Asia FX weakens slightly, rupee recovers from record low as RBI holds rates

Introduction & Market Context

Tecsys Inc. (TSX:TCS), a provider of supply chain management solutions, presented its Q4 and full-year FY2025 results on June 27, 2025, highlighting continued revenue growth driven by its SaaS business model. The company reported annual revenue of $176 million, up from $171 million in FY2024, as it continues to focus on complex supply networks across healthcare and distribution sectors.

With over 40 years of experience in complex supply chain solutions, Tecsys has established itself as a trusted provider, with 14 appearances in Gartner (NYSE:IT)’s Magic Quadrant for Warehouse Management Systems (WMS). The company now serves over 1,000 customers globally, with 72% of revenue coming from the United States, 18% from Canada, and 10% from the rest of the world.

Quarterly Performance Highlights

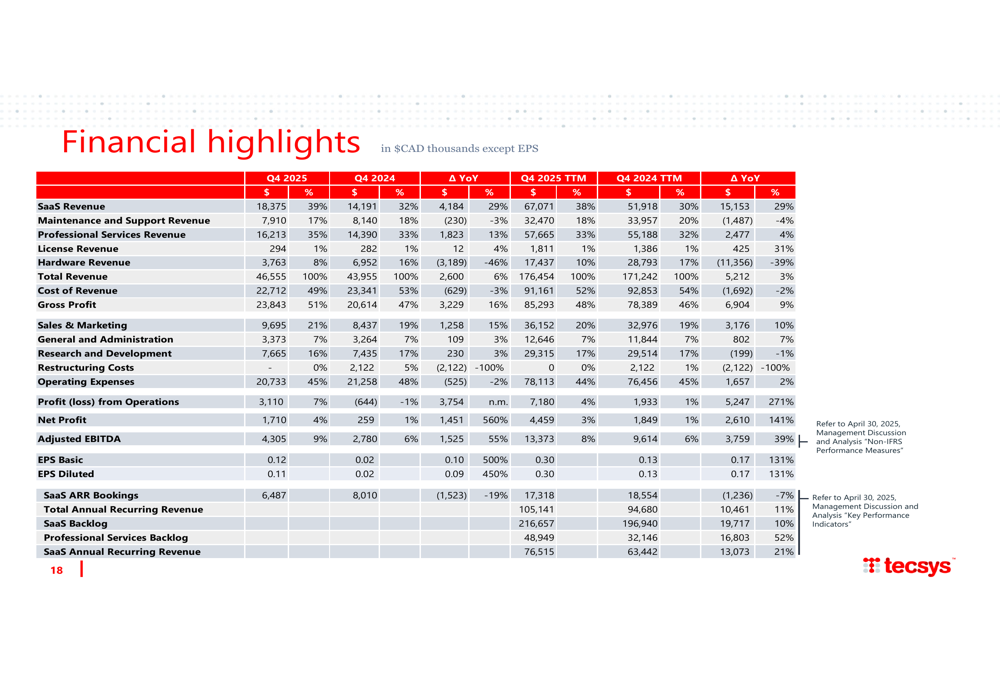

For Q4 FY2025, Tecsys reported total revenue of $46.6 million, a 5.9% increase from $44.0 million in Q4 FY2024. The company’s SaaS revenue showed significant growth, reaching $18.4 million for the quarter, up 29.5% from $14.2 million in the same period last year.

Profitability metrics showed substantial improvement, with Q4 net profit rising to $1.7 million from $259,000 in the prior year quarter. Adjusted EBITDA for Q4 FY2025 increased to $4.3 million, compared to $2.8 million in Q4 FY2024, reflecting improved operational efficiency and scaling of the SaaS business.

As shown in the following comprehensive financial summary:

SaaS Transition and Recurring Revenue Growth

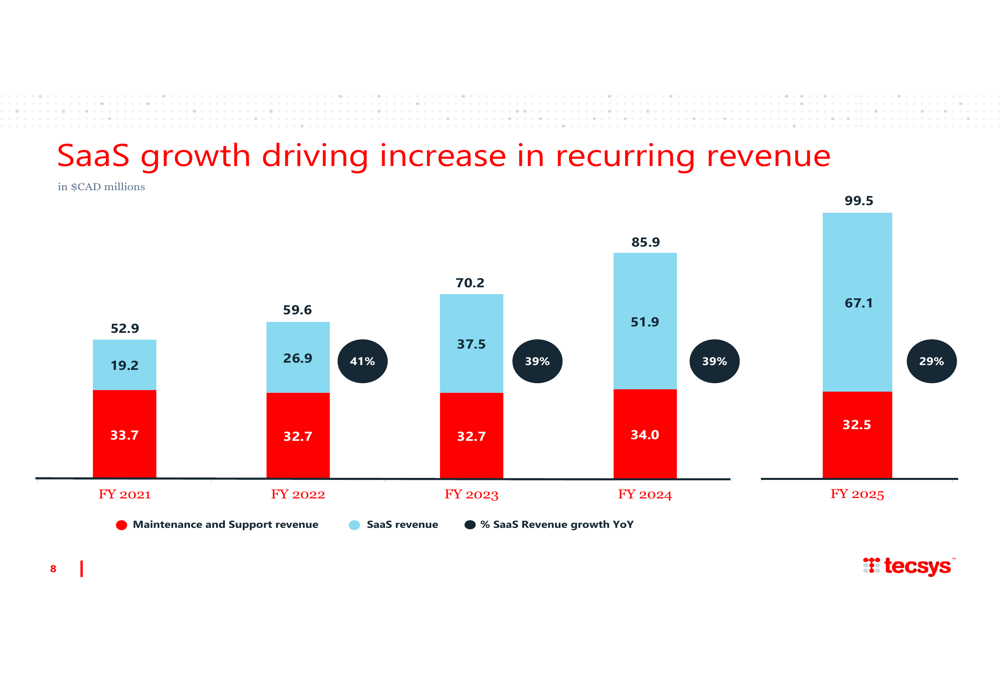

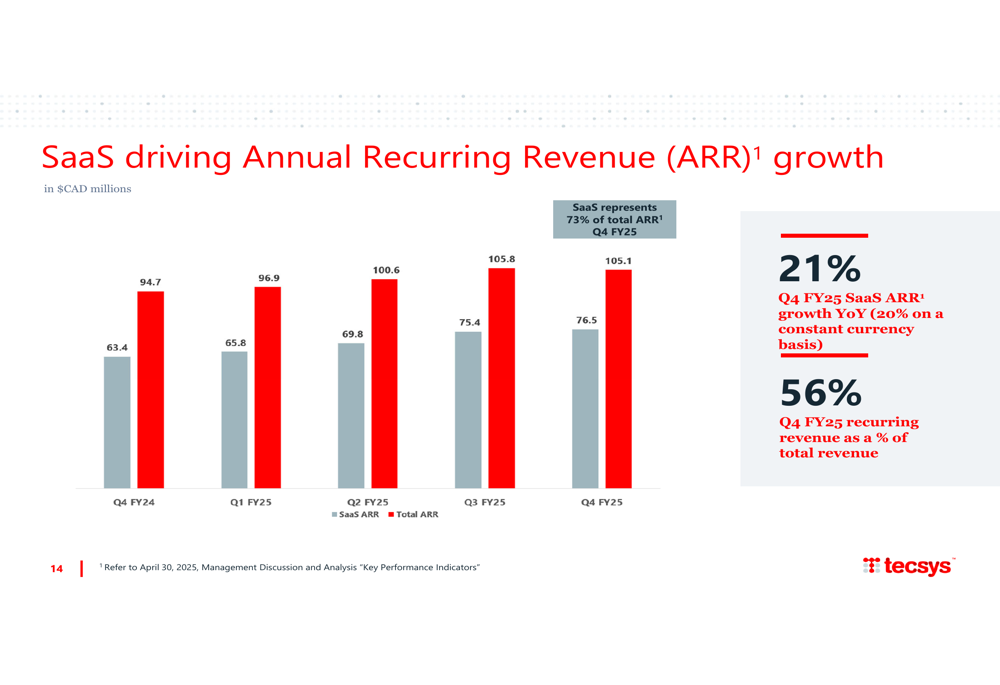

Tecsys continues to successfully transition its business model toward SaaS offerings, with SaaS revenue growing 29% year-over-year to reach $67.1 million for FY2025. This growth has driven the company’s annual recurring revenue (ARR) to $105.1 million as of April 30, 2025, with SaaS ARR representing 73% of the total at $76.5 million.

The company’s recurring revenue strategy is clearly illustrated in this multi-year progression:

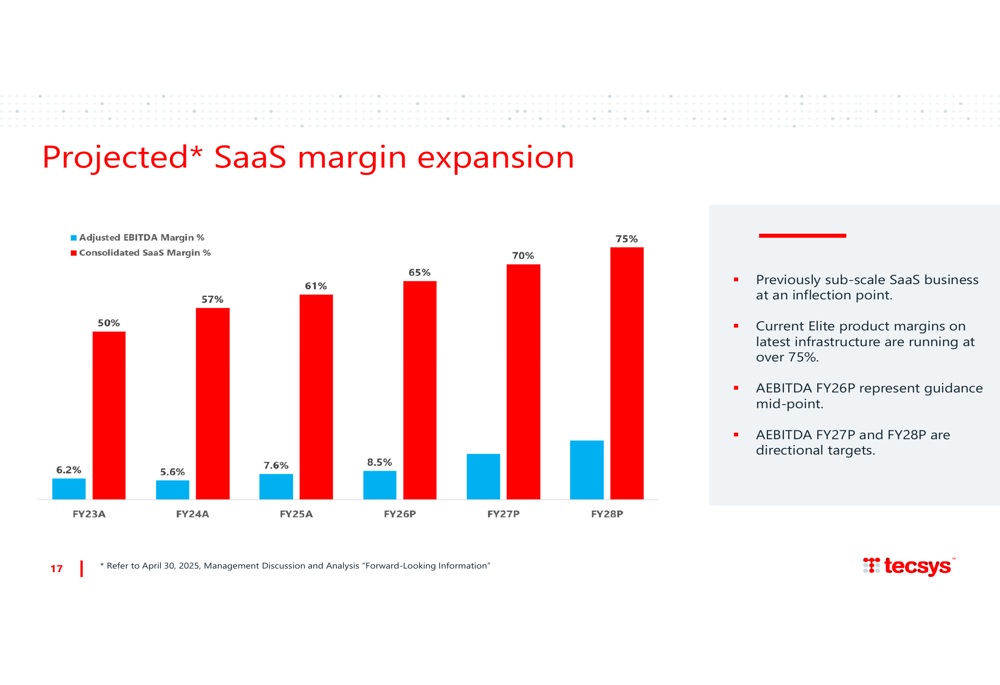

The SaaS business is also showing improving economics, with consolidated SaaS margins expanding to 61% in FY2025, up from 57% in FY2024 and 50% in FY2023. Management projects further margin expansion to 65% in FY2026 and potentially reaching 75% by FY2028, as shown in the following chart:

The company’s SaaS Remaining Performance Obligation (RPO), representing contracted future revenue, reached $217 million by the end of FY2025, growing 10% year-over-year. However, the net retention rate declined slightly to 106% in 2025 from 113% in the previous two years, indicating some moderation in expansion within the existing customer base.

Market Opportunities and Strategic Focus

Tecsys identified significant market opportunities in its two core verticals. In healthcare, which represents 77% of the company’s SaaS ARR, Tecsys targets 382 health systems with a total addressable market of $1.5 billion. The company currently holds only 15% market share, suggesting substantial room for growth.

In the distribution sector, Tecsys is pursuing a $6 billion market opportunity across 12,000 potential customers in high-volume distribution and wholesaling of hard goods, targeting companies with revenues between $200 million and $10 billion.

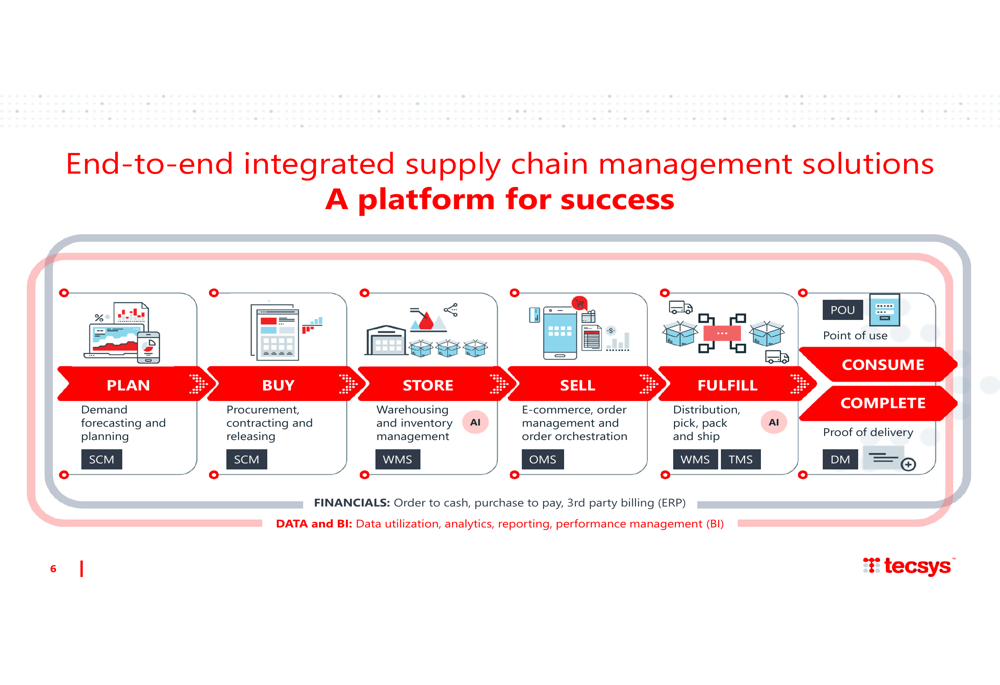

The company’s end-to-end integrated supply chain management solutions position it well to address these markets:

Tecsys has also expanded its partner ecosystem to accelerate market penetration, with partners now influencing 29% of the current sales pipeline. Key technology partners include AWS, Workday (NASDAQ:WDAY), Oracle (NYSE:ORCL), and Shopify (NASDAQ:SHOP), while advisory partners include Deloitte, CGI, and KPMG.

Financial Outlook and Investor Positioning

With a market capitalization of approximately $629 million and insider ownership of 17%, Tecsys presents itself as an investment opportunity based on its cloud-based platform serving two major supply chain segments, significant market opportunities, and SaaS growth trajectory.

The company highlighted that it trades at 3.0x next twelve months (NTM) enterprise value to sales, representing a 72% discount to its closest comparable, Manhattan Associates (NASDAQ:MANH), suggesting potential valuation upside.

For investors, Tecsys offers a dividend of 33 cents per year and has coverage from five brokerage firms: Cormark Securities, National Bank Financial, Raymond (NSE:RYMD) James, Stifel, and Ventum Financial.

Looking ahead, Tecsys aims to continue expanding its SaaS business while improving margins. The company’s strong backlog and focus on healthcare and complex distribution markets position it to pursue growth opportunities, though investors should note the slight deceleration in SaaS revenue growth from 39% in FY2024 to 29% in FY2025.

In its recent Q1 FY2026 earnings call, Tecsys reported continued momentum with 33% year-over-year SaaS revenue growth and a 57% increase in SaaS bookings, including a major healthcare migration deal covering over 100 hospitals, reinforcing the company’s strategic direction outlined in this presentation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.