ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

TransAlta Corp (TSX:TA) presented its second quarter 2025 results on August 1, showing strong earnings growth despite falling short on revenue expectations. The company's stock rose 2.52% following the presentation, closing at $17.09, as investors responded positively to the company's operational efficiency and strategic initiatives.

The Canadian power generator delivered an earnings per share (EPS) of $0.18, significantly exceeding analyst expectations of $0.0878, while revenue came in at $613 million, missing forecasts of $666.97 million. This mixed performance highlights TransAlta's ability to drive profitability through operational excellence and strategic hedging despite top-line challenges.

Quarterly Performance Highlights

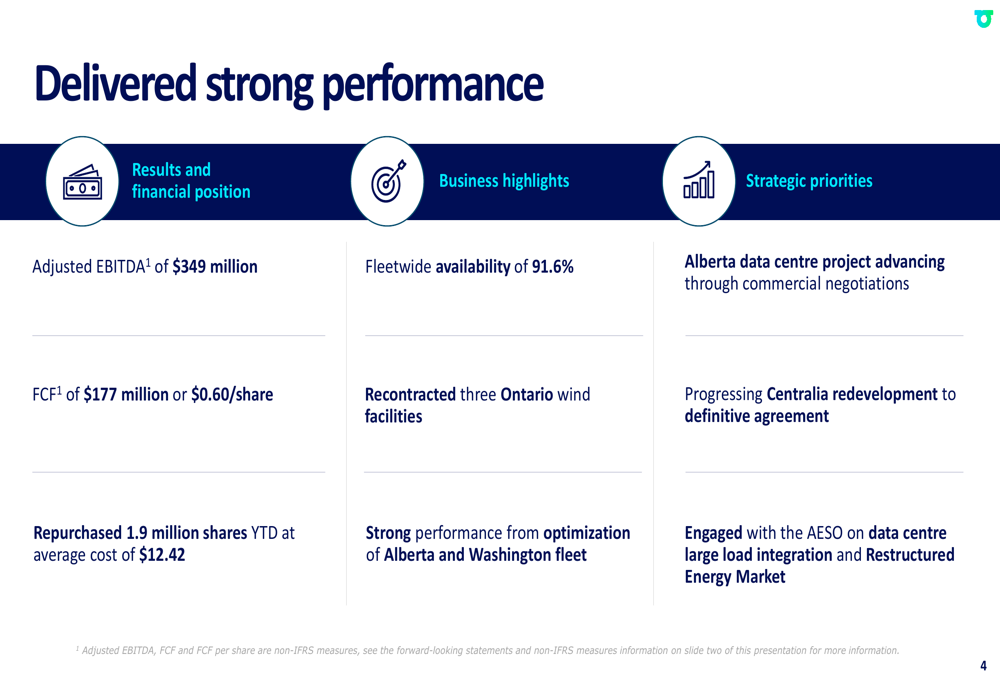

TransAlta reported Adjusted EBITDA of $349 million for Q2 2025, representing a 10.4% increase from $316 million in the same period last year. The company achieved a strong fleetwide availability of 91.6% and generated Free Cash Flow (FCF) of $177 million, or $0.60 per share.

As shown in the following comprehensive performance summary:

The company's strong results were driven by effective optimization of its Alberta and Washington fleet, strategic hedging that delivered premium pricing, and higher utilization of carbon offsets in Alberta. TransAlta also reported the repurchase of 1.9 million shares year-to-date at an average cost of $12.42, demonstrating confidence in its business model and commitment to shareholder returns.

Segment Performance Analysis

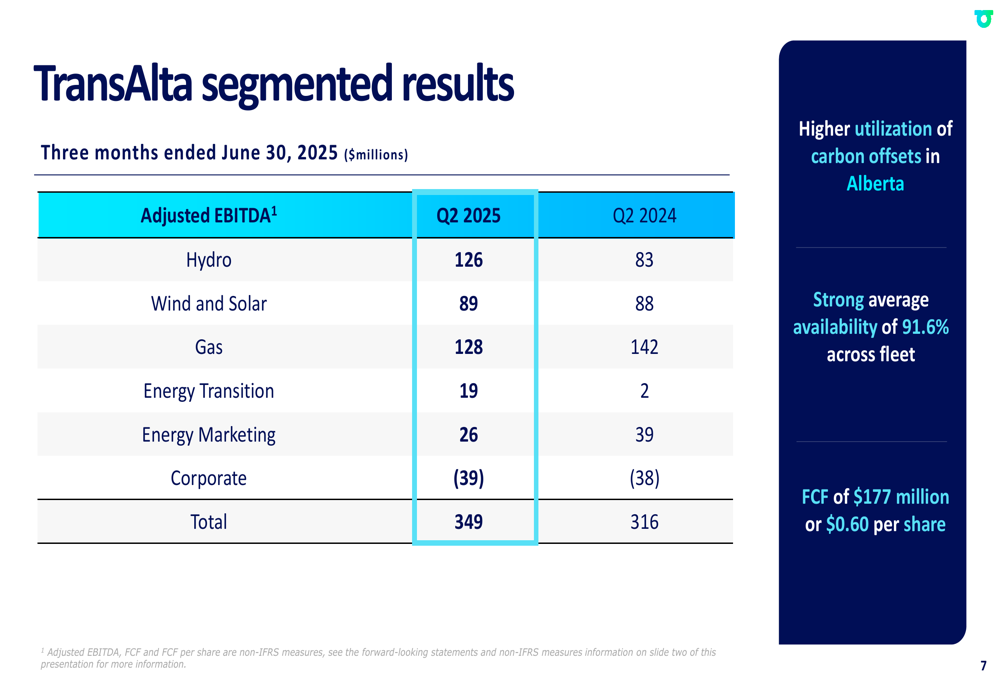

TransAlta's segmented results reveal varying performance across its diversified portfolio. The Hydro segment was the standout performer, with Adjusted EBITDA increasing 51.8% year-over-year to $126 million, while the Energy Transition segment grew dramatically from $2 million to $19 million. However, the Gas and Energy Marketing segments experienced declines.

The following breakdown illustrates the performance across all business segments:

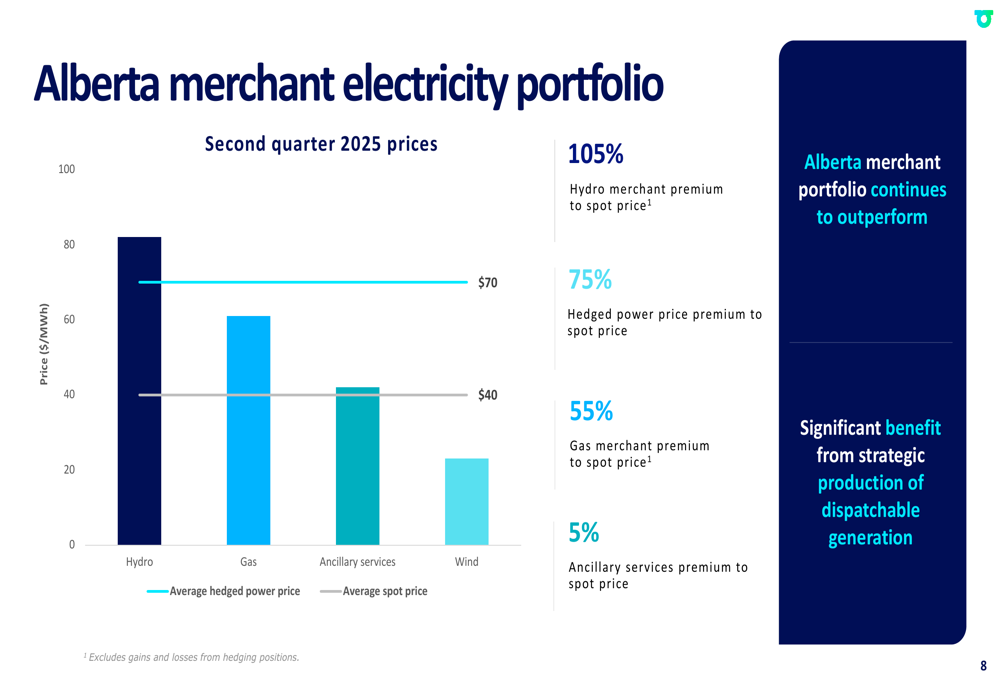

A key driver of TransAlta's performance was its strategic hedging in the Alberta merchant electricity market. The company's hedging strategy delivered significant premiums over spot prices, particularly in the Hydro segment where merchant prices exceeded spot prices by 105%.

The following chart demonstrates the effectiveness of TransAlta's hedging strategy across its portfolio:

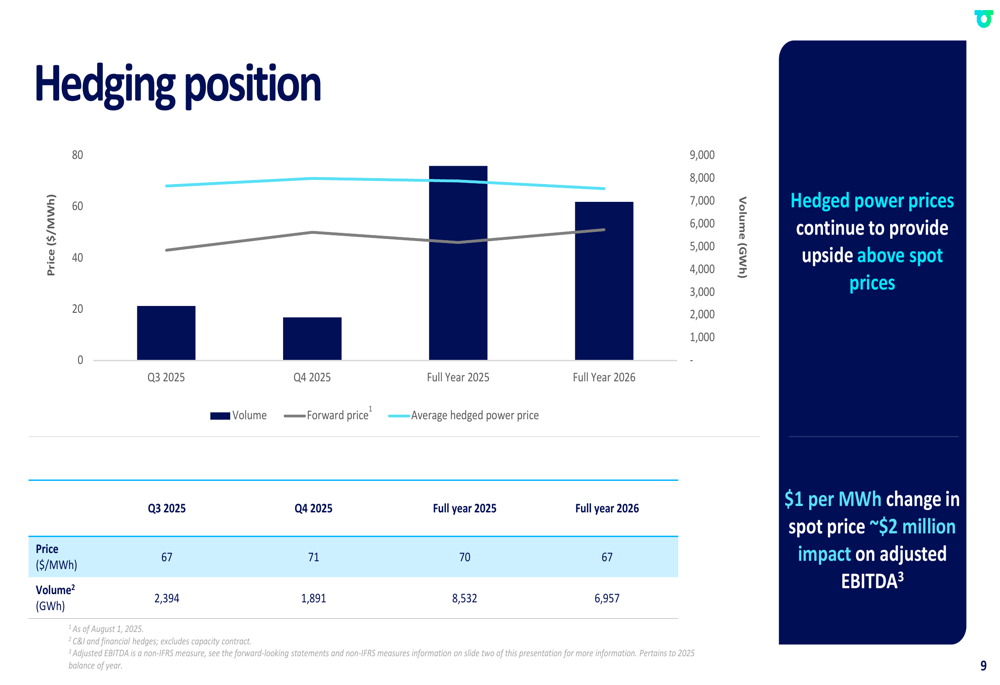

Looking ahead, TransAlta's hedging position shows relatively stable forward prices through 2026, with volumes gradually decreasing. The company noted that a $1 per MWh change in spot price would impact adjusted EBITDA by approximately $2 million.

Strategic Initiatives

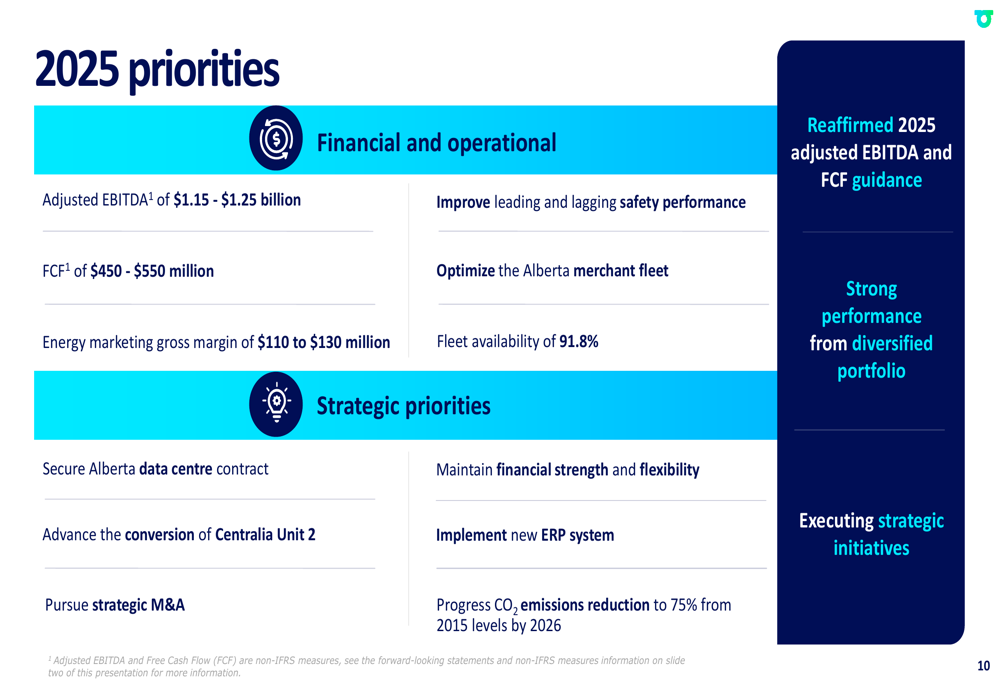

TransAlta is advancing several strategic initiatives to drive future growth, with particular focus on data center opportunities and legacy asset conversion. The company reported active commercial negotiations for its Alberta data center project, with the Alberta Electric System Operator (AESO) Demand Transmission Service timeline for contract execution expected by mid-September.

The company is also progressing with the conversion of its Centralia Unit 2, with a definitive agreement expected in the second half of 2025. This project would secure a long-term contract for 100% of capacity with opportunities for future expansion.

The following slide details these strategic initiatives:

CEO John Kousinioris expressed confidence in these projects during the earnings call, stating, "We delivered exceptional results during the second quarter," and highlighting the company's successful hedging strategy and asset optimization.

Forward Guidance & Outlook

TransAlta reaffirmed its 2025 guidance, projecting Adjusted EBITDA of $1.15-$1.25 billion and Free Cash Flow of $450-$550 million. The company's priorities are divided between financial/operational goals and strategic initiatives, with a continued focus on clean energy transition and carbon emissions reduction.

The following comprehensive overview outlines TransAlta's priorities for the remainder of 2025:

TransAlta's value proposition centers on being a safe and reliable operator with a diversified and increasingly contracted portfolio. The company positions itself as a clean electricity leader with high-potential legacy energy campuses and strong financial flexibility to support future growth.

The company faces several challenges, including revenue growth concerns following the current quarter's miss, market volatility affecting energy prices, regulatory changes impacting clean energy initiatives, and increasing competition in the data center and energy markets.

Despite these challenges, TransAlta's strong operational performance, effective hedging strategy, and strategic positioning in growth markets like data centers suggest the company is well-positioned to continue delivering value to shareholders while advancing its clean energy transition goals.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.