German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

TeraWulf Inc (NASDAQ:WULF) shares surged 21.79% in premarket trading to $6.65 following the release of its Q2 2025 presentation on August 14, 2025, which revealed a significant financial recovery and strategic expansion of its dual business model. The company, which faced challenges in Q1 with disappointing financial results, has rebounded strongly in the second quarter while advancing its strategy of balancing Bitcoin mining with high-performance computing (HPC) infrastructure.

The presentation highlighted TeraWulf’s return to positive adjusted EBITDA and outlined major contracts with Core42 and Fluidstack, the latter backed by Google, positioning the company as a significant player in the digital infrastructure space.

Quarterly Performance Highlights

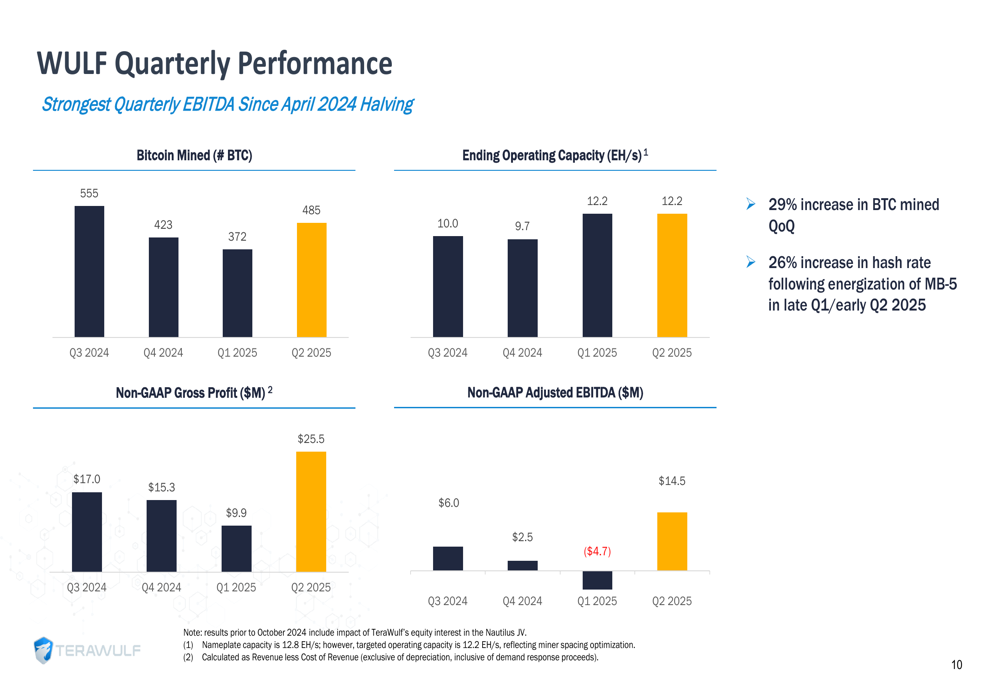

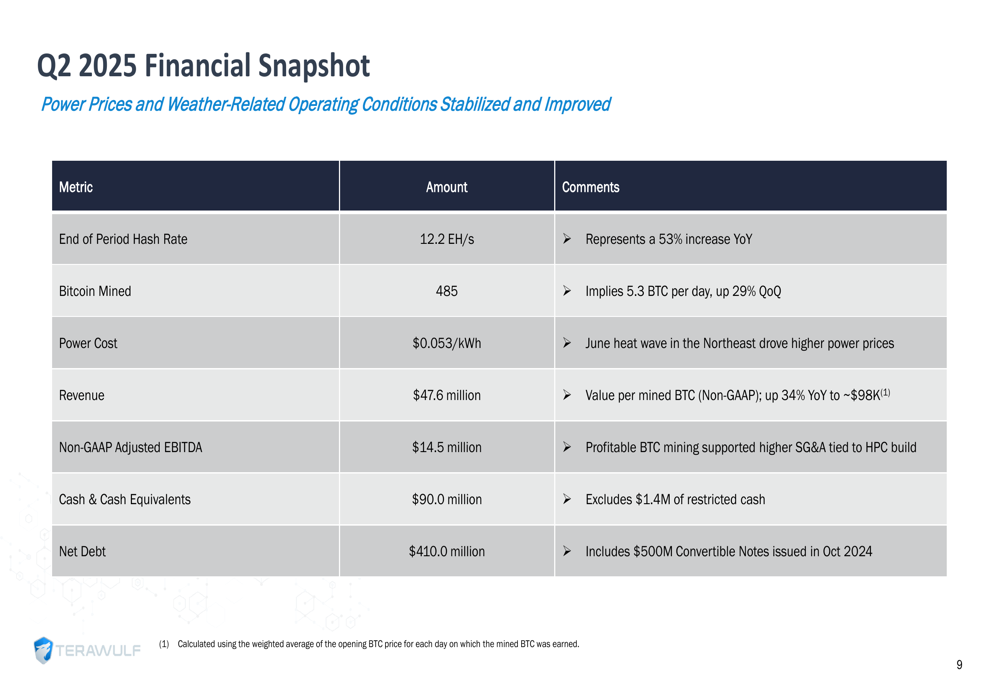

TeraWulf reported a substantial improvement in its financial performance for Q2 2025, with adjusted EBITDA of $14.5 million, compared to a negative $4.7 million in Q1 2025. The company mined 485 Bitcoin during the quarter, representing a 29% increase quarter-over-quarter, at an average rate of 5.3 BTC per day.

Revenue reached $47.6 million, with the value per mined Bitcoin increasing 34% year-over-year to approximately $98,000. The company maintained a hash rate of 12.2 EH/s at quarter end, representing a 53% increase year-over-year.

As shown in the following quarterly performance chart:

The company’s power cost averaged $0.053/kWh during the quarter, which TeraWulf noted was impacted by a June heat wave in the Northeast. Despite these challenges, the company achieved a non-GAAP gross profit of $25.5 million, significantly higher than the $9.9 million reported in Q1 2025.

TeraWulf’s cash position stood at $90 million at quarter-end, down from $218 million in Q1 2025, primarily due to significant capital expenditures related to its HPC infrastructure buildout.

The following financial snapshot provides additional context for the quarter’s performance:

Strategic Initiatives

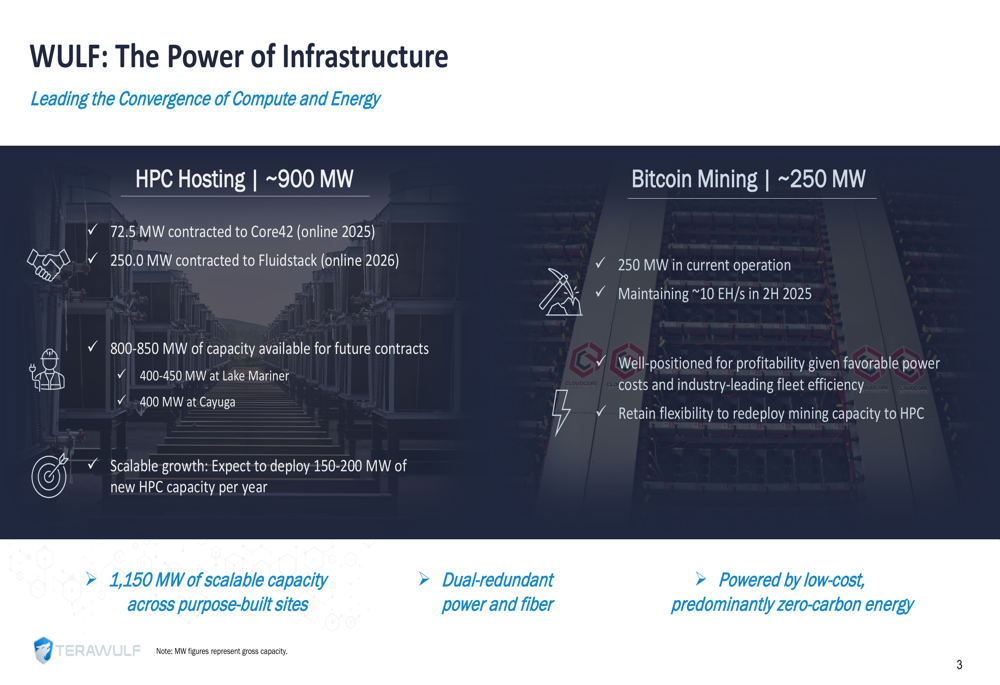

TeraWulf’s presentation emphasized its evolution into a dual-focused digital infrastructure company with approximately 900 MW dedicated to HPC hosting and 250 MW to Bitcoin mining. This strategic positioning allows the company to maintain flexibility, with the ability to redeploy mining capacity to HPC as market conditions warrant.

The company’s infrastructure strategy is illustrated in this overview:

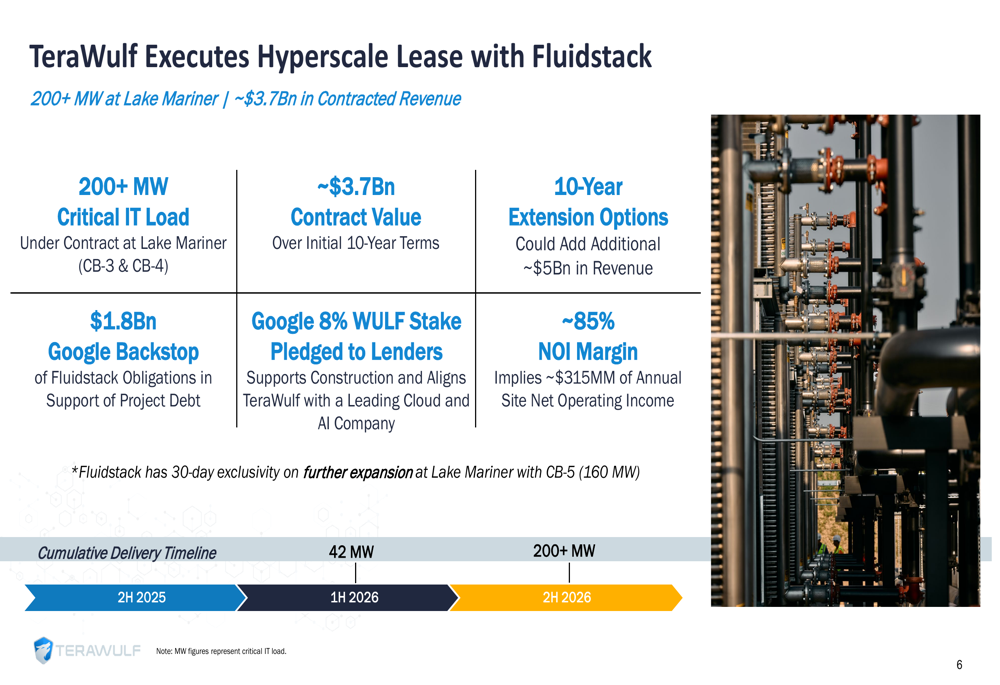

A significant milestone for TeraWulf is its hyperscale lease agreement with Fluidstack, valued at approximately $3.7 billion over an initial 10-year term. The contract, which includes Google backing with an 8% stake in WULF pledged to lenders, covers over 200 MW of critical IT load at the Lake Mariner facility. The agreement includes 10-year extension options that could add an additional $5 billion in revenue, with TeraWulf projecting approximately 85% NOI margin, implying around $315 million in annual site net operating income.

The details of this transformative agreement are shown here:

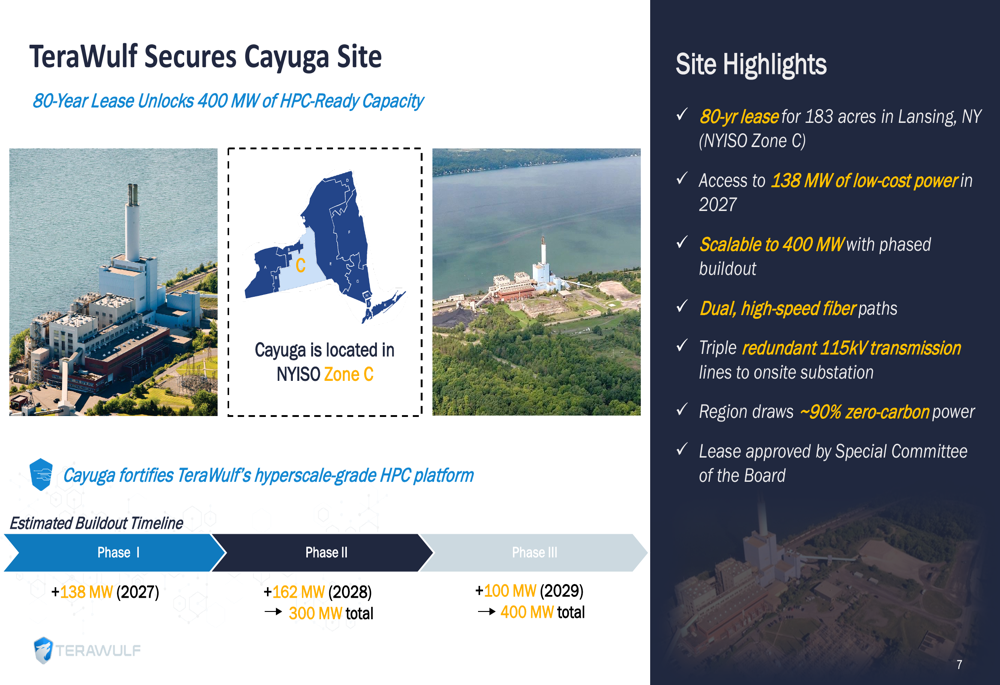

TeraWulf also announced securing the Cayuga site for HPC expansion, featuring an 80-year lease for 183 acres in Lansing, NY. The site provides access to 138 MW of low-cost power beginning in 2027 and is scalable to 400 MW with a phased buildout through 2029. The location draws approximately 90% zero-carbon power and includes dual high-speed fiber paths and triple redundant transmission lines.

The Cayuga expansion plan is detailed in the following slide:

Capital Allocation & Forward-Looking Statements

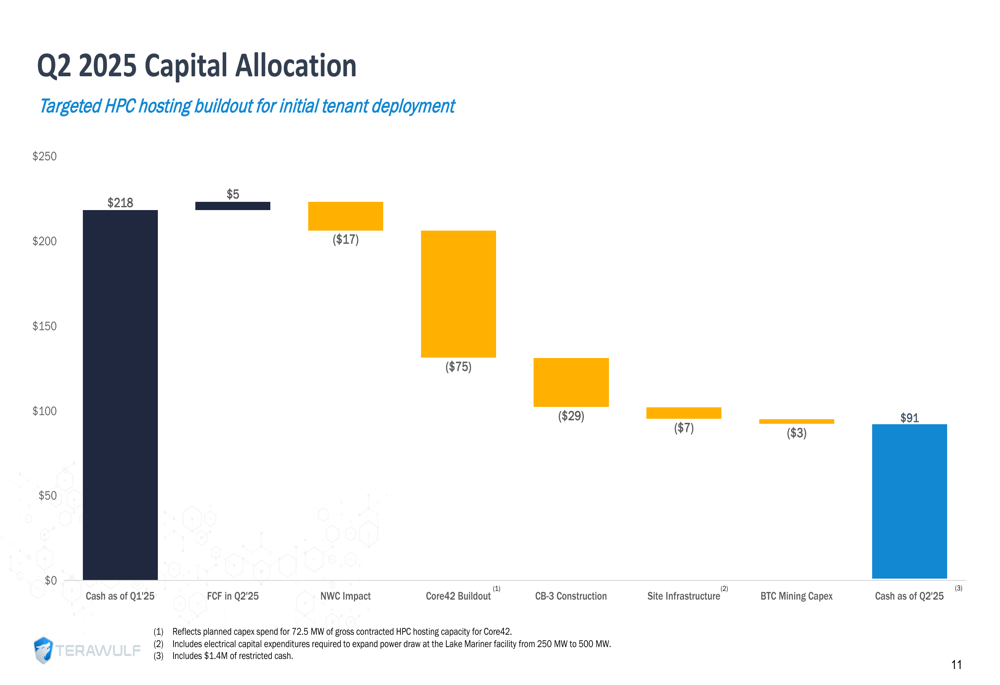

TeraWulf’s capital allocation during Q2 2025 focused heavily on HPC infrastructure development, with $75 million directed to the Core42 buildout, $29 million to CB-3 construction, and $7 million to site infrastructure. These investments reduced the company’s cash position from $218 million to $91 million during the quarter.

The capital allocation breakdown is illustrated here:

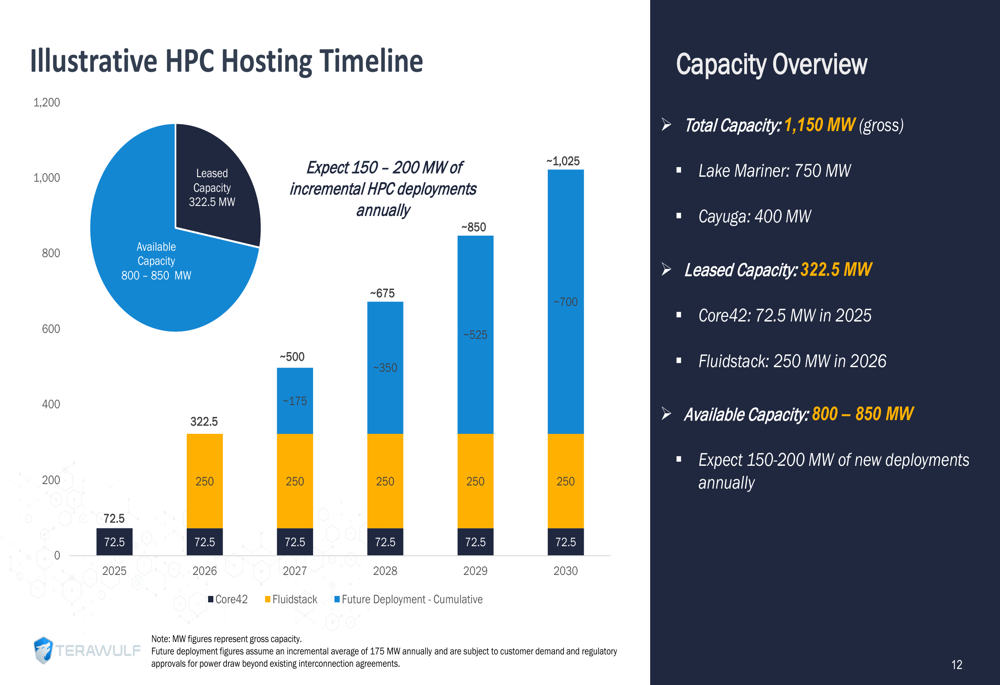

Looking ahead, TeraWulf projects continued growth in its HPC hosting business, with a target of deploying 150-200 MW of new HPC capacity annually. The company has 800-850 MW of available capacity across its sites for future contracts, positioning it for substantial growth in the coming years.

The company’s HPC hosting timeline and capacity overview demonstrates this growth trajectory:

For its Bitcoin mining operations, TeraWulf expects to maintain approximately 10 EH/s in the second half of 2025, with projected power costs of $0.05/kWh at Lake Mariner. The company’s fixed operating costs for 2025 are projected to be between $84-94 million, including $50-55 million in SG&A expenses and $14 million in interest on convertible notes.

Execution Track Record

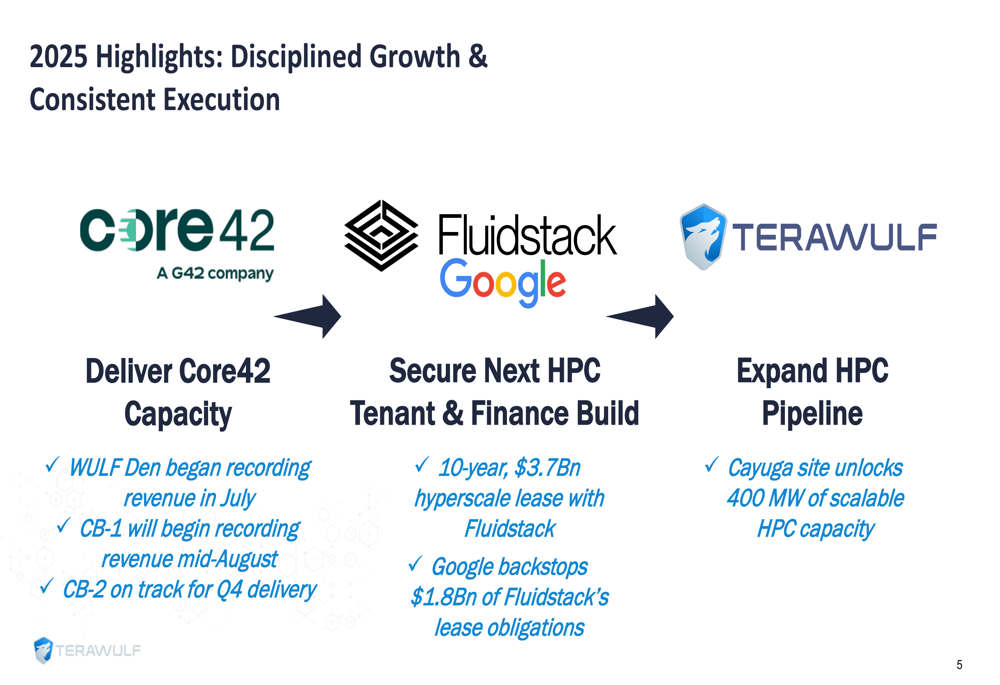

TeraWulf emphasized its proven execution capabilities, highlighting its development of over 600 MW of digital infrastructure to date. The company’s seasoned executive team brings decades of experience in power infrastructure development and energy market operations, which it views as a competitive advantage in delivering complex infrastructure projects.

The company’s 2025 highlights showcase its execution focus:

This recovery in Q2 2025 represents a significant turnaround from the challenging first quarter, when TeraWulf reported disappointing financial results with an EPS of -$0.16 against expectations of -$0.04. The positive market reaction to the Q2 presentation suggests investors are encouraged by the company’s recovery and strategic direction as it continues to balance Bitcoin mining operations with its expanding HPC infrastructure business.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.