German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

Thomson Reuters (NYSE:TRI) reported its first-quarter 2025 results on May 1, demonstrating continued momentum with 6% organic revenue growth and particularly strong performance in its core business segments. The company maintained its full-year guidance while highlighting its ongoing strategic shift toward higher-growth products.

The information services provider reported a slight decline in adjusted EBITDA margin but showed modest improvements in adjusted earnings per share and free cash flow. Thomson Reuters continues to benefit from its resilient business model, with recurring revenue comprising over 80% of total revenue.

In premarket trading following the release, Thomson Reuters shares were down 2.4% to $181.51, after closing at $185.98 on April 30.

Quarterly Performance Highlights

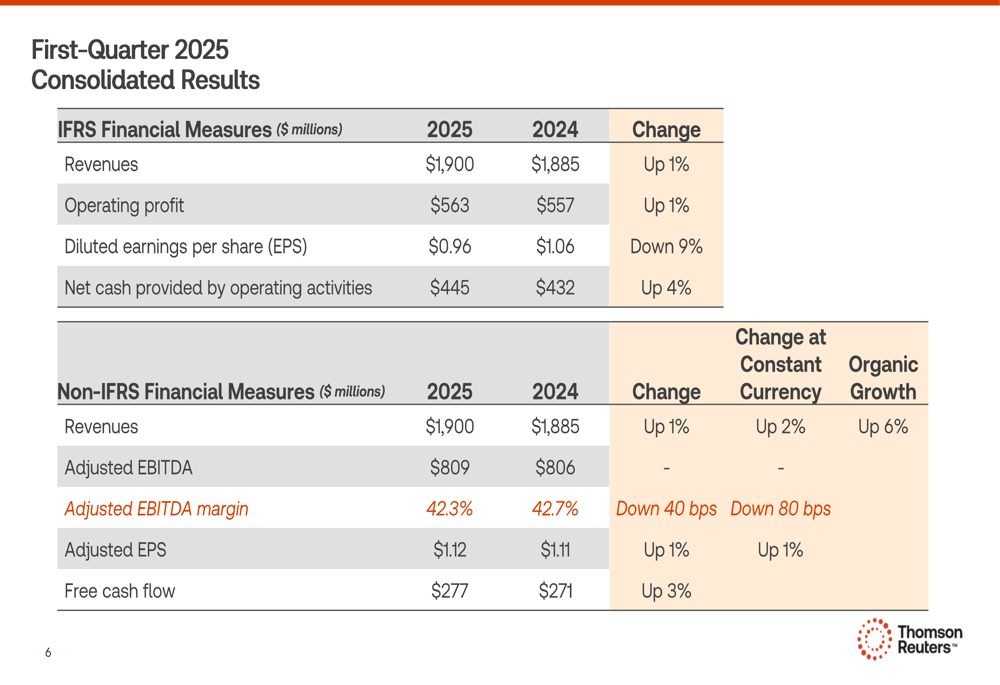

Thomson Reuters reported total revenue of $1.9 billion for Q1 2025, up 1% from the same period last year. Organic revenue growth was 6%, driven by a robust 9% increase in recurring revenue. The company’s adjusted EBITDA was $809 million with a margin of 42.3%, down slightly from 42.7% in Q1 2024.

As shown in the following consolidated results:

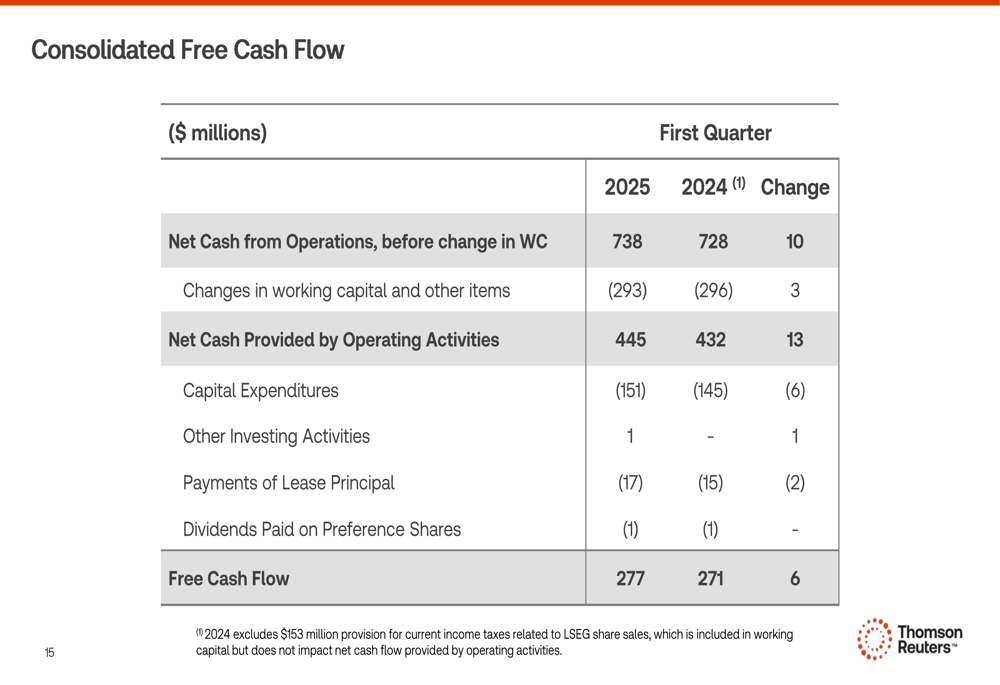

Adjusted earnings per share increased 1% to $1.12, compared to $1.11 in the first quarter of 2024. Free cash flow grew 3% to $277 million. The company’s "Big 3" segments, which include Legal Professionals, Corporates, and Tax & Accounting Professionals, collectively delivered 9% organic growth and represented 84% of total revenue.

Segment Performance Analysis

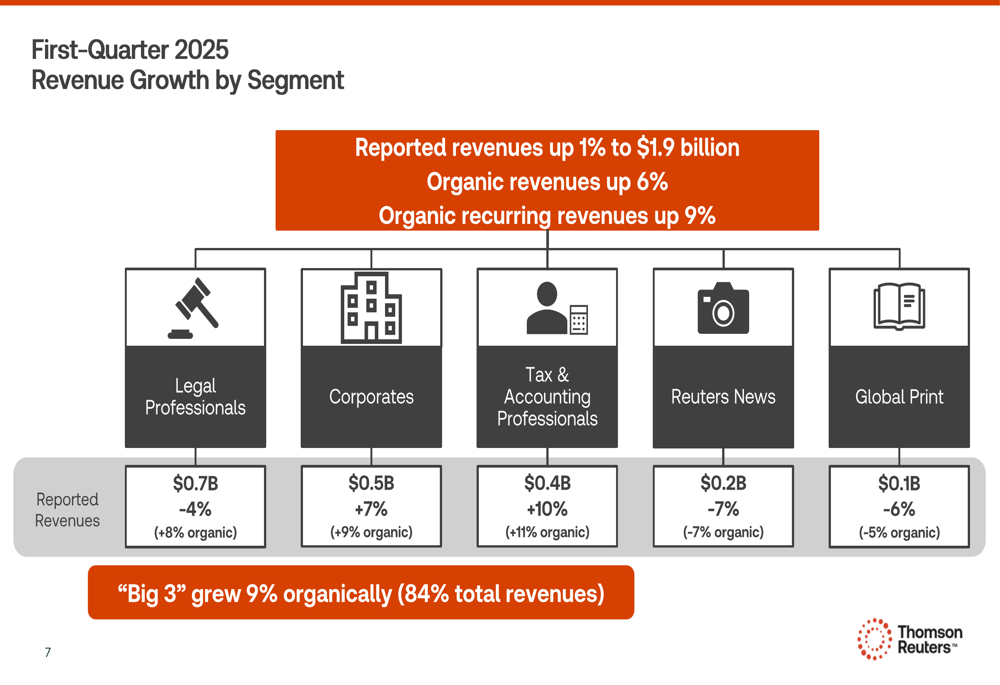

The company’s segment performance showed varying results, with particularly strong organic growth in the core business segments despite some reported revenue declines due to divestitures:

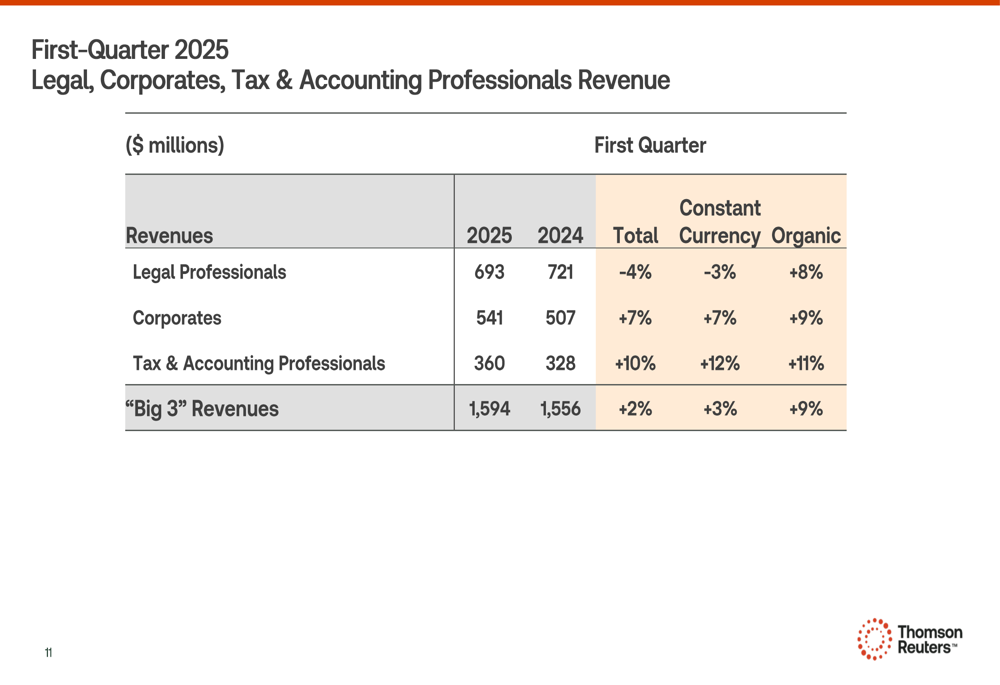

Looking at the "Big 3" segments in detail, Legal Professionals reported revenue of $693 million, down 4% on a reported basis but up 8% organically. The Corporates segment generated $541 million in revenue, increasing 7% on a reported basis and 9% organically. Tax & Accounting Professionals delivered the strongest performance with revenue of $360 million, up 10% on a reported basis and 11% organically.

The detailed segment breakdown shows the strength of these core businesses:

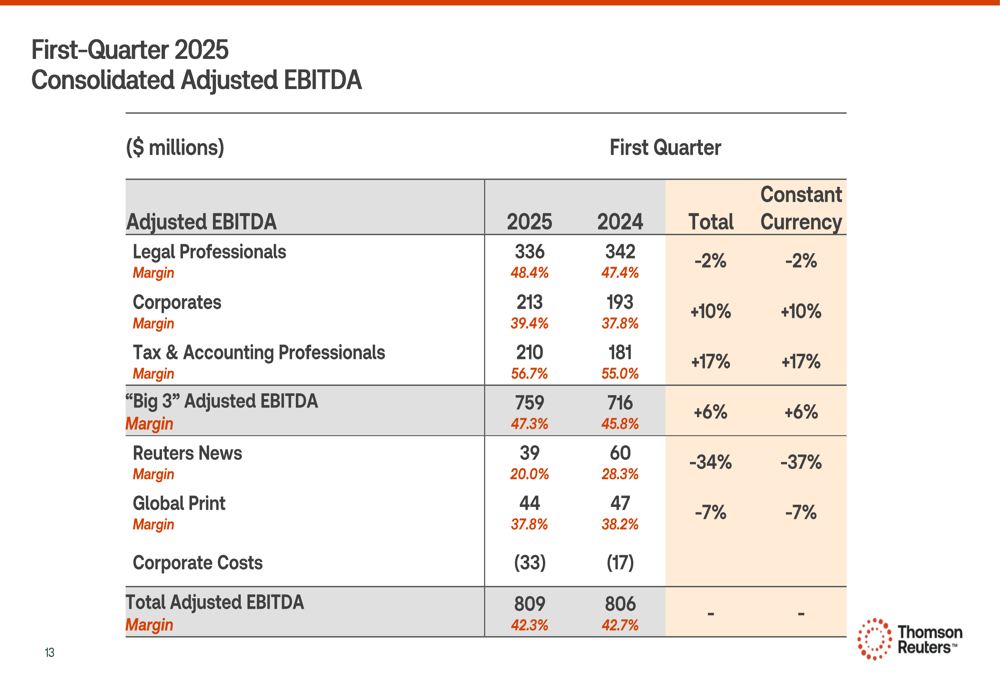

From a profitability perspective, the "Big 3" segments showed improved adjusted EBITDA margins, reaching 47.3% compared to 45.8% in Q1 2024. However, Reuters News saw a significant decline in adjusted EBITDA, falling 34% to $39 million with margin compression to 20.0% from 28.3% in the prior year.

The following chart details the adjusted EBITDA performance by segment:

Strategic Initiatives and Product Innovation

Thomson Reuters continues to execute against its 2025 product innovation roadmap, with a particular focus on AI-powered solutions. During the first quarter, the company launched CoCounsel Tax, Audit & Accounting, and in April added the CoCounsel chat experience to Westlaw and Practical Law.

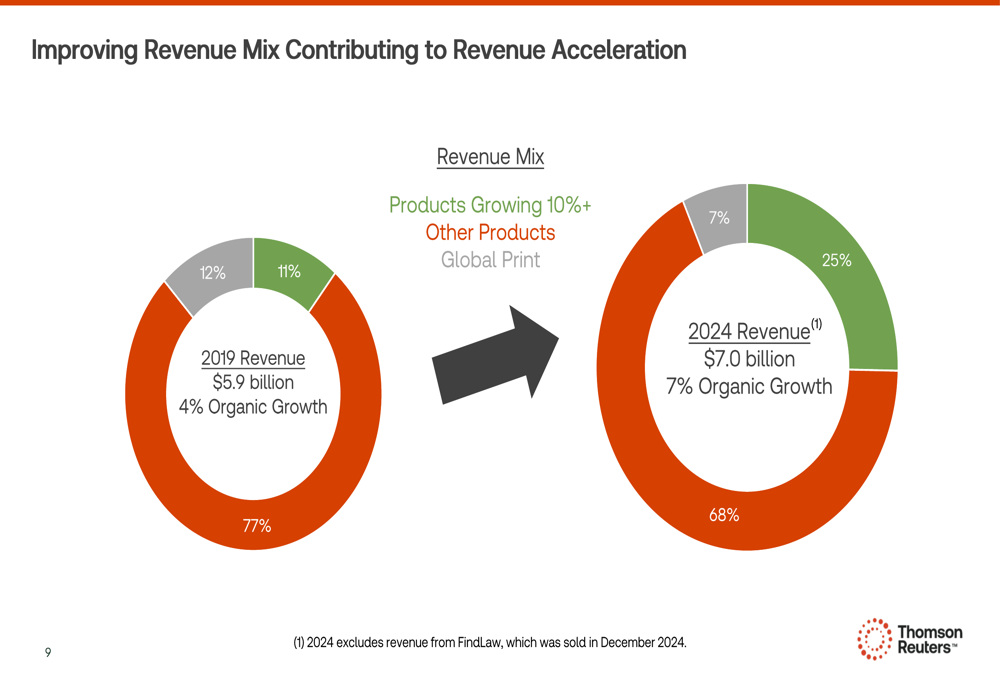

A key strategic focus for Thomson Reuters has been improving its revenue mix to accelerate growth. The company has significantly increased the proportion of higher-growth products in its portfolio, as illustrated in the following chart:

As shown above, products growing at 10%+ rates now represent 25% of total revenue, up from just 12% in 2019. This strategic shift has helped Thomson Reuters increase its organic growth rate from 4% in 2019 to 7% in 2024.

The company completed the acquisition of SafeSend for approximately $600 million in January 2025, further strengthening its portfolio. This follows the company’s Q4 2024 divestiture of FindLaw, which according to the previous earnings report was sold to Internet Brands for up to $410 million.

Financial Position and Outlook

Thomson Reuters maintains a strong financial position with net leverage of 0.6x as of March 31, 2025. The company estimates it will have approximately $10 billion of capital capacity by 2027, providing substantial flexibility for additional M&A activity and shareholder returns.

In February 2025, Thomson Reuters increased its common share dividend by 10% to $2.38, reflecting confidence in its financial strength and future prospects.

The company’s free cash flow calculation shows solid performance:

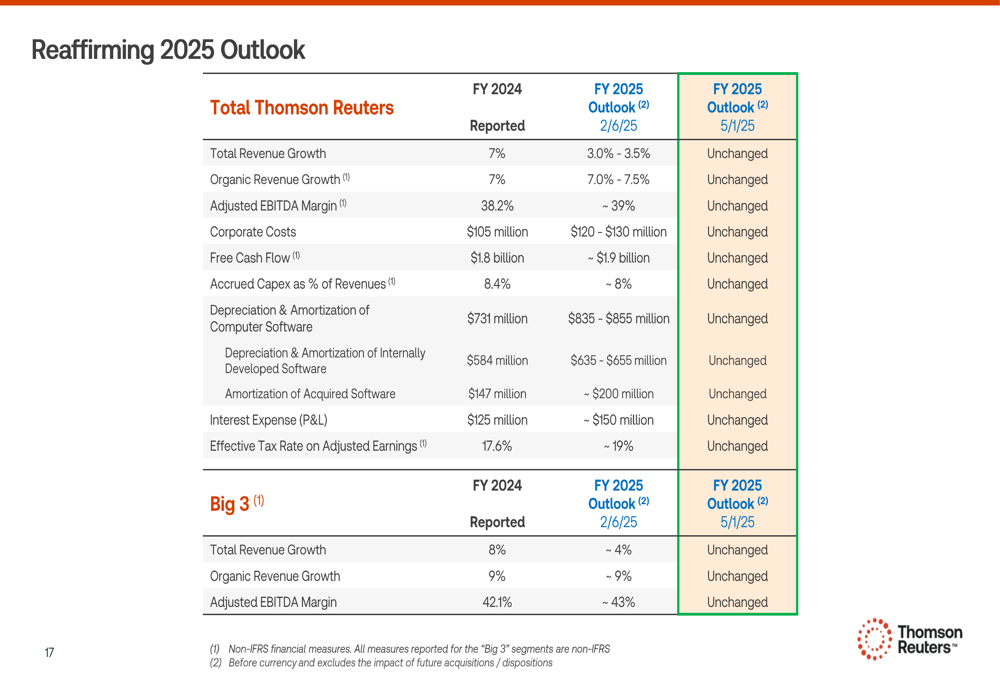

Based on its Q1 performance, Thomson Reuters has reaffirmed its full-year 2025 guidance across all key metrics:

The outlook includes expectations for 7.0-7.5% organic revenue growth for the total company and 9% for the "Big 3" segments. Adjusted EBITDA margin is projected to reach approximately 39% for the full year, up from 38.2% in 2024.

This guidance aligns with the company’s performance trajectory from late 2024, when it had raised its full-year organic revenue growth forecast to approximately 7%. The continued strong performance of the "Big 3" segments remains central to Thomson Reuters’ growth strategy as it continues to invest in product innovation and strategic acquisitions while maintaining its leadership positions in stable, attractive markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.