German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

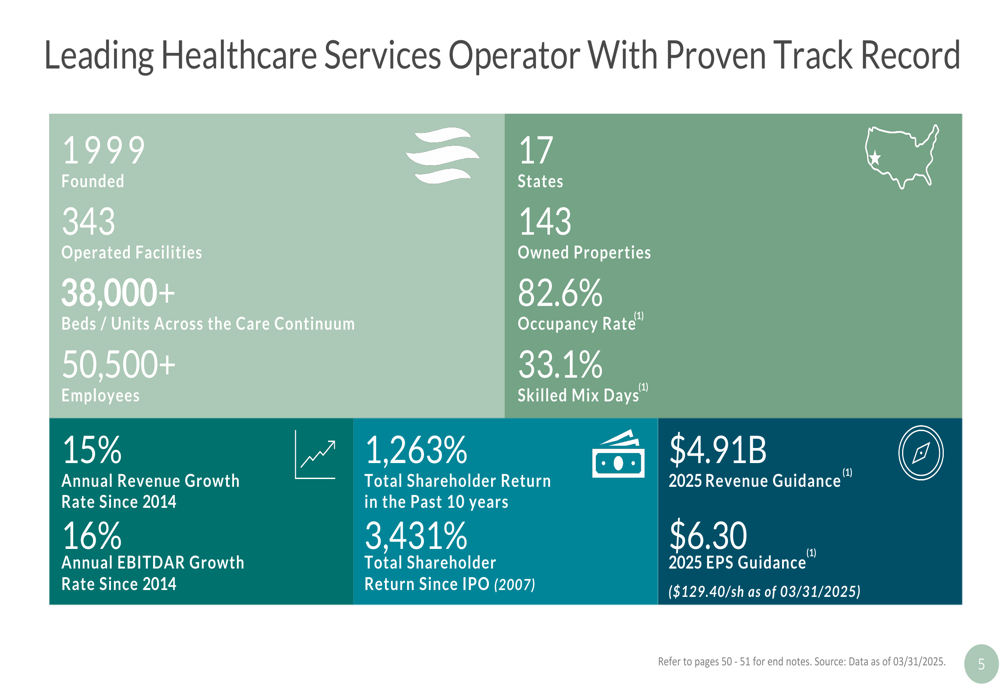

The Ensign Group , Inc. (NASDAQ:ENSG) presented its investor presentation for April 2025, highlighting strong Q1 2025 results and an optimistic outlook for the remainder of the year. The healthcare services provider continues to demonstrate robust growth across its portfolio of skilled nursing facilities, senior living communities, and healthcare-related real estate properties.

Operating in a fragmented market where it holds just 2.2% market share, Ensign has positioned itself as a high-quality, low-cost provider in the evolving value-based care environment. The company’s diversified business model spans 17 states with 343 facilities, 38,000+ beds/units, and employs over 50,500 people.

As shown in the following comprehensive overview of Ensign’s key metrics, the company has established itself as a leading healthcare services operator with impressive growth and returns:

Quarterly Performance Highlights

Ensign Group reported strong financial results for Q1 2025, with revenue reaching $1.17 billion, a 16.1% increase compared to $1.01 billion in Q1 2024. Consolidated adjusted net income grew to $89.0 million from $75.4 million in the prior year period, representing an 18% year-over-year increase.

The company’s diluted earnings per share rose to $1.37, up from $1.19 in Q1 2024, while adjusted diluted earnings per share increased to $1.52 from $1.30, marking a 16.9% improvement. These results demonstrate Ensign’s continued operational excellence and effective growth strategy.

The following chart illustrates the quarter-over-quarter highlights, showing the significant growth in key financial metrics:

Ensign’s same facility skilled nursing facility revenue grew to $834.8 million in Q1 2025 from $790.8 million in Q1 2024. The company maintained a solid occupancy rate of 82.6% across its portfolio, with skilled mix days at 33.1%, indicating a favorable patient mix that contributes to higher reimbursement rates.

Strategic Growth Initiatives

Ensign’s growth strategy centers on its unique local leadership model and disciplined approach to acquisitions. The company has completed 73 acquisitions since 2023, with 28.8% of its skilled nursing operations having been operated for less than three full years. This approach has consistently yielded improvements in key metrics for acquired facilities.

The company’s geographic footprint spans across 17 states, with a strategic focus on markets with favorable demographic trends. The following map illustrates Ensign’s operational presence:

A key component of Ensign’s success is the correlation between clinical quality and financial performance. The company has reduced its percentage of 1-star facilities from 41.3% to 20.1%, while simultaneously growing adjusted EBITDAR from $87 million to $706 million. This demonstrates how improved clinical outcomes drive financial results:

Ensign’s disciplined approach to acquisitions has proven effective in driving growth. The company targets underperforming facilities and implements its local leadership model to improve operations. This strategy has resulted in significant increases in skilled mix revenue and EBITDAR margins over time, as facilities mature under Ensign’s management.

Real Estate Portfolio & Standard Bearer REIT

A significant component of Ensign’s business model is its real estate strategy. The company has established Standard Bearer, a captive REIT structure that provides increased visibility, expanded acquisition opportunities, and capital flexibility.

The following chart provides a breakdown of Ensign’s real estate portfolio, showing that 28.6% of facilities are owned and operated by the company, while the remainder are under various lease arrangements:

Standard Bearer REIT has grown substantially, now managing 137 properties with a real estate fair value of $1.5 billion across 16 states. The REIT structure provides Ensign with strategic advantages, including the ability to separate real estate ownership from operations and create additional value for shareholders.

The following slide illustrates key metrics for Standard Bearer:

The REIT maintains strong long-term leases with a weighted average lease tenor of 14.3 years, providing stability and predictable cash flows. The tenant rent coverage ratios remain healthy, as shown in the following chart:

Financial Outlook & Forward-Looking Statements

Ensign has demonstrated consistent revenue and EBITDAR growth, with a 15% CAGR for revenue and 16% CAGR for adjusted EBITDAR since 2014. This long-term growth trajectory is illustrated in the following chart:

Based on strong Q1 results and positive operational trends, Ensign has raised its 2025 guidance. The company now expects annual revenue between $4.89 billion and $4.94 billion, with diluted adjusted EPS between $6.22 and $6.38. This represents a 15% increase over 2024 and a 32% increase over 2023 at the midpoint.

Ensign’s shareholder returns have been exceptional, with a total return of 1,263% over the past 10 years and 3,431% since its IPO in 2007. The following chart illustrates this impressive performance:

The company maintains a strong balance sheet with $282.7 million in cash and cash equivalents as of March 31, 2025, and $572.1 million available under its credit facility. The net debt to adjusted EBITDAR ratio stands at 2.13x, indicating a conservative leverage profile that provides flexibility for future growth.

Ensign’s continued success is driven by its unique culture, local leadership model, strategic positioning across the care continuum, and disciplined approach to acquisitions. With favorable demographic trends supporting long-term demand for post-acute care services and a fragmented market offering consolidation opportunities, Ensign appears well-positioned to continue its growth trajectory in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.