German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

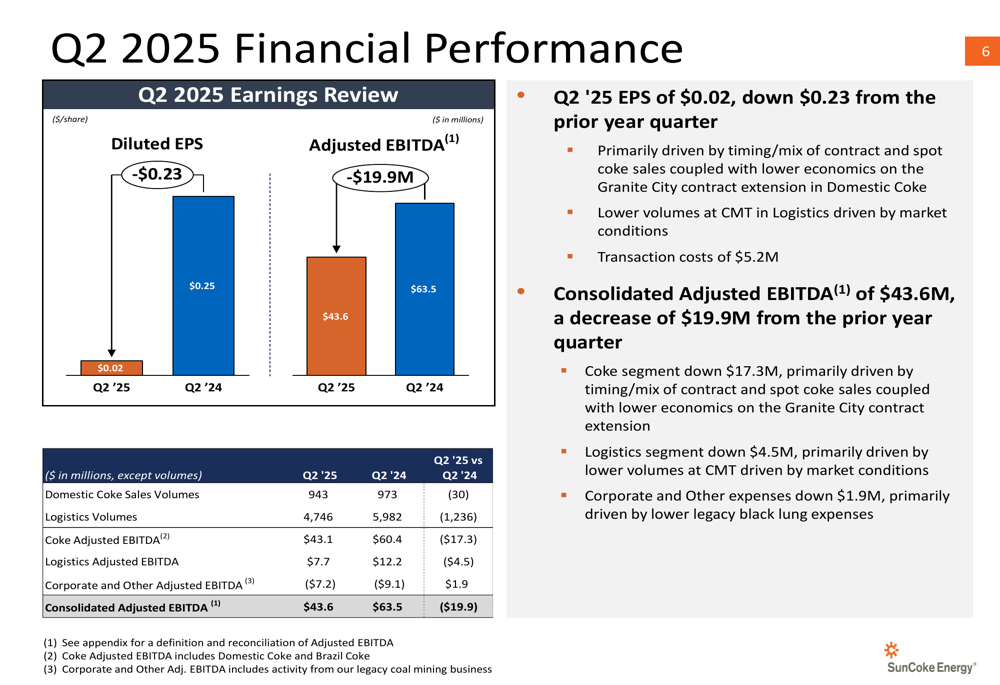

SunCoke Energy Inc . (NYSE:SXC) reported a sharp decline in second-quarter earnings while simultaneously announcing a significant acquisition aimed at diversifying its business. The company’s Q2 2025 earnings per share plummeted to $0.02, down $0.23 from the prior year quarter, while consolidated adjusted EBITDA fell to $43.6 million from $63.5 million in Q2 2024.

This performance deterioration follows a first quarter that had already shown signs of weakness, with Q1 2025 EPS of $0.20 representing a $0.03 year-over-year decline. Despite beating analyst expectations in Q1, SunCoke’s stock has remained under pressure, trading at $8.28 as of July 29, 2025, well below its 52-week high of $12.82.

Quarterly Performance Highlights

SunCoke’s second quarter results revealed significant challenges across its business segments. The company attributed the earnings decline primarily to timing and mix of contract and spot coke sales, lower economics on the Granite City contract extension, and reduced volumes at its logistics terminals.

As shown in the following detailed financial performance breakdown:

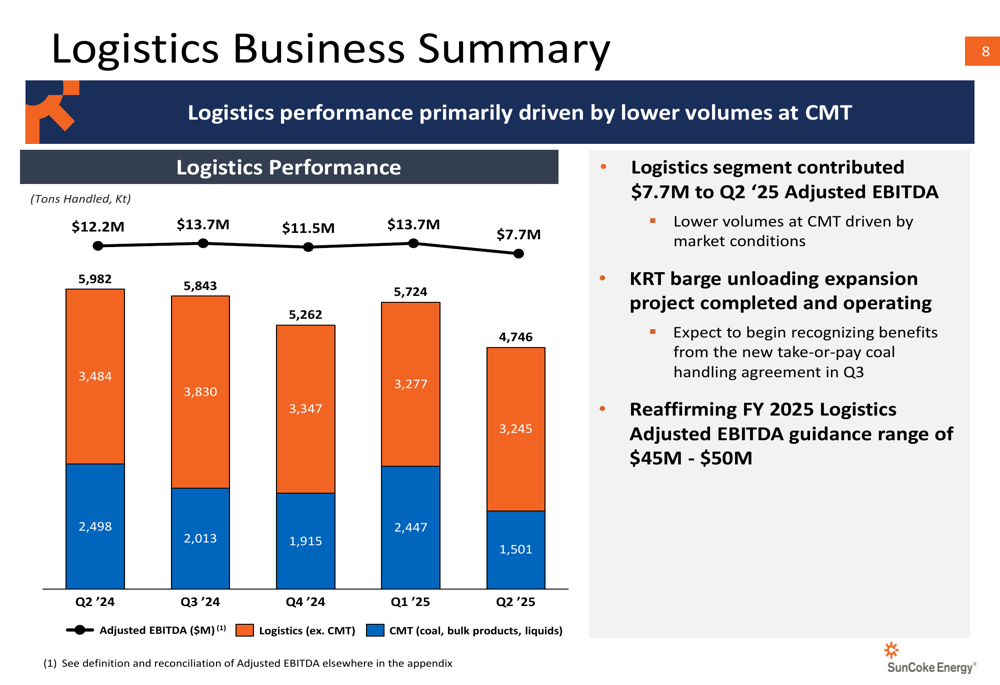

The domestic coke segment was particularly hard hit, with adjusted EBITDA falling to $43.1 million from $60.4 million in the prior year quarter. This decline was driven by a shift in sales mix at Haverhill toward lower-margin spot sales and reduced economics from the Granite City contract extension. Logistics segment adjusted EBITDA also declined to $7.7 million from $12.2 million, primarily due to lower volumes at the company’s Convent Marine Terminal (CMT).

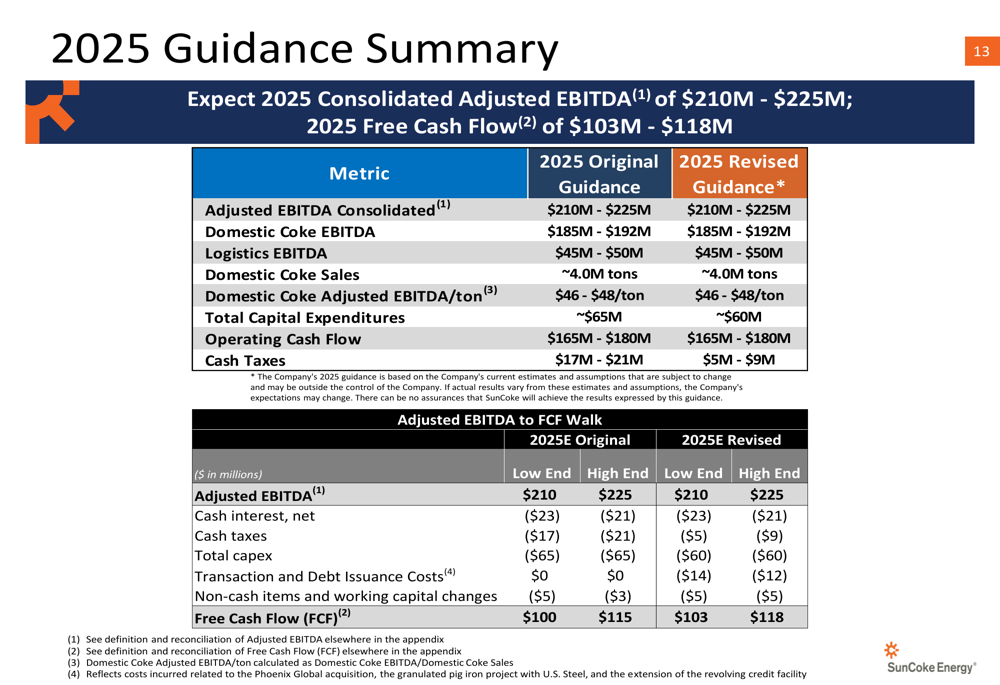

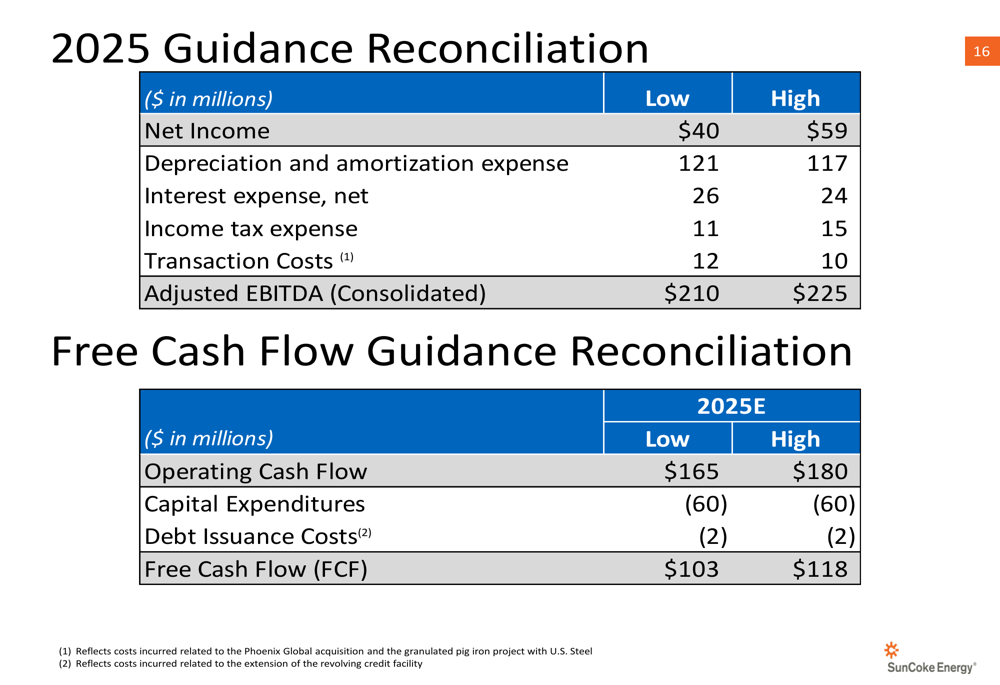

Despite these challenges, SunCoke maintained its quarterly dividend of $0.12 per share, payable on September 2, 2025, and reaffirmed its full-year 2025 consolidated adjusted EBITDA guidance range of $210 million to $225 million.

Strategic Initiatives

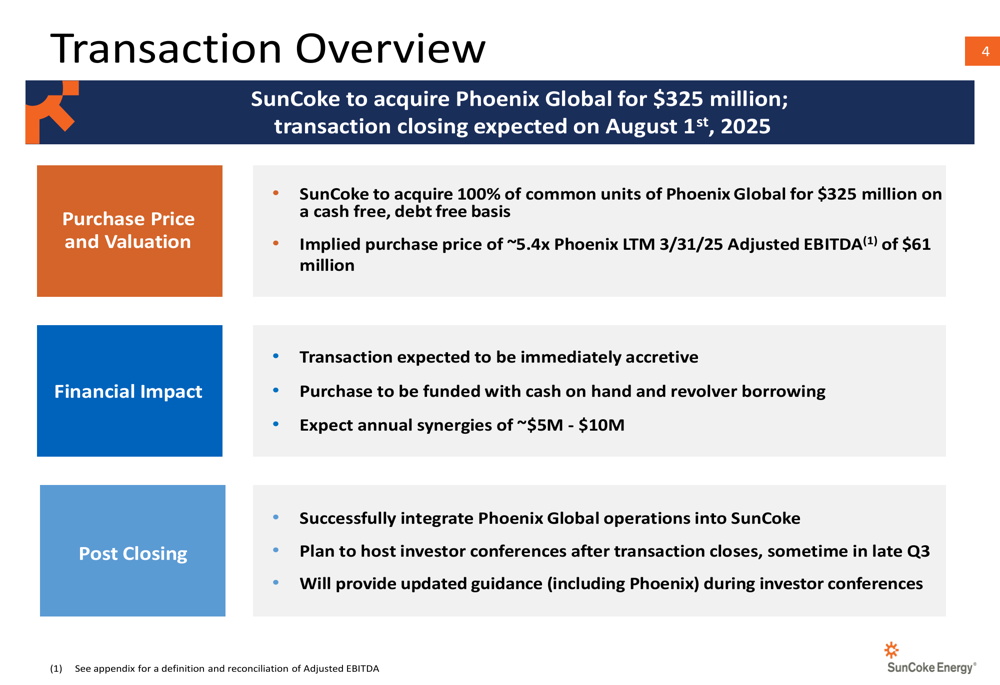

The centerpiece of SunCoke’s strategic initiatives is the announced acquisition of Phoenix Global for $325 million, expected to close on August 1, 2025. This transaction represents a significant pivot for the company as it seeks to diversify beyond its traditional coke-making operations.

The acquisition details and valuation metrics are outlined in the following slide:

At approximately 5.4 times Phoenix’s last twelve months adjusted EBITDA of $61 million, the acquisition is expected to be immediately accretive. SunCoke plans to fund the purchase with a combination of cash on hand and revolver borrowing, while targeting annual synergies of $5-10 million.

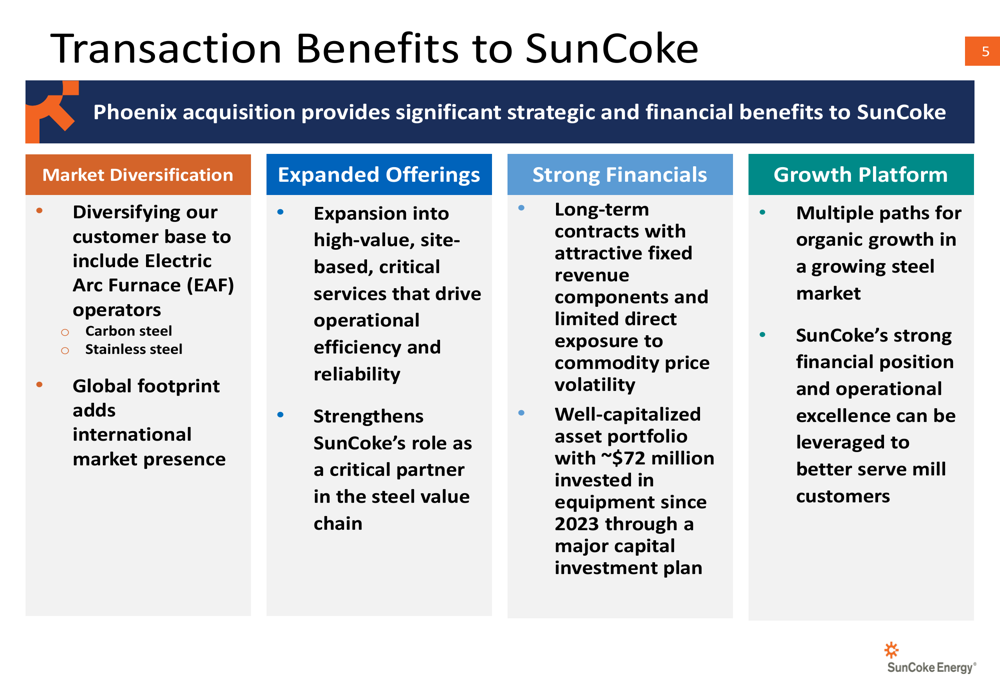

The company highlighted several strategic benefits from the Phoenix acquisition:

Key benefits include diversification into serving Electric Arc Furnace (EAF) operators in both carbon and stainless steel production, expansion into international markets, and the addition of high-value, site-based critical services. The acquisition also brings long-term contracts with attractive fixed revenue components and limited direct exposure to commodity price volatility.

Detailed Financial Analysis

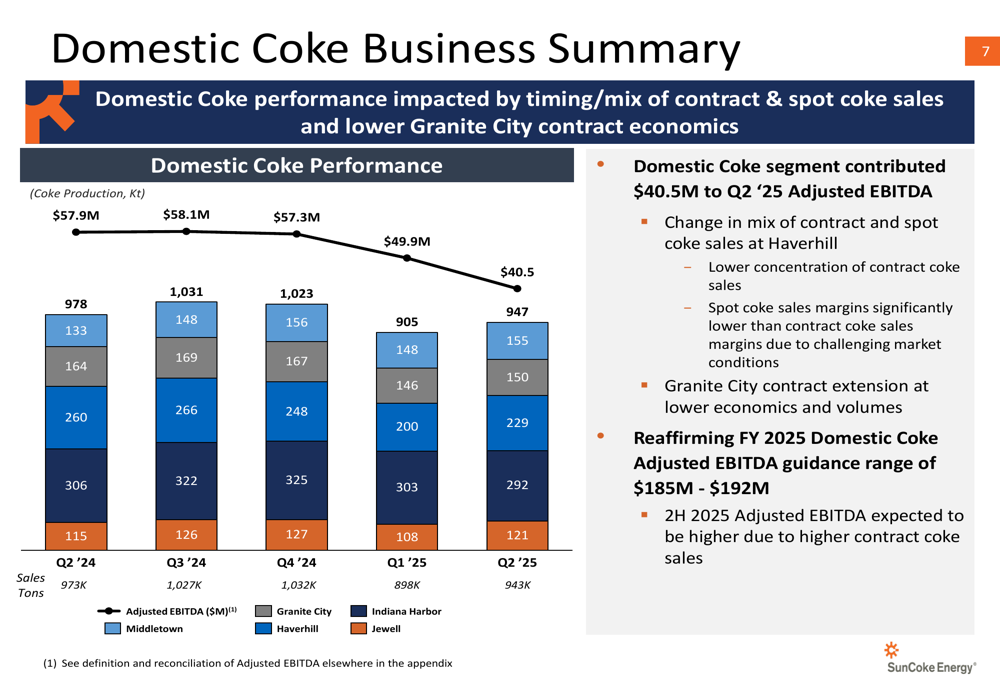

SunCoke’s domestic coke business, traditionally its core revenue generator, showed significant weakness in Q2 2025:

Production volumes across facilities remained relatively stable compared to previous quarters, but the segment’s adjusted EBITDA fell to $40.5 million in Q2 2025. The company cited a change in mix of contract and spot coke sales at Haverhill, with spot coke sales margins significantly lower than contract sales due to challenging market conditions. Additionally, the Granite City contract extension was secured at lower economics and volumes.

The logistics segment also faced headwinds:

Logistics volumes declined to 4,746 thousand tons in Q2 2025 from 5,982 thousand tons in Q2 2024, primarily due to lower throughput at the Convent Marine Terminal. The company did highlight the completion of the KRT barge unloading expansion project, which is expected to begin generating benefits in Q3 from a new take-or-pay coal handling agreement.

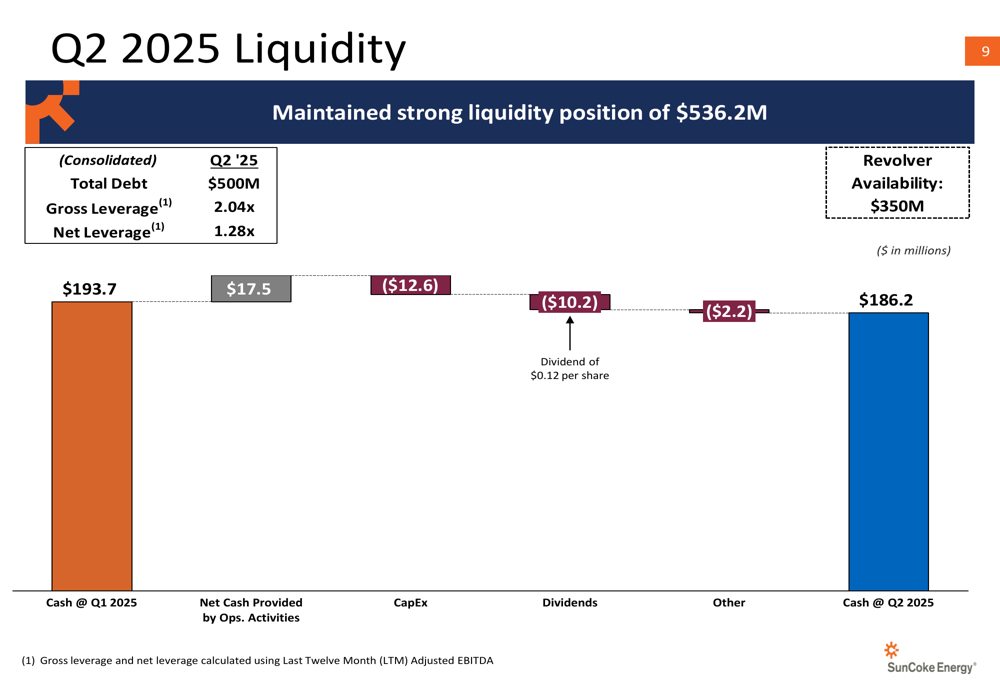

Despite operational challenges, SunCoke maintained a strong liquidity position:

The company ended Q2 with $186.2 million in cash and $350 million in revolver availability, for total liquidity of $536.2 million. Total (EPA:TTEF) debt remained at $500 million, resulting in gross leverage of 2.04x and net leverage of 1.28x based on last twelve months adjusted EBITDA.

Forward-Looking Statements

Despite the significant drop in Q2 performance, SunCoke reaffirmed its full-year 2025 guidance:

The company maintained its consolidated adjusted EBITDA guidance range of $210-225 million and free cash flow projection of $103-118 million. This suggests management expects a significant improvement in the second half of 2025, potentially driven by higher contract coke sales and contributions from the Phoenix acquisition.

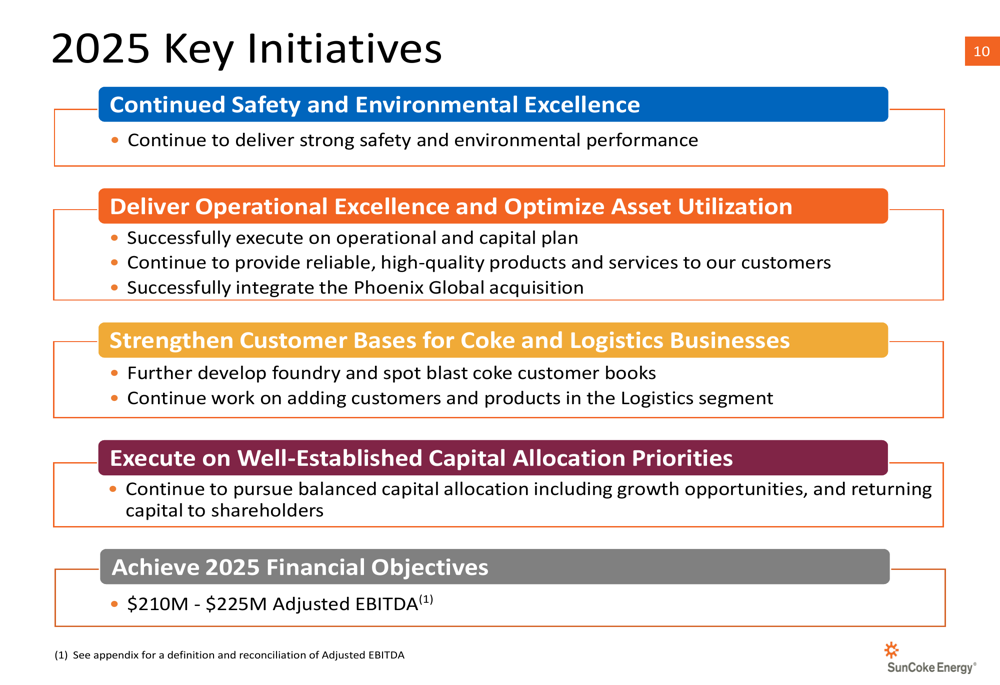

SunCoke outlined several key initiatives for the remainder of 2025:

These initiatives include continued safety and environmental excellence, operational optimization, strengthening customer bases for both coke and logistics businesses, balanced capital allocation, and achieving the company’s financial objectives.

The guidance reconciliation provides additional insight into how SunCoke expects to achieve its full-year targets:

With net income projected between $40-59 million for the full year, the company will need to significantly improve performance in the second half to reach these targets, given that first-half net income totaled just $22.9 million.

In conclusion, SunCoke Energy’s Q2 2025 results reveal a company at a strategic inflection point. While core business performance has deteriorated significantly, management is betting on diversification through the Phoenix Global acquisition to strengthen its position in the steel value chain and reduce dependency on traditional blast furnace customers. Investors will be watching closely to see if this strategic pivot can deliver the projected second-half improvement needed to meet full-year guidance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.