TSX slides as gold price drops

Introduction & Market Context

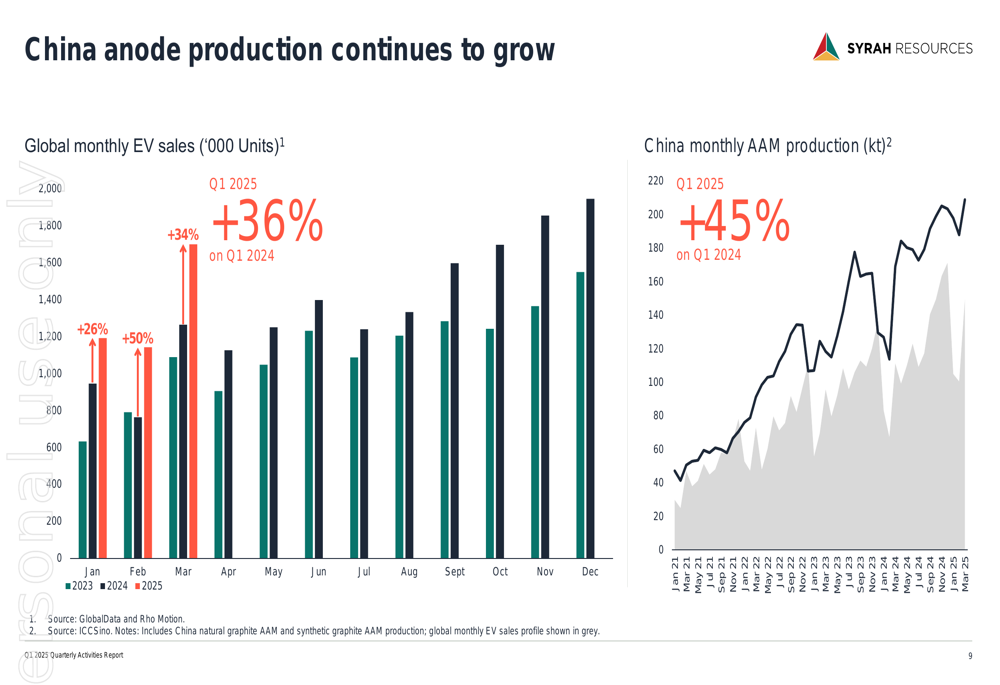

Syrah Resources Ltd (ASX:SYR) released its Q1 2025 quarterly activities report on April 29, highlighting a challenging period marked by zero production at its Balama graphite operation in Mozambique due to protest actions. Despite these operational challenges, the company pointed to positive market dynamics with global EV sales increasing 36% year-over-year in Q1 2025.

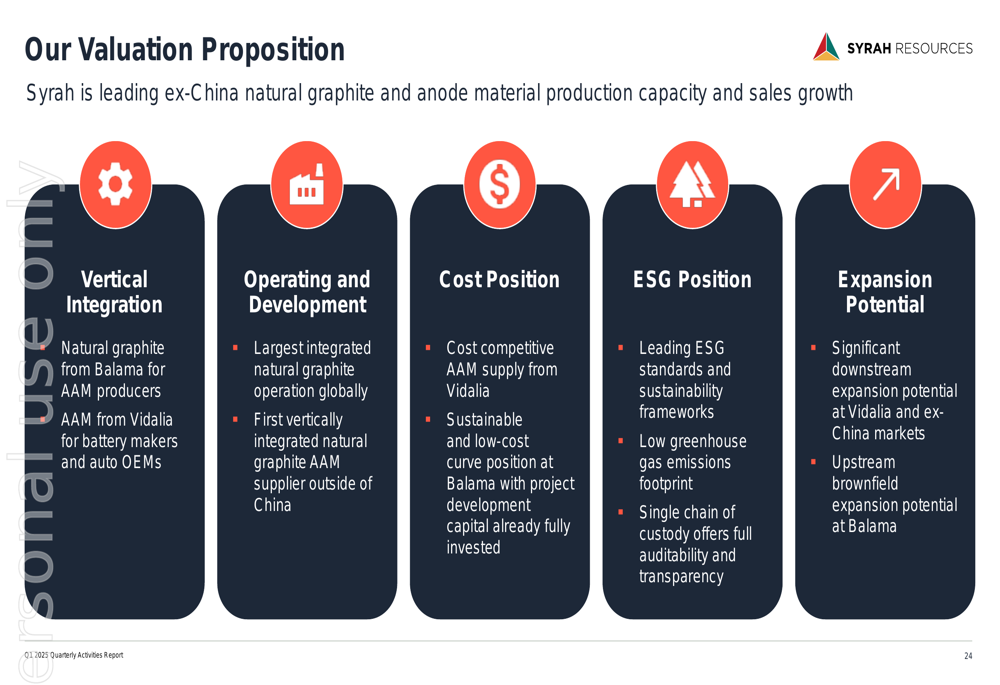

As the only operating vertically integrated natural graphite active anode material (AAM) supplier outside of China, Syrah continues to position itself strategically in a market where natural graphite and AAM demand is expected to increase two and four times, respectively, over the next decade.

Quarterly Performance Highlights

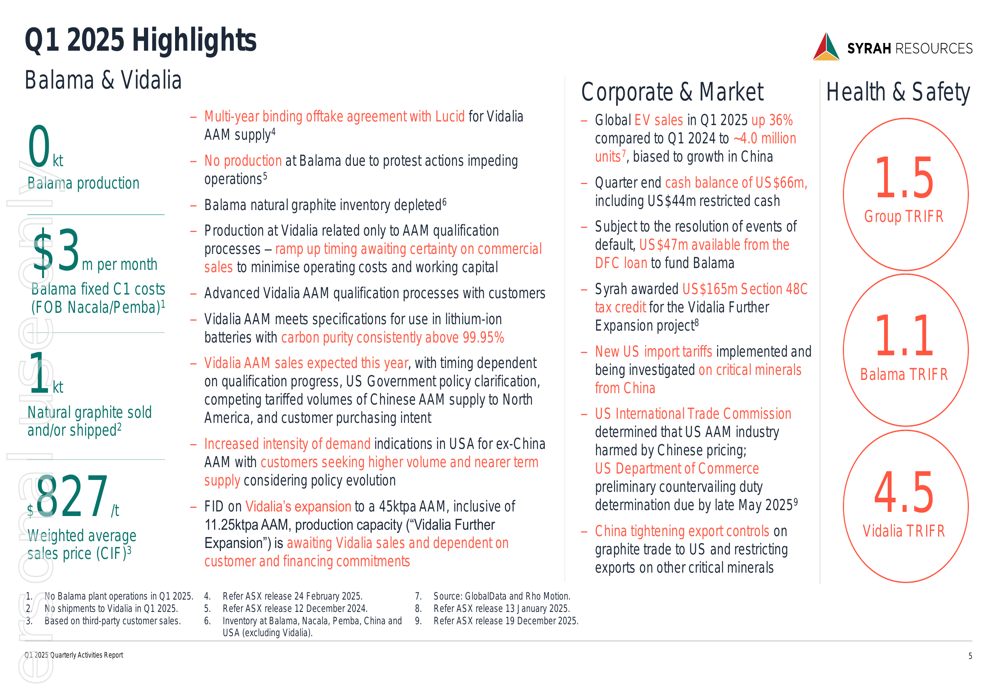

The first quarter of 2025 presented significant challenges for Syrah, with the most notable being the complete halt of production at its Balama facility. Key performance metrics include:

- Balama production: 0kt

- Balama fixed C1 costs: $3 million per month

- Natural graphite sold/shipped: 1kt

- Weighted average sales price: $827/t

- Quarter-end cash balance: US$66 million

The company also reported securing a multi-year binding offtake agreement with Lucid (NASDAQ:LCID) for Vidalia AAM supply, while maintaining strong safety performance with a Group Total (EPA:TTEF) Recordable Injury Frequency Rate (TRIFR) of 1.5.

Balama Operations and Restart Plans

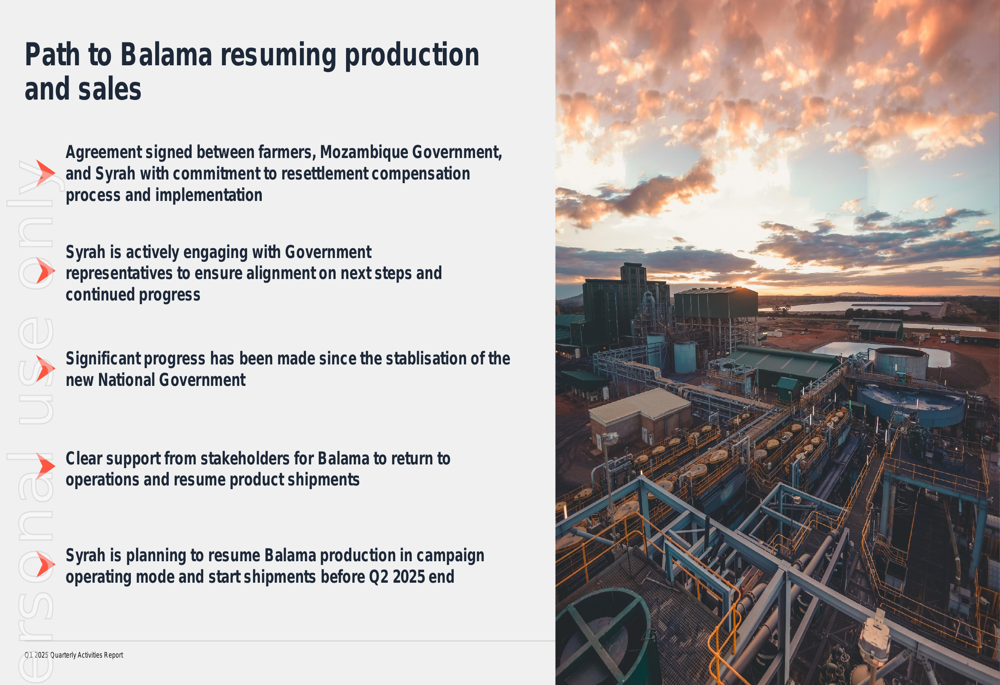

The complete production stoppage at Balama has depleted Syrah’s natural graphite inventory, creating urgency around restarting operations. According to the presentation, the company has made significant progress toward resuming activities:

- An agreement has been signed between farmers, the Mozambique Government, and Syrah

- Active engagement with Government representatives continues

- Significant progress has been made since the stabilization of the new National Government

- Clear support from stakeholders has been established

Syrah plans to resume Balama production in campaign operating mode and start shipments before the end of Q2 2025, which would mark a critical turning point for the company’s cash flow.

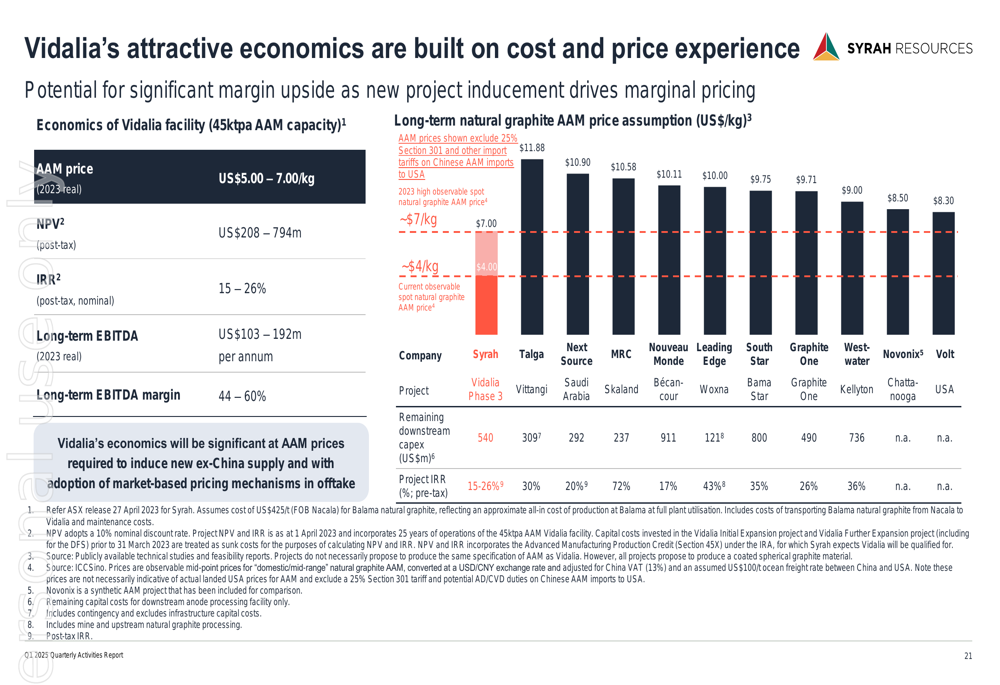

Vidalia Facility and Strategic Positioning

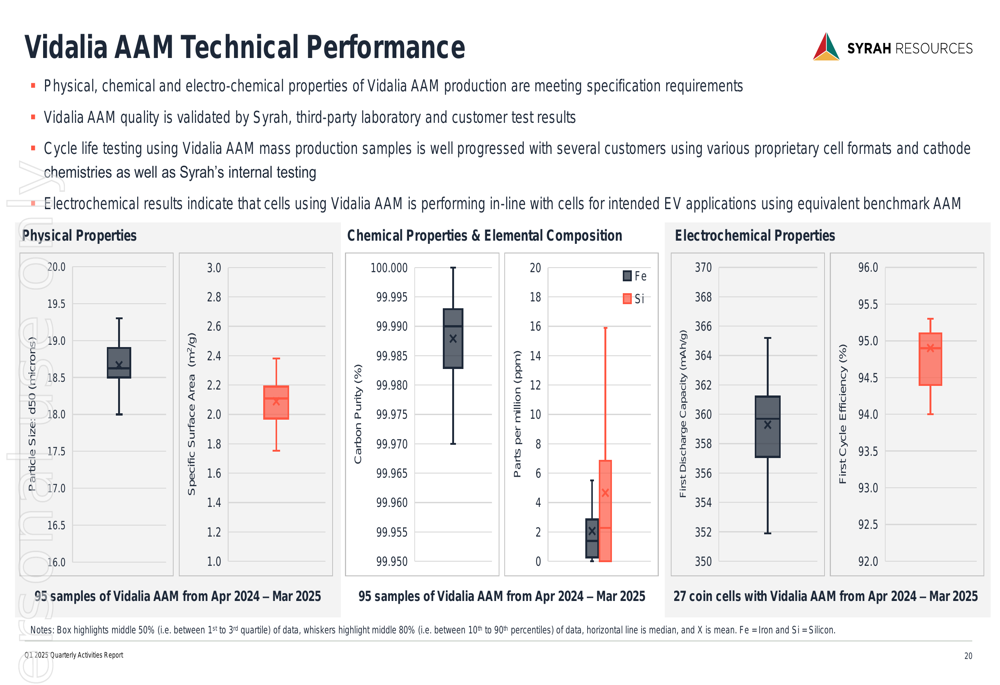

While Balama operations were halted, Syrah continued to emphasize the strategic importance of its Vidalia AAM facility in the United States. The company reported that Vidalia AAM consistently meets lithium-ion battery specifications with carbon purity above 99.95%.

The technical performance data presented shows that Vidalia’s product meets or exceeds industry standards across physical properties, chemical composition, and electrochemical performance metrics, positioning it as a competitive alternative to Chinese suppliers.

Syrah is positioning Vidalia as the cornerstone of its downstream business, with current production capacity of 11.25ktpa and plans to expand to 45ktpa by 2028. The company highlighted that Vidalia’s economics are expected to be favorable at AAM prices required for new ex-China supply.

Financial Analysis

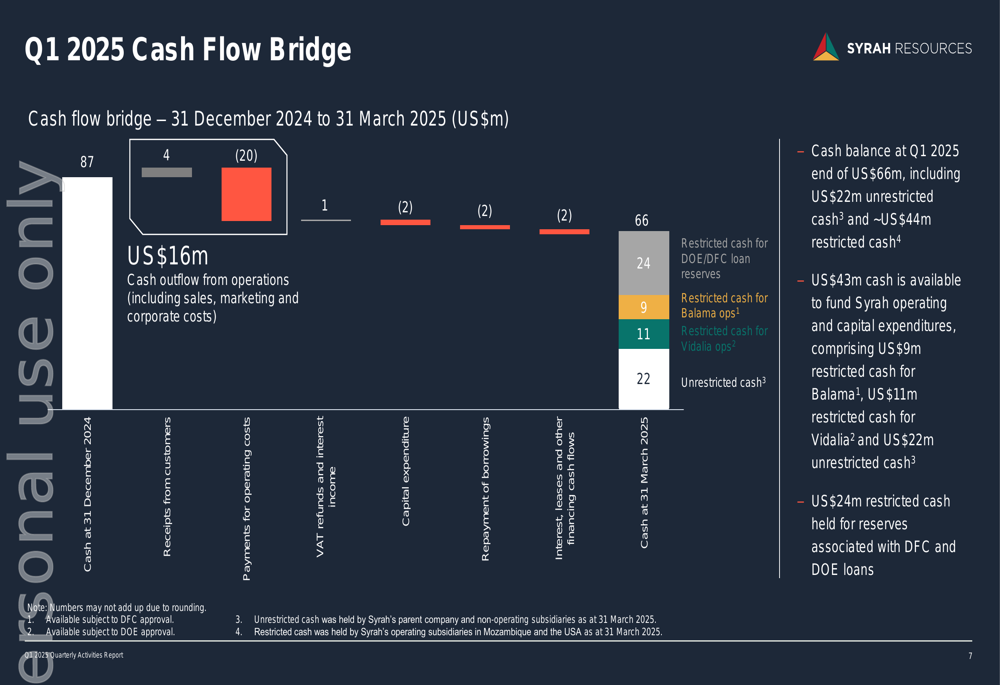

The first quarter saw Syrah’s cash position decline from $87 million on December 31, 2024, to $66 million by March 31, 2025. This cash burn reflects the ongoing fixed costs at Balama despite zero production, alongside continued investments in Vidalia.

The cash flow bridge reveals that of the $66 million end-of-quarter balance, only $22 million is unrestricted cash, with the remainder allocated to specific reserves:

- $24 million restricted for DOE/DFC loan reserves

- $9 million restricted for Balama operations

- $11 million restricted for Vidalia operations

Cash outflow from operations (including sales, marketing, and corporate costs) totaled $16 million for the quarter, highlighting the financial pressure on the company during the production halt.

Market Outlook and Competitive Position

Despite operational challenges, Syrah emphasized several positive market trends supporting its long-term strategy. Global EV sales increased 36% year-over-year in Q1 2025, while China’s AAM production grew 45% compared to Q1 2024.

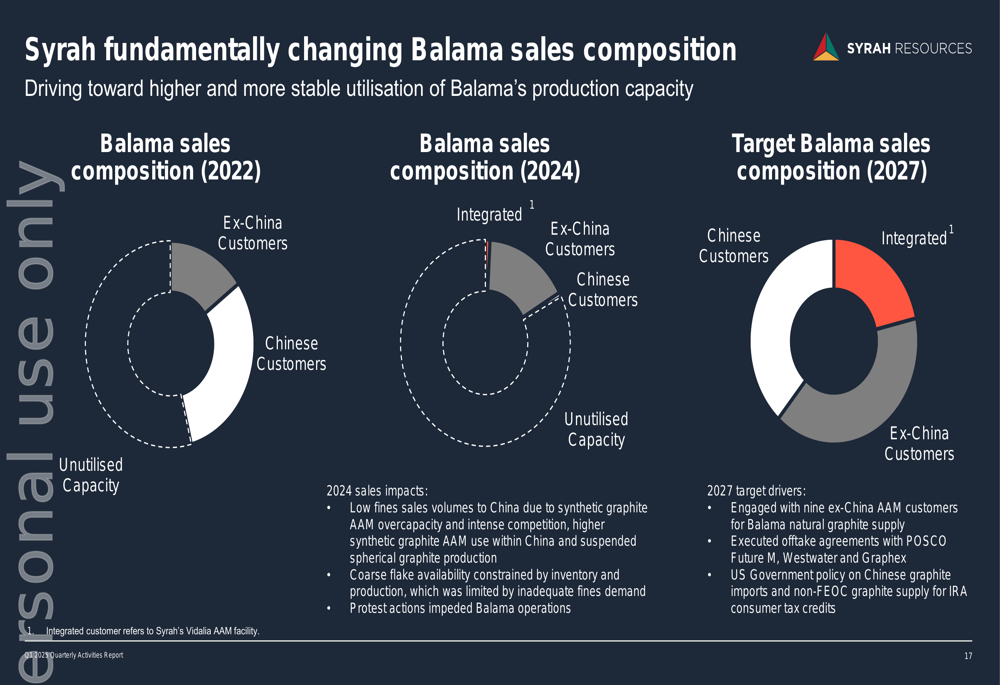

However, the company also acknowledged market headwinds, including increasing Chinese graphite exports and declining export prices. This competitive pressure comes as Syrah attempts to shift its Balama sales composition away from Chinese customers toward ex-China markets.

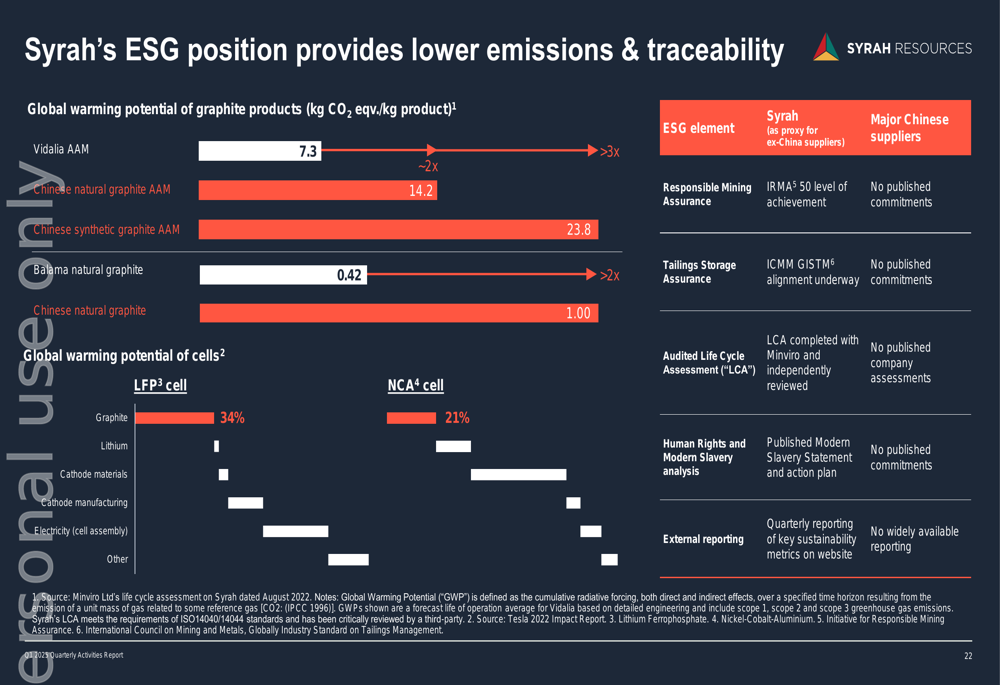

Syrah highlighted its environmental advantages, noting that Vidalia AAM has a global warming potential (GWP) of 7.3, significantly lower than Chinese graphite, while Balama natural graphite has an even lower GWP of 0.42. These ESG credentials could provide competitive differentiation in Western markets increasingly focused on sustainability.

The company’s presentation emphasized its unique value proposition as a vertically integrated supplier with leading ESG standards and significant expansion potential, particularly as governments in the US and other Western markets implement policies to reduce dependence on Chinese battery materials.

As Syrah works to restart Balama operations and ramp up Vidalia production, the coming quarters will be critical in determining whether the company can successfully navigate the challenging market dynamics while managing its cash position.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.