SoFi stock falls after announcing $1.5B public offering of common stock

Introduction & Market Context

TopBuild Corp (NYSE:BLD) presented its third-quarter 2025 results on November 4, revealing a strategy heavily focused on acquisitions to counter ongoing softness in residential markets. Despite beating analyst expectations with EPS of $5.36 (versus $5.27 forecast) and revenue of $1.39 billion (exceeding $1.37 billion expected), the stock dropped 2.27% during trading, reflecting investor concerns about the residential construction outlook.

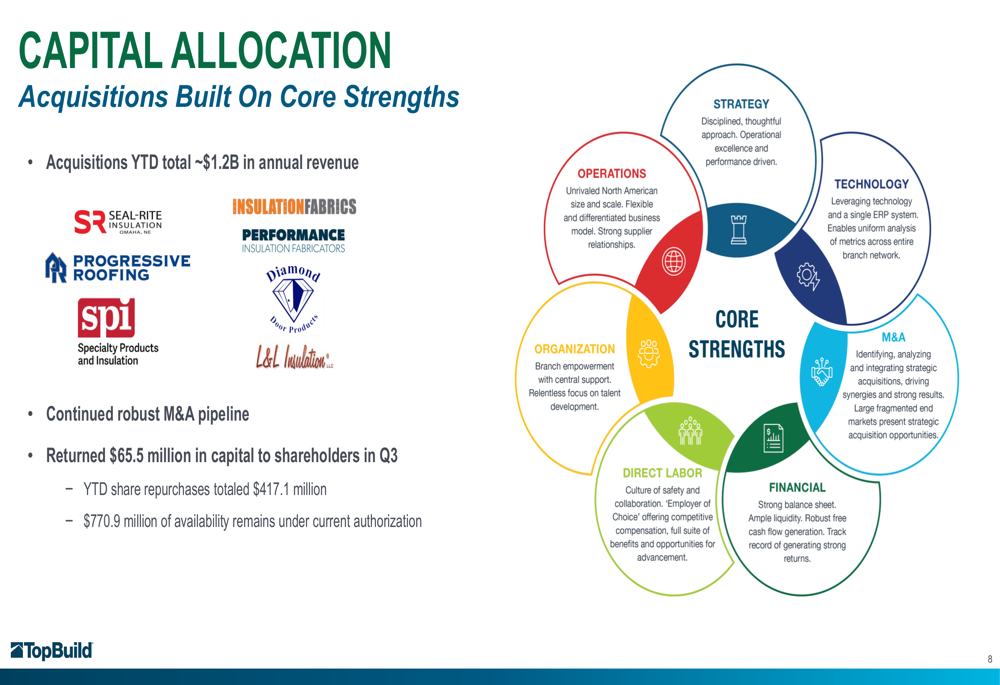

The building products installer and distributor continues to navigate a challenging residential environment by strategically expanding its commercial and industrial presence through acquisitions, which have added approximately $1.2 billion in annual revenue year-to-date.

Quarterly Performance Highlights

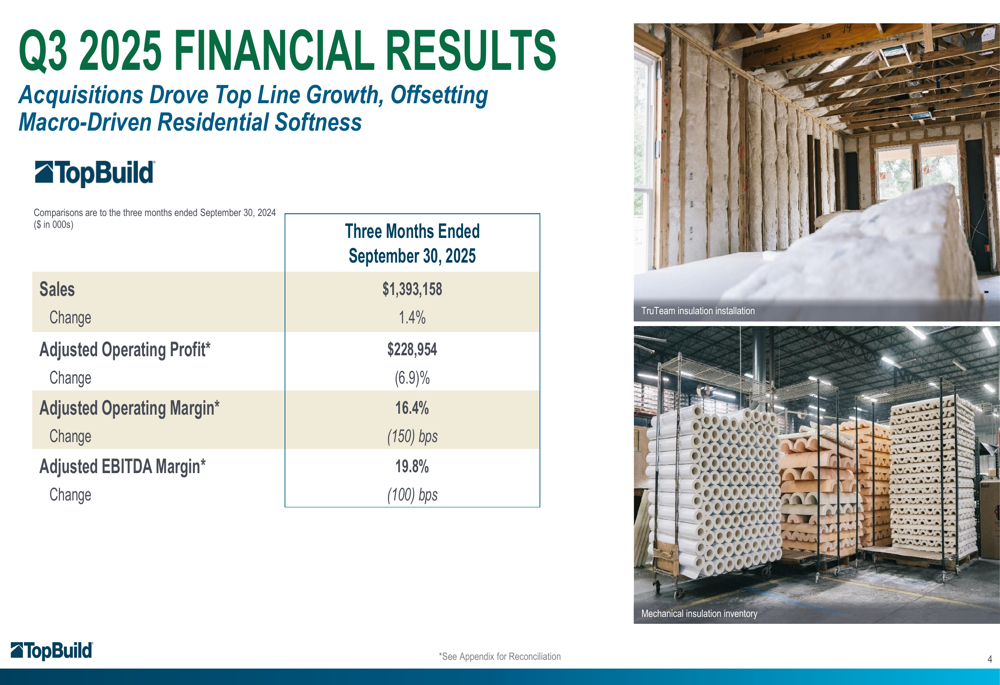

TopBuild reported a 1.4% year-over-year increase in sales to $1.39 billion for Q3 2025, primarily driven by acquisitions that offset weakness in the residential sector. However, profitability metrics showed some pressure, with adjusted operating profit declining 6.9% to $228.9 million and adjusted operating margin contracting 150 basis points to 16.4%.

As shown in the company's quarterly financial summary:

The Installation Services segment demonstrated resilience with a 0.2% sales increase and a relatively modest 60 basis point decline in operating margin to 19.5%. Meanwhile, the Specialty Distribution segment saw sales grow by 1.4%, though its operating margin contracted 140 basis points to 14.4% compared to the same period last year.

Robert Buck, President and CEO, emphasized the company's operational excellence in maintaining healthy profit margins despite soft demand in residential and light commercial sectors. This sentiment was echoed in the earnings call, where Buck highlighted long-term opportunities in the U.S. housing market despite current challenges.

Acquisition Strategy & Business Diversification

TopBuild's aggressive acquisition strategy has been central to its growth narrative in 2025. The company highlighted two major transactions: the Q3 Progressive Roofing acquisition adding approximately $440 million in annual revenue, and the Q4 SPI transaction contributing around $700 million. Additionally, five smaller acquisitions are expected to add over $65 million in annual revenue.

The company's capital allocation priorities were clearly illustrated in the presentation:

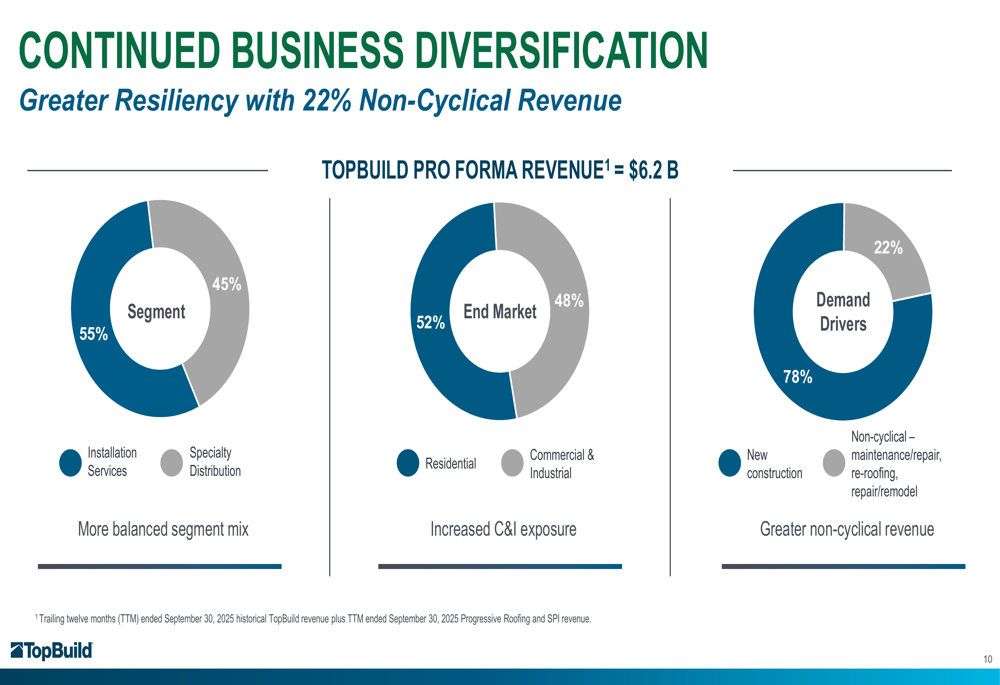

These strategic acquisitions are deliberately reshaping TopBuild's business mix toward more stable revenue streams. The company now reports that 22% of its revenue comes from non-cyclical sources such as maintenance, repair, and remodeling, providing greater resilience against housing market fluctuations.

The following chart demonstrates how TopBuild has diversified its revenue streams:

The SPI acquisition particularly strengthens TopBuild's position in commercial and industrial mechanical insulation solutions, serving customers across various sectors including data centers, industrial manufacturing, and energy. This strategic move aligns with the company's goal of reducing exposure to cyclical residential construction.

Balance Sheet & Cash Flow Strength

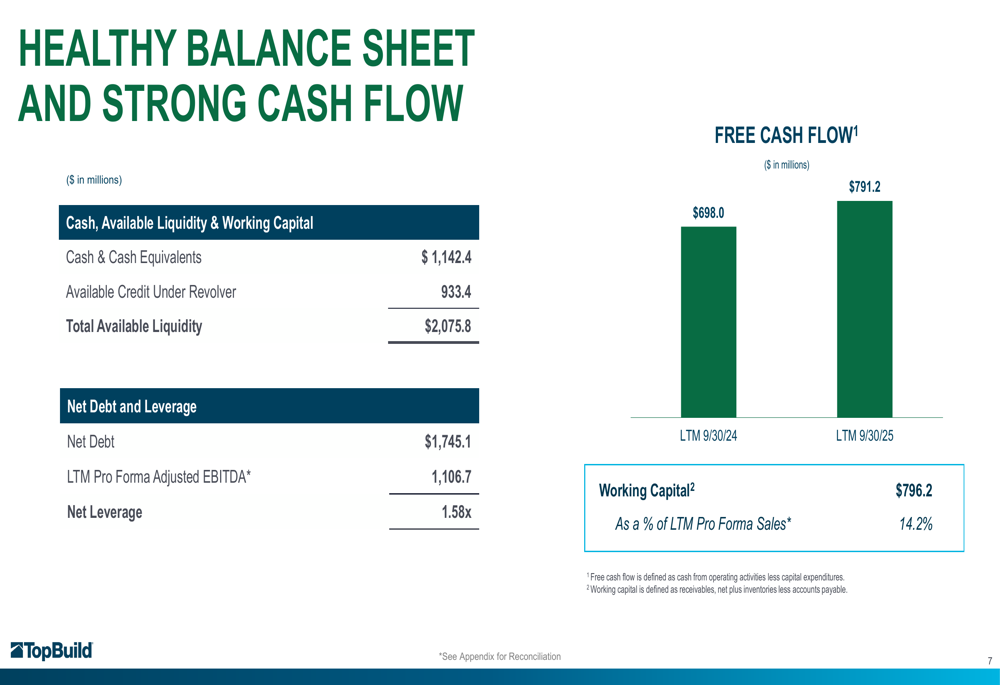

TopBuild's financial position remains robust, with $2.08 billion in total available liquidity, including $1.14 billion in cash and cash equivalents. The company's net leverage ratio stands at a comfortable 1.58x, providing significant capacity for further acquisitions.

Free cash flow has shown impressive growth, reaching $791.2 million for the trailing twelve months ended September 30, 2025, a 13.4% increase from the prior year period.

This strong cash generation has enabled TopBuild to return $65.5 million to shareholders in Q3 through share repurchases, with year-to-date buybacks totaling $417.1 million. The company still has $770.9 million available under its current repurchase authorization.

CFO Rob Kuhns highlighted during the earnings call that the company's resilient margins were supported by strategic cost-saving measures and supply chain improvements, contributing to the strong cash flow performance despite market challenges.

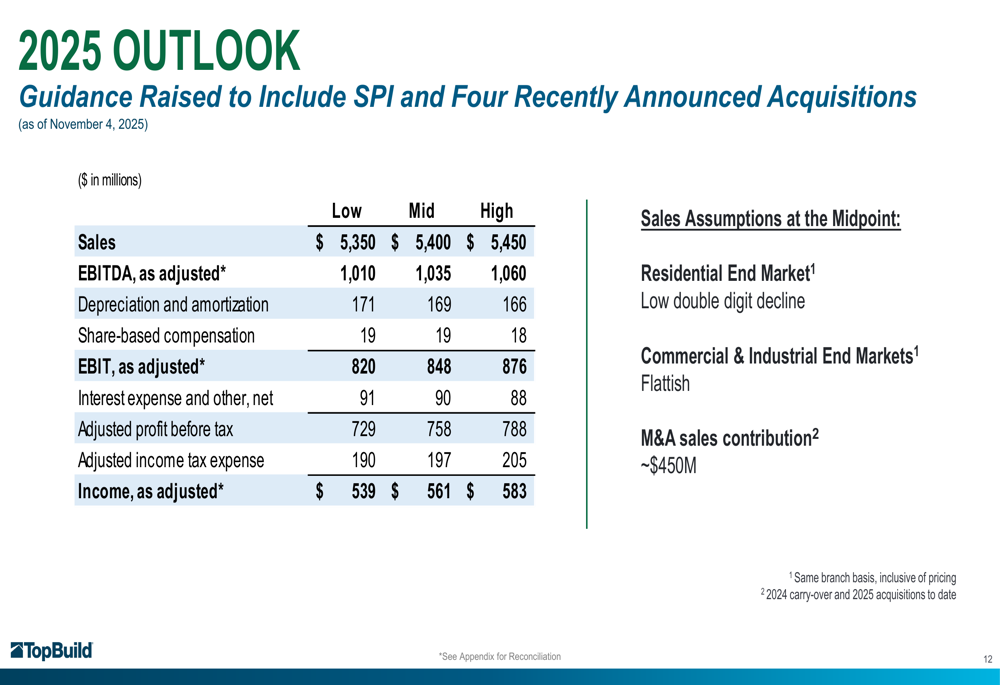

Forward-Looking Statements & Outlook

TopBuild has raised its 2025 guidance to include SPI and four recently announced acquisitions. The updated outlook projects:

Management expects the residential end market to experience a low double-digit decline, while commercial and industrial markets are anticipated to remain relatively flat. The M&A contribution to sales is projected at approximately $450 million.

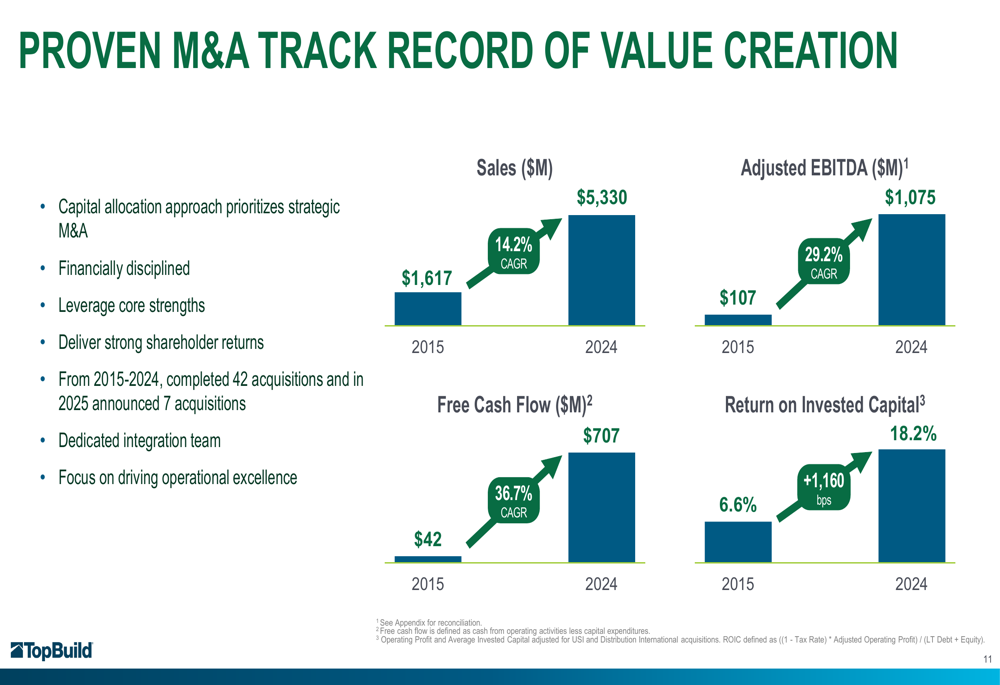

The company's long-term growth strategy continues to focus on its proven M&A track record, which has delivered substantial value creation since 2015:

While TopBuild's presentation emphasizes its strategic positioning and diversification efforts, investors appear cautious about near-term challenges in the residential market, as reflected in the stock's performance following the earnings release.

The company faces several ongoing risks, including continued weakness in residential construction, potential pricing pressures in competitive markets, and integration challenges from its numerous recent acquisitions. However, management remains confident that its diversification strategy and strong financial position will enable it to navigate these challenges effectively while pursuing additional growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.