Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

Thryv Holdings Inc (NASDAQ:THRY) presented its Q2 2025 investor slides on July 30, highlighting the company’s accelerating transformation from a marketing services provider to a SaaS-focused business. The quarter marked a significant milestone as SaaS revenue now represents the majority of Thryv’s business, underscoring the success of its strategic pivot.

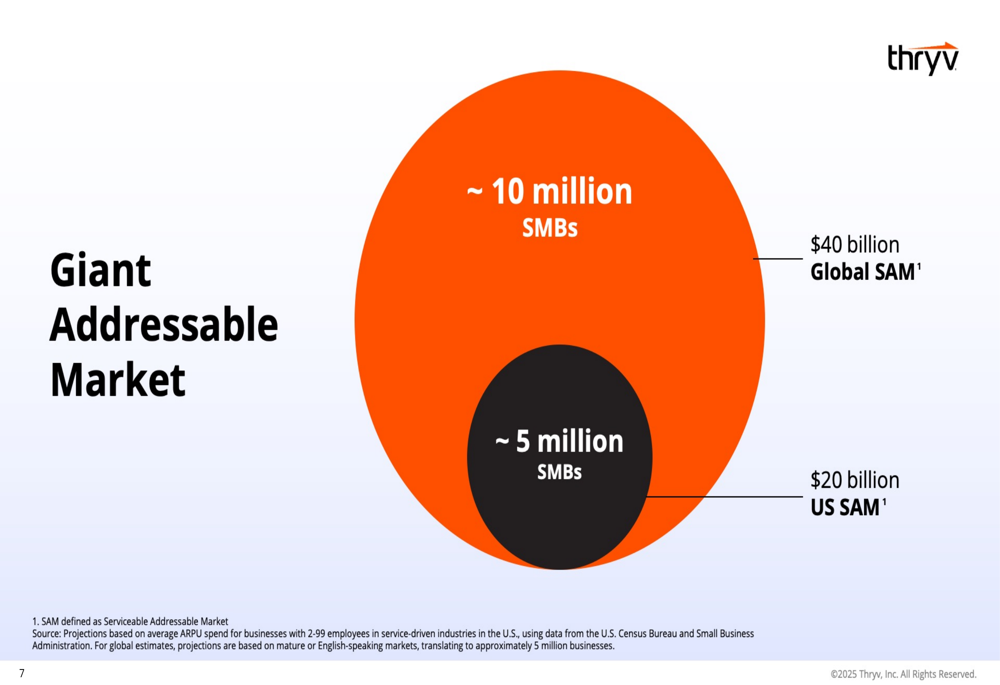

The company is targeting service-based small and medium-sized businesses (SMBs) with 2-99 employees, positioning itself between higher-end solutions like Salesforce (NYSE:CRM) and HubSpot (NYSE:HUBS) and lower-end options such as Square and Mailchimp. According to the presentation, Thryv’s global serviceable addressable market encompasses approximately 10 million businesses with an annual spend potential of $40 billion.

As shown in the following market opportunity visualization:

Quarterly Performance Highlights

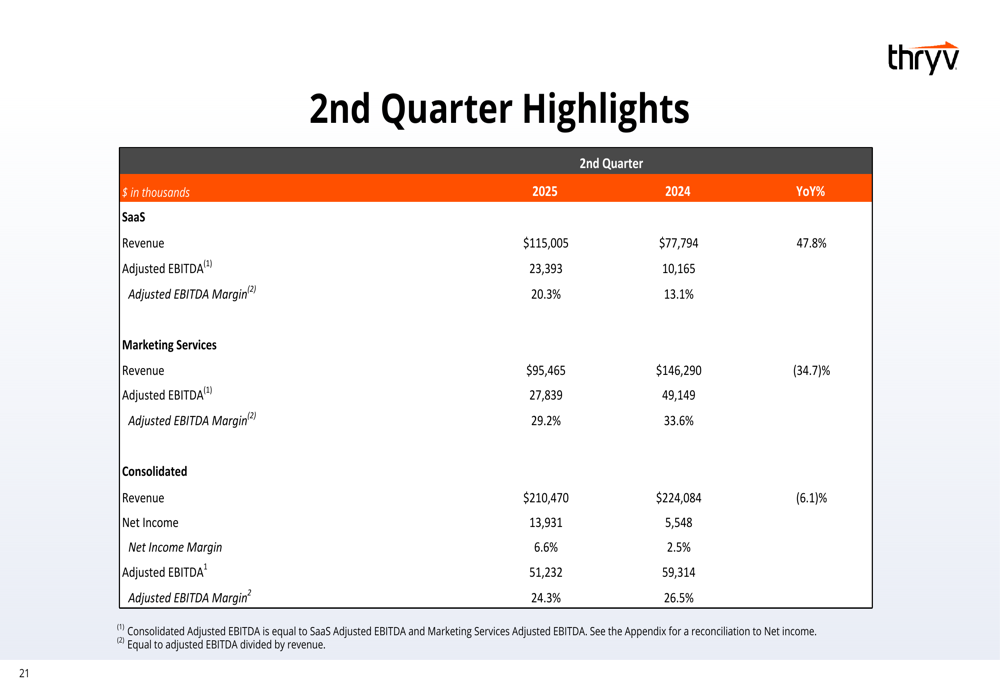

Thryv reported strong financial results for Q2 2025, with SaaS revenue reaching $115 million, a 47.8% year-over-year increase from $77.8 million in Q2 2024. This growth contrasts with the company’s marketing services segment, which declined 34.7% to $95.5 million, resulting in a consolidated revenue decrease of 6.1% to $210.5 million.

The company’s second quarter financial highlights are detailed in the following slide:

Despite the overall revenue decline, Thryv’s profitability metrics showed significant improvement. Net income reached $13.9 million, more than doubling from $5.5 million in the prior year, with net income margin expanding to 6.6% from 2.5%. SaaS adjusted EBITDA grew to $23.4 million with a margin of 20.3%, compared to $10.2 million and 13.1% in Q2 2024.

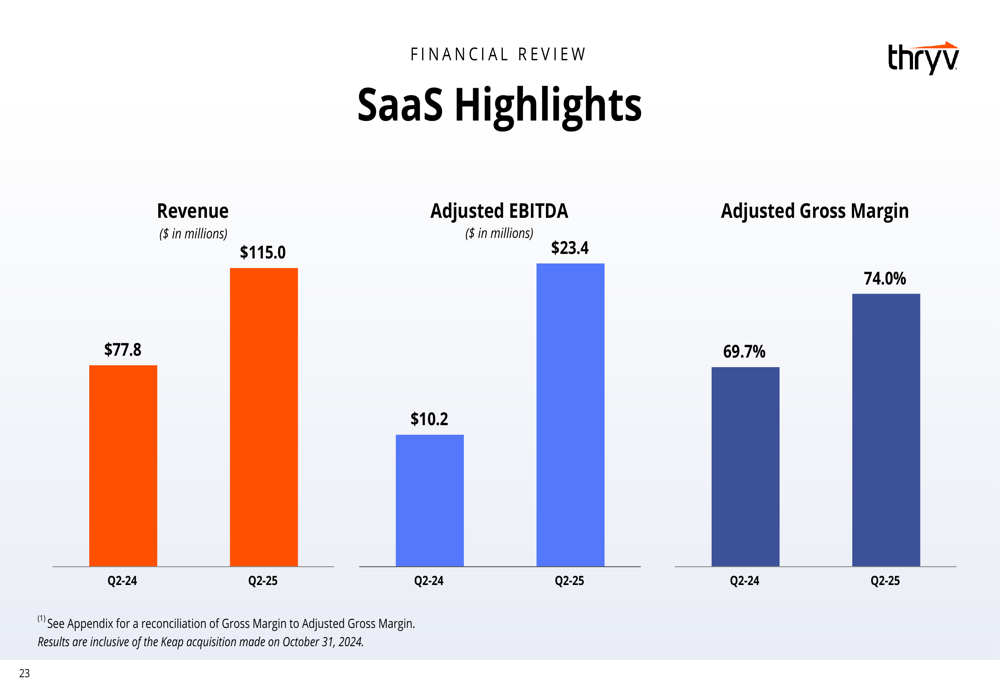

The SaaS segment’s performance was particularly impressive, as illustrated in this highlights slide:

The comparison between Q2 2024 and Q2 2025 SaaS metrics shows substantial growth across key indicators:

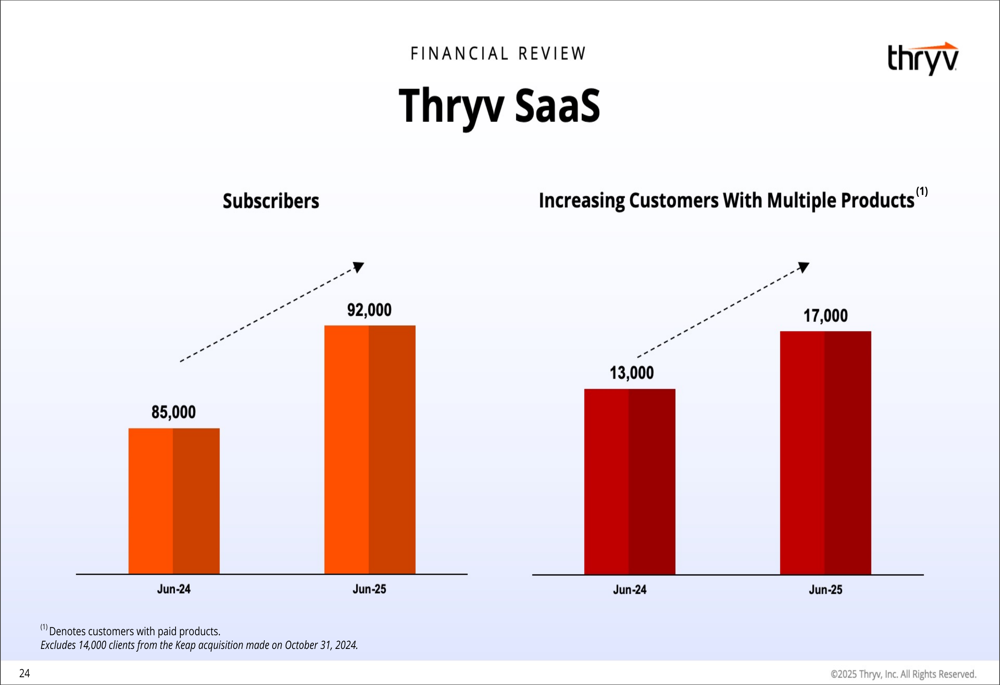

Subscriber growth has been steady, with total SaaS subscribers increasing to 92,000 by June 2025, up 25% year-over-year. Importantly, customers with multiple products grew to 17,000, up from 13,000 a year earlier, indicating successful cross-selling efforts. The presentation notes that these figures exclude 14,000 clients from the Keap acquisition completed in October 2024.

The subscriber growth trend is visualized in the following graph:

Strategic Initiatives

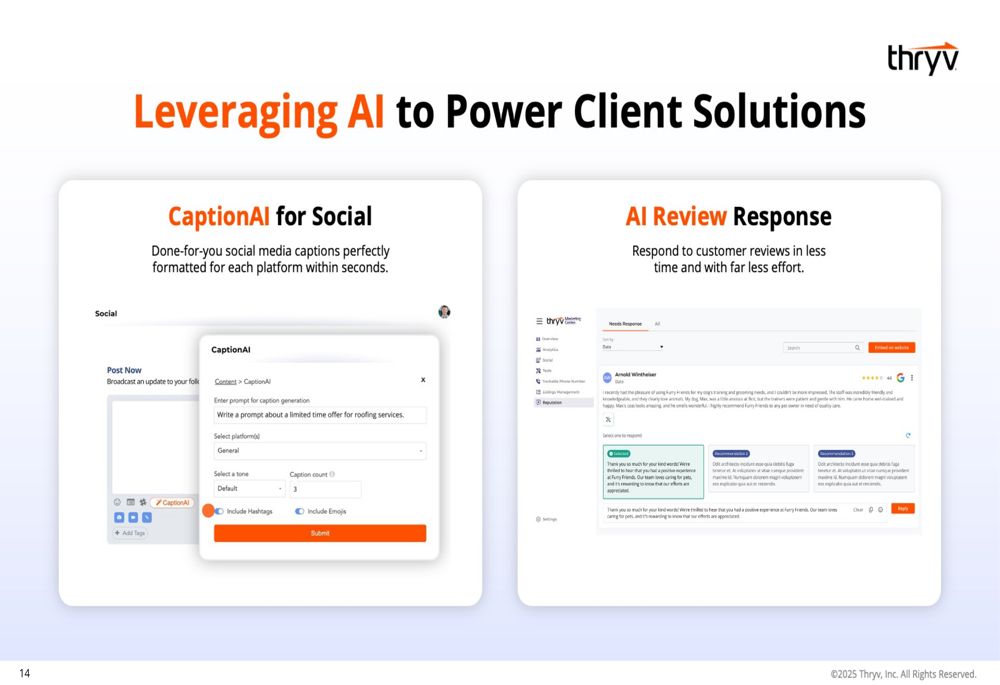

Thryv’s strategic focus includes expanding its product offerings and leveraging AI capabilities to enhance customer value. The company has introduced several new features, including a Workforce Center in 2025, adding to its existing Business Center, Marketing Center, Keap Automations, and Reporting Center.

AI integration is becoming increasingly important to Thryv’s product strategy, as demonstrated by features like CaptionAI for social media content generation and AI-powered review responses:

The company’s platform has demonstrated measurable results for its SMB customers, including a 25% increase in new customers, 61% more appointments booked, $1.3 billion in digital payments collected in 2024, and time savings of over 20 hours per week:

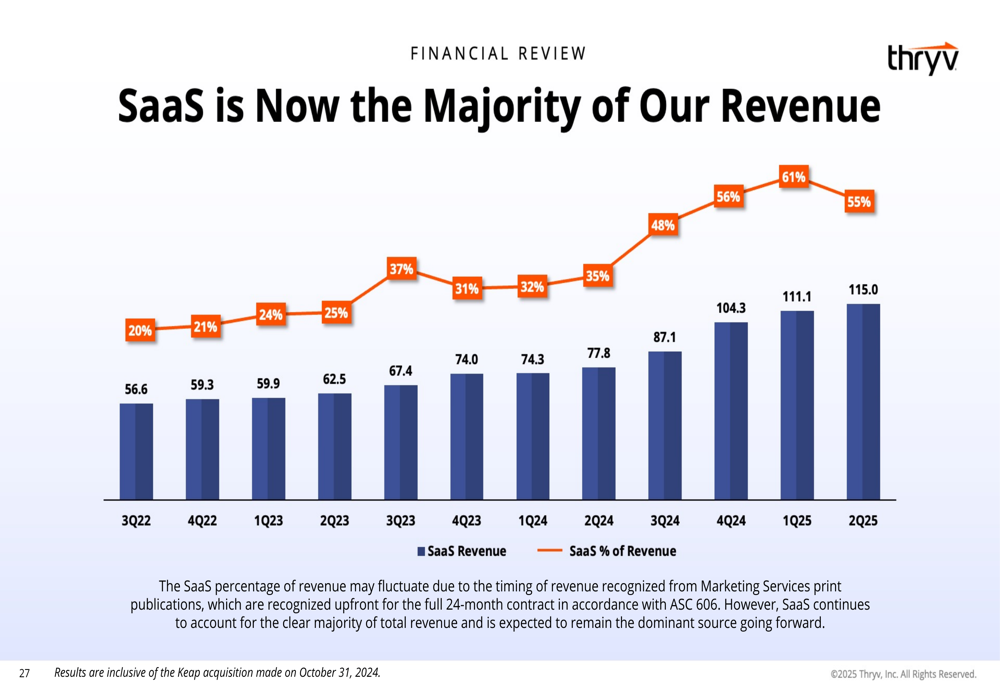

Thryv’s business transformation is evident in the growing proportion of revenue coming from SaaS, which now exceeds 50% of total revenue:

The company has received notable industry recognition, including placement on Newsweek’s list of Top 100 Global Most Loved Workplaces for 2024 and winning the Martech Breakthrough Award 2023 for Best SMB CRM Solution:

Forward-Looking Statements

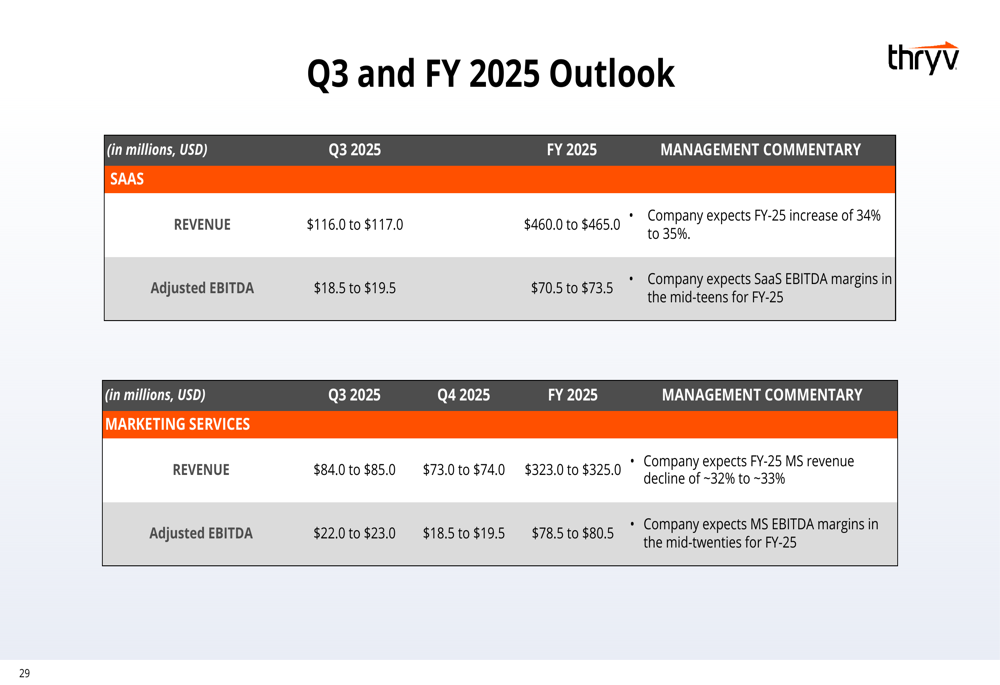

Looking ahead, Thryv provided guidance for Q3 and full-year 2025. For Q3, the company expects SaaS revenue between $116.0 and $117.0 million with adjusted EBITDA of $18.5 to $19.5 million. For the full year, SaaS revenue is projected at $460.0 to $465.0 million with adjusted EBITDA between $70.5 and $73.5 million.

The detailed outlook is presented in this forecast table:

Longer-term, Thryv aims to reach approximately $1 billion in SaaS annual recurring revenue by the end of the decade. The company also projects Print Unlevered Free Cash Flow of $250-$300 million between 2025 and 2030, providing financial flexibility for continued investment in growth initiatives.

The Q2 2025 results represent a significant improvement from Q1 2025, when the company reported an earnings per share loss of $0.22. The turnaround in profitability, combined with the accelerating shift toward SaaS revenue, suggests Thryv’s transformation strategy is gaining momentum despite the stock’s relatively flat performance, trading at $12.14 as of July 29, 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.