Berkshire Hathaway reveals $4.3 billion stake in Alphabet, cuts Apple

Introduction & Market Context

Thomson Reuters (NYSE:TRI) released its third-quarter 2025 results on November 4, showcasing solid organic growth across its core business segments despite a challenging market reaction. The company’s stock fell 5.33% to $155.72 following the announcement, with premarket trading showing a slight recovery of 0.28%.

The information and analytics provider continues to emphasize its strategic investments in artificial intelligence while highlighting the competitive advantage of its extensive content library, particularly in its legal segment. The quarter’s performance reflects Thomson Reuters’ ongoing transformation into a content-enabled technology company.

Quarterly Performance Highlights

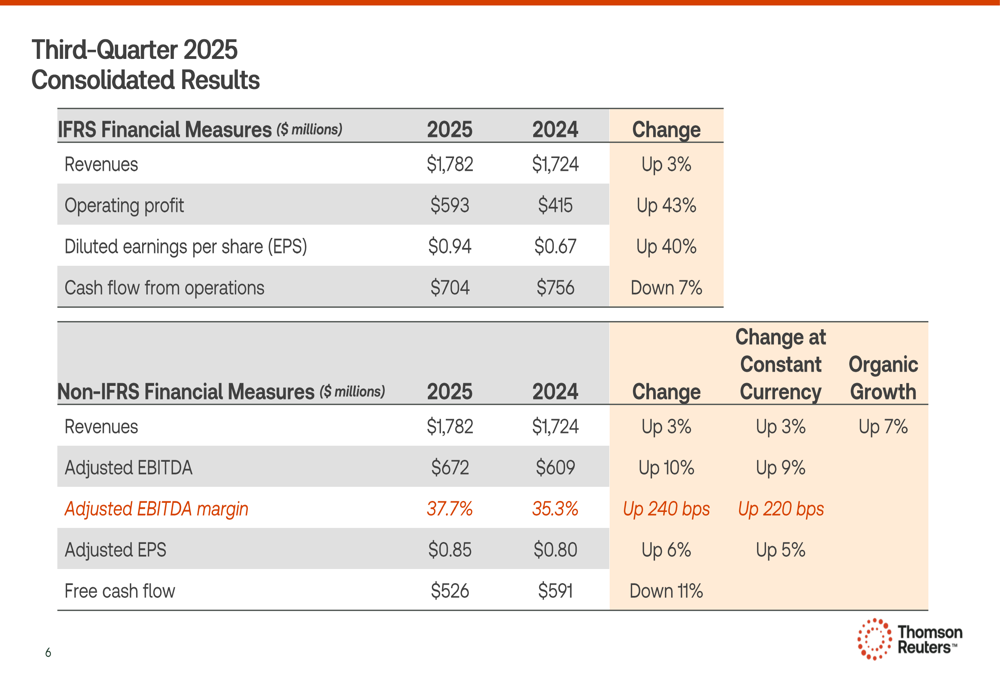

Thomson Reuters reported 7% organic revenue growth in the third quarter of 2025, driven by 9% recurring revenue growth. The company’s adjusted EBITDA increased 10% to $672 million, with margins expanding by 240 basis points to 37.7% compared to 35.3% in the same period last year.

As shown in the following consolidated results summary:

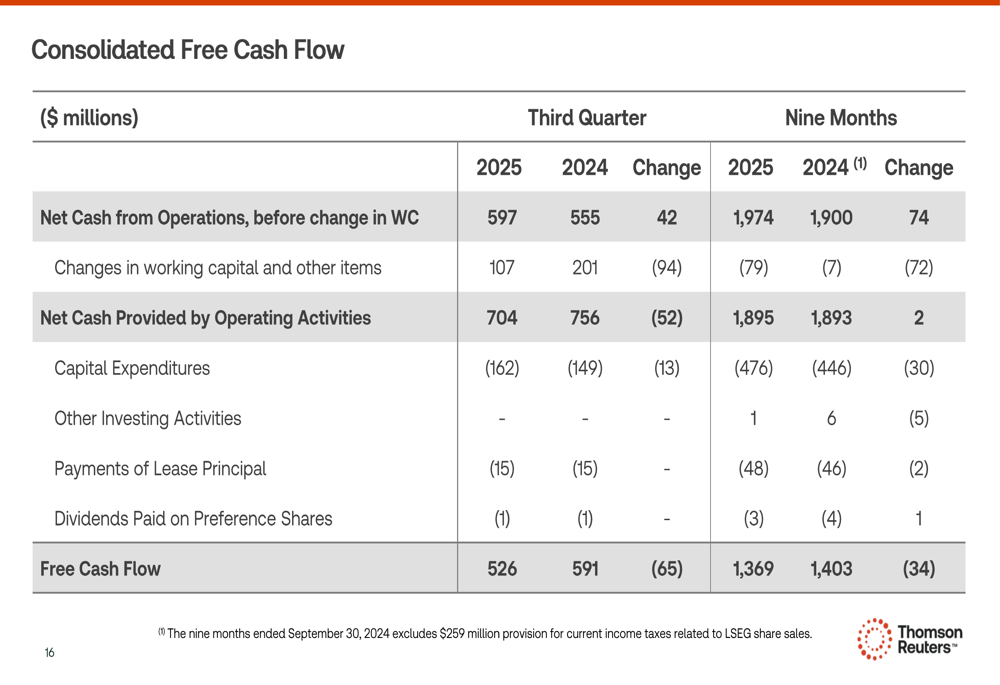

Adjusted earnings per share rose 6% to $0.85 from $0.80 in Q3 2024, while reported revenues increased by a more modest 3% to $1.78 billion, reflecting the impact of divestitures. Free cash flow declined 11% to $526 million, compared to $591 million in the prior year period, potentially contributing to investor concerns despite the otherwise strong operational performance.

The company completed a $1 billion share repurchase program in October and maintains a strong balance sheet with net leverage of 0.6x as of September 30, providing approximately $9 billion of capital capacity by 2027 for potential acquisitions and shareholder returns.

Segment Performance Analysis

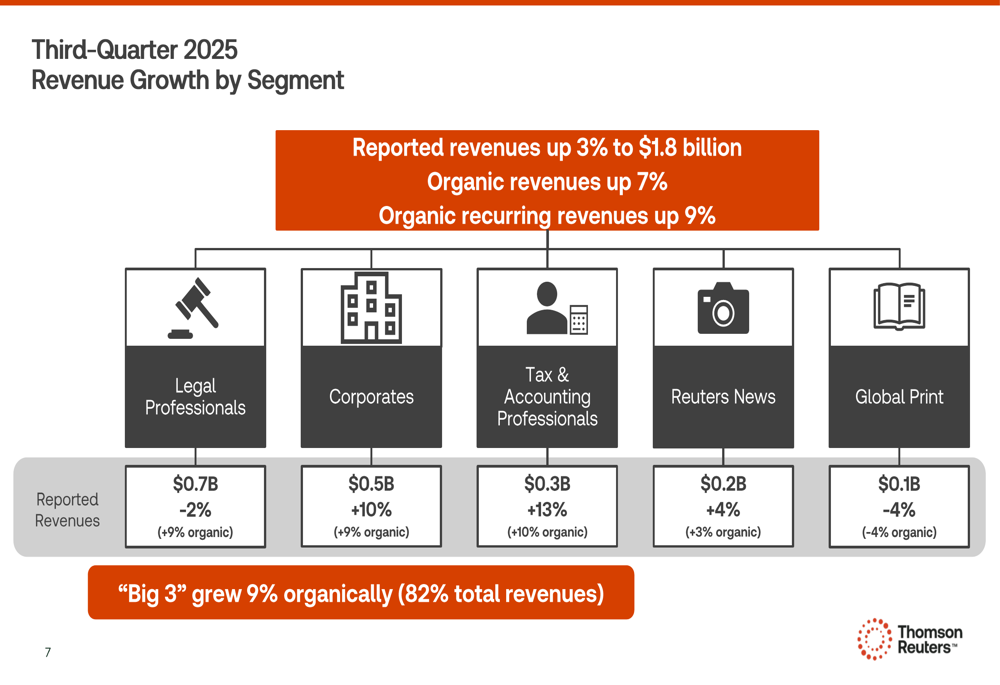

The "Big 3" segments—Legal Professionals, Corporates, and Tax & Accounting Professionals—which represent 82% of total revenues, collectively delivered 9% organic growth. The breakdown of revenue by segment shows varied performance:

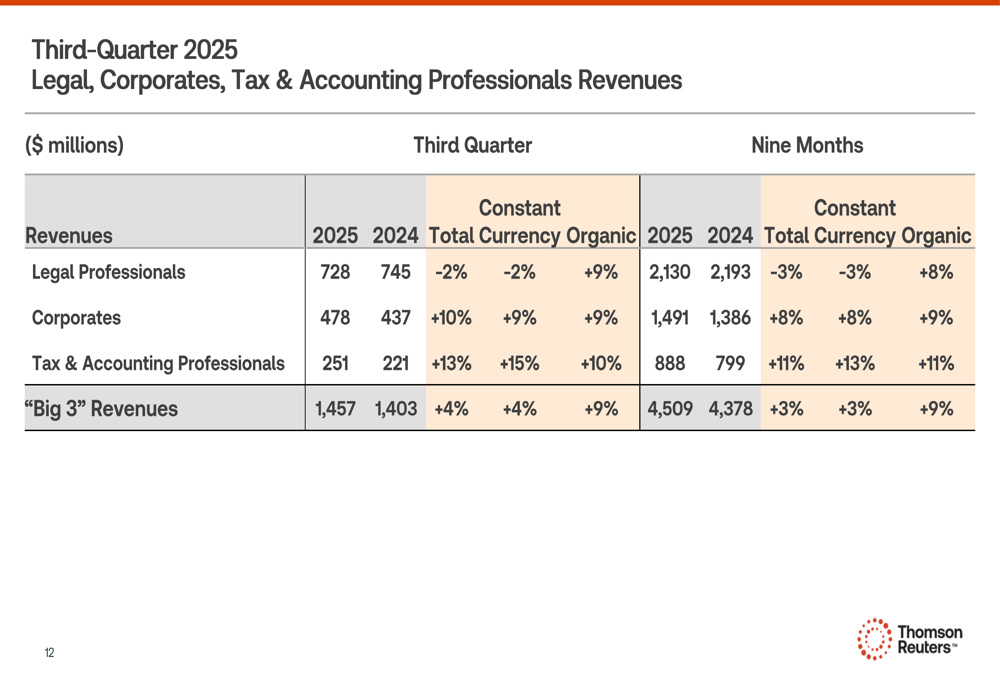

Legal Professionals, the company’s largest segment, achieved 9% organic growth despite a 2% decline in reported revenues due to divestitures. The Corporates segment posted 10% reported revenue growth and 9% organic growth. Tax & Accounting Professionals demonstrated the strongest performance with 13% reported revenue growth and 10% organic growth.

A detailed look at the segment revenue performance reveals consistent strength across these core business areas:

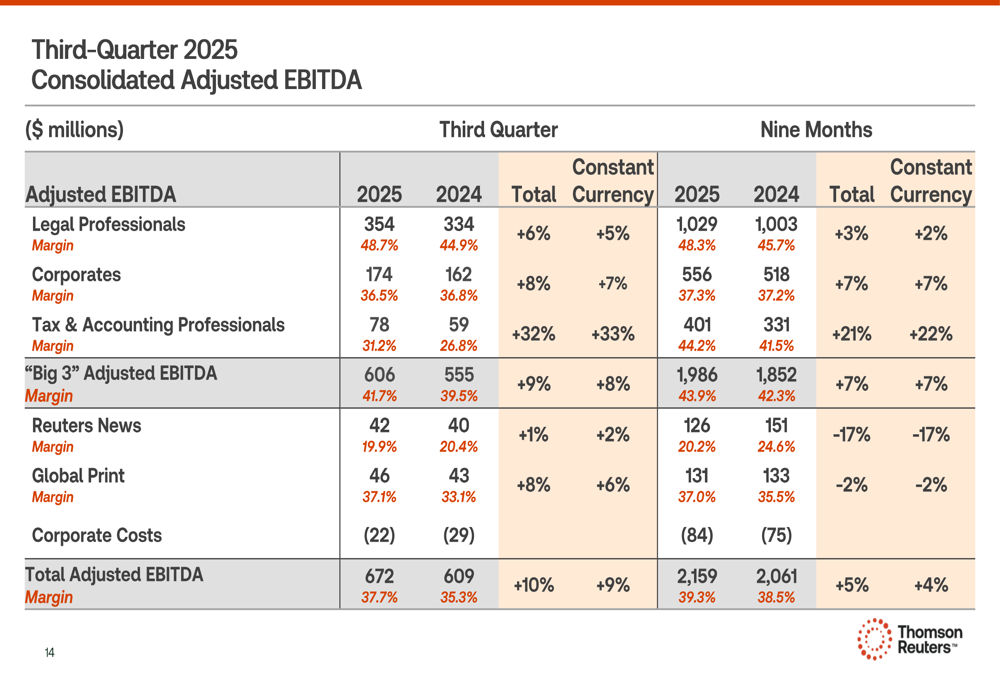

On the profitability front, all major segments showed margin improvements. The Legal Professionals segment achieved a 48.7% adjusted EBITDA margin, up from 44.9% in Q3 2024. Tax & Accounting Professionals saw the most significant margin expansion, increasing to 31.2% from 26.8% in the prior year.

Strategic Initiatives: AI and Content Focus

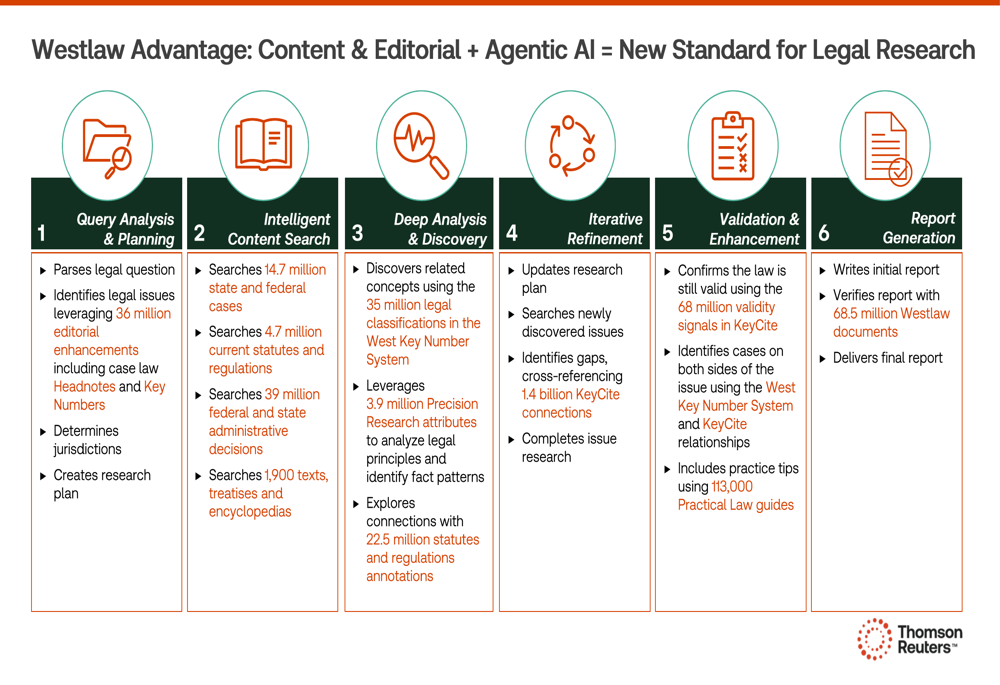

Thomson Reuters continues to emphasize its strategic advantage in combining extensive proprietary content with artificial intelligence capabilities. The company highlighted the differentiation of its Westlaw legal research platform, which contains 1.9 billion documents and processes 300 million documents annually from 3,500+ sources.

The presentation detailed Westlaw’s comprehensive content and editorial capabilities:

Building on this content foundation, Thomson Reuters is integrating advanced AI capabilities to create what it calls the "new standard for legal research." The company’s approach combines its extensive content and editorial expertise with agentic AI to enhance user workflows:

During the earnings call, CEO Steve Hasker noted, "We’re seeing our customers wrestle with spending more on technology and potentially less on real estate," reflecting the broader industry trend toward digital transformation and AI-powered solutions.

Updated Outlook and Financial Framework

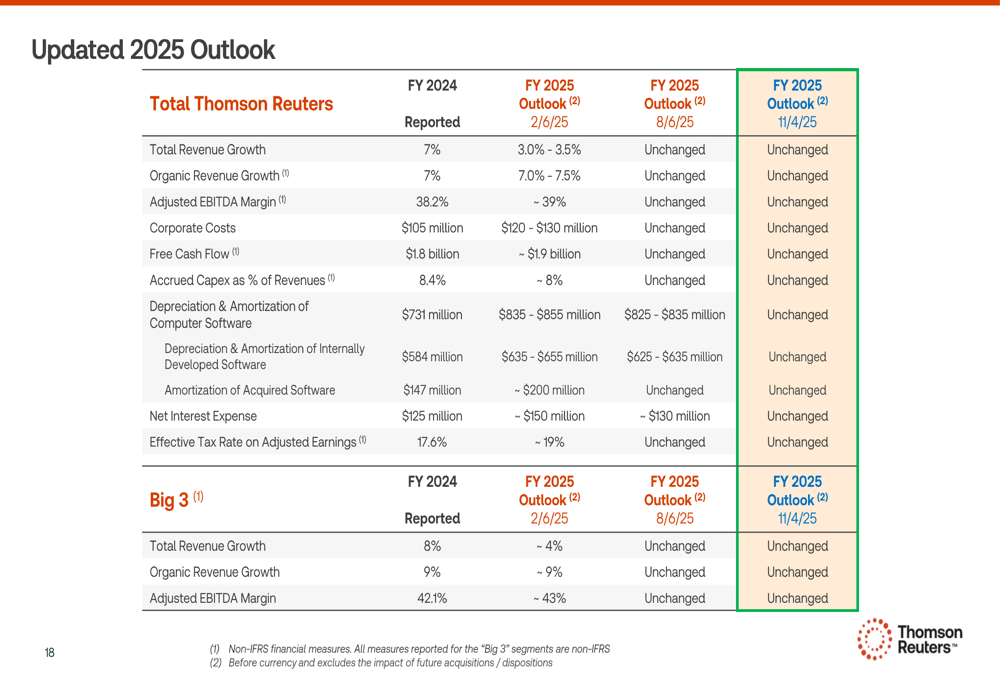

Thomson Reuters reaffirmed its full-year 2025 outlook while noting that total and organic revenue are trending toward the lower end of the previously provided ranges of 3.0-3.5% and 7.0-7.5%, respectively. The "Big 3" segments are still expected to deliver approximately 9% organic growth for the year.

The company provided the following updated outlook for 2025:

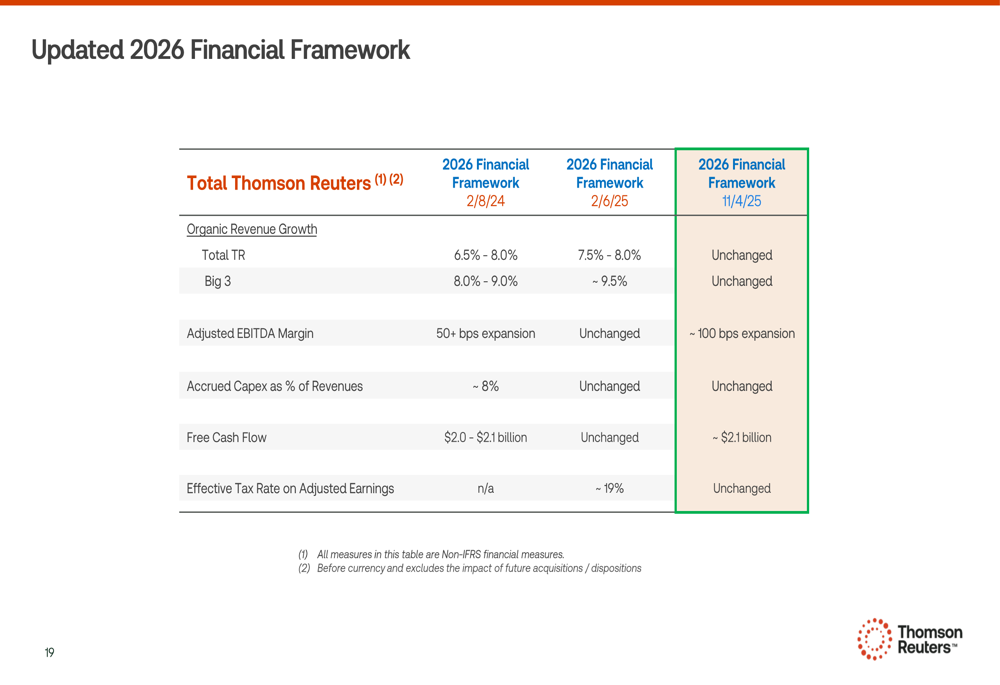

More notably, Thomson Reuters upgraded its 2026 financial framework, increasing its adjusted EBITDA margin expansion target to approximately 100 basis points, up from the previous target of 50+ basis points. The company also narrowed its free cash flow projection to approximately $2.1 billion, from the prior range of $2.0-$2.1 billion.

CFO Mike Eastwood emphasized during the call, "We will continue to invest wherever we see sufficient returns," highlighting the company’s strategic focus on balancing growth investments with profitability improvements.

Market Response and Challenges

Despite the solid operational performance and improved outlook, Thomson Reuters’ stock declined 5.33% following the earnings release. This reaction may reflect investor concerns about several challenges mentioned during the earnings call, including:

1. Talent shortages in the tax and accounting sectors

2. Increasing competition in AI-powered professional services

3. Potential macroeconomic headwinds affecting client spending

4. Challenges in securing government contracts

5. The complexity and cost of integrating AI into existing workflows

The slight decline in free cash flow, despite EBITDA growth, may also have contributed to investor caution. The company’s free cash flow for the first nine months of 2025 was down compared to the same period in 2024:

Nevertheless, Thomson Reuters’ strong organic growth, margin expansion, and improved long-term outlook suggest the company remains well-positioned to capitalize on the increasing demand for AI-powered information services in its core professional markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.