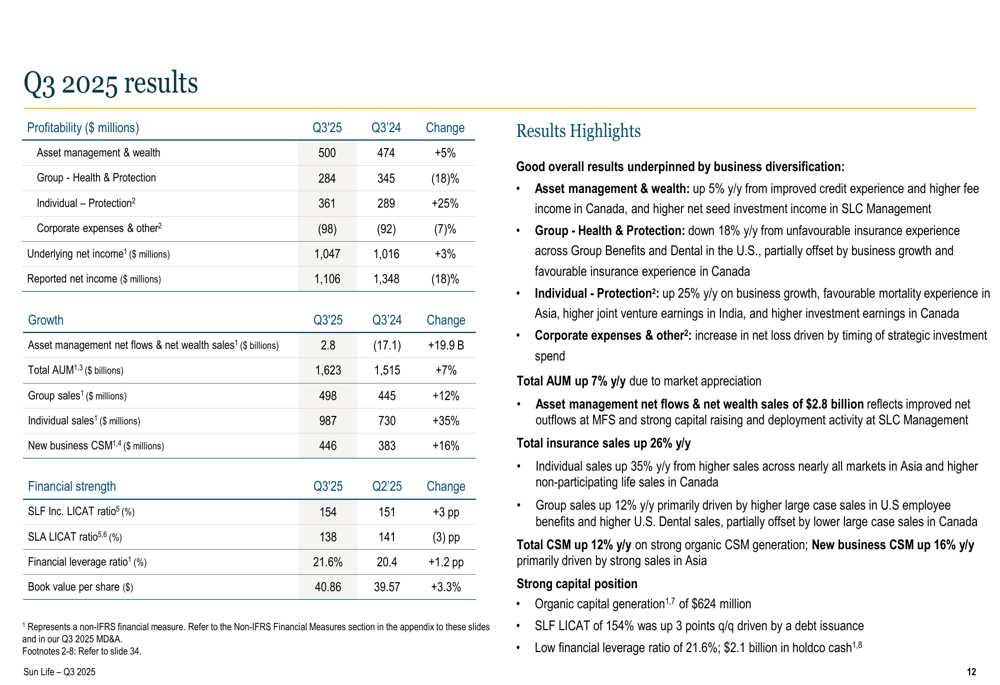

Sun Life's Q3 2025 results demonstrated the company's resilience amid varying performance across business segments. Underlying net income reached $1.047 billion, up 3% from the previous year, while reported net income declined 18% to $1.106 billion.

As shown in the following detailed financial breakdown:

The company's performance was led by strong growth in Individual Protection, which saw profits increase by 25% year-over-year. Asset Management & Wealth also performed well with a 5% profit increase. However, these gains were partially offset by an 18% decline in the Group - Health & Protection segment, which executives attributed to rising US healthcare costs and utilization challenges in the Medicaid dental market during the earnings call.

Total assets under management grew to $1.623 trillion, representing a 7% increase, while asset management net flows and net wealth sales reached $2.8 billion, a substantial improvement from the previous year.

Business Segment Analysis

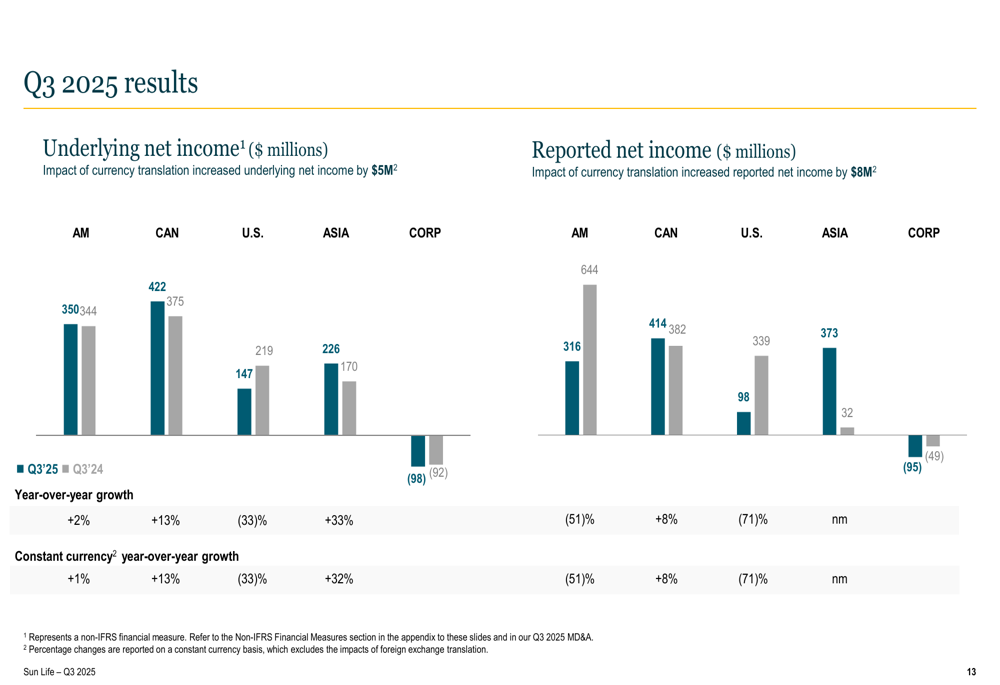

Sun Life's presentation provided a detailed breakdown of performance by region, highlighting the company's global diversification:

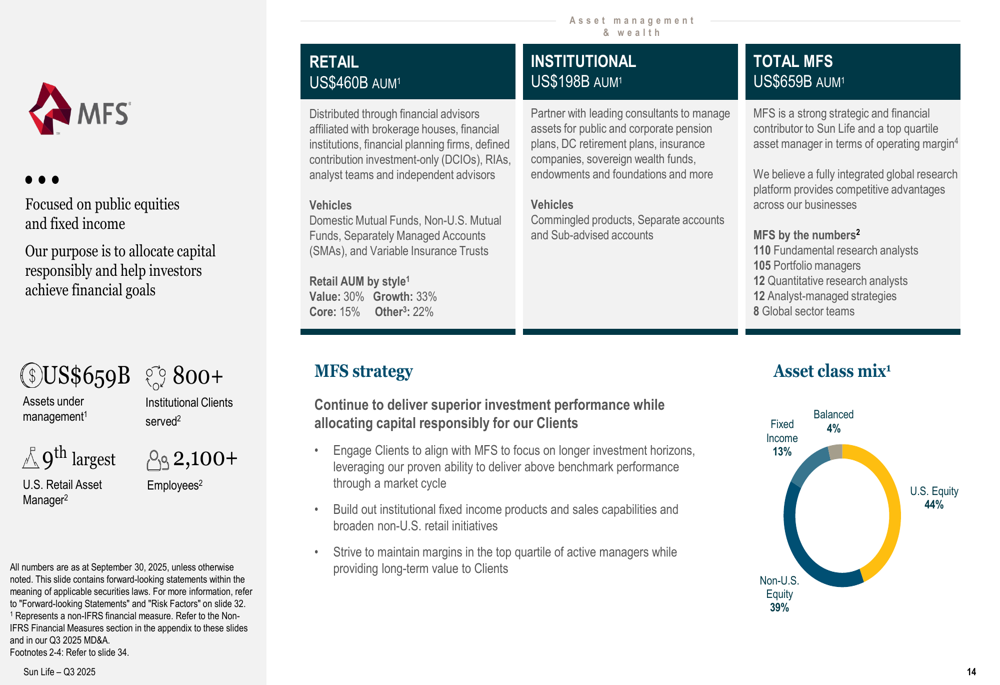

The Asset Management segment, which includes MFS and SLC Management, continues to be a significant contributor to Sun Life's earnings. MFS, with $659 billion in assets under management, serves over 800 institutional clients globally:

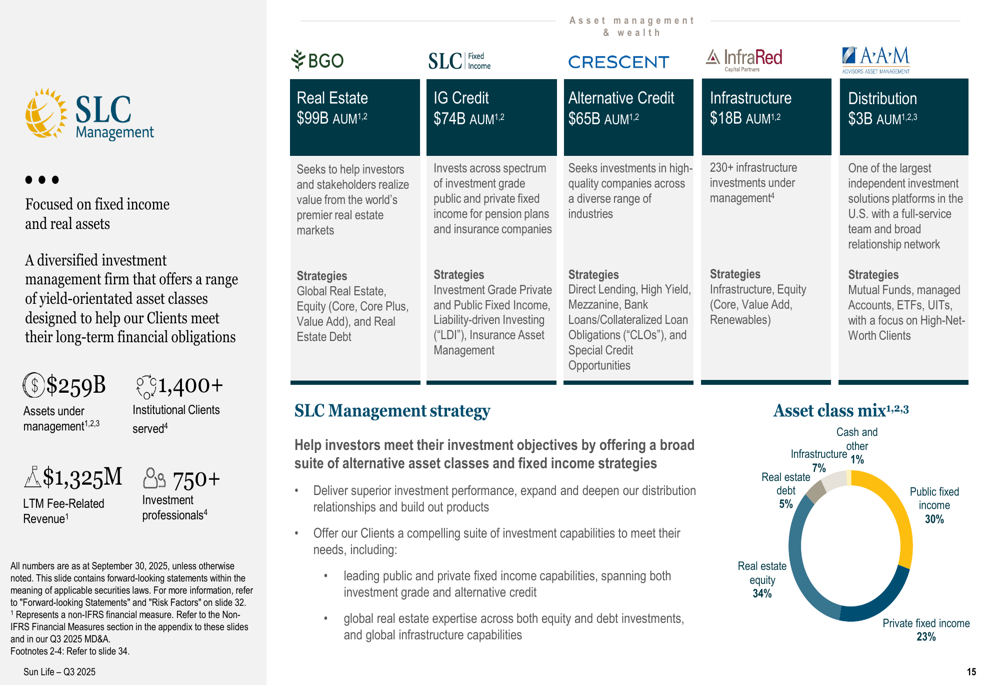

Meanwhile, SLC Management is growing as a premier alternatives platform with $259 billion in assets under management across real estate, infrastructure, and credit investments:

The Canadian business remains the largest contributor to underlying net income, while Asia continues to show strong growth potential with operations in eight markets serving over 30 million clients. The US business, despite facing challenges in healthcare costs, maintains a strong position in the employee benefits market.

Capital Position and Shareholder Returns

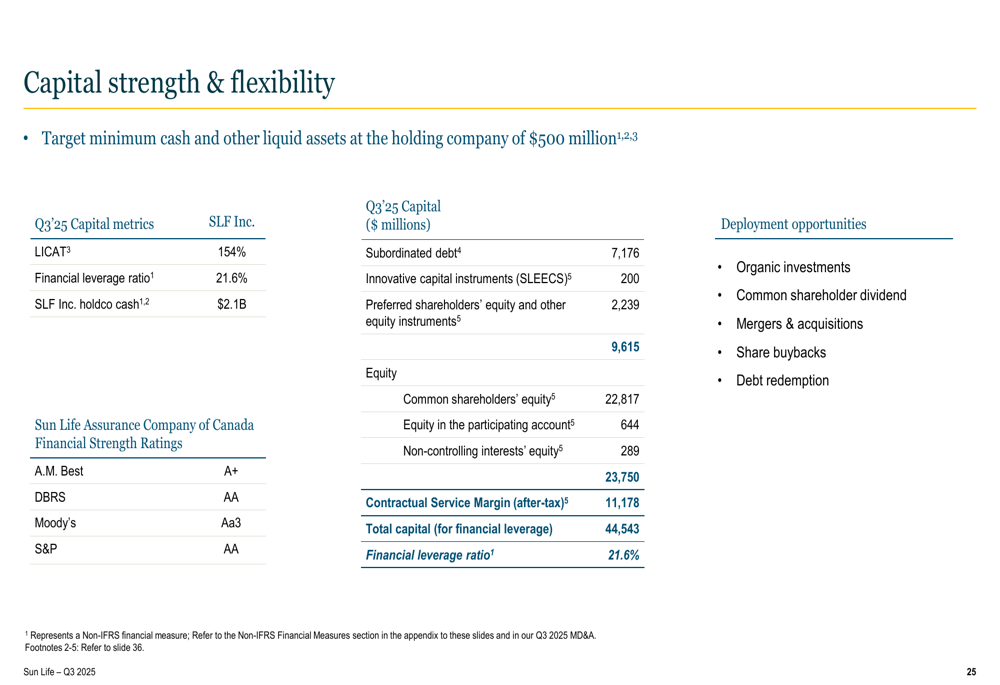

Sun Life maintained a robust capital position in Q3 2025, with a Life Insurance Capital Adequacy Test (LICAT) ratio of 154%, up 3 percentage points quarter-over-quarter. The company's financial leverage ratio stood at 21.6%, with $2.1 billion in holding company cash providing significant flexibility for capital deployment.

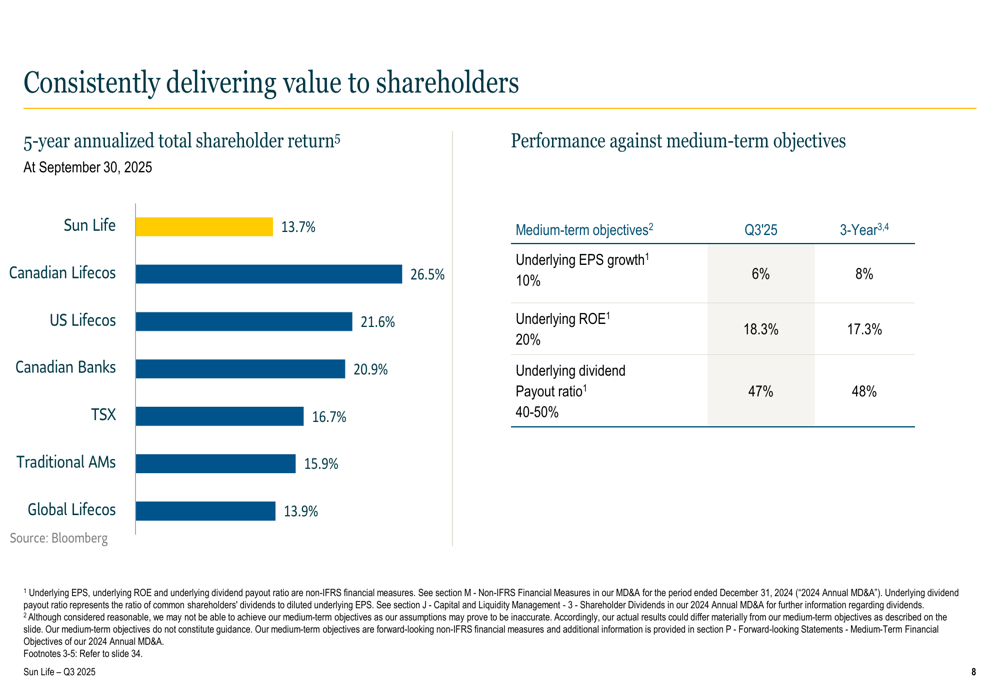

The company has consistently delivered value to shareholders, outperforming several peer groups in terms of 5-year annualized total shareholder return:

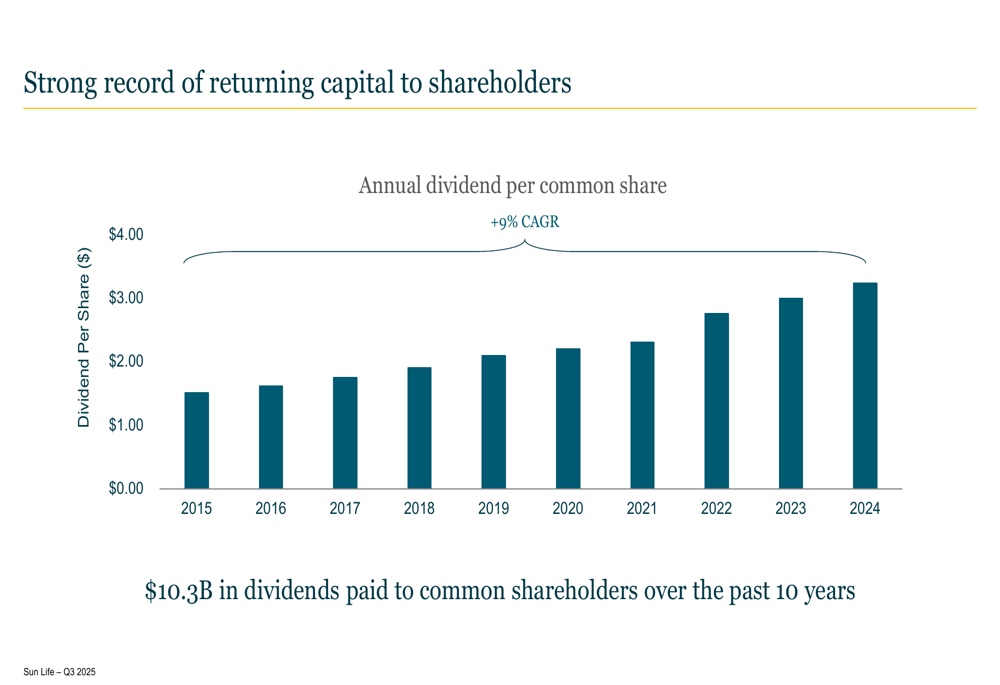

Sun Life has also maintained a strong track record of returning capital to shareholders through dividends, with the most recent quarterly dividend increased by 4.5% to $0.92 per share. This continues the company's pattern of consistent dividend growth:

Strategic Initiatives and Outlook

Sun Life's presentation emphasized four strategic imperatives: leveraging asset management capabilities, accelerating momentum in Asia, deepening impact along the client's health journey, and operating like a digital company.

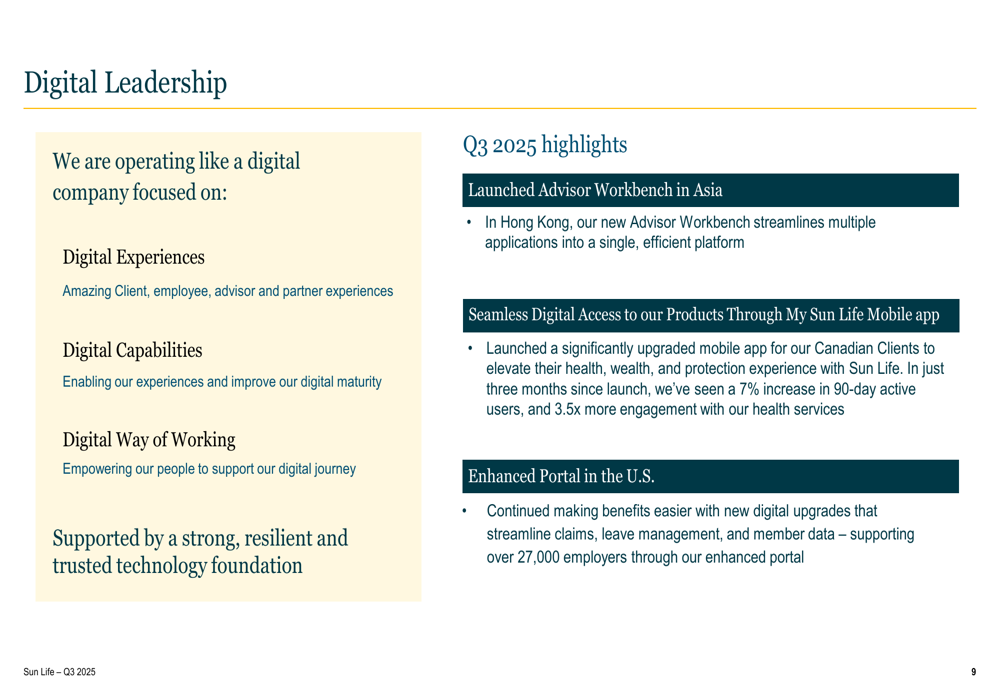

The company highlighted its digital transformation efforts, including the launch of the Advisor Workbench in Asia and enhancements to the My Sun Life Mobile app:

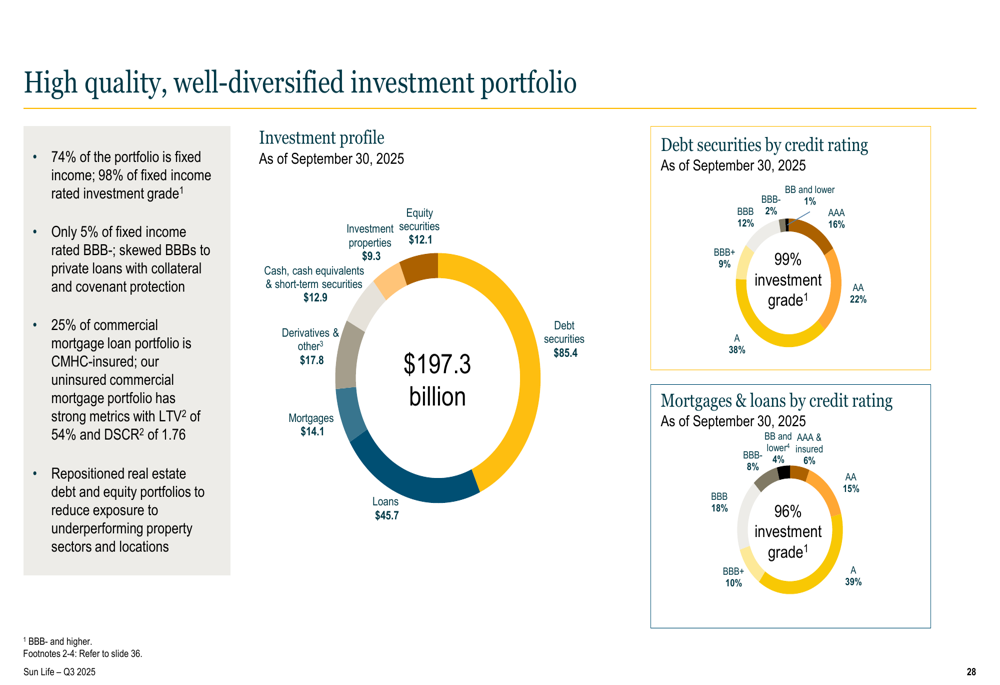

Sun Life's investment portfolio remains high-quality and well-diversified, with 74% in fixed income assets, of which 98% are rated investment grade. This conservative approach positions the company well for potential market volatility:

Looking ahead, Sun Life remains committed to its medium-term objectives, targeting 10% underlying EPS growth and 20% underlying ROE, though current performance (6% and 18.3% respectively) falls slightly short of these targets. The company is preparing for a $2 billion transaction in early 2026 and continues to focus on strategic acquisitions that align with its growth priorities.

Despite the positive earnings results and strong fundamentals, investors appeared cautious, perhaps reflecting concerns about the challenges in the US healthcare segment and broader market conditions. Nevertheless, Sun Life's diversified business model and strong capital position provide a solid foundation for navigating these challenges while pursuing long-term growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.