Trading Nvidia earnings report? These are the entry and exit levels to watch for

Introduction & Market Context

Topaz Energy Corp (TSX:TPZ) released its latest corporate presentation on May 5, 2025, highlighting its unique position as a hybrid royalty and infrastructure company in the Western Canadian Sedimentary Basin (WCSB). The company, which went public in October 2020, has grown to a $3.6 billion market cap entity with a differentiated business model that combines high-margin royalty assets with stable infrastructure revenue.

Trading at $23.21 as of May 5, 2025, Topaz shares have shown resilience in a volatile energy market, supported by the company’s diversified revenue streams and strategic asset positioning. With significant insider ownership of 26% (including 21.3% held by Tourmaline Oil Corp (TSX:TOU)), management interests remain aligned with shareholders.

Business Model & Competitive Advantages

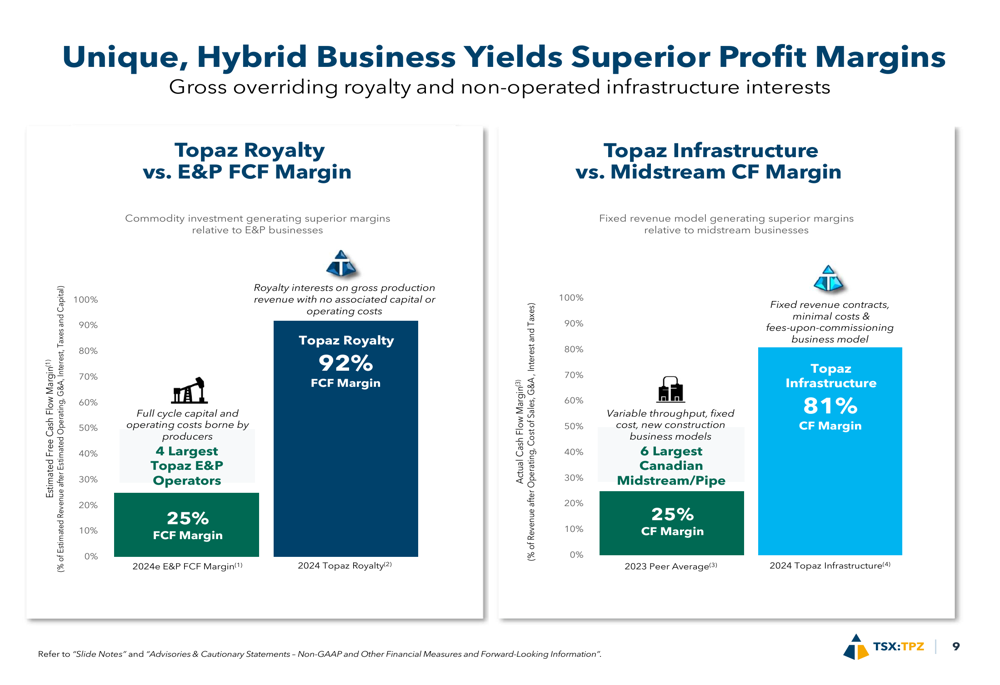

Topaz Energy’s hybrid business model sets it apart from traditional energy companies, combining royalty interests with infrastructure ownership to create superior profit margins and cash flow stability. This approach has yielded impressive financial metrics that outperform industry peers.

As shown in the following comparison of profit margins, Topaz’s royalty business achieves a 92% FCF margin compared to just 25% for the four largest E&P operators in its portfolio, while its infrastructure assets generate an 81% cash flow margin versus 25% for major Canadian midstream companies:

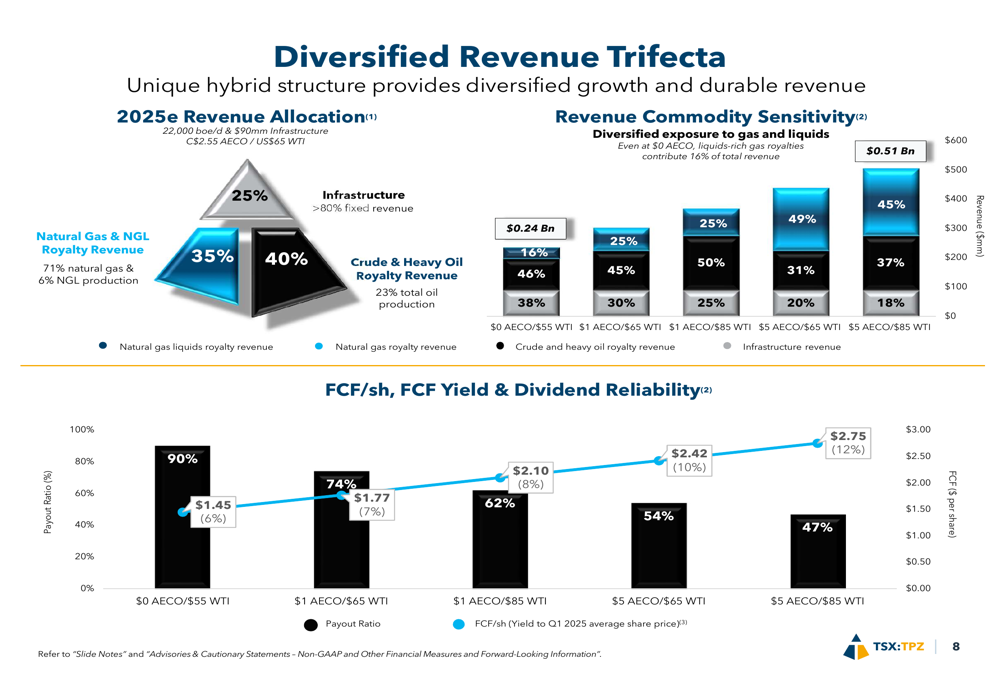

The company maintains a diversified revenue structure that provides natural hedging against commodity price fluctuations. For 2025, Topaz projects its revenue will be allocated as 25% from infrastructure, 35% from natural gas and NGL royalties, and 40% from crude and heavy oil royalties. This diversification helps maintain dividend reliability even during commodity price volatility.

As illustrated in the revenue trifecta chart below, this balanced approach provides significant protection against commodity price swings, with the company noting that even at $0 AECO natural gas prices, liquids-rich gas royalties would still contribute 16% of total revenue:

Financial Performance & Outlook

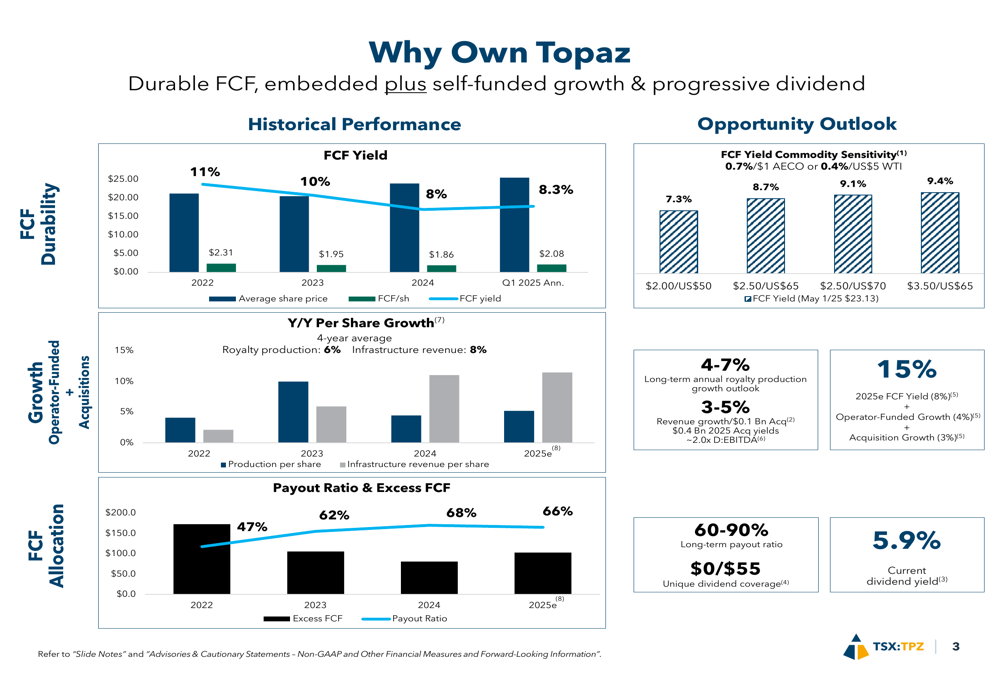

Topaz Energy has demonstrated strong financial performance with an annualized Q1 2025 free cash flow yield of 8.3%, supporting its current dividend yield of 5.9%. The company has maintained a disciplined approach to its payout ratio, which is projected at 66% for 2025, within its long-term target range of 60-90%.

The company’s historical performance shows consistent growth in key metrics. Over a four-year average, Topaz has achieved 6% year-over-year growth in royalty production per share and 8% growth in infrastructure revenue per share. This growth has been achieved while maintaining strong dividend coverage.

As shown in the following chart, Topaz offers compelling reasons for investment based on its durable free cash flow, self-funded growth, and progressive dividend strategy:

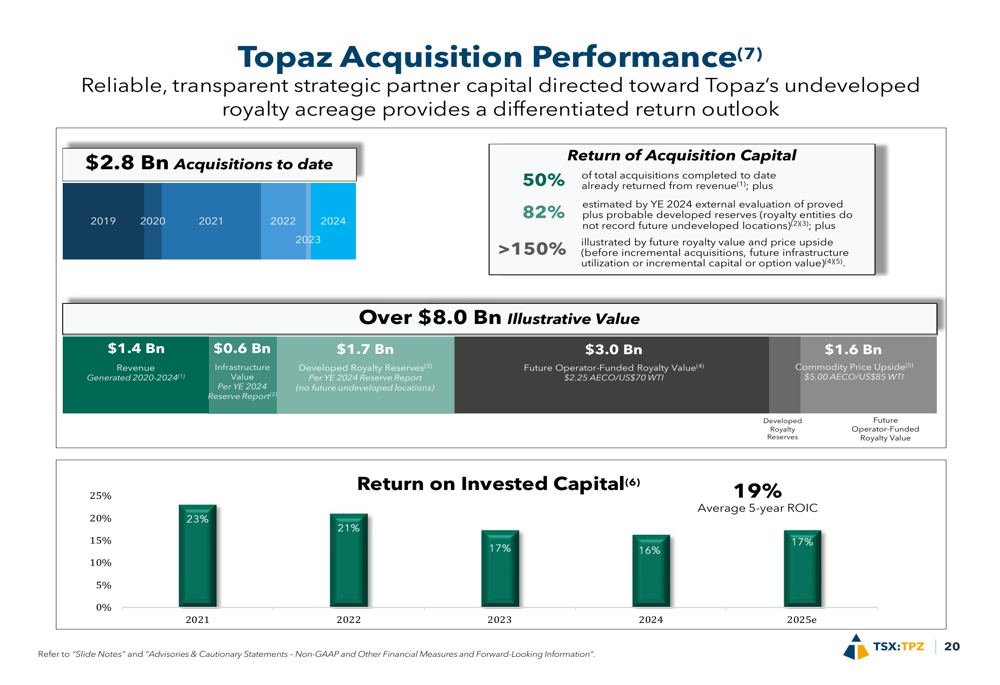

Since inception, Topaz has generated $1.5 billion in free cash flow, representing approximately 42% of its current market capitalization. The company has completed $2.8 billion in acquisitions to date, demonstrating its ability to execute on its growth strategy while maintaining financial discipline.

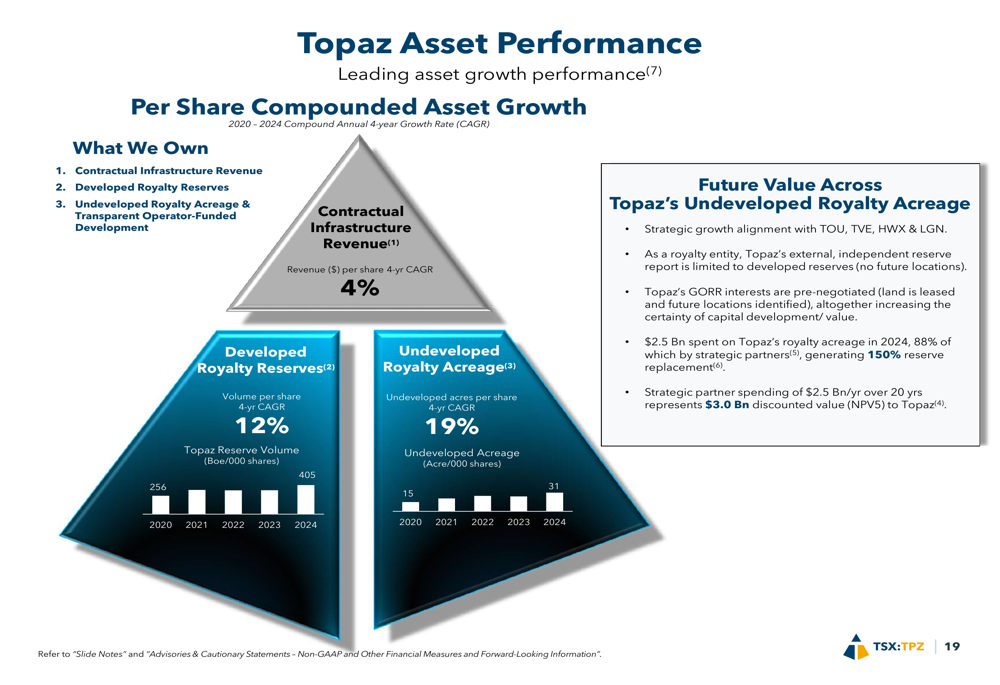

The company’s asset growth has been impressive across all segments, with particularly strong performance in undeveloped royalty acreage:

Strategic Asset Positioning

Topaz Energy has strategically positioned its assets in some of the most economic plays in the Western Canadian Sedimentary Basin. The company holds 8.9 million royalty acres across the WCSB, with 93% of its royalty volume generated from leading Canadian operators with strong economic resiliency.

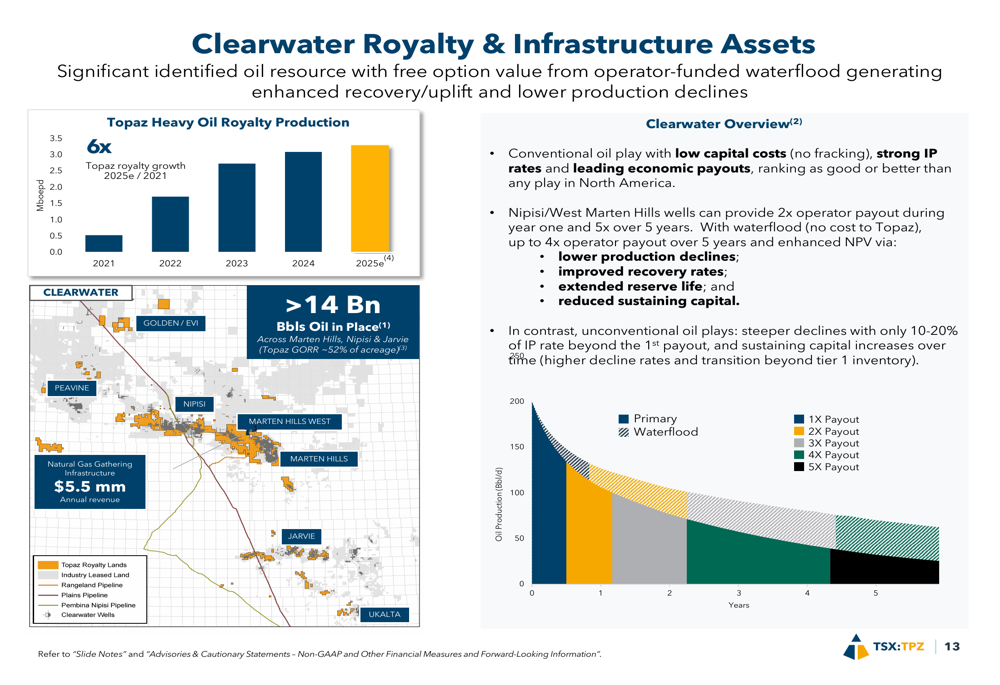

A key growth area for Topaz is the Clearwater play, where the company has achieved 6x royalty growth. The Clearwater represents one of the most economic conventional oil plays in the WCSB, with low capital costs, strong initial production rates, and leading economic payouts.

The following map illustrates Topaz’s extensive Clearwater royalty and infrastructure assets:

Another significant area of focus is the NEBC Montney, where Topaz holds 1.6 million gross acres and 10% ownership in the Gundy gas plant. The company projects 6-8% annual royalty production growth from this region, which is positioned to benefit from LNG Canada Phase I providing 10% egress expansion.

Topaz’s portfolio is predominantly undeveloped, providing significant long-term growth potential as operators continue to develop these assets. The company benefits from operator-funded capital activity, with reliable drilling activity from strategic partners’ long-term development plans.

Dividend Strategy & Capital Allocation

Topaz Energy has established a track record of dividend growth, having paid $0.9 billion in dividends since inception, representing 25% of its average market capitalization from Q1 2020 to Q1 2025. The company’s current dividend yield of 5.9% is supported by its diversified revenue streams and high-margin assets.

A distinctive feature of Topaz’s dividend strategy is its coverage from multiple revenue sources. The company notes that 43% of its 2025 estimated dividend coverage comes from reliable, high-margin infrastructure revenue, providing a solid foundation even during commodity price fluctuations.

The company’s competitive advantages can be summarized in the following key points:

Looking ahead, Topaz Energy is well-positioned to continue its growth trajectory. With 86% of its royalty acreage under long-term tenure and a projected 4-7% long-term annual royalty production growth outlook, the company has established a sustainable model for generating shareholder returns through both dividends and capital appreciation.

The company’s acquisition strategy has delivered strong returns on invested capital, with significant value creation from its $2.8 billion in acquisitions to date:

Topaz Energy’s Q2 2025 presentation reinforces its position as a premium, differentiated energy investment with a unique hybrid business model that generates superior margins, resilient cash flow, and sustainable dividend growth. With strategic assets in key Canadian energy plays and a disciplined approach to capital allocation, Topaz appears well-positioned to continue delivering value to shareholders in various commodity price environments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.