Raymond James raises Fulgent Genetics stock price target to $36 on strong performance

Introduction & Market Context

Targa Resources Inc. (NYSE:TRGP) presented its third quarter 2025 earnings on November 5, showcasing significant growth across its midstream operations. The company’s stock responded positively to the results, rising 6.67% to close at $164.88, after gaining 1.73% in pre-market trading.

The midstream energy infrastructure company, which connects natural gas and NGL supplies to domestic and international markets, demonstrated continued momentum in its Permian Basin operations, driving substantial increases in both financial and operational metrics.

Quarterly Performance Highlights

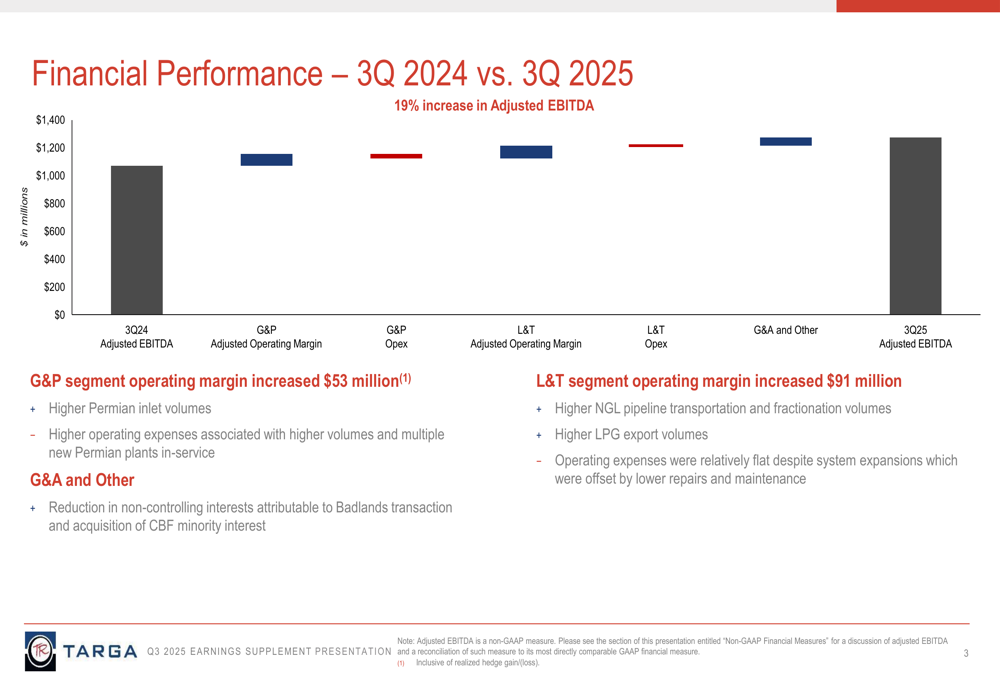

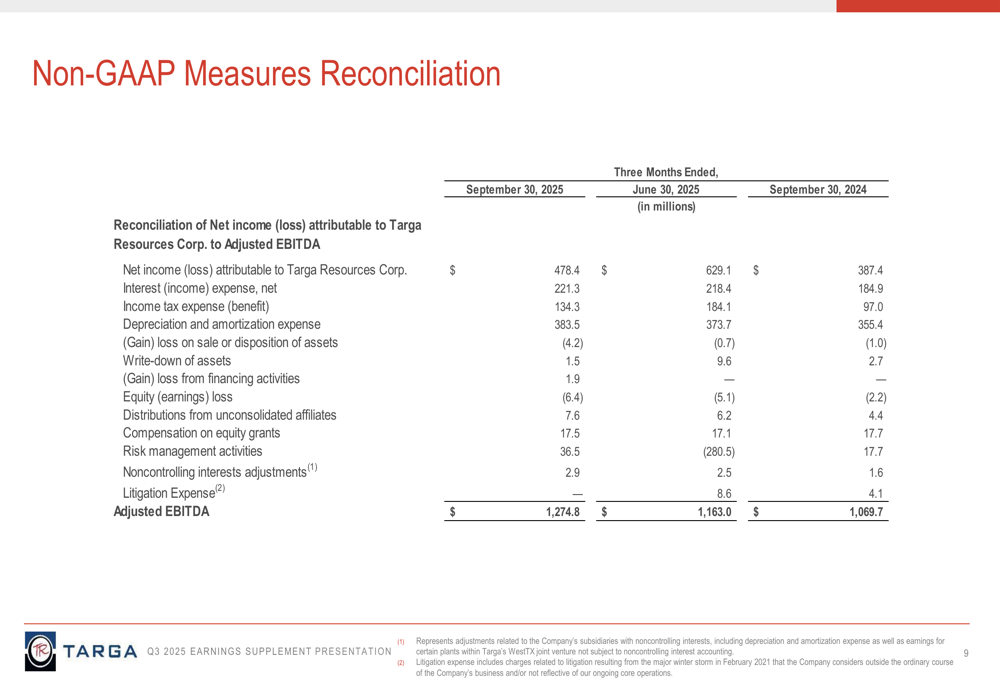

Targa reported a 19% year-over-year increase in Adjusted EBITDA for Q3 2025, reaching $1.275 billion compared to $1.070 billion in Q3 2024. This growth was primarily driven by higher volumes across the company’s integrated value chain, from gathering and processing to transportation and fractionation.

As shown in the following chart comparing Q3 2024 to Q3 2025 financial performance:

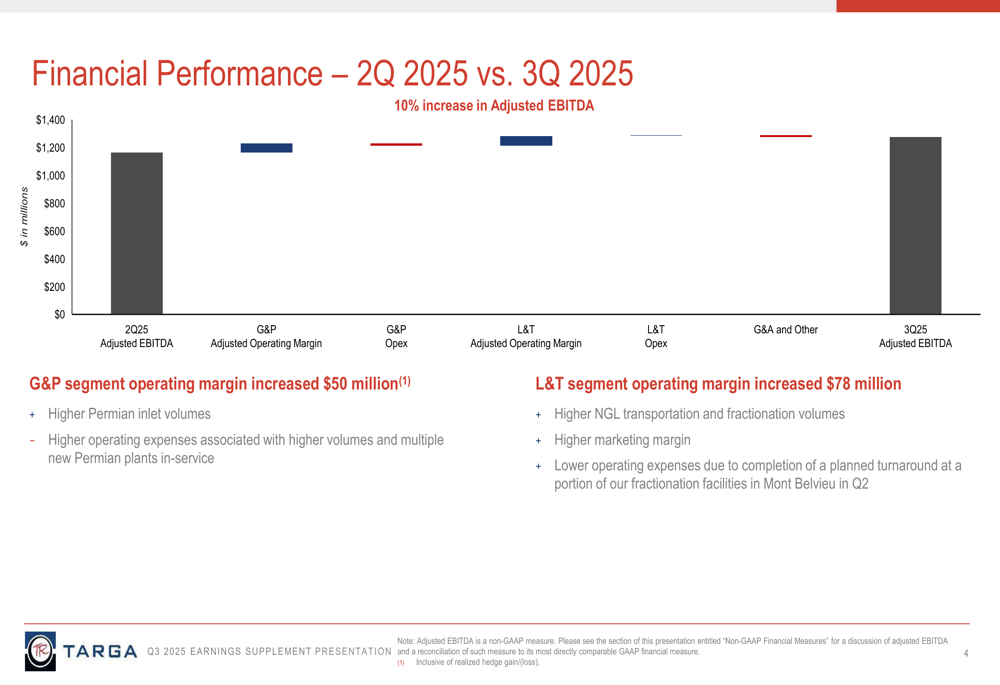

The sequential comparison was equally impressive, with Adjusted EBITDA increasing 10% from Q2 2025 to Q3 2025. This growth was fueled by higher Permian inlet volumes in the Gathering & Processing segment and increased NGL transportation and fractionation volumes in the Logistics & Transportation segment.

As illustrated in this quarter-over-quarter comparison:

Net income attributable to Targa Resources Corp. reached $478.4 million in Q3 2025, up from $387.4 million in Q3 2024, but down from $629.1 million in Q2 2025. Despite exceeding earnings expectations with an EPS of $2.13 versus the forecasted $2.11, the company fell short on revenue, reporting $4.15 billion against an expected $4.7 billion.

Operational Performance

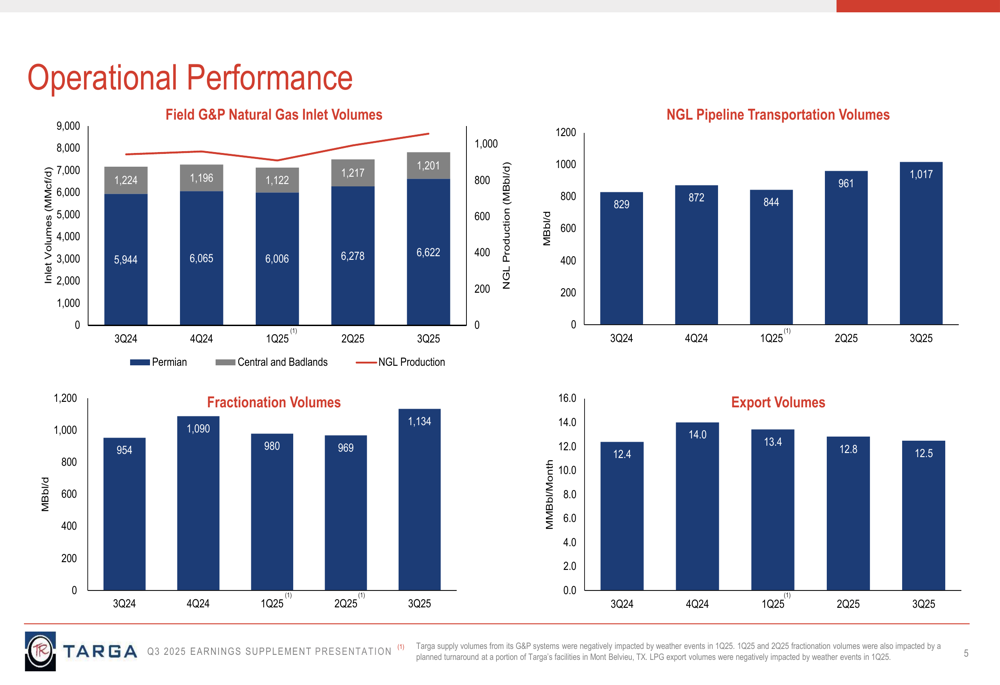

Targa’s operational metrics showed robust growth across all key areas. Field gathering and processing natural gas inlet volumes increased to 6,622 MMcf/d in Q3 2025, up from 5,944 MMcf/d in the same period last year. NGL pipeline transportation volumes grew significantly from 829 MBbl/d to 1,017 MBbl/d year-over-year, while fractionation volumes increased from 954 MBbl/d to 1,134 MBbl/d.

The following charts illustrate this consistent operational growth across Targa’s business segments:

It’s worth noting that Targa’s supply volumes were negatively impacted by weather events in Q1 2025, and fractionation volumes were affected by planned turnarounds in Q1 and Q2 2025. Despite these challenges, the company has demonstrated strong recovery and growth in Q3.

Detailed Financial Analysis

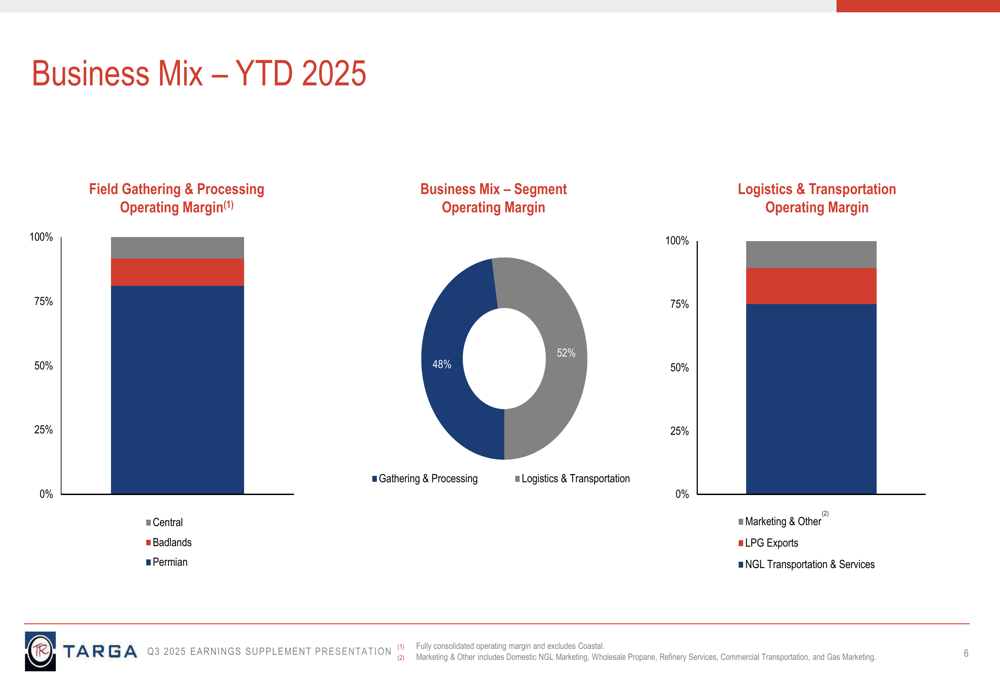

Targa’s business model shows a well-balanced mix between its two primary segments. For year-to-date 2025, the Gathering & Processing segment contributed 48% of operating margin, while the Logistics & Transportation segment provided 52%. This balanced approach highlights Targa’s integrated midstream model and diversified revenue streams.

The company’s business mix for YTD 2025 is illustrated below:

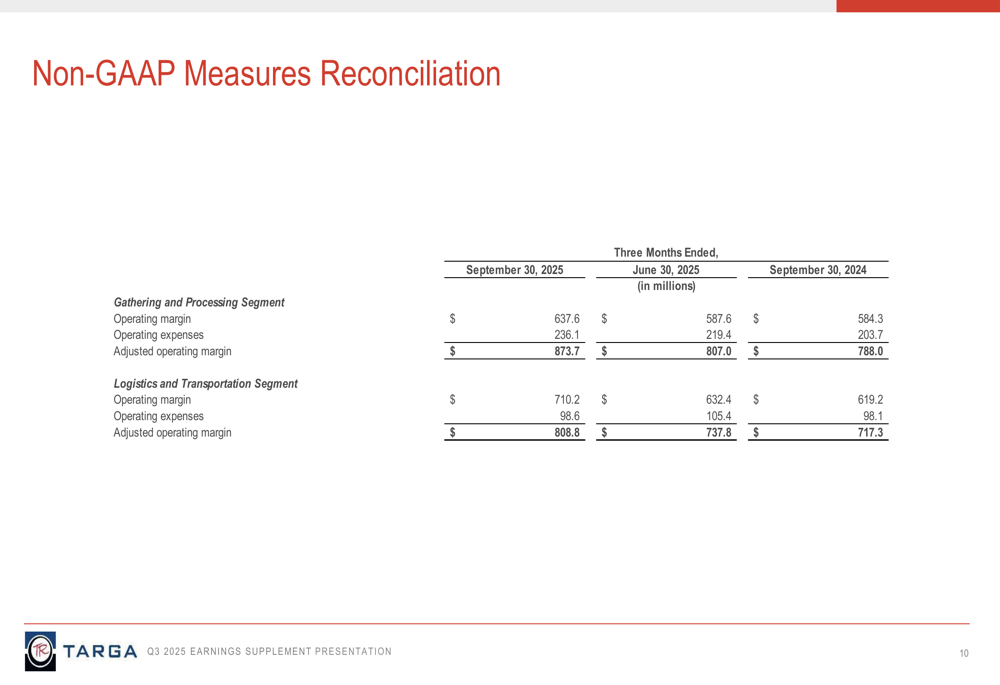

The Gathering & Processing segment saw its adjusted operating margin increase to $873.7 million in Q3 2025, up from $788.0 million in Q3 2024 and $807.0 million in Q2 2025. This growth was primarily driven by higher Permian inlet volumes, though partially offset by increased operating expenses.

Similarly, the Logistics & Transportation segment’s adjusted operating margin grew to $808.8 million in Q3 2025, compared to $717.3 million in Q3 2024 and $737.8 million in Q2 2025. This improvement was attributed to higher NGL transportation and fractionation volumes, as well as higher marketing margins.

The reconciliation of these non-GAAP measures provides additional insight into Targa’s financial performance:

Forward-Looking Statements

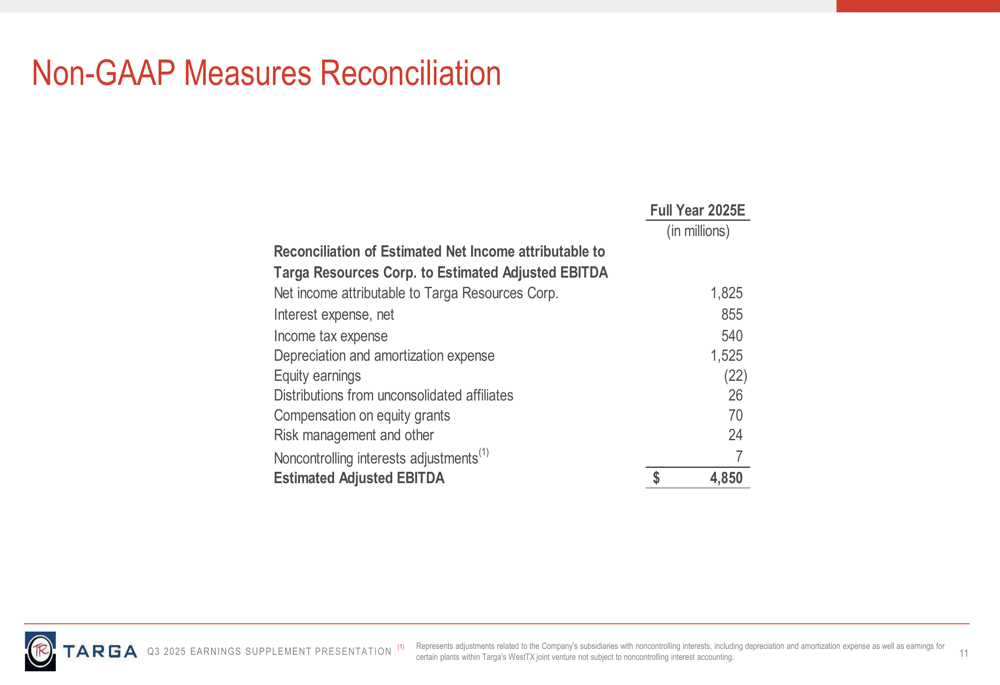

Looking ahead, Targa Resources provided guidance for full-year 2025, estimating Adjusted EBITDA of $4.85 billion. The company anticipates continued strong long-term growth in Permian gas and NGL volumes, supporting its ongoing infrastructure expansions.

The company’s full-year 2025 guidance reconciliation is shown below:

During the earnings call, CEO Matt Meloy emphasized the company’s transformation into a large integrated NGL infrastructure company, stating, "We are working towards Targa’s next transformation." President Jen Kneale highlighted the benefits of increasing gas-to-oil ratios, noting, "We continue to see a broad theme of increasing GORs, which we’re certainly a beneficiary of."

Targa maintains a strong financial position with available liquidity of $2.3 billion and a pro forma consolidated leverage ratio of 3.6x. The company expects to maintain strong free cash flow and aims to reduce its leverage ratio while continuing to increase dividends and pursue share repurchases.

While the company faces challenges including revenue shortfalls and potential market volatility, its strategic positioning in the Permian Basin and continued infrastructure investments appear to have resonated positively with investors, as evidenced by the strong market reaction to its Q3 2025 results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.