U.S. stock futures slip lower; Cook’s firing increases Fed independence worries

Introduction & Market Context

Toll Brothers Inc (NYSE:TOL) released its third quarter 2025 company overview presentation on August 20, 2025, highlighting its performance and strategic positioning in the luxury homebuilding market. The presentation comes as the stock trades at $132.18, with premarket activity showing a decline of 1.54% to $130.14, following a recent earnings beat in Q2 where the company reported EPS of $3.50 versus the forecasted $2.84.

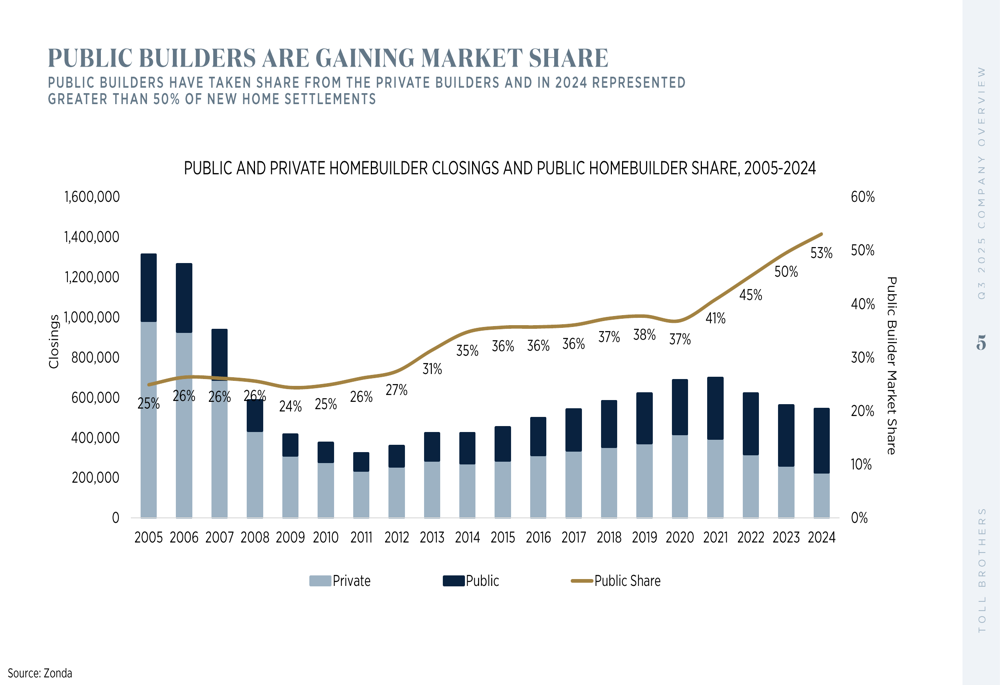

The presentation emphasizes how public homebuilders like Toll Brothers have been steadily gaining market share in an industry characterized by constrained supply and evolving consumer preferences. This trend is illustrated in the company’s analysis of market dynamics, showing public builders now control over half of the new home market.

As shown in the following chart of public versus private homebuilder market share:

Executive Summary

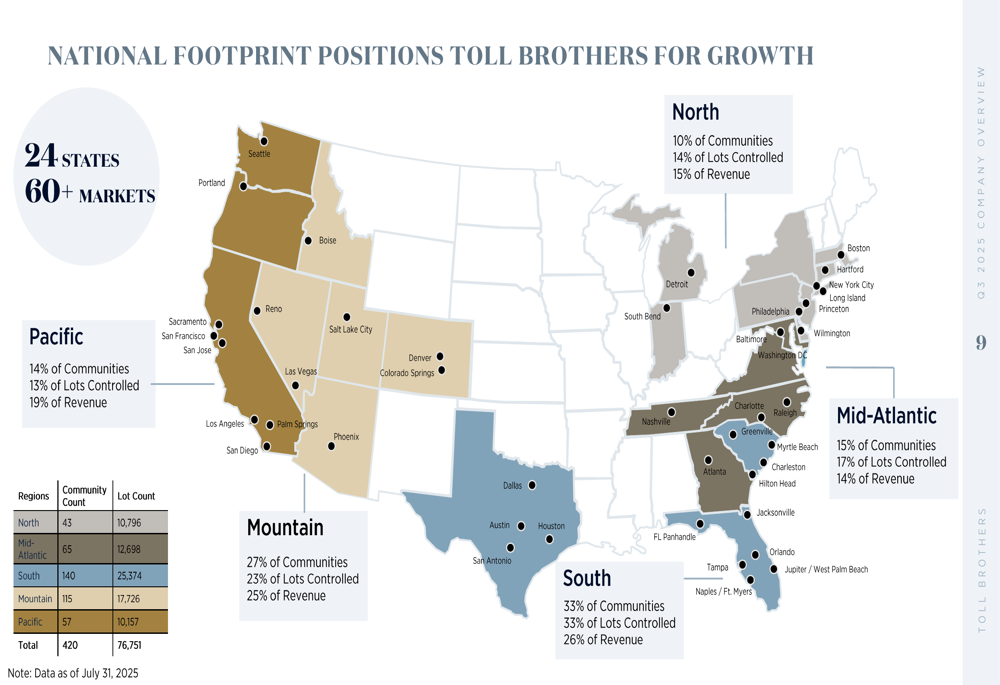

Toll Brothers positions itself as "America’s Luxury Home Builder" with operations spanning 24 states and over 60 markets. The company has delivered consistent financial growth with a 28% CAGR in earnings per share from 2013 to 2024, reaching $15.01 per share in fiscal 2024. This performance has translated into strong shareholder returns, with 5-year returns of 228% outpacing both the homebuilding industry index (96%) and S&P 500 (108%).

The presentation highlights several fundamental factors supporting housing demand, including constrained supply, demographic shifts with Millennials entering prime home-buying years, and the aging of existing housing stock. These factors have created favorable conditions for new home construction despite broader economic uncertainties.

The company’s national footprint provides diversification and positions it for continued growth:

Quarterly Performance Highlights

Toll Brothers reported strong performance in recent quarters, with contracts up 27% in both units and dollars from 2023 to 2024. Revenue increased by 7% in dollars and 13% in units during the same period, while net income grew 15% and earnings per share rose 21% to $15.01 in 2024.

This performance aligns with the company’s Q2 2025 earnings report, which showed revenue of $2.71 billion and EPS of $3.50, significantly exceeding analyst expectations. The company delivered 2,899 homes in Q2 at an average price of $934,000, reinforcing its position in the luxury segment.

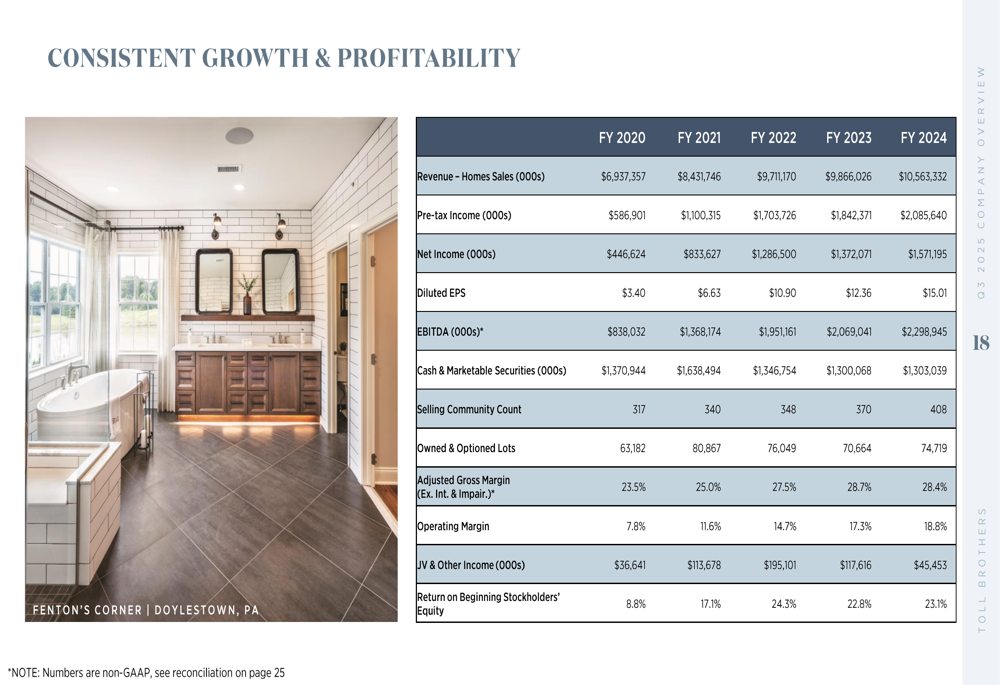

The presentation provides a comprehensive view of the company’s consistent growth and profitability across key metrics:

Detailed Financial Analysis

Toll Brothers has demonstrated impressive financial performance over the past decade. Book value per share has grown at a 13% CAGR from $19.68 in 2013 to $76.87 in 2024, while return on beginning equity has improved from 5.5% to 23.1% over the same period.

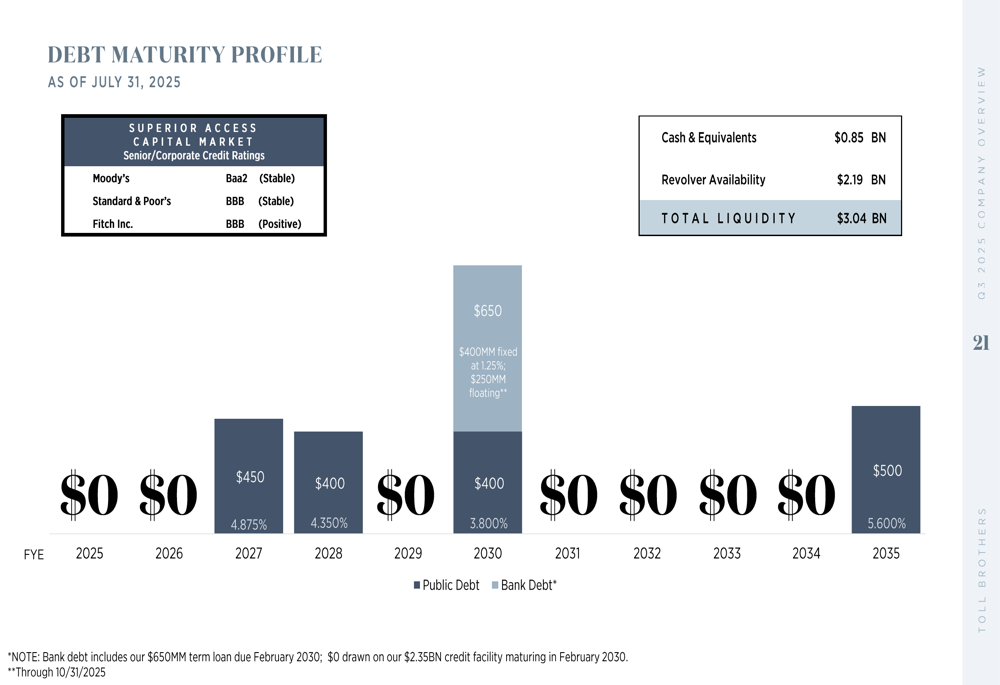

The company maintains a strong liquidity position with $0.85 billion in cash and equivalents and $2.19 billion in revolver availability, providing total liquidity of $3.04 billion. This financial strength is complemented by a well-structured debt maturity profile:

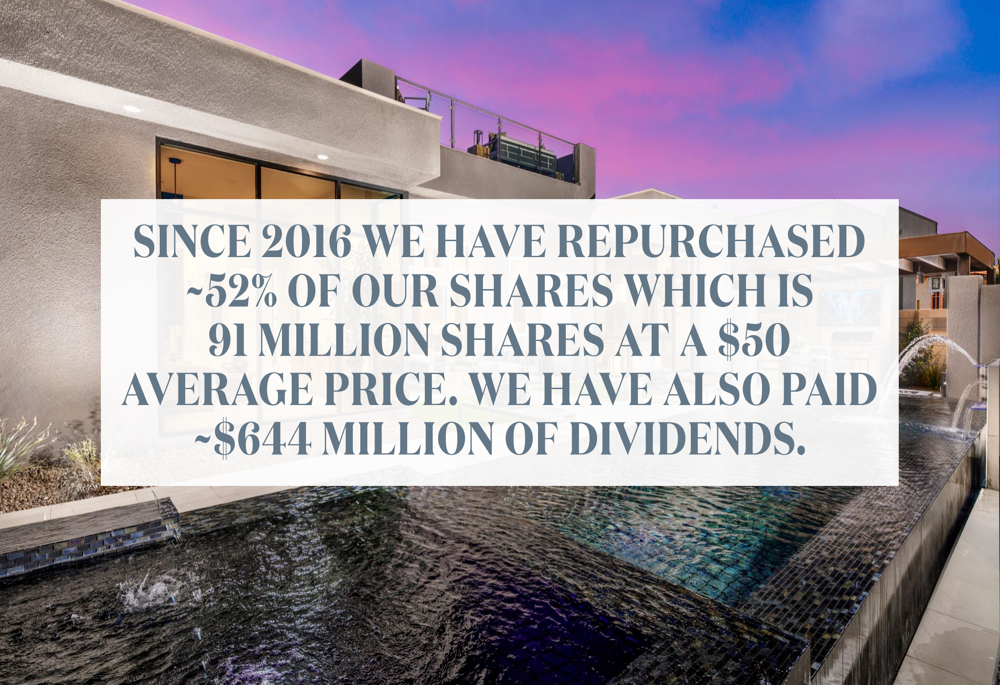

Toll Brothers has been actively returning capital to shareholders, repurchasing approximately 52% of outstanding shares since 2016 (91 million shares at an average price of $50) and paying approximately $644 million in dividends. This capital return strategy has been a key driver of shareholder value:

Competitive Industry Position

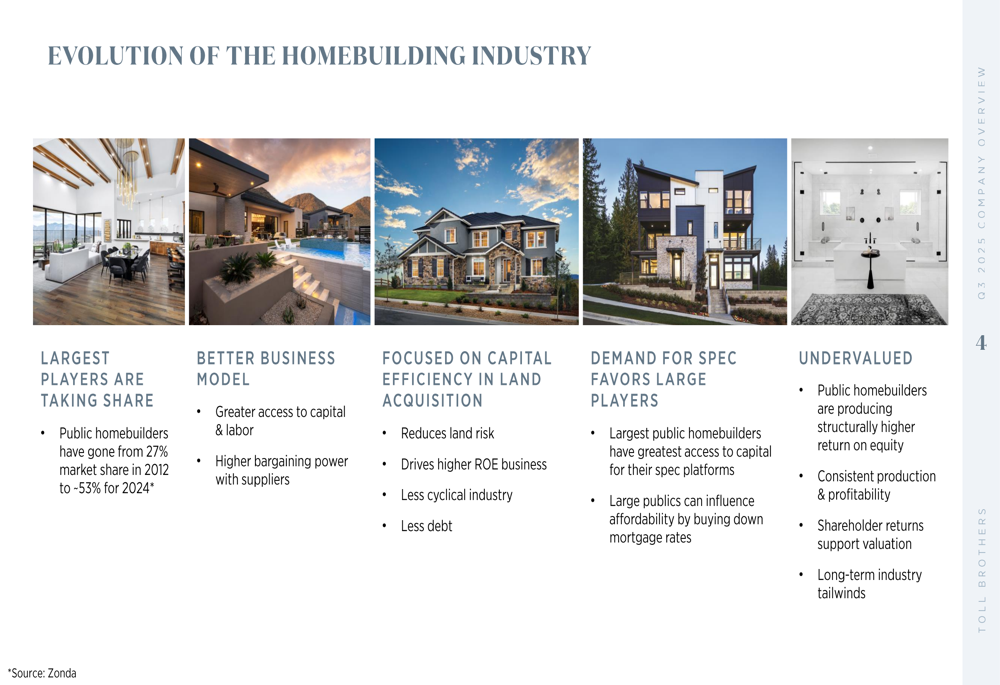

The presentation emphasizes the structural evolution of the homebuilding industry, with public homebuilders gaining significant market share. Their share has increased from 27% in 2012 to approximately 53% in 2024, driven by better access to capital, improved bargaining power with suppliers, and greater capital efficiency in land acquisition.

This trend is occurring against a backdrop of housing undersupply, with average annual housing starts of just 1.10 million from 2008-2024 compared to 1.77 million in the 1970s, despite continued household formation. Additionally, the median age of owner-occupied homes has increased from 32 years in 2005 to 44 years in 2023, creating demand for new construction.

The evolution of the homebuilding industry is illustrated in this comprehensive overview:

Another key industry trend is the compression of the new home premium, which has decreased from a historical average of 17% to just 3% in 2025, making new homes more competitive with existing inventory:

Strategic Initiatives

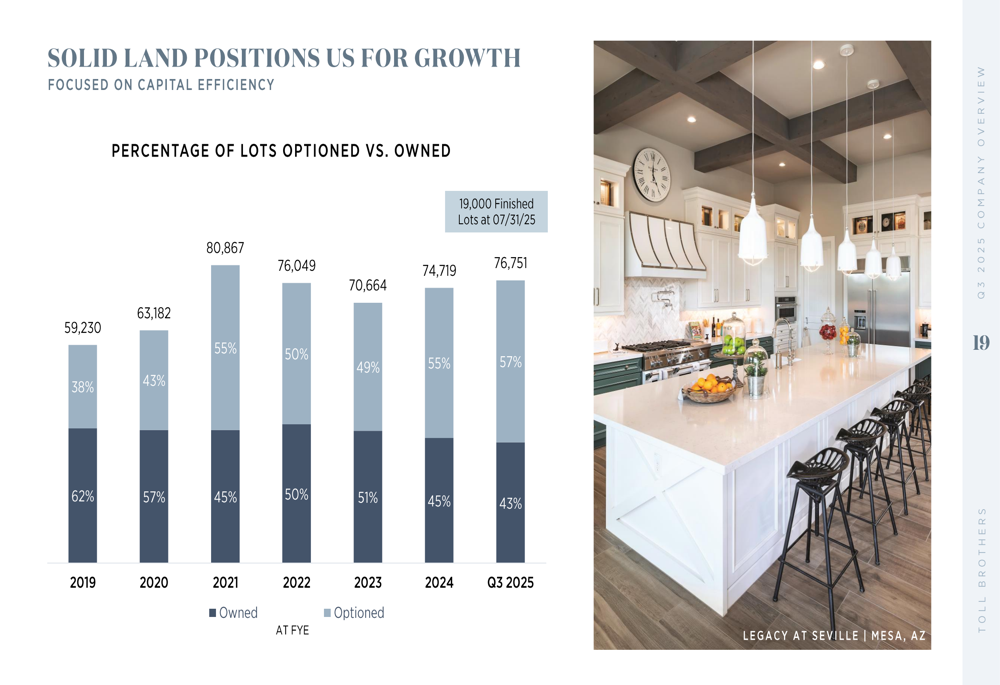

Toll Brothers’ strategy focuses on three key areas: optimized land acquisition, capital return to shareholders, and improved operations. The company has been strategically shifting its land position, increasing the percentage of optioned land to reduce risk and improve capital efficiency.

The presentation outlines the company’s approach to driving shareholder returns through these strategic initiatives:

In terms of land management, Toll Brothers has been evolving its approach to land positions, with a significant portion of its lots now controlled through options rather than outright ownership:

Forward-Looking Statements

Looking ahead, Toll Brothers has reaffirmed its full-year guidance for fiscal 2025, projecting home sales revenue of $10.9 billion and delivery of 11,400 to 11,600 homes. The company expects earnings of approximately $14 per share for the fiscal year.

The presentation identifies several fundamentals supporting future demand, including demographic tailwinds with Millennials in prime home-buying years, the largest wealth transfer from Boomers to Millennials in history, and increased desire for high-quality, move-in-ready homes. The company also notes that its addressable market includes 16 million households with income over $200,000, representing 68% growth since 2012.

Despite near-term market fluctuations, Toll Brothers appears well-positioned to capitalize on these long-term trends with its focus on the luxury segment, where it currently captures approximately 2% of its total addressable market of 575,000 housing transactions annually.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.