Bubble or no bubble, this is the best stock for AI exposure: analyst

Introduction & Market Context

Teleflex Incorporated (NYSE:TFX) presented its second quarter 2025 earnings on July 31, 2025, reporting modest revenue growth but significantly raising its full-year guidance. The medical technology company's stock remained stable in aftermarket trading, closing at $120.09, according to available market data.

The company continues to navigate a mixed market environment, with strong performance in some segments offset by challenges in others. Teleflex's strategic initiatives, including a major acquisition and planned company separation, form key elements of its growth strategy amid competitive pressures in the medical device industry.

Quarterly Performance Highlights

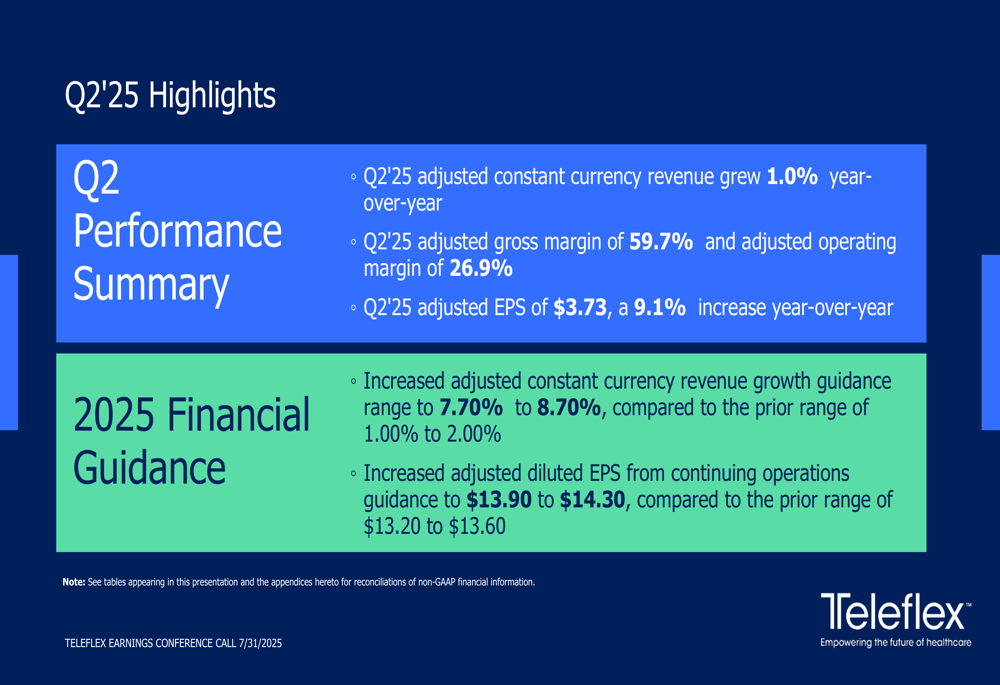

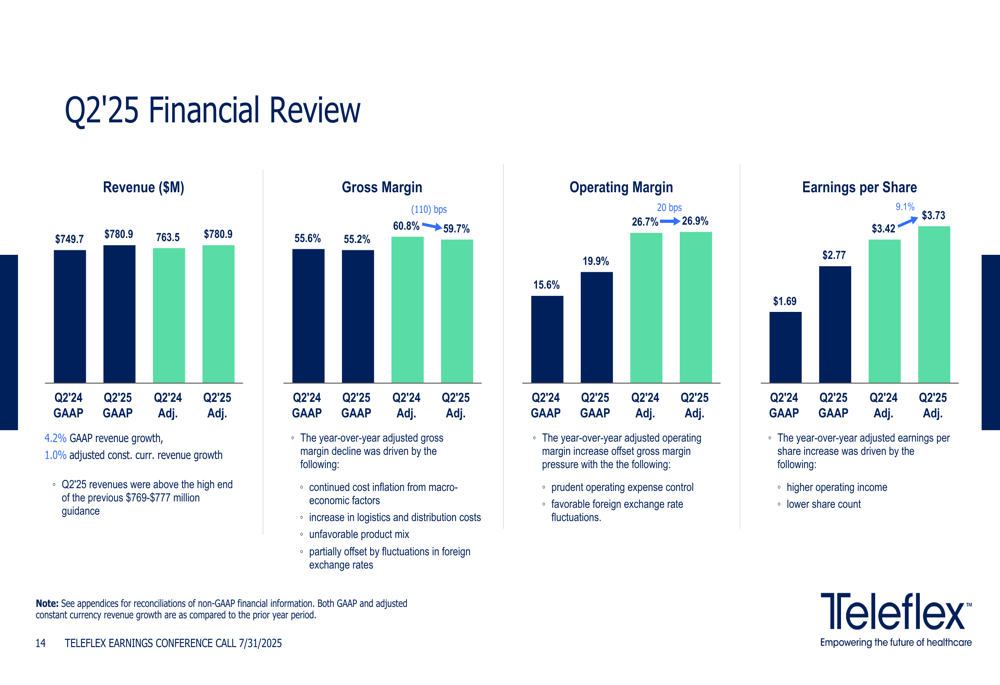

Teleflex reported Q2 2025 revenue of $780.9 million, representing 4.2% reported growth and 1.0% adjusted constant currency growth year-over-year. Adjusted earnings per share reached $3.73, a 9.1% increase from the prior year, driven by higher operating income and a lower share count.

As shown in the following summary of Q2 2025 highlights:

The company's adjusted gross margin was 59.7%, a decrease from the previous year, while adjusted operating margin improved slightly to 26.9%. Management attributed the gross margin pressure to cost inflation, increased logistics costs, and unfavorable product mix, partially offset by foreign exchange fluctuations. Despite these challenges, Teleflex was able to offset gross margin pressure through expense control and favorable foreign exchange rates.

The following financial review provides a visual breakdown of these key metrics:

Segment and Product Performance

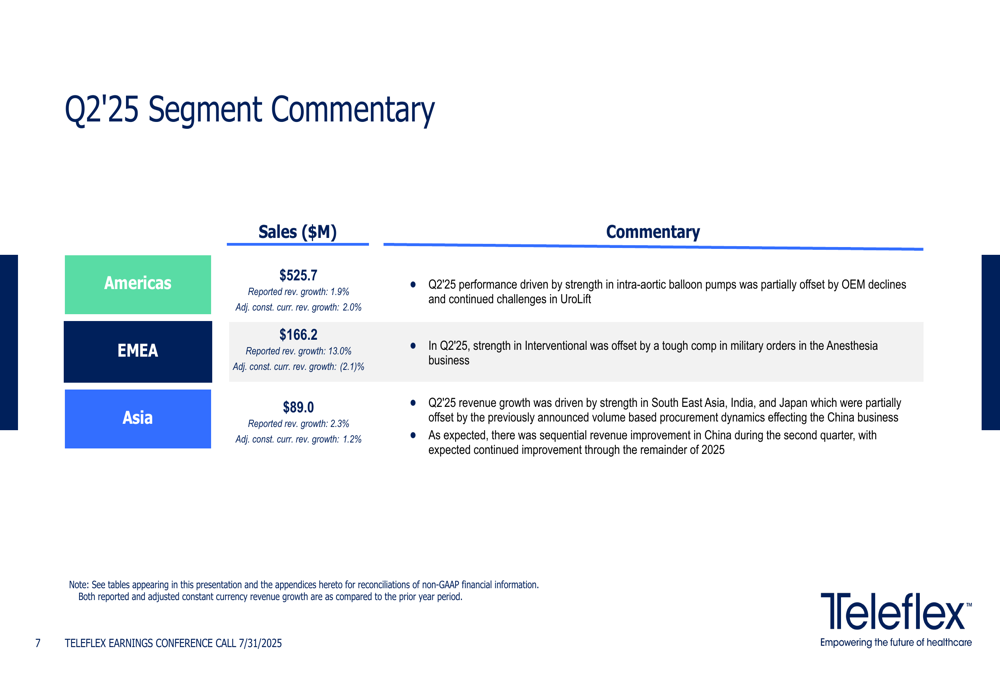

Teleflex's performance varied significantly across geographic segments and product categories. The Americas region, which accounted for approximately 67% of total revenue at $525.7 million, grew 2.0% on an adjusted constant currency basis. EMEA (Europe, Middle East, and Africa) revenue declined 2.1% on the same basis, while Asia showed modest growth of 1.2%.

The segment breakdown reveals regional performance drivers and challenges:

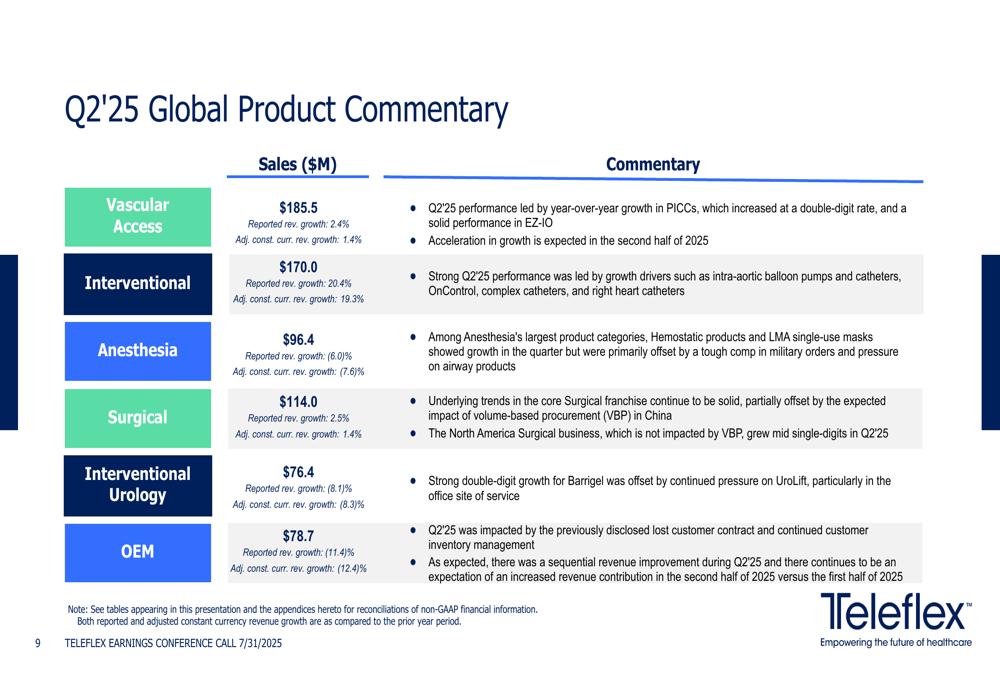

Among product categories, the Interventional segment was the standout performer with 19.3% adjusted constant currency growth, driven by strong performance in intra-aortic balloon pumps, OnControl, and complex and right heart catheters. In contrast, Interventional Urology declined 8.3% despite strong Barrigel performance, due to pressure on the UroLift business. The OEM segment saw the largest decline at 12.4%, impacted by a lost contract and inventory issues.

The following chart details performance across all product categories:

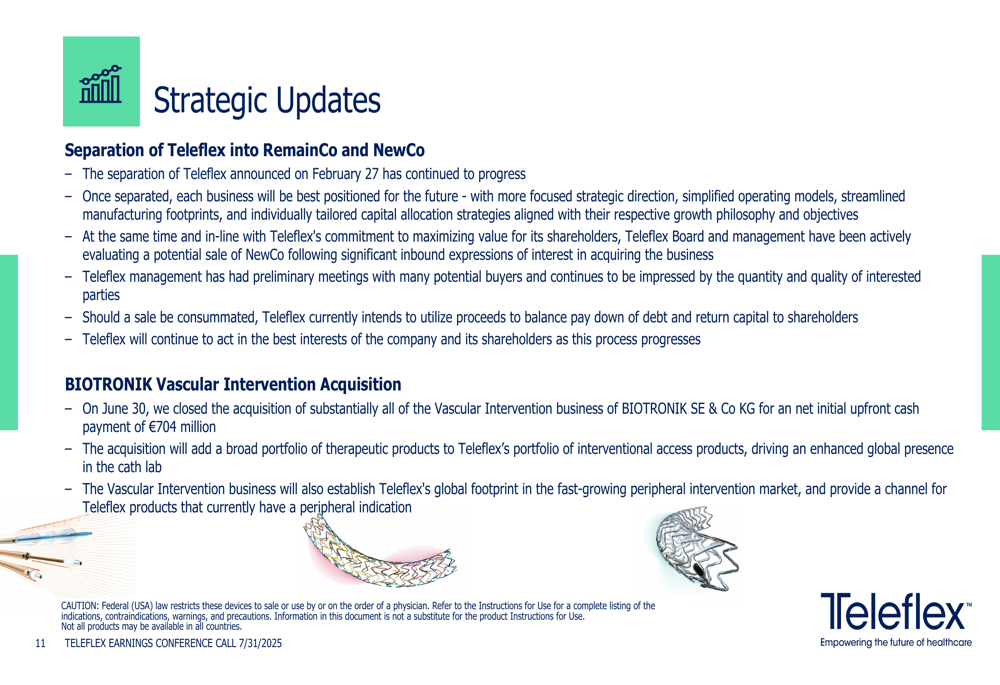

Strategic Initiatives

Teleflex highlighted significant progress on two major strategic initiatives. First, the company completed the acquisition of BIOTRONIK's Vascular Intervention business for €704 million, adding therapeutic products to its portfolio and establishing a global footprint in peripheral intervention.

Second, the company continues to advance its planned separation into two entities (RemainCo and NewCo), with management actively evaluating a potential sale of NewCo. The company intends to use proceeds from any potential sale to reduce debt and return capital to shareholders.

These strategic updates were outlined as follows:

The company also reported positive clinical developments, including new data supporting the efficacy of Arrow chlorhexidine-impregnated central venous catheters in reducing infection rates in ICU patients, and a study showing reduced post-operative gastroesophageal reflux disease rates with the Titan SGS™ Stapler compared to multi-fire staplers.

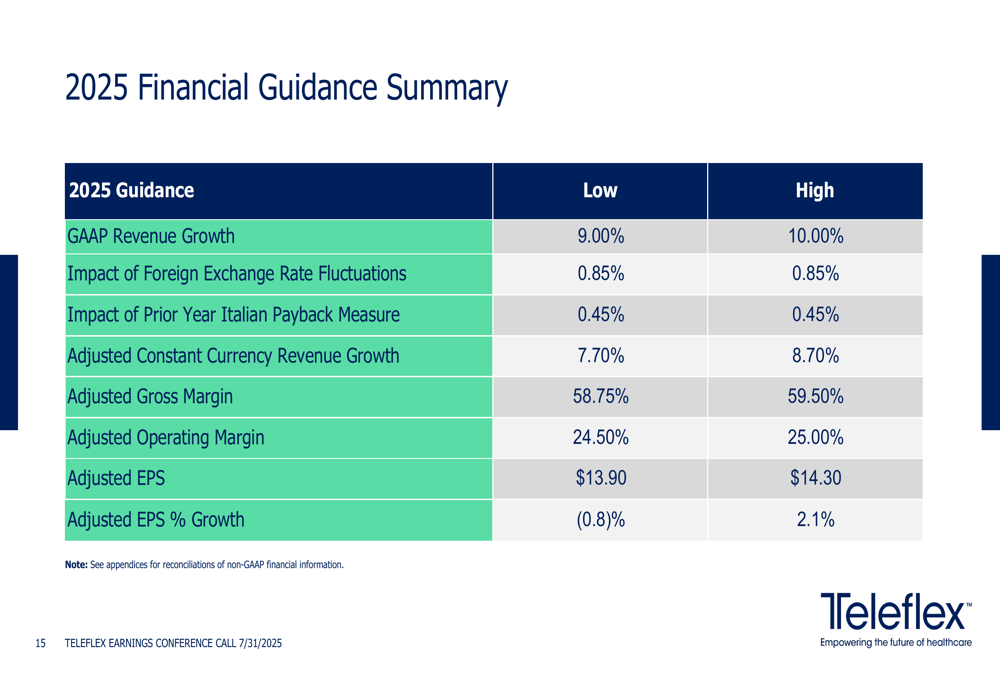

Financial Outlook and Guidance

In a significant development, Teleflex substantially raised its full-year 2025 guidance. The company now expects adjusted constant currency revenue growth of 7.70% to 8.70%, up from the previous range of 1.00% to 2.00%. Similarly, adjusted EPS guidance was increased to $13.90 to $14.30, compared to the prior range of $13.20 to $13.60.

The comprehensive guidance update is presented in the following chart:

This substantial increase in guidance suggests management's confidence in accelerating performance in the second half of 2025, likely driven by the BIOTRONIK acquisition integration and expected improvements in challenged segments like OEM, where the company anticipates "increased contribution expected in H2 2025."

Key Takeaways

Teleflex summarized the key takeaways from its Q2 2025 performance, emphasizing its execution of strategic objectives and delivery of revenues above guidance. The company highlighted the completion of the Vascular Intervention business acquisition and ongoing integration activities as significant milestones.

The presentation concluded with these key points:

Looking ahead, Teleflex appears positioned for stronger growth in the second half of 2025, driven by its recent acquisition and strategic initiatives. However, challenges remain in segments like Interventional Urology and OEM, which will require continued management attention. The company's planned separation continues to progress, with management focused on maximizing shareholder value through this transformation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.