Nvidia’s results, Indian tariffs, French markets - what’s moving markets

Introduction & Market Context

Thryv Holdings Inc (NASDAQ:THRY) presented its first quarter 2025 results on May 1, highlighting the company’s continued transformation from a marketing services provider to a SaaS-focused business. The company reported that SaaS revenue now represents 61.3% of total revenue, marking a significant milestone in its strategic shift. This transition comes as Thryv continues to integrate its Keap acquisition, completed in October 2024, which has substantially expanded its subscriber base and product offerings.

The company’s stock closed at $13.70 on April 30, 2025, significantly below its 52-week high of $26.42, suggesting investors may still be assessing the long-term impact of the company’s transformation strategy despite the strong SaaS growth metrics.

Quarterly Performance Highlights

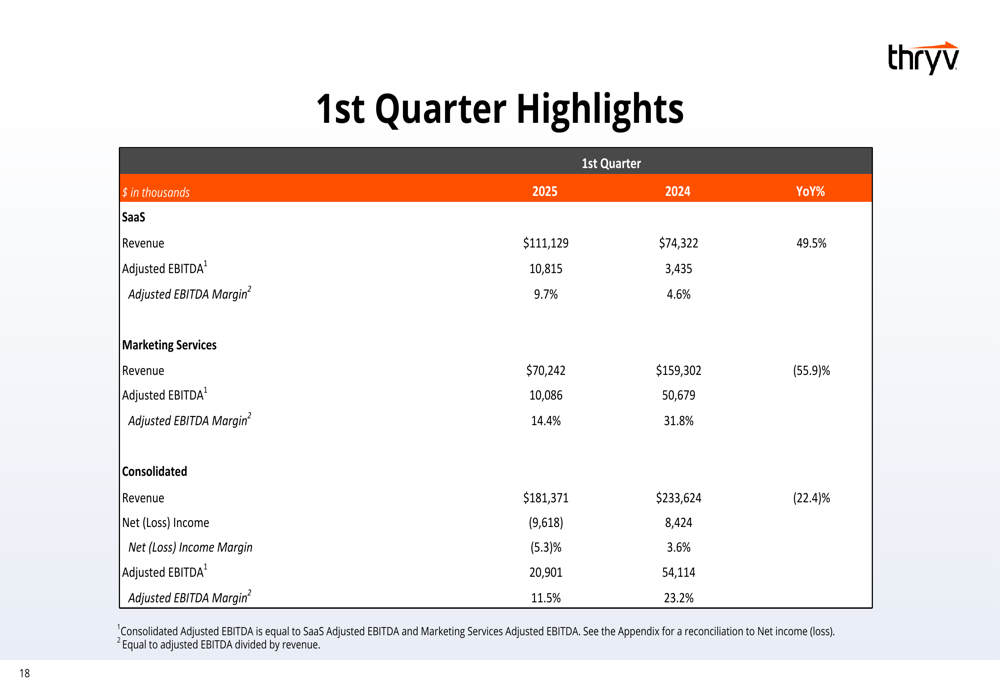

Thryv reported consolidated revenue of $181.4 million for Q1 2025, representing a 22.4% decrease from $233.6 million in Q1 2024. However, this decline was driven by the planned reduction in the company’s legacy marketing services business, which fell 55.9% year-over-year to $70.2 million.

The company’s SaaS segment demonstrated robust growth, with revenue increasing 49.5% year-over-year to $111.1 million, compared to $74.3 million in Q1 2024. This growth was supported by both the Keap acquisition and organic expansion.

As shown in the following financial summary:

SaaS adjusted EBITDA reached $10.8 million (9.7% margin) in Q1 2025, up from $3.4 million (4.6% margin) in Q1 2024. However, the company reported a net loss of $9.6 million for the quarter, compared to net income of $8.4 million in the same period last year, reflecting the costs associated with its ongoing transformation and integration efforts.

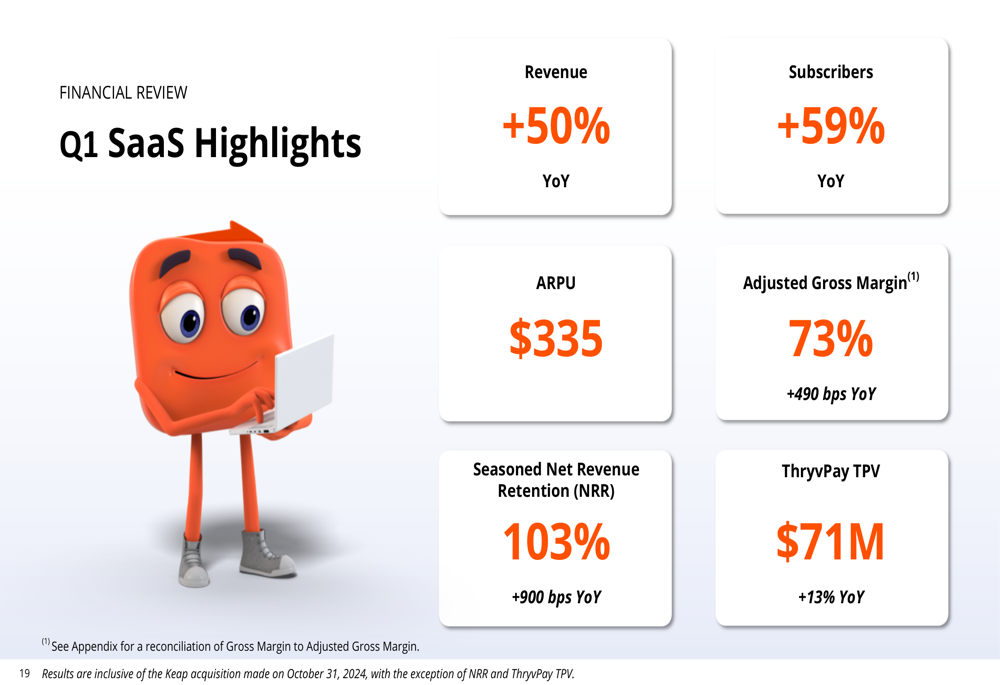

The SaaS segment showed impressive operational metrics, including substantial subscriber growth and improved profitability:

Strategic Initiatives

Thryv’s strategic focus remains on expanding its SaaS platform capabilities while managing the decline of its marketing services business. The company highlighted its key investment thesis, emphasizing its best-in-class SaaS platform, massive market opportunity, and efficient customer acquisition strategy.

The following slide outlines Thryv’s key investment highlights, including its growing AI capabilities and high-margin recurring revenue potential:

The acquisition of Keap in October 2024 has significantly enhanced Thryv’s market position, bringing the total subscriber count to over 100,000 SaaS users. This acquisition has also strengthened Thryv’s partner channel capabilities, creating cross-selling opportunities across both customer bases.

Thryv continues to innovate its product offerings, with a clear roadmap for expansion. The company has introduced several new products and centers, including the Thryv Reporting Center in 2025 and the upcoming Thryv Workforce Center:

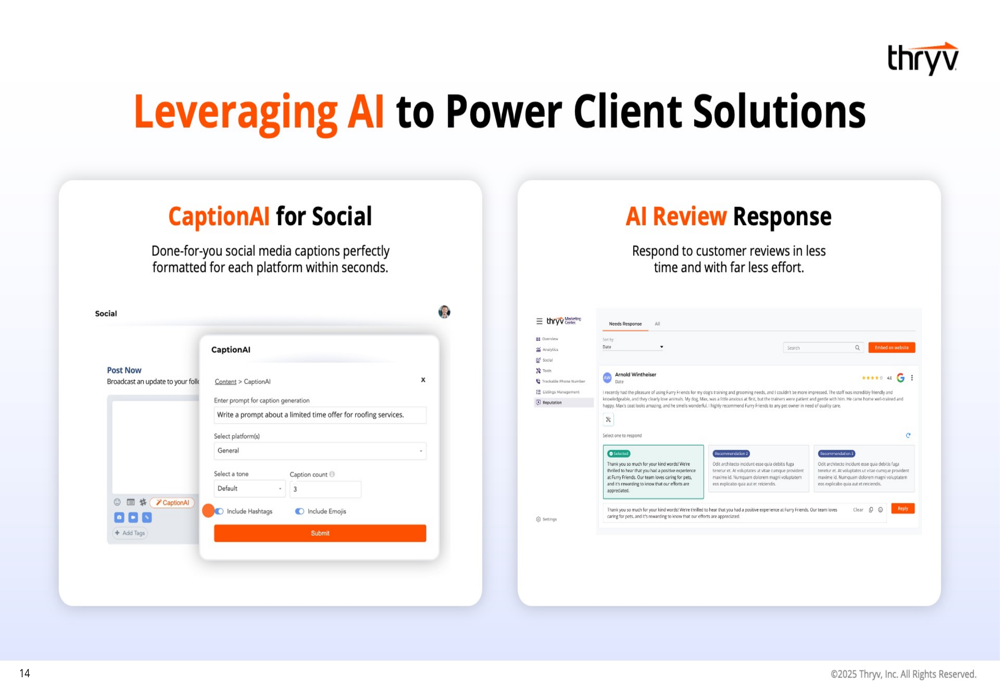

The company is also leveraging artificial intelligence to enhance its platform capabilities, particularly in areas such as social media content generation and customer review responses:

Market Positioning and Opportunity (SO:FTCE11B)

Thryv positions itself in the mid-market segment, targeting businesses with annual software spending of over $8,000. This places the company between enterprise solutions like Salesforce (NYSE:CRM) ($100,000+) and basic tools like Square and Mailchimp (under $2,000).

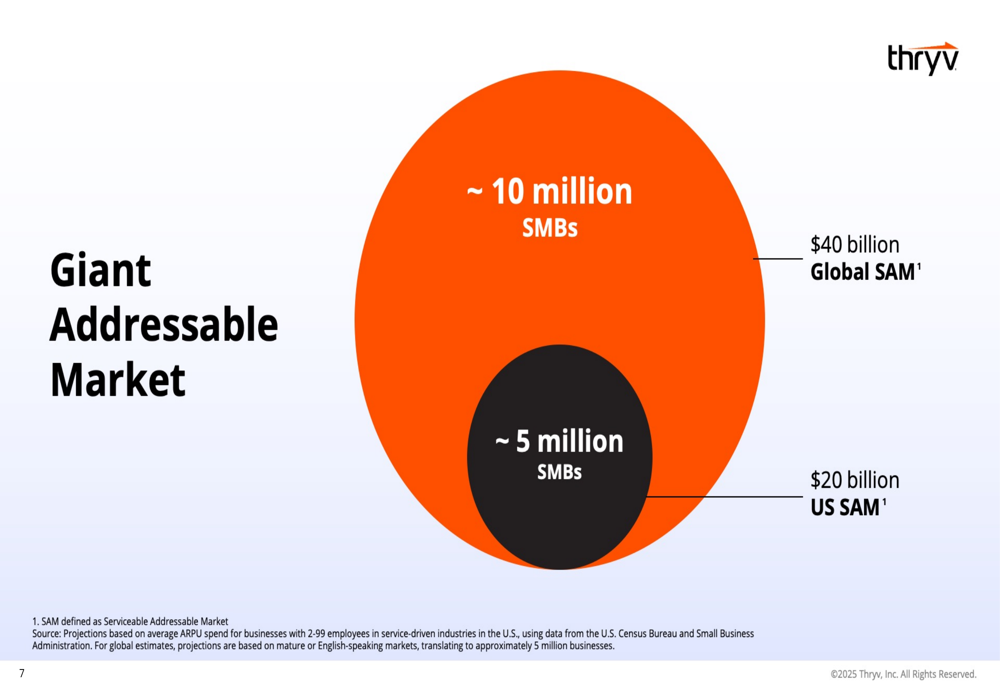

The company estimates its global serviceable addressable market (SAM) at approximately 10 million small and medium-sized businesses with $40 billion in annual spend, with the US market representing about half of that opportunity:

Thryv’s market credibility is reinforced by numerous industry accolades, including recognition as a Global Most Loved Workplace in Newsweek’s 2024 list and multiple G2 Leader Awards:

Forward-Looking Statements

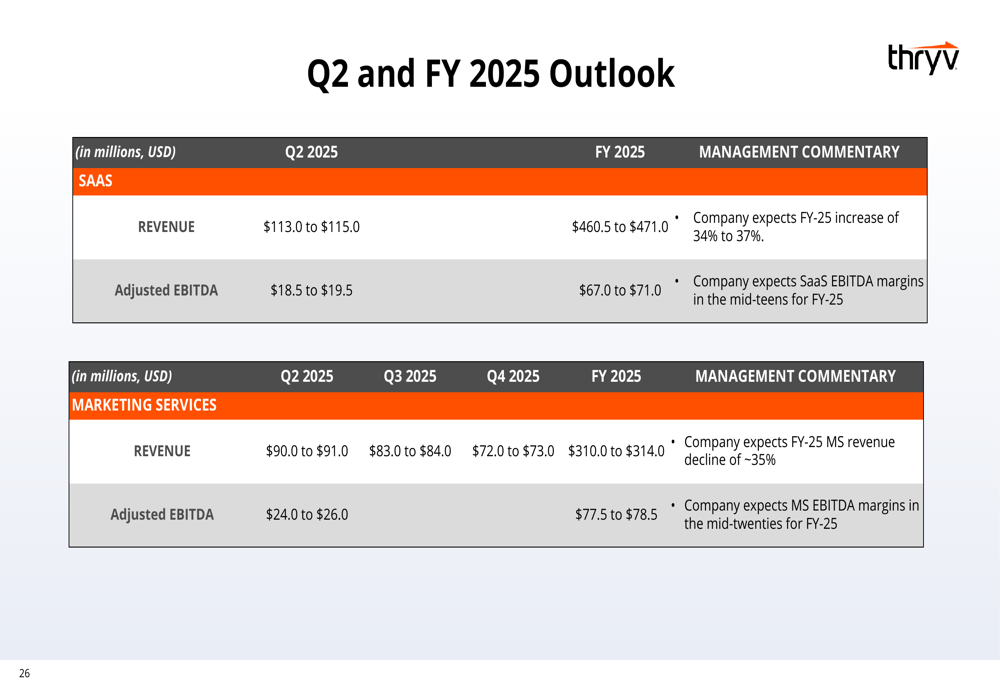

For Q2 2025, Thryv expects SaaS revenue between $113.0 and $115.0 million, representing 34-37% year-over-year growth. The company anticipates SaaS adjusted EBITDA to be between $18.5 and $19.5 million for the quarter.

For the full year 2025, Thryv projects SaaS adjusted EBITDA margins in the mid-teens, while Marketing Services revenue is expected to continue its planned decline:

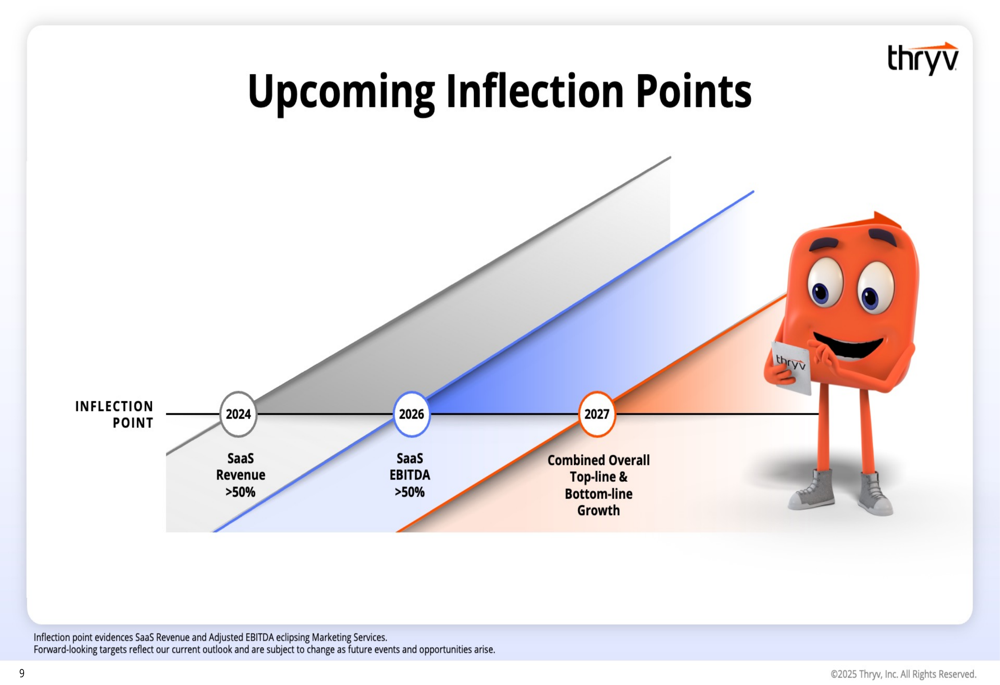

The company outlined several upcoming inflection points in its transformation journey, including SaaS revenue exceeding 50% of total revenue in 2024 (already achieved), SaaS EBITDA exceeding 50% of total EBITDA by 2026, and combined overall top-line and bottom-line growth by 2027:

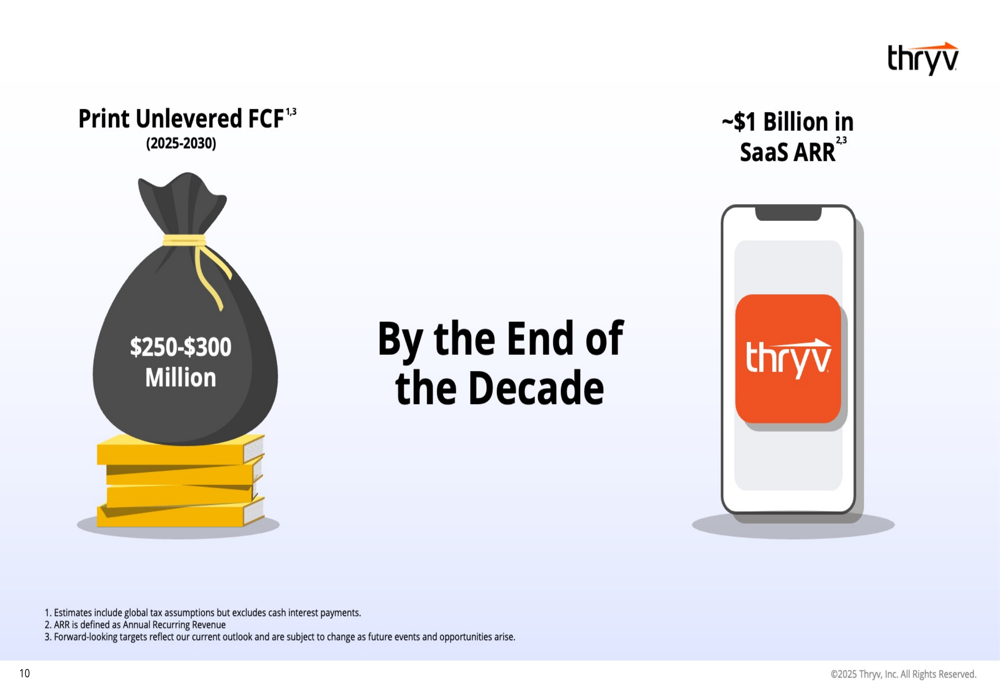

Looking further ahead, Thryv has set ambitious long-term financial targets, including approximately $1 billion in SaaS annual recurring revenue (ARR) by the end of the decade, and $250-300 million in print unlevered free cash flow between 2025-2030:

Conclusion

Thryv’s Q1 2025 results demonstrate the company’s continued progress in its strategic transformation from a marketing services provider to a SaaS-focused business. With SaaS now representing over 61% of total revenue, the company has reached a significant milestone in this journey. The Keap acquisition has accelerated this transition, contributing to substantial growth in subscribers and revenue.

While the company faces challenges, including a net loss for the quarter and ongoing integration efforts, the improving SaaS margins and strong subscriber growth suggest positive momentum. As Thryv continues to expand its product offerings and leverage AI capabilities, it remains focused on capturing a larger share of the estimated $40 billion global addressable market for small business software solutions.

Investors will be watching closely to see if the company can maintain its SaaS growth trajectory while successfully managing the planned decline of its marketing services business, ultimately achieving its goal of combined top-line and bottom-line growth by 2027.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.