US stock futures inch lower after Wall St marks fresh records on tech gains

Introduction & Market Context

Tourmaline Oil Corp . (TSX:TOU), Canada’s largest natural gas producer, has outlined an ambitious growth strategy in its July 2025 corporate presentation, targeting production of 850,000 barrels of oil equivalent per day (boepd) by 2031. The company currently holds a market capitalization of $25.6 billion as of June 30, 2025, with its stock trading at $62.93 as of July 30, 2025, closer to its 52-week low of $54.37 than its high of $70.73.

The presentation comes after Tourmaline reported disappointing Q1 2025 results, with earnings per share of $0.56 significantly missing analyst expectations of $1.54, despite revenue beating forecasts at $1.89 billion. This earnings miss resulted in a 1.92% decline in after-hours trading following the Q1 report.

Executive Summary

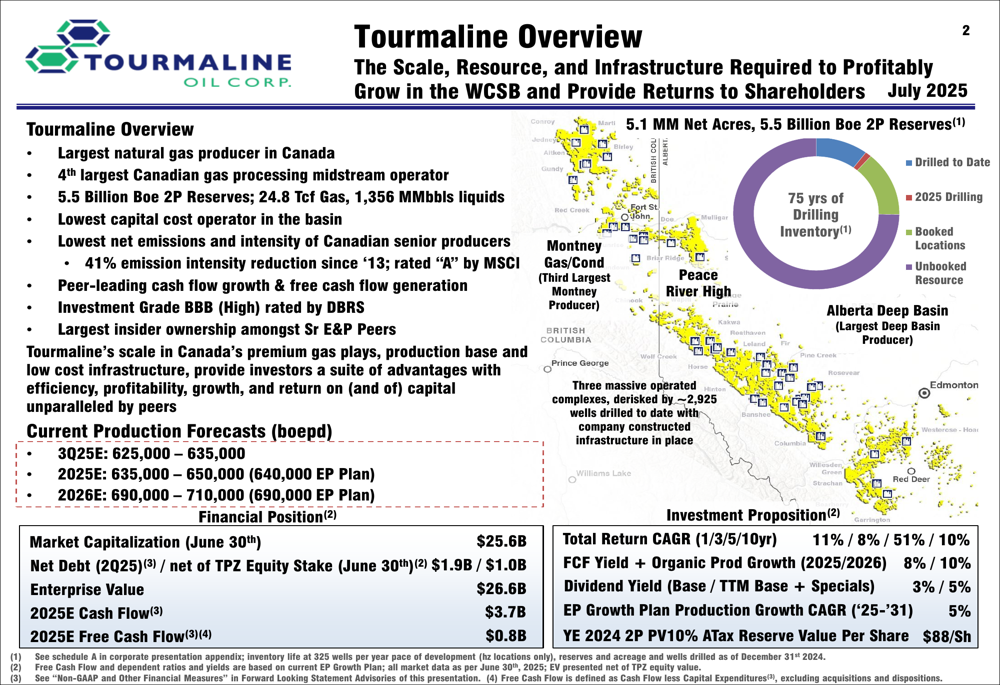

Tourmaline’s presentation positions the company as a dominant player in the Canadian energy landscape, highlighting its status as the largest natural gas producer in Canada and the fourth largest Canadian gas processing midstream operator. With 5.5 billion barrels of oil equivalent in 2P reserves (24.8 Tcf gas, 1,356 MMbbls liquids), the company emphasizes its operational scale and efficiency.

As shown in the following overview slide, Tourmaline maintains a strong market position with significant assets across British Columbia and Alberta:

The company projects production of 625,000-635,000 boepd for Q3 2025, with full-year 2025 production estimated at 635,000-650,000 boepd. For 2026, Tourmaline forecasts production growth to 690,000-710,000 boepd, demonstrating its ambitious expansion plans.

Detailed Financial Analysis

Tourmaline projects 2025 cash flow of $3.7 billion and free cash flow of $0.8 billion, with capital expenditures between $2.6-2.85 billion. However, these projections should be viewed in the context of the company’s Q1 2025 performance, which showed cash flow of $963 million and free cash flow of only $150 million, suggesting potential challenges in meeting full-year targets.

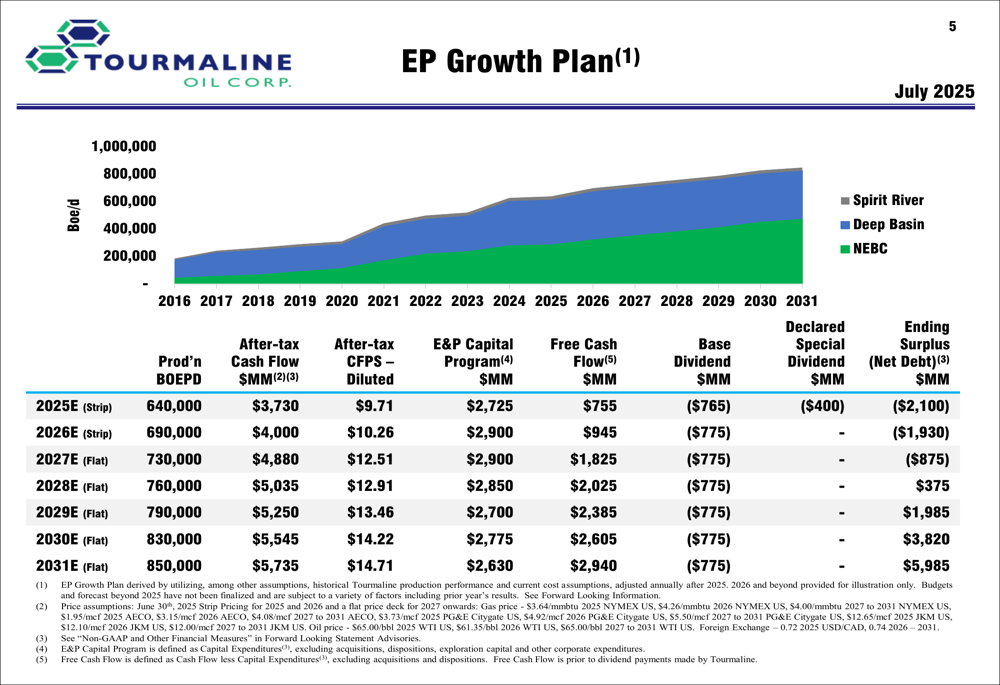

The company’s EP (Exploration and Production) Growth Plan outlines a clear path to increasing production and financial returns through 2031, as illustrated in this comprehensive chart:

By 2031, under flat pricing assumptions, Tourmaline projects production of 850,000 boepd, after-tax cash flow of $5.7 billion, and free cash flow of $2.9 billion. This represents a significant increase from 2025 projections and highlights the company’s focus on long-term growth and value creation.

Competitive Industry Position

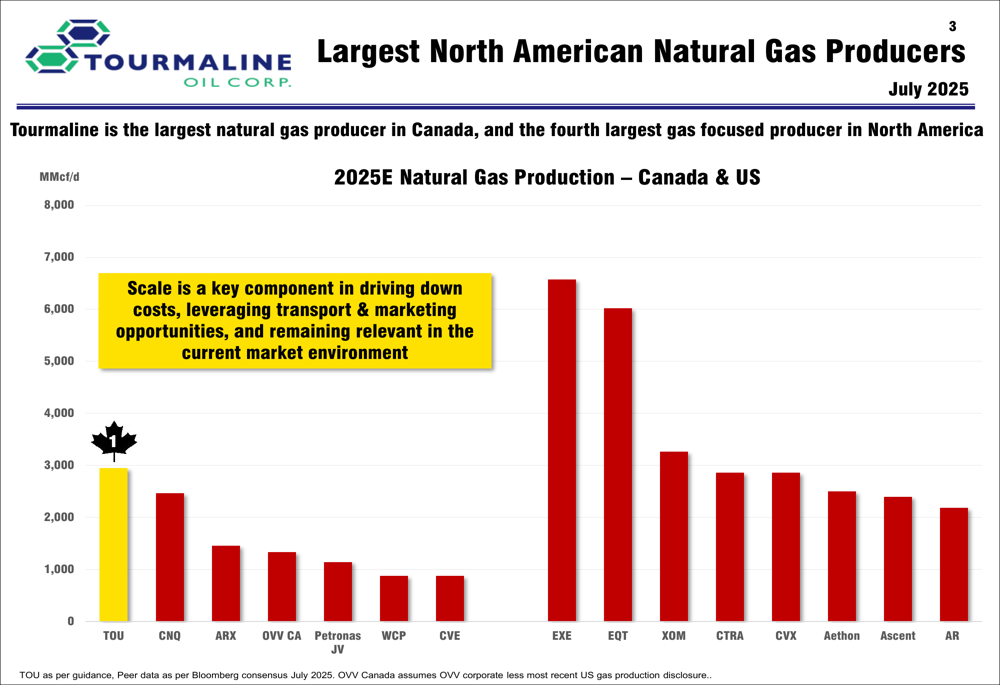

Tourmaline maintains its position as the largest natural gas producer in North America, outpacing both Canadian and U.S. competitors. This scale provides advantages in cost efficiency, marketing opportunities, and overall market relevance.

The following chart illustrates Tourmaline’s leading position among North American natural gas producers:

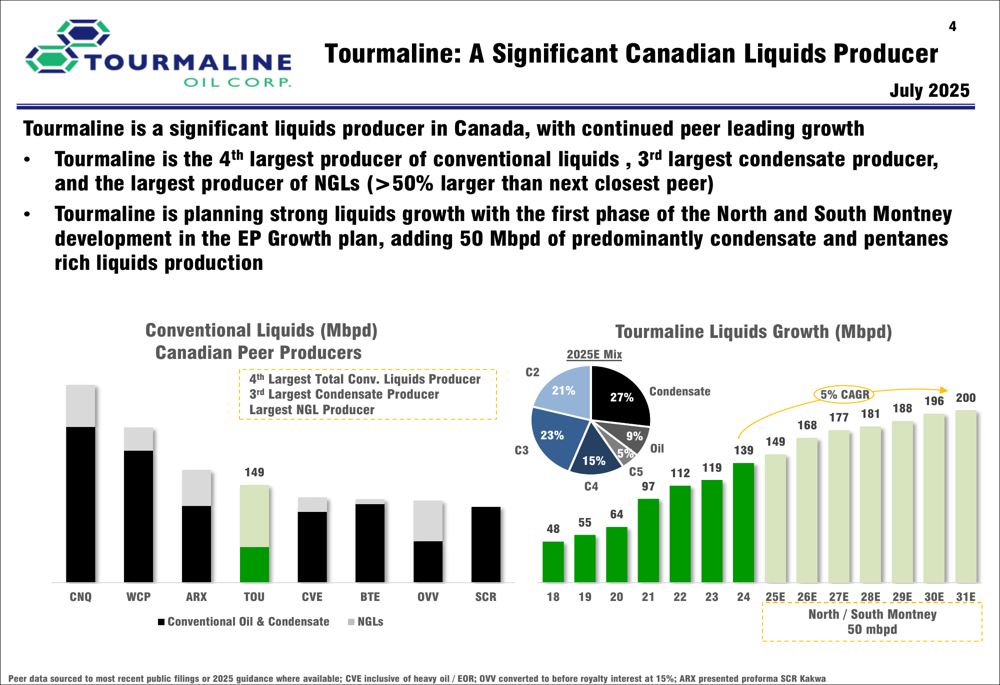

Beyond natural gas, Tourmaline has also established itself as a significant liquids producer in Canada. The company ranks as the fourth largest producer of conventional liquids and the third largest condensate producer in the country, with plans to add 50,000 barrels per day of predominantly condensate and pentanes-rich liquids production.

As shown in the following chart, Tourmaline’s liquids production compares favorably with Canadian peers:

Strategic Initiatives

The centerpiece of Tourmaline’s growth strategy is its Northeast British Columbia (NEBC) infrastructure build-out, which includes two new facilities, four complex expansions, and three new liquids hubs. This project is expected to add 200,000 boepd of high-margin volume growth into the next decade.

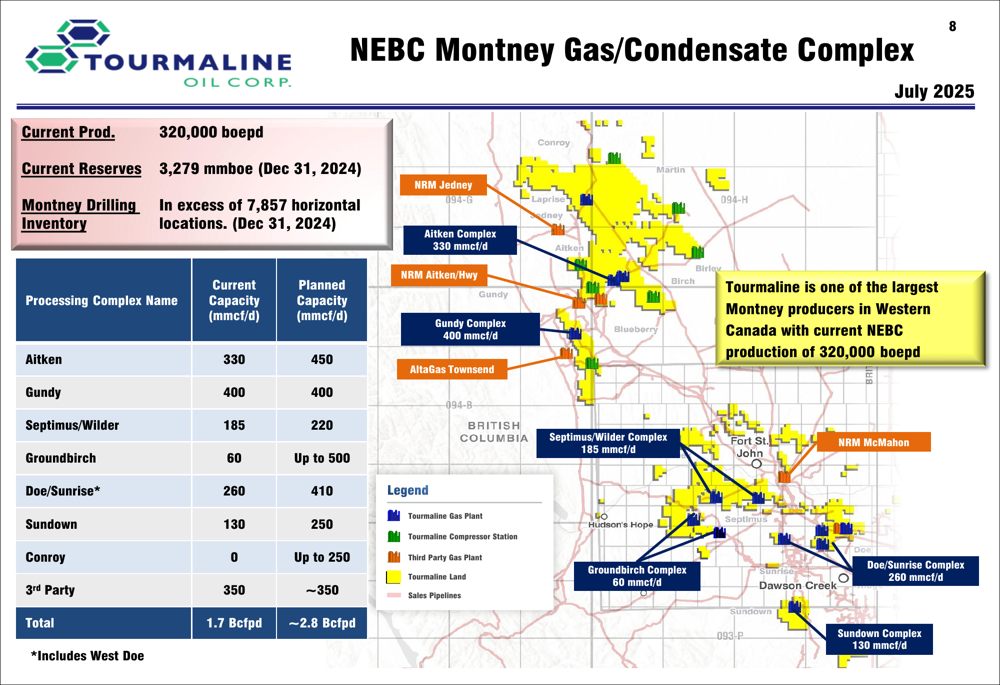

The NEBC Montney Gas/Condensate Complex represents a core asset for Tourmaline, with current production of 320,000 boepd and planned processing capacity expansions across multiple facilities:

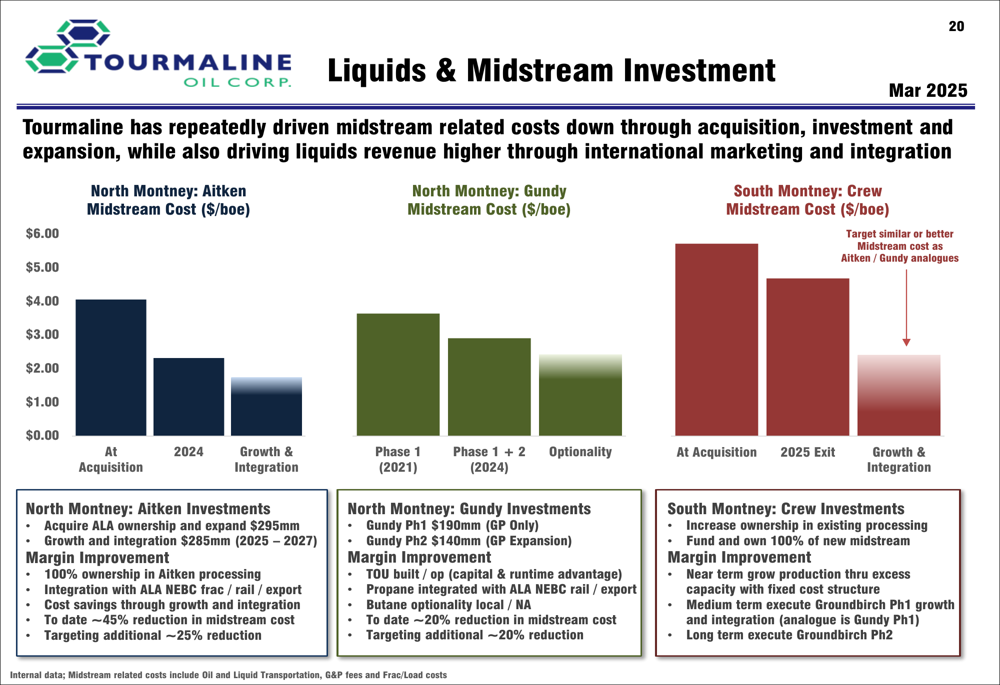

Tourmaline is also focusing on improving its midstream operations and liquids handling capabilities, which is expected to enhance margins and operational efficiency:

Forward-Looking Statements

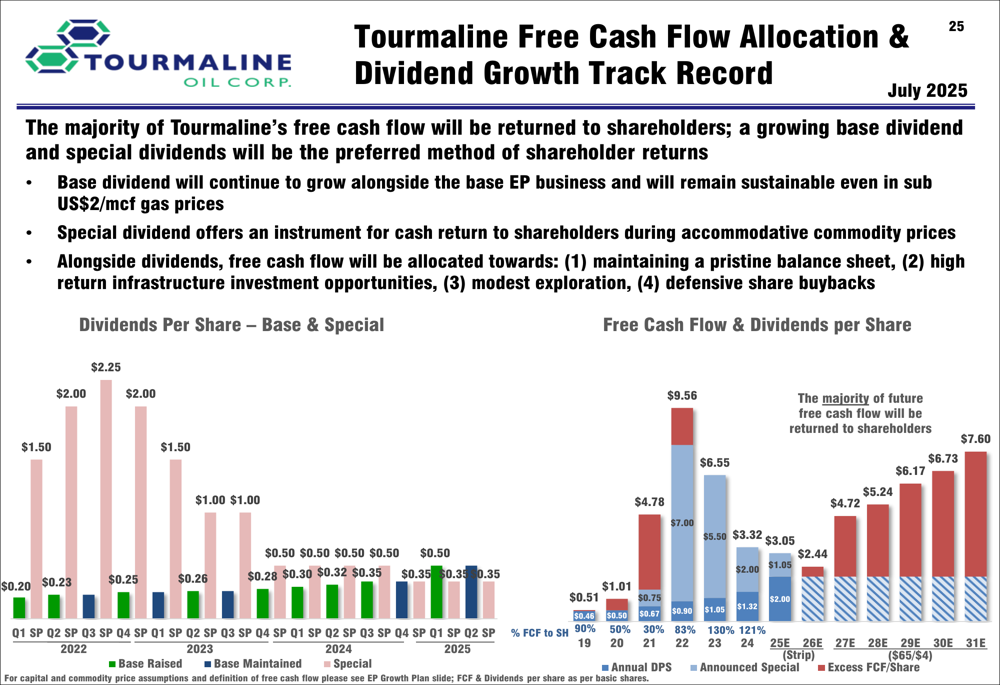

Tourmaline’s dividend strategy remains a key component of its shareholder return policy. The company currently offers a base dividend yield of 3%, with total yield (including special dividends) of 5% over the trailing twelve months. Management has emphasized that excess free cash flow will continue to be returned to shareholders.

The following chart illustrates Tourmaline’s dividend growth track record and free cash flow allocation:

CEO Mike Rose expressed optimism about natural gas prices in the Q1 earnings call, stating, "We expect natural gas prices to go up." This outlook supports the company’s aggressive growth plans, though execution risks and potential volatility in natural gas prices remain key challenges.

Outlook

Tourmaline’s long-term business plan aims to position the company for sustained growth and shareholder returns. The company expects to achieve maintenance capital levels by 2031, which would generate over $3 billion in annual free cash flow at flat pricing assumptions.

The company’s guidance for 2025 includes production of 635,000-650,000 boepd, cash flow of $3.73 billion (at 640,000 boepd), and capital expenditures between $2.85-3.1 billion. These projections will be closely watched by investors, particularly in light of the recent earnings miss.

While Tourmaline’s ambitious growth plans and strong market position provide a solid foundation for future success, the company faces execution risks associated with its large-scale infrastructure projects, potential regulatory changes affecting the energy sector, and ongoing volatility in natural gas prices. The significant gap between projected and actual earnings in Q1 2025 also raises questions about the company’s ability to meet its financial targets in the near term.

Nevertheless, Tourmaline’s scale, operational efficiency, and extensive reserve base position it well to capitalize on growing demand for natural gas, particularly as Canadian LNG export capacity expands in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.