BigBear.ai appoints Sean Ricker as chief financial officer

Introduction & Market Context

TPG Inc (NASDAQ:TPG), a leading global alternative asset management firm, reported its first quarter 2025 financial results on May 7, 2025, showcasing strong growth in assets under management and a significant turnaround in profitability. The company’s presentation highlighted a shift from a net loss in the year-ago period to positive net income, while maintaining stable fee-related earnings despite margin compression.

In premarket trading following the release, TPG shares were up 4.96% to $48.48, indicating positive investor reception to the results. The stock had closed at $46.19 on May 6, 2025, down 2.04% in the regular session.

Quarterly Performance Highlights

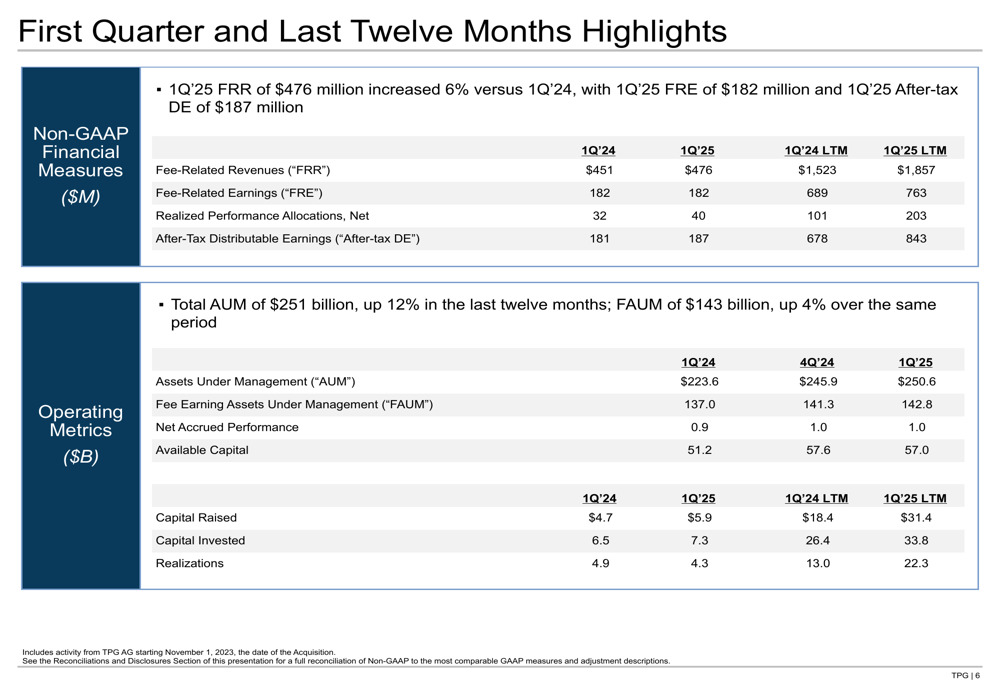

TPG reported net income of $87.8 million for Q1 2025, a substantial improvement from a net loss of $9.0 million in Q1 2024. Net income attributable to TPG Inc. was $25.4 million, up from $15.5 million in the prior-year period. The company’s fee-related revenue increased 6% year-over-year to $476 million, while fee-related earnings remained flat at $182 million.

As shown in the following comprehensive overview of TPG’s quarterly performance metrics:

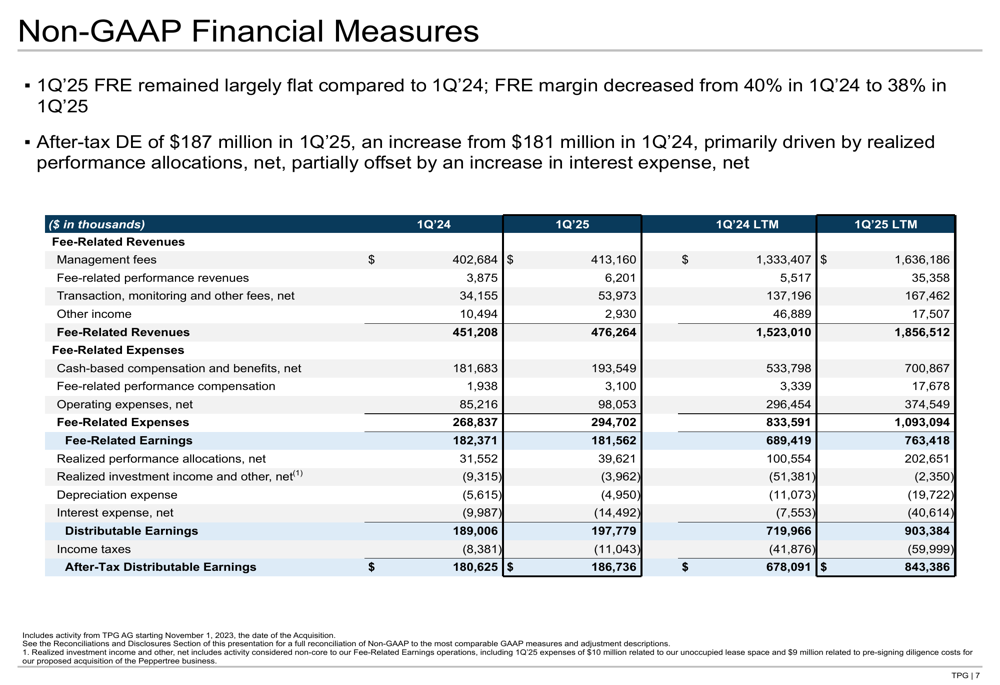

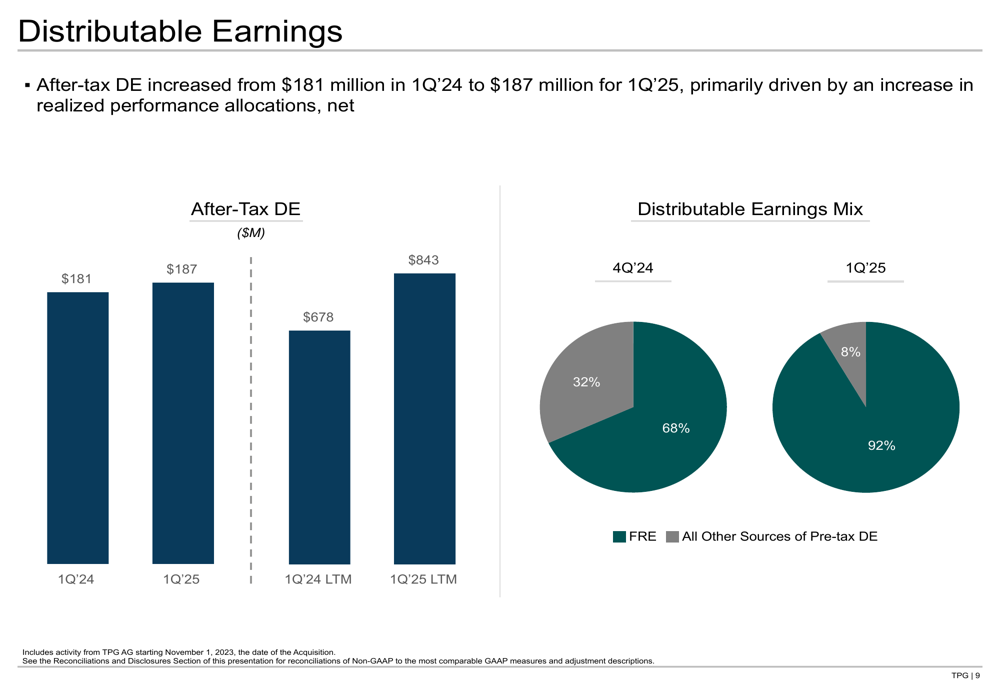

After-tax distributable earnings, a key metric for alternative asset managers, reached $187 million in Q1 2025, a modest increase from $181 million in Q1 2024. This growth was primarily driven by realized performance allocations, partially offset by higher interest expenses. The company’s fee-related earnings margin decreased from 40% in Q1 2024 to 38% in Q1 2025, though the trailing twelve-month margin stood at a healthy 41%.

A detailed breakdown of TPG’s non-GAAP financial measures reveals the components driving the company’s performance:

Assets Under Management Growth

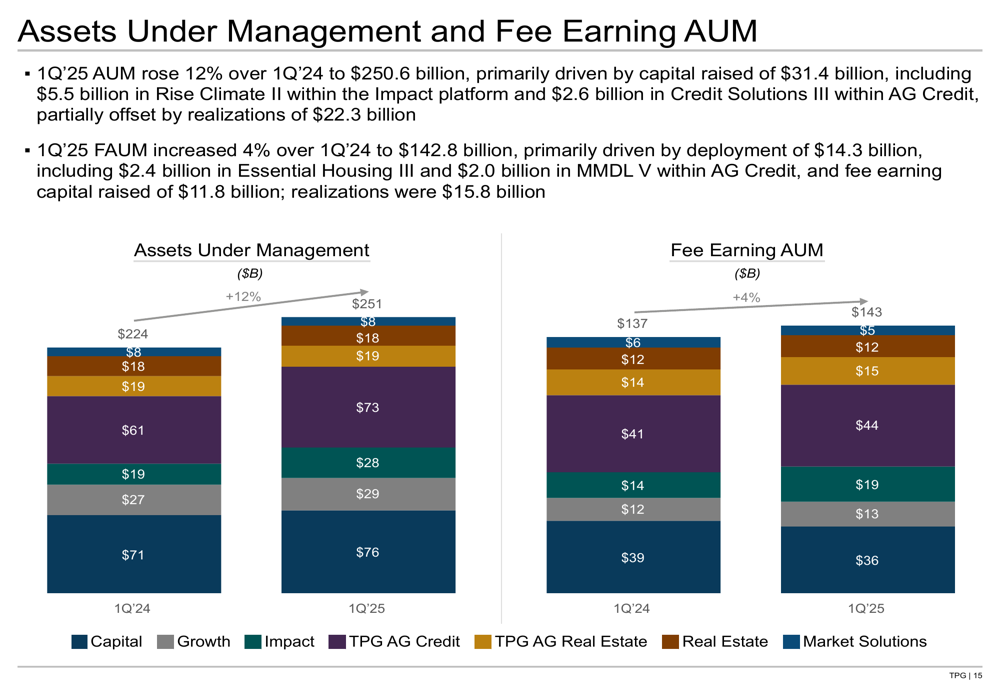

TPG’s total assets under management reached $251 billion as of March 31, 2025, representing a 12% increase from the prior year. Fee-earning AUM grew 4% year-over-year to $143 billion. During the quarter, the firm raised $5.9 billion in new capital and invested $7.3 billion across its various platforms.

The following chart illustrates the composition of TPG’s AUM and fee-earning AUM across its diverse investment platforms:

CEO Jon Winkelried emphasized the firm’s strong position with $57 billion in dry powder available for deployment, positioning TPG to capitalize on investment opportunities across its platforms. This substantial available capital represents approximately 23% of the firm’s total AUM.

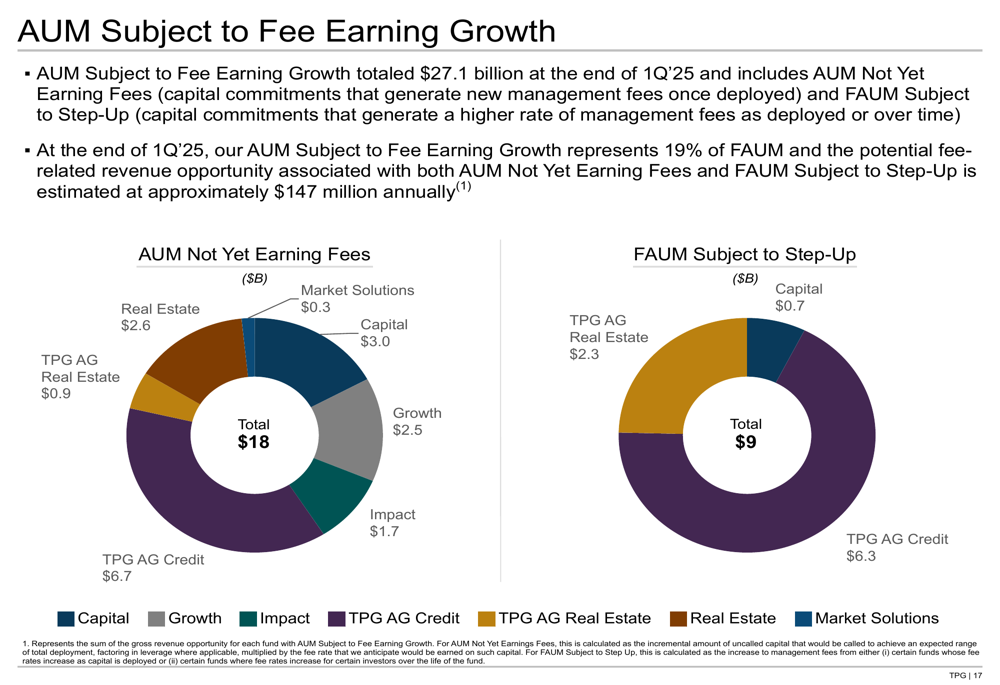

The company’s presentation also highlighted the potential for future fee-related revenue growth, with $27.1 billion of AUM subject to fee-earning growth. This includes both AUM not yet earning fees and FAUM subject to step-up, representing an estimated annual fee-related revenue opportunity of approximately $147 million.

As shown in the following breakdown of AUM subject to fee-earning growth:

Performance and Distributable Earnings

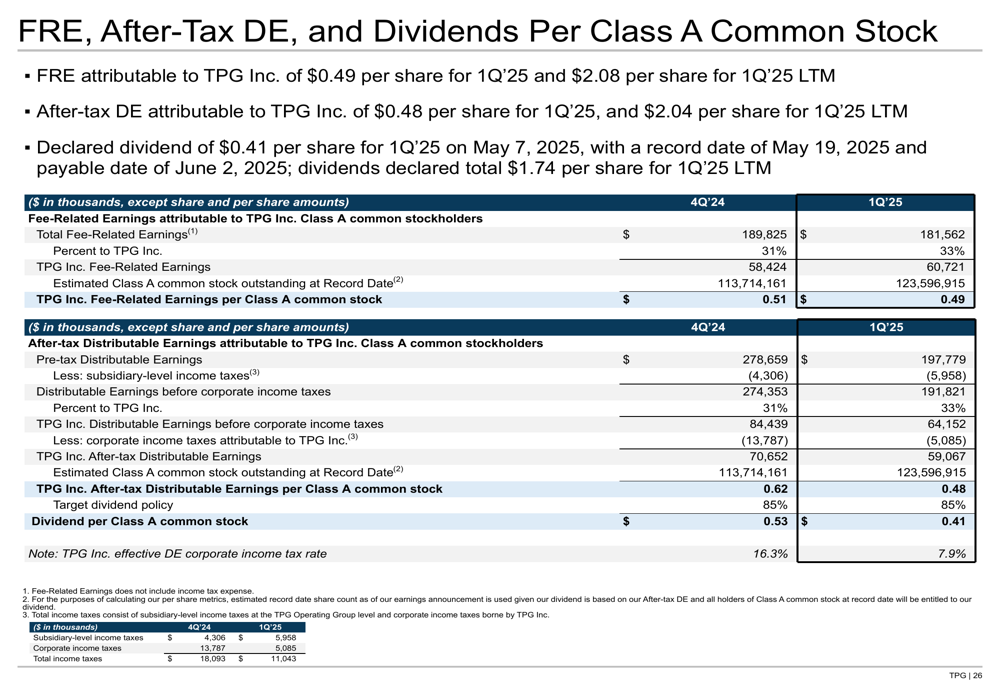

TPG’s after-tax distributable earnings of $187 million translated to $0.48 per share for Q1 2025, compared to $0.45 per share reported in Q3 2024. The company’s distributable earnings mix showed that fee-related earnings contributed 8% of pre-tax distributable earnings in Q1 2025, down from 32% in the previous quarter, reflecting the increased contribution from performance allocations.

The following chart illustrates TPG’s distributable earnings trend and composition:

Realized performance allocations, net, were $40 million in Q1 2025, primarily driven by the Capital platform (TPG VII and TPG VIII), Impact platform (Rise Climate I), and TPG AG Credit (MMDL IV). For the trailing twelve months, realized performance allocations reached $203 million across various platforms.

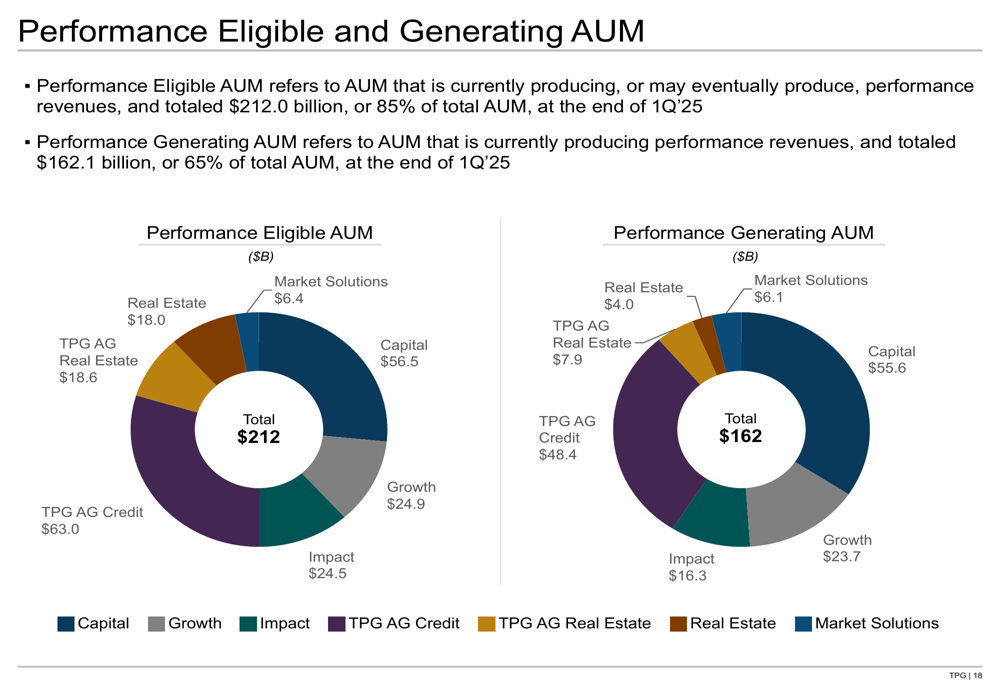

The company’s performance-eligible AUM, which refers to assets that are currently producing or may eventually produce performance revenues, totaled $212.0 billion, representing 85% of total AUM. Of this, $162.1 billion (65% of total AUM) was already generating performance revenues.

As illustrated in the following breakdown of performance-eligible and generating AUM:

Balance Sheet and Dividends

TPG declared a quarterly dividend of $0.41 per share of Class A common stock, payable on June 2, 2025, to shareholders of record as of May 19, 2025. This represents a slight increase from the $0.38 per share dividend announced in Q3 2024, reflecting the company’s commitment to returning capital to shareholders.

The following table shows TPG’s per-share metrics for fee-related earnings, after-tax distributable earnings, and dividends:

As of March 31, 2025, TPG reported cash and cash equivalents of $0.8 billion and total debt obligations of $1.5 billion. The increase in debt obligations included $180 million borrowed on the Senior Unsecured Revolving Credit Facility during Q1 2025. The company maintained $1.0 billion in undrawn capacity on its revolving credit facility, providing additional financial flexibility.

Strategic Initiatives

In a significant strategic move, TPG announced an agreement to acquire Peppertree Capital Management, a firm focused on wireless communications towers. This acquisition aligns with TPG’s continued expansion strategy, following its substantial growth in assets under management over the past year.

The company’s presentation emphasized its long-term investment approach, with approximately 72% of AUM and 71% of FAUM in perpetual or long-dated funds with a duration of 10 or more years. Additionally, about 69% of FAUM had a remaining lifespan of 5 or more years, providing visibility into the company’s future fee-earning potential.

Forward-Looking Statements

With $57 billion in dry powder, TPG is well-positioned to capitalize on investment opportunities across its diverse platforms. The company has invested approximately $33.8 billion during the last twelve months, demonstrating its active deployment strategy.

The potential fee-related revenue opportunity from AUM not yet earning fees and FAUM subject to step-up represents a significant growth driver for the company. As these assets begin generating fees, TPG could see meaningful increases in fee-related revenue and earnings in future quarters.

Building on the momentum from Q3 2024, when management indicated expectations for accelerated fee growth in 2025, the Q1 results show early signs of this acceleration with the 6% increase in fee-related revenue. However, the slight compression in fee-related earnings margin will be an area to watch in upcoming quarters as the company works toward its previously stated goal of approaching mid-40s FRE margin by the end of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.