CVS Group shares surge over 10% after FY25 EBITDA beats estimates

Introduction & Market Context

Transat AT Inc. (TSX:TRZ) presented its third-quarter 2025 results on September 11, showing improved financial performance despite ongoing operational challenges. The Canadian leisure airline continues to navigate a shifting market landscape characterized by changing consumer behavior and competitive pressures.

The company’s stock closed at $3.22 on September 10, 2025, near its 52-week high of $3.25, suggesting investor optimism about the company’s recent financial improvements. This follows a challenging second quarter where the stock dropped 9.64% despite beating earnings expectations.

Quarterly Performance Highlights

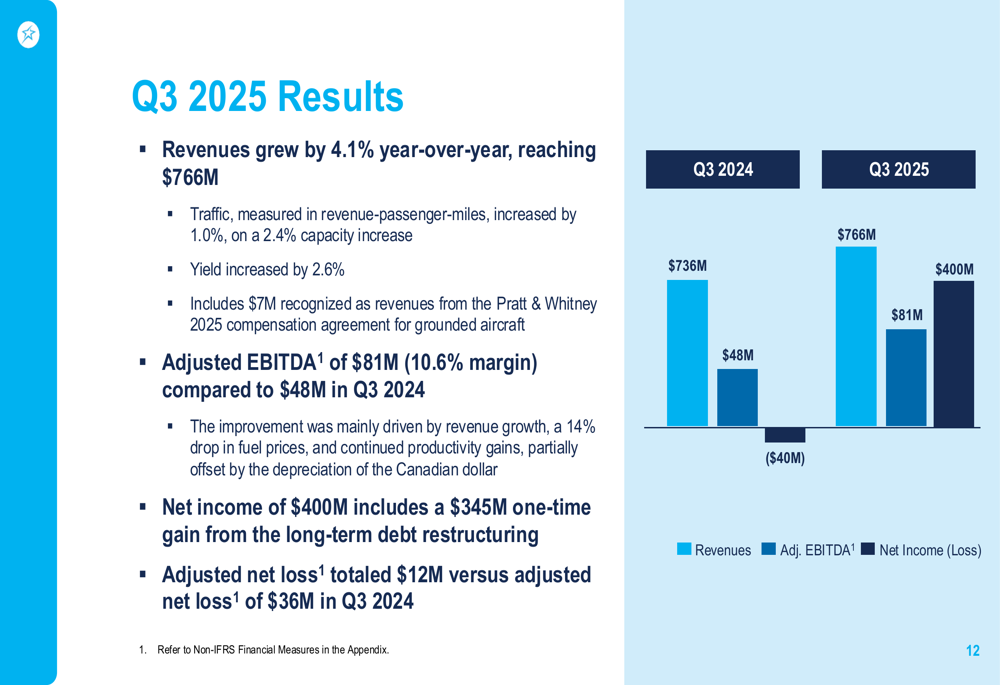

Transat reported revenue of $766 million for Q3 2025, representing a 4.1% increase year-over-year. The company achieved an adjusted EBITDA of $81 million with a 10.6% margin, significantly improving from $48 million in the same period last year.

Net income reached $400 million, though this figure includes a substantial one-time gain of $345 million from long-term debt restructuring. On an adjusted basis, the company posted a net loss of $12 million, considerably better than the $36 million adjusted net loss in Q3 2024.

As shown in the following financial results chart:

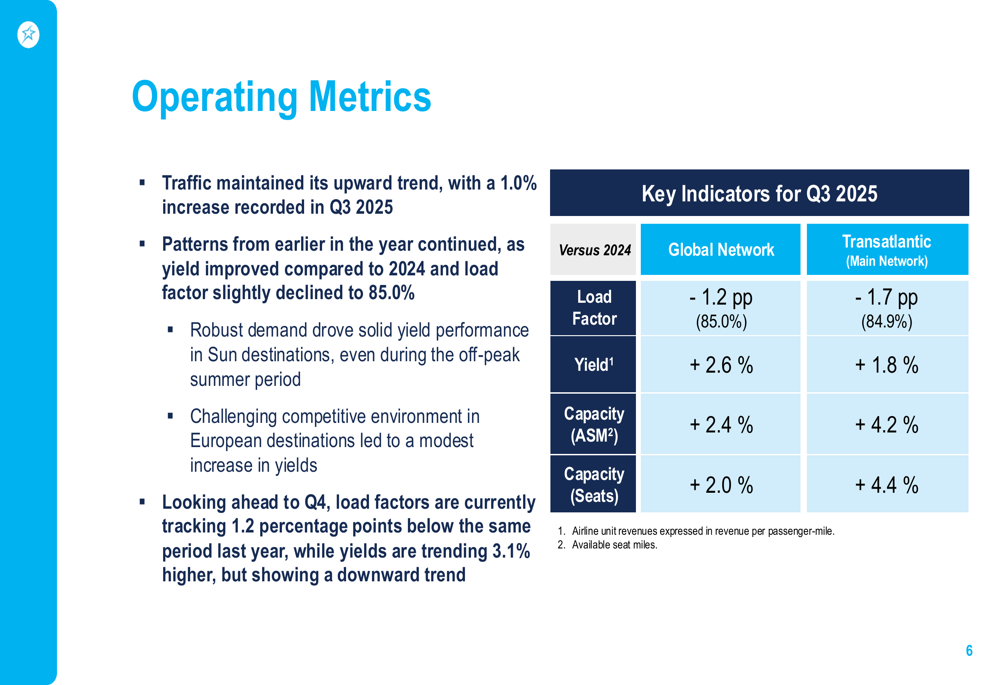

The company’s revenue growth was supported by a 2.6% increase in yield compared to 2024, despite a slight decline in load factor to 85.0% (a decrease of 1.2 percentage points). Capacity increased by 2.4% in available seat miles (ASM) and 2.0% in seats.

The operational metrics reveal the company’s performance across its network:

Debt Restructuring and Financial Position

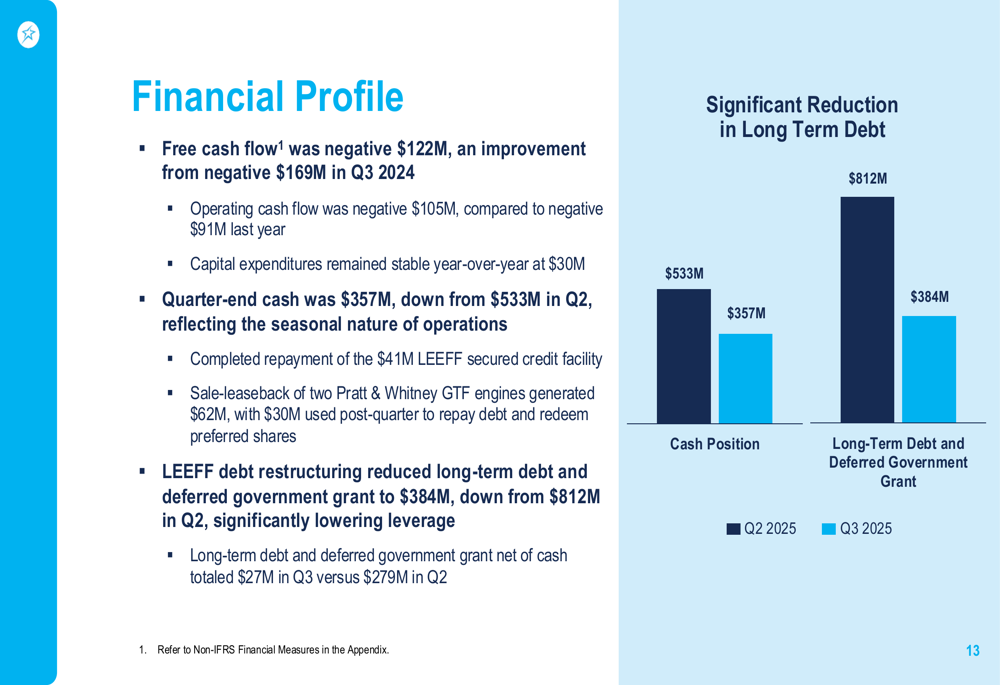

A major achievement during the quarter was the completion of the LEEFF debt restructuring, which reduced Transat’s total outstanding corporate debt balance to $384 million from $812 million in the previous quarter. Additionally, the company extended its Revolving Credit Facility maturity from November 2026 to November 2027.

The financial profile shows significant changes in both cash position and debt levels:

Free cash flow was negative $122 million, an improvement from negative $169 million in Q3 2024. The quarter-end cash position stood at $357 million, down from $533 million in Q2 2025, partly due to debt repayment.

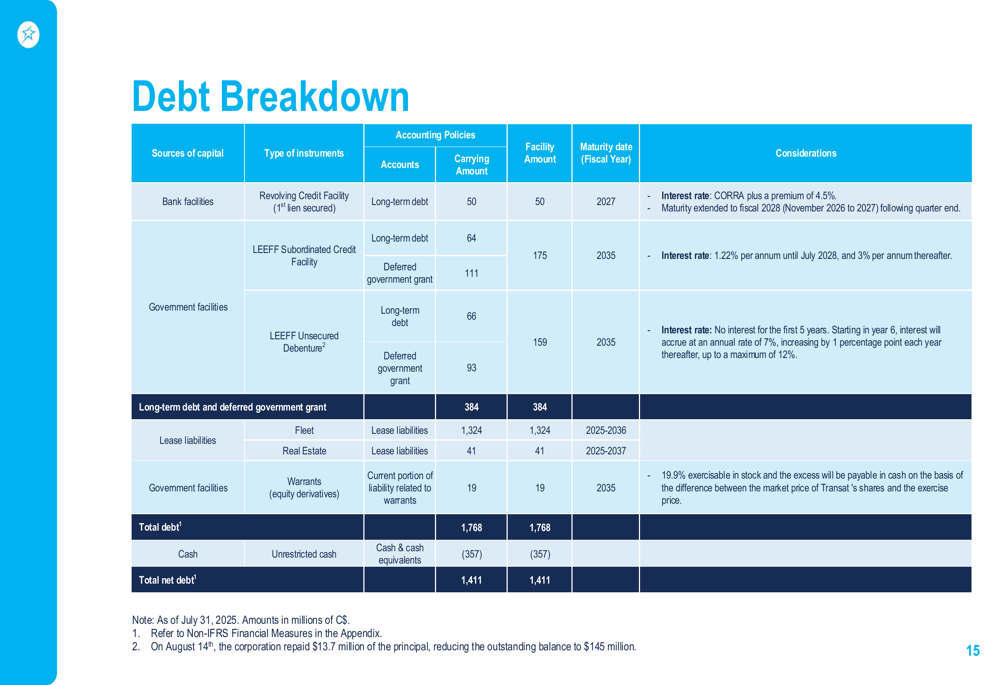

The company also completed a sale-leaseback transaction for two Pratt & Whitney GTF engines, generating $62 million that was used to further reduce debt. The detailed debt breakdown provides insight into the company’s current obligations:

Operational Challenges and Strategy

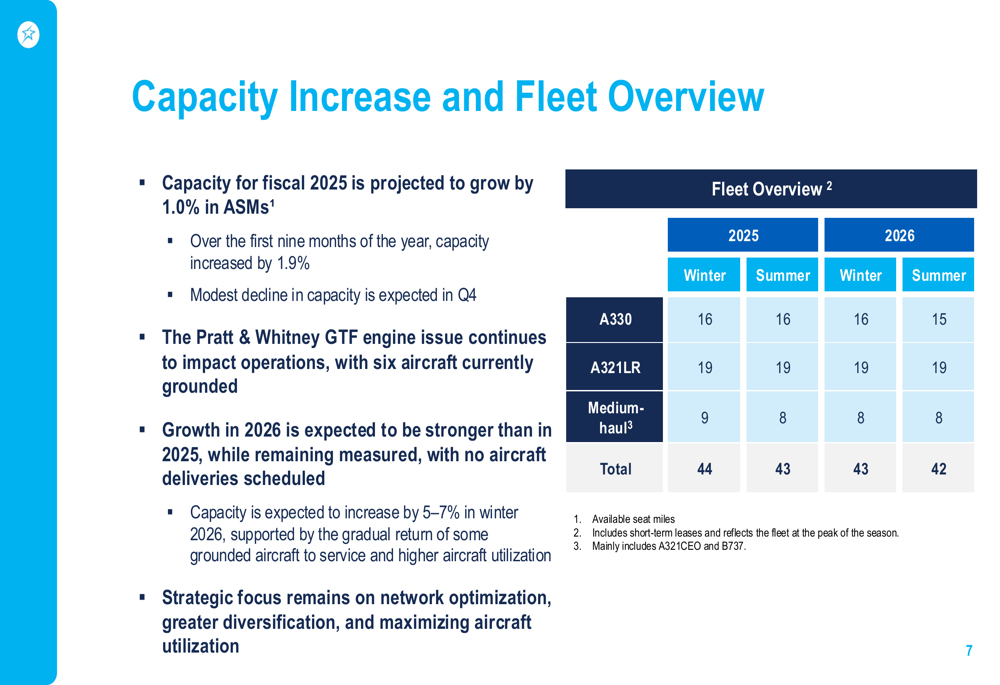

Transat continues to face challenges from the Pratt & Whitney GTF engine issues, with six aircraft currently grounded. This aligns with CEO Anik’s statement during the Q2 earnings call that "We expect the number of grounded aircraft to remain at six or seven for the remainder of the year."

Despite these challenges, the company is maintaining its strategic focus on network optimization, greater diversification, and maximizing aircraft utilization. Capacity for fiscal 2025 is projected to grow by 1.0% in ASMs, with stronger growth of 5-7% expected for winter 2026.

The fleet overview shows the company’s aircraft distribution:

The Elevation Program, launched one year ago, has reached its implementation target and is projected to generate $100 million in adjusted EBITDA by mid-2026. This aligns with information provided in the Q2 earnings call and represents a critical component of Transat’s turnaround strategy.

Forward-Looking Statements

Transat noted that a shift in market conditions is becoming apparent as economic slowdown begins to weigh on consumer behavior. Additionally, capacity re-deployment by other carriers is impacting the competitive environment, creating potential headwinds for the company.

Management emphasized that disciplined execution and continued rollout of the Elevation program remain key priorities, along with close monitoring of macroeconomic conditions. The company’s cautious outlook mirrors sentiments expressed in previous communications, where it anticipated soft bookings in Q4, especially in European markets.

The Q3 results demonstrate progress in Transat’s financial recovery, particularly through debt restructuring and operational improvements. However, the company faces ongoing challenges from aircraft groundings and changing market dynamics that could impact future performance. Investors will be watching closely to see if the Elevation Program delivers its promised benefits by mid-2026.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.