TSX futures inch lower after index closes at new all-time high

Introduction & Market Context

TC Energy Corporation (NYSE:TRP) presented its first quarter 2025 results on May 1, highlighting modest growth in comparable EBITDA alongside significant progress on strategic projects. The Canadian energy infrastructure company reported strong operational performance across its natural gas pipeline network in Canada, the United States, and Mexico, positioning itself to capitalize on growing demand for natural gas, particularly for power generation and data centers.

The company’s stock closed at $50.41 on April 30, 2025, showing a slight increase of 0.38% before the earnings call. TC Energy has been executing on its strategy of disciplined capital allocation while working toward its long-term debt-to-EBITDA target of 4.75x.

Quarterly Performance Highlights

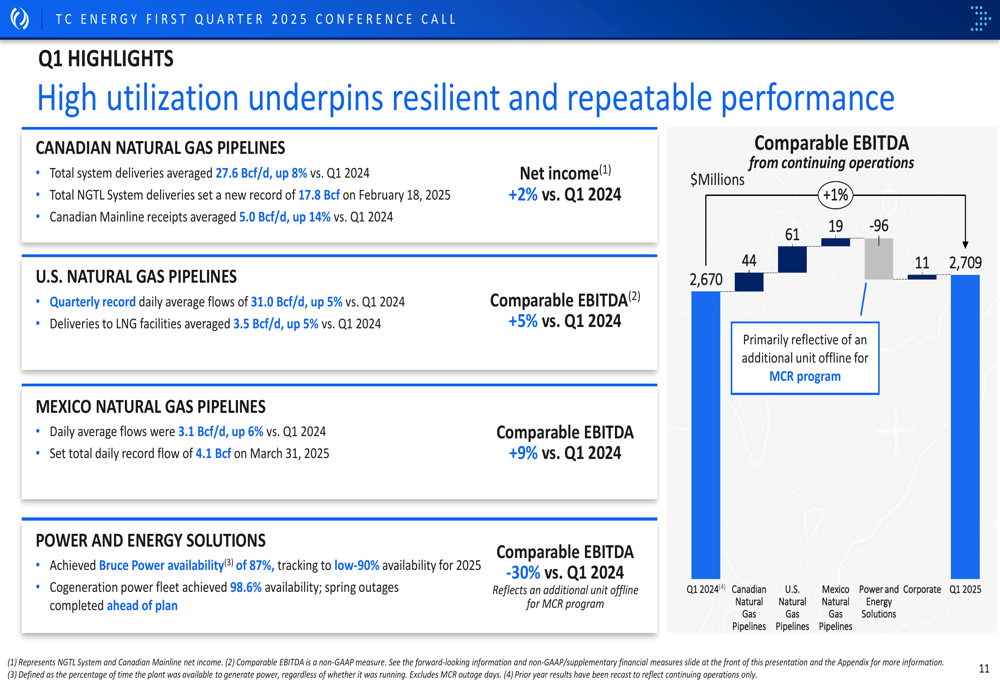

TC Energy reported comparable EBITDA of $2,709 million for Q1 2025, a modest 1.5% increase from $2,670 million in the same period last year. This growth was driven by strong operational performance across all business segments, with record pipeline flows in several regions.

As shown in the following chart detailing Q1 highlights and comparable EBITDA performance:

The company’s Canadian Natural (NYSE:CNQ) Gas Pipelines saw total system deliveries average 27.6 Bcf/d, an 8% increase compared to Q1 2024. The NGTL System set a record for deliveries, while Canadian Mainline receipts averaged 5.0 Bcf/d, up 14% year-over-year.

U.S. Natural Gas Pipelines achieved quarterly record daily average flows of 31.0 Bcf/d, a 5% increase from Q1 2024. Deliveries to LNG facilities averaged 3.5 Bcf/d, also up 5% year-over-year, highlighting TC Energy’s role in the growing U.S. LNG export market.

Mexico Natural Gas Pipelines continued to show strong performance with daily average flows of 3.1 Bcf/d, a 6% increase from Q1 2024. The segment set a total daily record flow of 4.1 Bcf on March 31, 2025, demonstrating the growing demand for natural gas in Mexico.

Despite the operational strength, comparable earnings per share decreased to $0.95 in Q1 2025 from $1.02 in Q1 2024, primarily due to higher interest expenses, foreign exchange losses, and increased depreciation and amortization.

Strategic Initiatives

TC Energy is making significant progress on several strategic initiatives that align with its focus on maximizing value, executing growth, and ensuring financial strength.

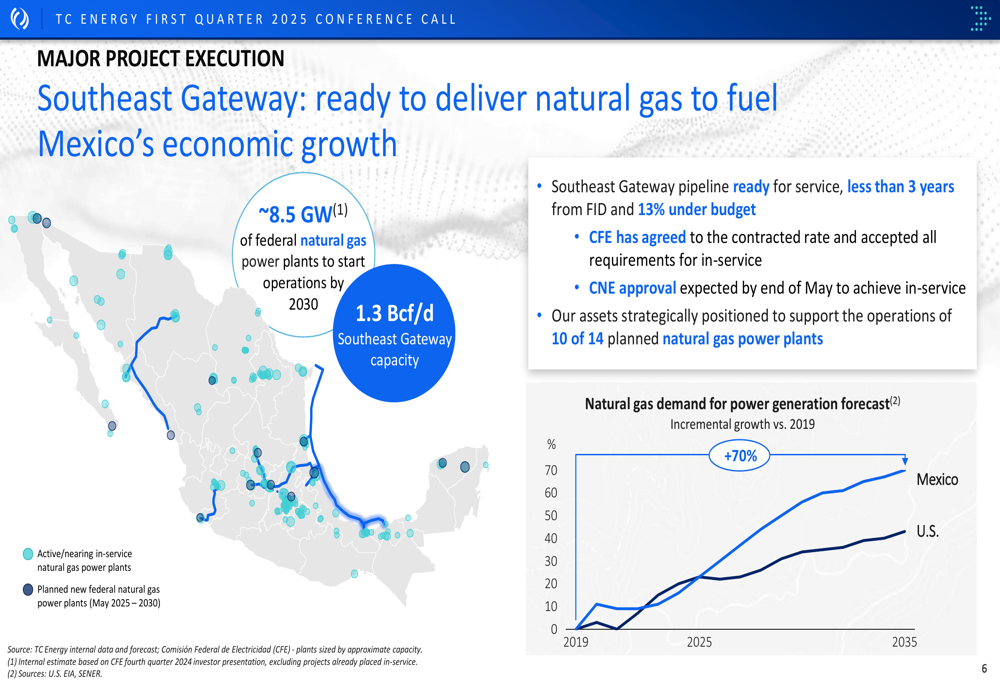

The company highlighted its Southeast Gateway pipeline project in Mexico, which is now ready for service less than three years from final investment decision (FID) and 13% under budget. As illustrated in the following slide, the pipeline is strategically positioned to support Mexico’s economic growth:

The Southeast Gateway pipeline will support the operations of 10 of 14 planned natural gas power plants in Mexico, helping to fuel the country’s economic growth. Natural gas demand for power generation in Mexico is projected to grow by 70% by 2035 compared to 2019 levels, significantly outpacing growth in the United States.

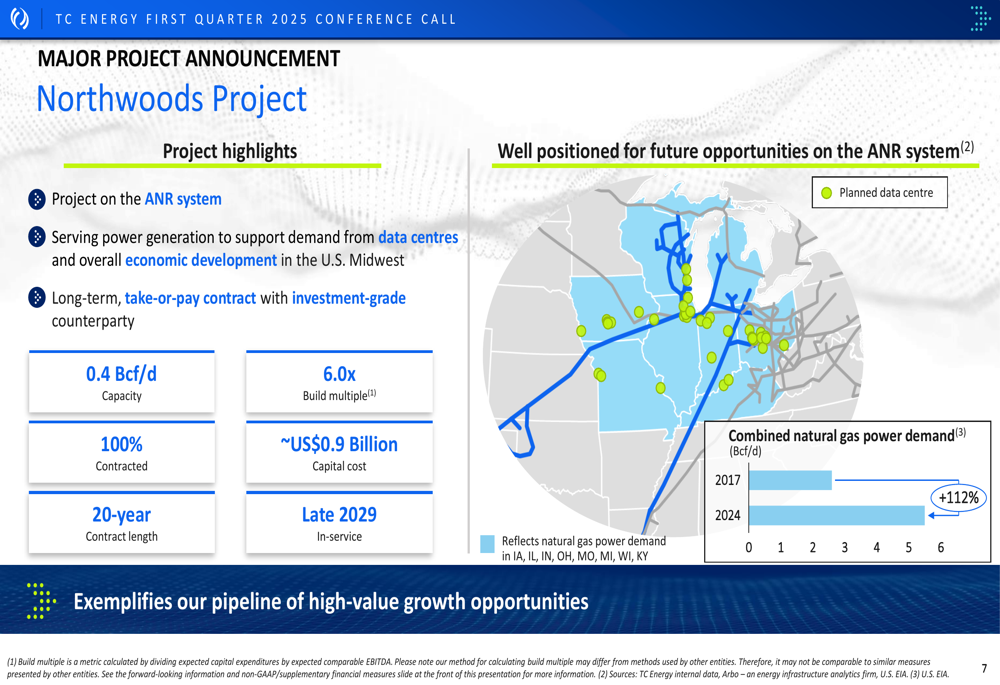

TC Energy also announced the Northwoods Project on its ANR system, a new initiative to support power generation for data centers and economic development in the U.S. Midwest. The following slide details this strategic project:

With a capital cost of approximately US$0.9 billion, the Northwoods Project will have a capacity of 0.4 Bcf/d, which is 100% contracted under a long-term, take-or-pay agreement with an investment-grade counterparty. The project has a build multiple of 6.0x and is expected to be in service by late 2029. The company highlighted that combined natural gas power demand has grown by 112% from 2017 to 2024, driven largely by data center expansion.

In the power segment, TC Energy continues to advance its Bruce Power Major Component Replacement (MCR) program, which will extend the life of nuclear units by 35+ years. The company has sanctioned the Unit 5 MCR, adding $1.1 billion of emission-less nuclear investment to its secured capital table.

Detailed Financial Analysis

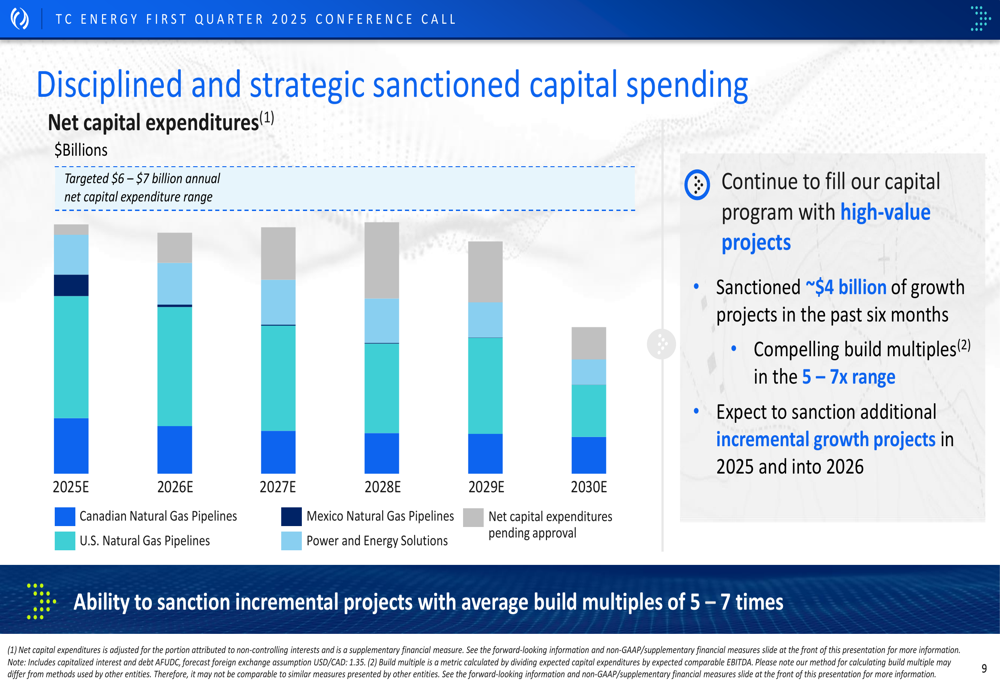

TC Energy’s financial strategy focuses on funding its capital program while maintaining financial strength. The company plans net capital expenditures of $5.5-6.0 billion for 2025 and maintains its commitment to annual net capital expenditures of $6-7 billion.

The following slide outlines the company’s disciplined capital spending approach:

TC Energy has sanctioned approximately $4 billion of growth projects in the past six months, with compelling build multiples in the 5-7x range. The company expects to sanction additional incremental growth projects in 2025 and into 2026, maintaining its disciplined approach to capital allocation.

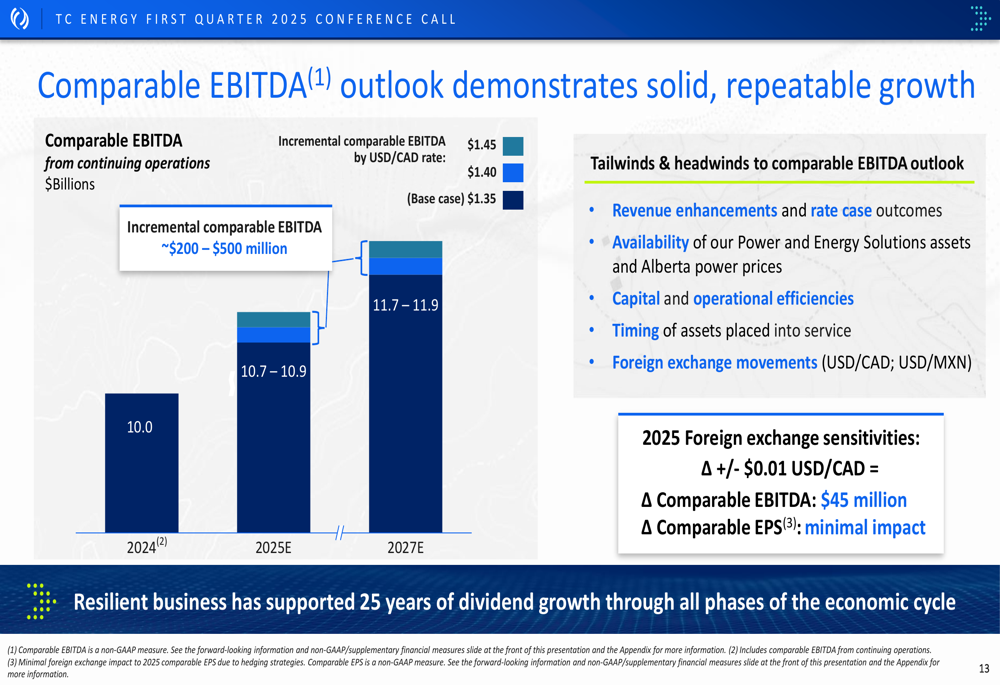

Looking ahead, TC Energy provided an outlook for comparable EBITDA growth, projecting $10.7-10.9 billion for 2025 and $11.7-11.9 billion for 2027, as shown in the following chart:

The company noted that its EBITDA outlook is subject to various factors, including foreign exchange movements, with a sensitivity of $45 million to comparable EBITDA for every $0.01 change in the USD/CAD exchange rate. Other factors influencing the outlook include revenue enhancements, rate case outcomes, asset availability, and capital and operational efficiencies.

TC Energy’s debt-to-EBITDA ratio stood at 4.8x as of December 31, 2024, an improvement from 5.1x in 2023, as the company continues its deleveraging efforts toward its long-term target of 4.75x.

Forward-Looking Statements

TC Energy outlined its strategic priorities for 2025, focusing on three key areas: maximizing value, executing growth, and ensuring financial strength. The company’s approach to these priorities is detailed in the following slide:

Under the "Maximizing Value" priority, TC Energy highlighted that safety incident rates are trending at five-year lows, and the company is filing Section 4 rate cases on ANR & GLGT with new rates expected by November 1, 2025.

For "Portfolio Growth," the company noted that the Southeast Gateway is ready for service less than 3 years from FID, CNE approval is expected by the end of May, and the company is on track to place $8.5 billion of assets into service in 2025, approximately 15% under budget.

In terms of "Financial Strength," TC Energy executed $3.5 billion in debt capital market transactions during Q1 2025 and continues its deleveraging efforts toward the long-term target of 4.75x debt-to-EBITDA.

The company’s messaging emphasizes "solid growth, low risk, repeatable performance" as it continues to execute its strategy in a disciplined manner.

Conclusion

TC Energy’s Q1 2025 results demonstrate the company’s ability to generate stable cash flows from its diversified portfolio of energy infrastructure assets while advancing strategic growth initiatives. Despite modest EBITDA growth and a slight decline in earnings per share, the company’s operational performance remains strong across all segments.

With significant projects like Southeast Gateway ready for service and new initiatives like the Northwoods Project addressing growing demand for natural gas, TC Energy appears well-positioned to capitalize on long-term energy trends, particularly in natural gas for power generation and data centers. The company’s disciplined approach to capital allocation and continued focus on deleveraging provide a solid foundation for sustainable growth in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.